展品99.2

Accretive二疊紀交易2024年1月4日

展品99.2

Accretive二疊紀交易2024年1月4日

Disclaimer Forward-Looking Statements This presentation and the oral statements made in connection therewith relate to a proposed business combination transaction between APA and Callon and contain forward-looking statements within the meaning of the federal securities laws, including Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements relate to future events and anticipated results of operations, business strategies, the anticipated benefits of the proposed transaction, the anticipated impact of the proposed transaction on the combined companys business and future financial and operating results, the expected amount and timing of synergies from the proposed transaction, the anticipated closing date for the proposed transaction, and other aspects of our operations or operating results. Words and phrases such as anticipate, estimate, believe, budget, continue, could, intend, may, might, plan, potential, possibly, predict, seek, should, will, would, expect, objective, projection, prospect, forecast, goal, guidance, outlook, effort, target, and other similar words can be used to identify forward-looking statements. However, the absence of these words does not mean that the statements are not forward-looking. All such forward-looking statements are based upon current plans, estimates, expectations, and ambitions that are subject to risks, uncertainties, and assumptions, many of which are beyond the control of APA and Callon, that could cause actual results to differ materially from those expressed or forecast in such forward-looking statements. The following important factors and uncertainties, among others, could cause actual results or events to differ materially from those described in these forward-looking statements: the risk that the approval under the Hart-Scott-Rodino Antitrust Improvements Act of 1976 is not obtained or is obtained subject to conditions that are not anticipated by APA and Callon; uncertainties as to whether the potential transaction will be consummated on the expected time period or at all, or if consummated, will achieve its anticipated benefits and projected synergies within the expected time period or at all; APAs ability to integrate Callons operations in a successful manner and in the expected time period; the occurrence of any event, change, or other circumstance that could give rise to the termination of the transaction, including receipt a competing acquisition proposal; risks that the anticipated tax treatment of the potential transaction is not obtained; unforeseen or unknown liabilities; customer, shareholder, regulatory, and other stakeholder approvals and support; unexpected future capital expenditures; potential litigation relating to the potential transaction that could be instituted against APA and Callon or their respective directors; the possibility that the transaction may be more expensive to complete than anticipated, including as a result of unexpected factors or events; the effect of the announcement, pendency, or completion of the potential transaction on the parties business relationships and business generally; risks that the potential transaction disrupts current plans and operations of APA or Callon and their respective management teams and potential difficulties in Callons ability to retain employees as a result of the transaction; negative effects of this announcement and the pendency or completion of the proposed acquisition on the market price of APAs or Callons common stock and/or operating results; rating agency actions and APAs and Callons ability to access short- and long-term debt markets on a timely and affordable basis; various events that could disrupt operations, including severe weather, such as droughts, floods, avalanches, and earthquakes, and cybersecurity attacks, as well as security threats and governmental response to them, and technological changes; labor disputes; changes in labor costs and labor difficulties; the effects of industry, market, economic, political, or regulatory conditions outside of APAs or Callons control; legislative, regulatory, and economic developments targeting public companies in the oil and gas industry; and the risks described in APAs and Callons respective periodic and other filings with the U.S. Securities and Exchange Commission (SEC), including their most recent Quarterly Reports on Form 10-Q和年度報告(Form 10-K)。前瞻性陳述代表管理層對S目前的期望,具有內在的不確定性,僅在本文發佈之日作出。除法律另有規定外,APA和Callon均不承擔或承擔任何義務更新任何前瞻性陳述,無論是作為新信息的結果,還是反映後續事件或情況或其他情況。投資者注意:美國證券交易委員會允許石油和天然氣公司在提交給美國證券交易委員會的文件中只披露已探明的、可能的和可能的儲量,這些儲量符合美國證券交易委員會S對此類術語的定義。本演示文稿和與此相關的口頭陳述可以使用某些術語, 例如資源、潛在資源、潛在資源、估計淨儲量、超可採儲量、可採儲量以及美國證券交易委員會準則嚴格禁止石油和天然氣公司包括在提交給美國證券交易委員會的文件中的其他類似術語。這些條款沒有考慮資源回收的確定性,資源回收的確定性取決於勘探成功、鑽井通道的技術改進、商業和其他因素,因此, 並不表明預期的未來資源回收,因此不應依賴。敬請投資者慎重考慮本公司在截至2022年12月31日的10-K年報中披露的S年報和在截至2022年12月31日的財年中披露的S年報。《美國醫學會S年度報告》的《10-K表》可在美國醫學會S網站免費索取,網址為:https://investor.apacorp.com.《S年度報告10-K表》可在S網站免費索取,網址為:https://callon.com/investors.您也可以通過以下方式從美國證券交易委員會獲取這些報告:1-800-美國證券交易委員會-0330 或從美國證券交易委員會和S網站www.sec.gov下載。A P A C O R P O R A T I O N 2

