回顾2024年,受风光装机高增、电改进程加速、储能系统价格回落、顶层政策明确等多项驱动因素影响,储能项目招标/规划量持续增长,配储时长稳步提升,全球储能市场迎来高速发展期。

回顾2024年,受风光装机高增、电改进程加速、储能系统价格回落、顶层政策明确等多项驱动因素影响,储能项目招标/规划量持续增长,配储时长稳步提升,全球储能市场迎来高速发展期。According to TrendForce, the global newly installed capacity for energy storage is expected to reach 86GW/221GWh by 2025, with a year-on-year increase of 27%/36%, and an average storage duration of about 2.6 hours.

The Zhito Finance APP reported that TrendForce stated that with the acceleration of the global energy transition, energy storage has become the NEW FOCUS AUTO in the energy sector, and renewable energy targets in various regions may ensure the growth of global medium to long-term energy storage demand. TrendForce expects that by 2025, the global newly installed capacity for energy storage is expected to reach 86GW/221GWh, a year-on-year increase of 27%/36%, with an average storage duration of about 2.6 hours.

2025 Global Energy Storage Market Installed Demand Outlook.

Looking back at 2024, influenced by multiple driving factors such as the high increase in wind and solar installations, accelerated electricity reform processes, falling energy storage system prices, and clear top-level policies, the tender/planning volume of energy storage projects continued to grow, and the storage duration steadily increased, ushering in a period of rapid development for the global energy storage market.

Looking back at 2024, influenced by multiple driving factors such as the high increase in wind and solar installations, accelerated electricity reform processes, falling energy storage system prices, and clear top-level policies, the tender/planning volume of energy storage projects continued to grow, and the storage duration steadily increased, ushering in a period of rapid development for the global energy storage market.

According to data from TrendForce, from a total perspective, the newly installed capacity for global new energy storage increased rapidly from 11.3GWh in 2020 to 110GWh in 2023, with an average annual compound growth rate as high as 113%, showing a rapidly rising trend.

TrendForce expects that from 2024 to 2025, while the demand for installed energy storage will still maintain a relatively high growth trend, the average annual compound growth rate will slow significantly to 27%. Among them, the newly installed capacity for global energy storage in 2025 will reach about 86GW/221GWh, achieving a year-on-year increase of 27%/36%.

Global energy storage segmented market installed demand.