免責聲明(續)非公認會計原則財務計量本報告

包括不符合公認會計原則(GAAP)編制的財務信息。淨債務和調整後的EBITDAX是非GAAP衡量標準。讀者除應考慮按照公認會計原則編制的財務信息外,還應考慮這種非公認會計原則信息。有關與最直接可比的公認會計準則財務指標的對賬,請參閲美國會計準則協會S網站https://investor.apacorp.com和凱龍S網站https://callon.com/investors.上發佈的公司季度業績本演示文稿和與此相關的口頭陳述不打算也不應構成買賣要約或徵求買賣任何證券的要約,或徵求任何投票或批准,也不得在任何司法管轄區進行任何證券銷售,在該司法管轄區內,此類要約、招攬或出售在根據任何此類司法管轄區的證券法註冊或資格之前是非法的。除非招股説明書符合修訂後的《1933年證券法》第10節的要求,否則不得發行證券。關於這項合併的更多信息以及在哪裏可以找到它與擬議的交易有關,APA打算以S-4表格的形式向美國證券交易委員會提交一份註冊説明書,其中將包括APA和卡隆的聯合委託書,這也構成了APA普通股的招股説明書。APA和CALLON還可以向美國證券交易委員會提交有關擬議交易的其他相關文件。本文檔不能替代聯合委託書/招股説明書或註冊説明書或美國運通或凱龍集團可能向美國證券交易委員會提交的任何其他文件。最終的聯合委託書/招股説明書(如果可用)將郵寄給APA和Callon的股東。我們敦促投資者和證券持有人在獲得註冊聲明、聯合委託書/招股説明書以及可能向美國證券交易委員會提交的任何其他相關文件以及對這些文件的任何修訂或補充後,仔細閲讀它們的全部內容,因為它們包含或將包含有關擬議交易的重要信息。

投資者和證券持有人將能夠免費獲得註冊聲明和聯合委託書/招股説明書(如果可用)和其他包含有關友邦保險、凱龍和擬議交易的重要信息的文件的副本。一旦這些文件通過美國證券交易委員會維護的網站提交給美國證券交易委員會,網址為http://www.sec.gov.APA提交給美國證券交易委員會的文件副本將在APA S網站上免費獲取,網址為:

https://investor.apacorp.com.凱龍提交給美國證券交易委員會的文件副本將在凱龍S的網站上免費提供,網址為https://callon.com/investors.徵集APA、Callon的參與者以及他們各自的董事、高管以及管理層和員工的其他成員可能被視為就建議的交易徵集委託書的參與者。APA董事和高管的信息,包括對他們直接或間接利益的描述,通過持有證券或其他方式,在APA S 2023年年度股東大會委託書中闡述,該聲明於2023年4月11日提交給美國證券交易委員會,以及

APA全球S年度報告,截至2022年12月31日的財政年度,它於2023年2月23日提交給美國證券交易委員會。有關凱龍董事和高管的信息,包括對他們通過持有證券或其他方式擁有的直接或間接利益的描述,已在凱龍S 2023年股東大會委託書中闡述,該委託書於2023年3月13日提交給美國證券交易委員會,以及

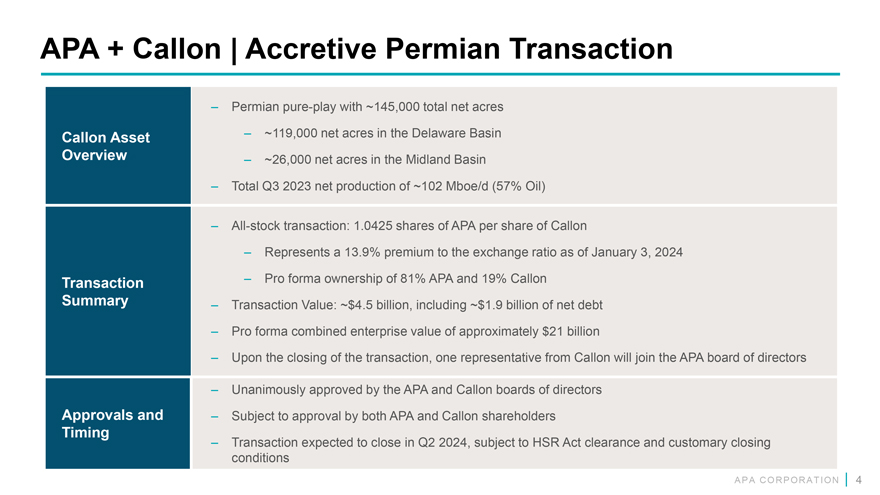

APA+Callon|增值二疊紀交易Callon總淨英畝約145,000英畝Callon 資產淨英畝~特拉華盆地淨英畝概述~米德蘭盆地淨英畝~26,000英畝2023年第三季度總淨產量約102 Mboe/d(57%石油)全股票交易:Callon每股1.0425股AAPA,較截至2024年1月3日的換股比例溢價13.9%。交易金額:約45億美元,其中包括約19億美元的淨債務,其中包括約19億美元的淨債務。交易完成後,Callon的一名代表將加入AAPA董事會,獲得AAPA和Callon董事會的一致批准,並有待APA和Callon股東的批准。交易預計將於2024年第二季度完成,受《高鐵法案》許可和慣例成交條件的制約

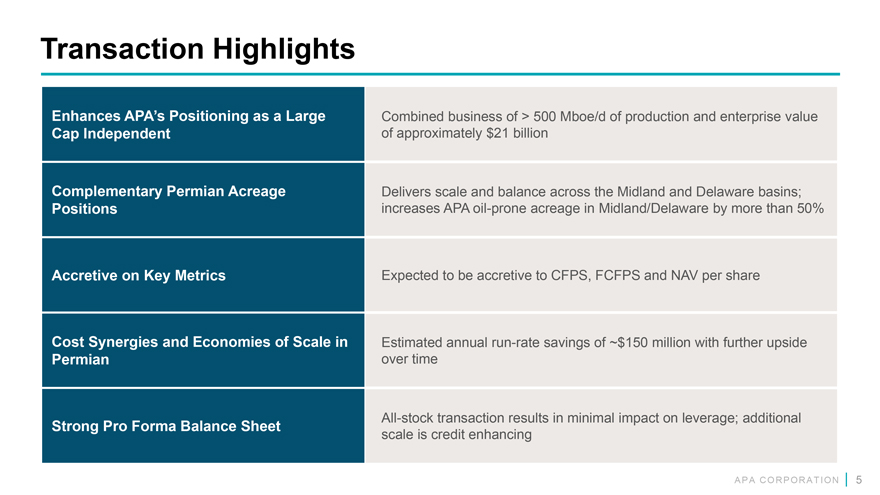

交易亮點提升APA作為一家大型聯合企業的定位, 日產量和企業價值超過5億桶油當量,獨立於約210億美元的上限補充二疊紀面積在米德蘭和特拉華盆地實現規模和平衡;增加APA的地位 米德蘭/特拉華州的易產油麪積增加了50%以上 預計將增加CFPS、FCFPS和每股NAV成本協同效應和規模經濟 預計每年可節省約1.5億美元的運行成本,並隨着時間的推移進一步上升所有股票交易對槓桿的影響最小;額外的 強勁的備考資產負債表規模是信用增強A P A C O R P O R A T I O N 5