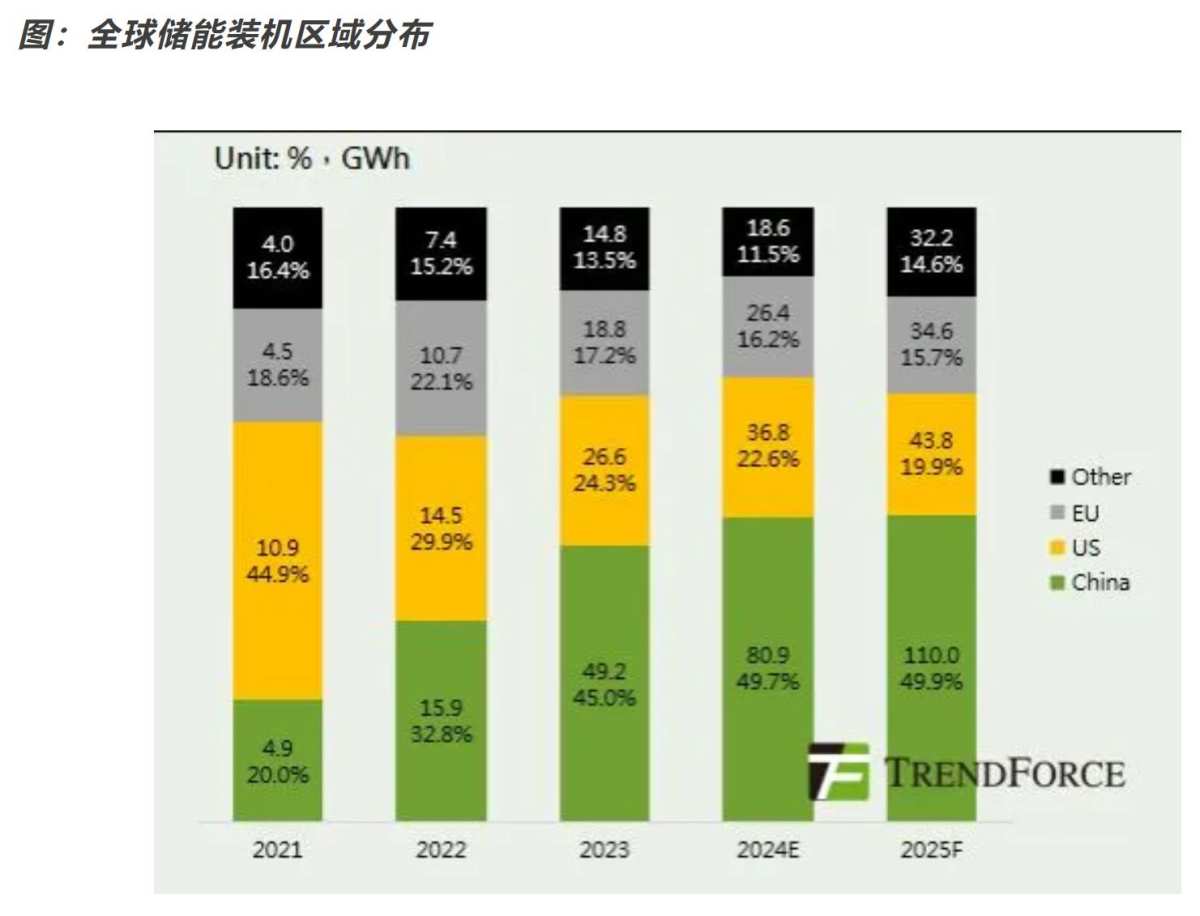

In the context of Energy transition, Global demand for energy storage is booming, with several countries and regions overseas releasing energy storage plans. From the market distribution perspective, TrendForce expects that the market pattern in key areas will remain unchanged, with China, Europe, and the USA still being the main markets, and the new installed capacity for energy storage in China, the USA, and Europe accounting for 85% of the global total, continuing to lead the growth in Global energy storage demand.

In China, it is estimated that in 2024/2025, the new installed capacity for new energy storage will be 81/110 GWh, with large-scale storage rapidly deploying and strong growth in industrial and commercial storage.

In the USA, it is estimated that in 2024/2025, the new installed capacity for new energy storage will be 37/44 GWh, with the majority still being large-scale storage.

In Europe, it is estimated that in 2024/2025, the new installed capacity for new energy storage will be 26/37 GWh, with a reduction in household storage demand due to some regions exiting subsidies, but large-scale storage is expected to see significant growth.

It is worth noting that in some Emerging Markets, driven by multiple factors such as Energy transition strategy, power shortages, and rising electricity prices, the demand for installed capacity is expected to accelerate. The Emerging Energy Storage market has shown bright performance, with the Middle East and Africa exhibiting the strongest growth. TrendForce estimates that in 2024/2025, the installed capacity for energy storage in the Middle East and Africa will be 2.8 GWh and 8.6 GWh respectively, with year-on-year growth of 43% and 24%.

Analysis of large-scale storage/household storage/industrial and commercial storage in different scenarios.

In the marketization process of the energy storage industry, the products in each sub-market exhibit certain differences, which significantly affect the market positioning, resource investment, product models, and development models of enterprises in the Industry Chain.

According to TrendForce Analyst, looking towards 2025, large storage will still be the main type of newly installed capacity globally, with a correction expected in residential storage in Europe, while demand for residential storage in Emerging Markets such as Asia, Africa, and Latin America is starting up.

Currently, large storage remains the main type of new energy installations globally. TrendForce expects global large storage installations to reach 72GW/188GWh in 2025, accounting for about 84%/85% of new energy storage installations. China and the USA are the major markets for large storage, and Europe and the Middle East markets are also gradually starting. Domestically, the business model for large storage is being gradually perfected through mandatory storage policies and electrical utilities market construction, while abroad it is being driven by subsidies and market returns, leading to continuous increases in installations.

Residential storage is the second largest installation type, with market demand expected to slightly decrease in 2025 compared to 2024, showing differentiated performance across regions. In Europe, under the backdrop of declining electricity and gas prices, the urgency for installations is weakened, and growth is likely to adjust. In the USA and Emerging Markets in Asia, Africa, and Latin America, growth is anticipated due to high electricity prices and power shortages.

Industrial and commercial energy storage installations are relatively small in scale. Domestically, the installation is rapidly increasing due to a time-of-use electricity pricing mechanism that encourages industrial and commercial storage. Overseas, due to relatively low electricity prices in Europe and the USA and insufficient incentive mechanisms, the industrial and commercial storage market is yet to be opened, leaving ample potential for future development.

With the rapid development of the industry, the scale of the energy storage market is rapidly expanding, and the diversification of technology and the decline in costs are seen as key factors driving market development. Furthermore, current market competition is intensifying, and Chinese companies face different opportunities and challenges in various markets, requiring continuous enhancement of their competitiveness to secure a larger share in the global energy storage market.