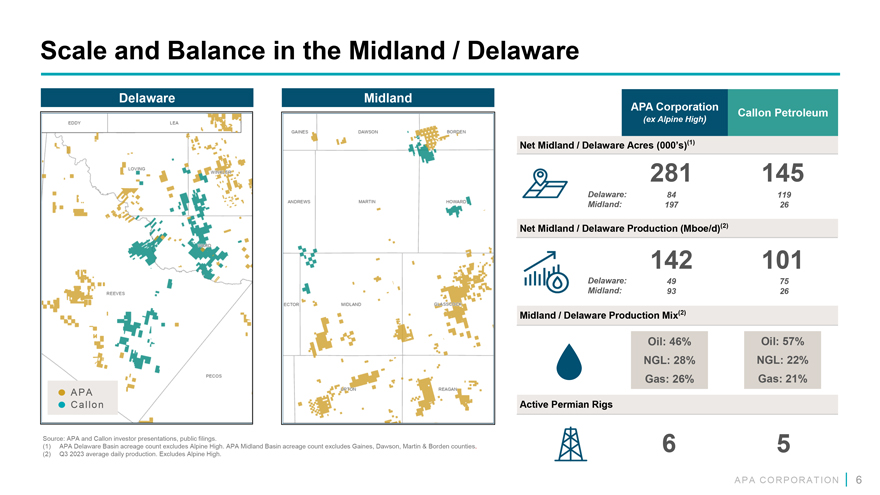

Midland / Delaware的規模和平衡Delaware Midland APA Corporation Callon Petroleum(ex Alpine High) 淨Midland / Delaware英畝數(000 s)(1)281 145 Delaware:84 119 Midland:197 26淨Midland / Delaware產量(Mboe/d)(2)142 101 Delaware:49 75 Midland:93 26 Midland / Delaware生產組合(2)石油:46%石油:57% NGL:28% NGL:22%天然氣: 26%天然氣:21% APA Ca l l o n Active Permian Rigs來源:APA和Callon投資者介紹,公開文件。(1)APA特拉華盆地面積計數不包括阿爾卑斯山高。APA米德蘭盆地面積計數不包括蓋恩斯,道森,馬丁和博登縣。6 5(2)2023年第三季度平均每日產量。不包括阿爾卑斯高中A P A C O R P O R A T I O N 6

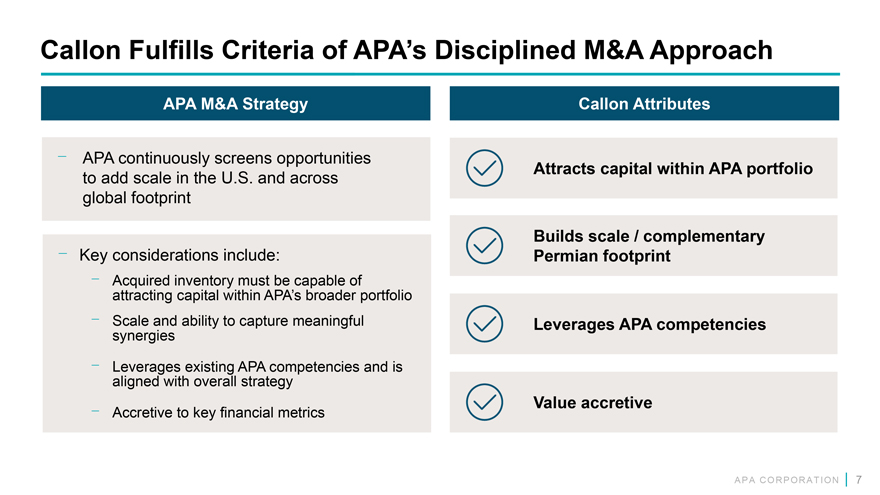

Callon符合APA的標準併購方法APA併購戰略Callon屬性APA 不斷篩選機會在APA投資組合中吸引資本,以增加在美國和全球的規模建立規模/互補性關鍵考慮因素包括:二疊紀足跡收購的庫存必須能夠在APA更廣泛的投資組合中吸引資本 規模和能力,以獲得有意義的Leadership APA能力協同效應Leadership現有APA能力,並與整體戰略保持一致增值對關鍵財務指標的增值A P A C O R P O R A T I O N 7

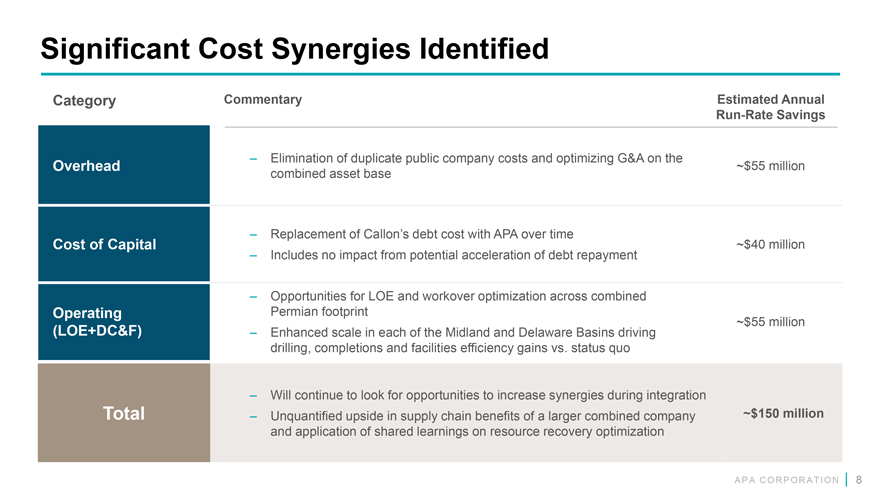

確定的重大成本協同效應類別註釋估計年度 運行率節省消除重複的上市公司成本並優化管理費用的G&A約5500萬美元的合併資產基礎在 時間內用APA替換Callon的債務成本資本成本約4000萬美元不包括潛在的加速債務償還的影響在合併運營中LOE和修井優化的機會 二疊紀足跡~ 5500萬美元 (LOE+DC&F)米德蘭盆地和特拉華盆地的規模擴大,推動鑽井、完井和設施效率提高,而不是維持現狀將繼續尋找機會,在整合過程中增加協同效應 總計合併後的大型公司在供應鏈方面的優勢無法量化約為1.5億美元,並將共享的經驗應用於資源回收優化A P A C O R P O R A T I O N 8

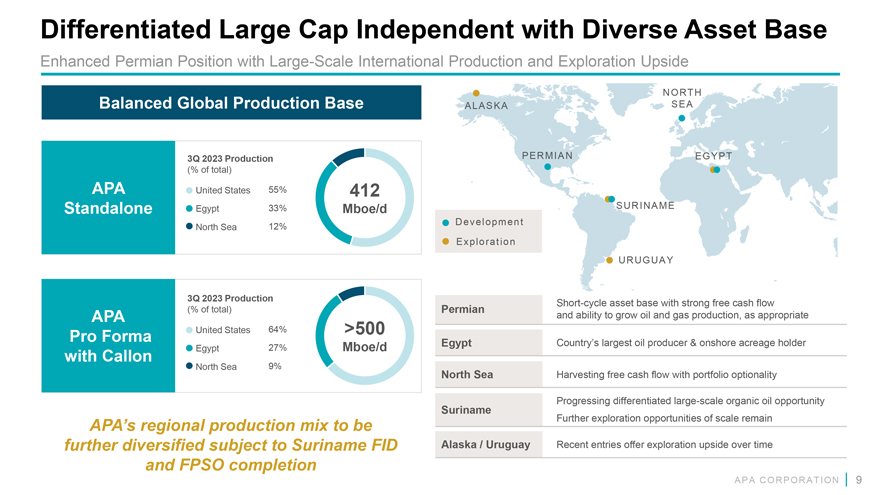

差異化的大型獨立公司,擁有多樣化的資產基礎,增強了二疊紀的地位,擁有大規模的國際生產和勘探優勢,沒有RT H平衡的全球生產基地A L A S K A S E A 2023年第3季度生產P E RM I A N G Y P T(佔總數的百分比)APA United States 55% 412 Standalone Egypt 33% Mboe/d S URI NA M E De ve l o p m e n t North Sea 12% E xp l o r a t i o n URUG UA Y 3Q 2023 Production Short-擁有強大自由現金流的週期資產基礎(佔總資產的百分比)二疊紀APA和適當增加石油和天然氣產量的能力備考美國64% >500埃及 該國最大的石油生產國和陸上面積持有者埃及27% Mboe/d與Callon北海9%通過投資組合選擇性收穫自由現金流北海蘇裏南不斷髮展的差異化大型-大規模有機油機會 APA的區域生產組合將進一步擴大勘探機會的規模,但仍將進一步多樣化,這取決於蘇裏南FID阿拉斯加/烏拉圭最近的項目隨着時間的推移和FPSO的完工而提供勘探優勢A P A C O R P O R A T I O N 9

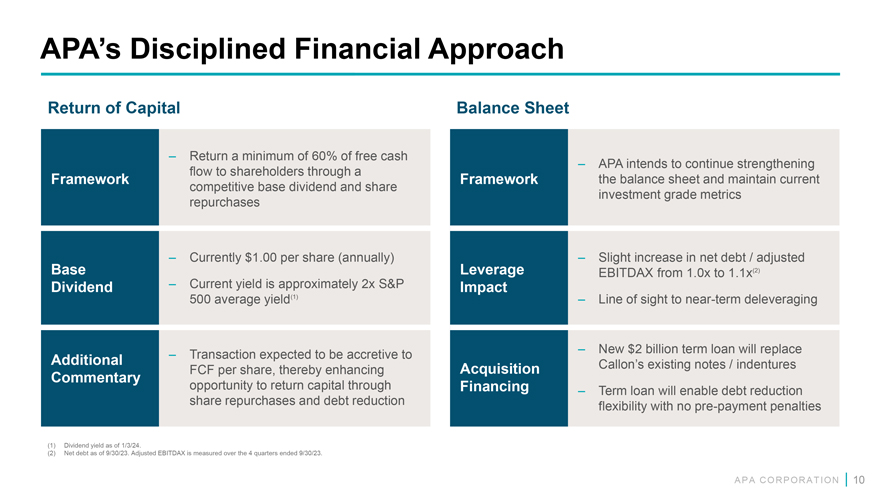

APA的固定財務方法資本回報資產負債表回報至少60%的 自由現金APA打算通過框架資產負債表繼續加強對股東的流動,並保持當前具有競爭力的基本股息和股票投資級別指標回購目前每股1. 00美元(每年)淨債務/調整後基本槓桿率EBITDAX從1. 0倍略微增加到1. 1倍(2)股息當前收益率約為標準普爾500影響平均收益率的2倍(1)視線到近期去槓桿化 交易預計將增加新的20億美元定期貸款將取代額外的Callon現有票據/契約每股FCF,從而提高收購評論通過融資回報資本的機會 定期貸款將實現債務減少股票回購和債務減少靈活性, 提前支付罰款(1)截至2024年1月3日的股息收益率。(2)截至2023年9月30日的淨債務。調整後的EBITDAX 是在截至2023年9月30日的4個季度內進行測量的。A P A C O R P O R A T I O N

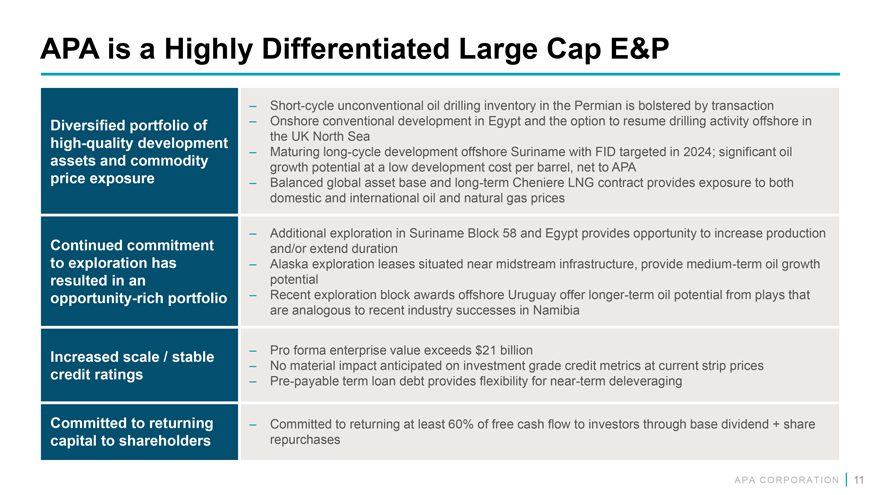

APA是一個高度差異化的大盤E&P短週期非常規石油鑽探庫存 二疊系受到埃及陸上常規開發的交易多元化組合以及在英國北海恢復近海鑽探活動的選項的支持 蘇裏南近海高質量開發和成熟的長週期開發 FID目標是2024年;巨大的石油資產和大宗商品增長潛力,每桶低開發成本,對APA價格的淨敞口,平衡的全球資產基礎和長期Cheniere LNG合同提供了對國內和國際石油和天然氣價格的敞口 蘇裏南第58號區塊和埃及的額外勘探提供了增加產量和/或延長勘探持續時間的機會 阿拉斯加勘探租約位於中游基礎設施附近,提供中期石油增長帶來了潛在的機會豐富的投資組合烏拉圭近海勘探區塊獎勵提供了與納米比亞最近的行業成功類似的較長期石油潛力 形式企業價值超過210億美元擴大規模/穩定增長按當前帶鋼價格計算,預計不會對投資級信用指標產生實質性影響信用評級 評級預付定期貸款債務為近期去槓桿化提供了靈活性承諾回報承諾通過基本股息 +股本向股東回購A P A C R P O R A T I O N 11向投資者返還至少60%的自由現金流

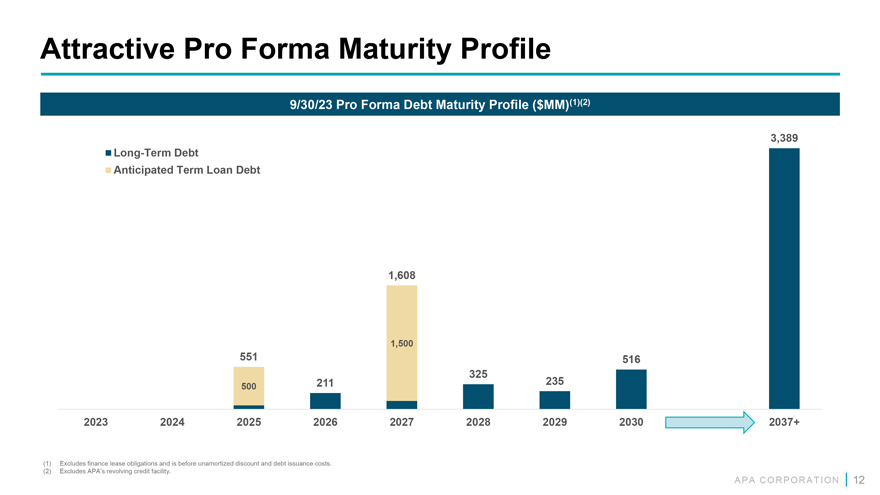

有吸引力的備考到期日概況23年9月30日備考債務到期日概況(百萬美元)(1)(2)3,389長期債務 預期定期貸款債務1,608 1,500 551 516 325 211 235 500 2023 2024 2025 2026 2027 2028 2029 2030 2020 20202 2037+(1)不包括融資租賃承擔,且未計未攤銷貼現及債務發行成本。(2)不包括APA的循環信用貸款。A P A C O R P O R A T I O N

apacorp.com