美國

證券交易 委員會

華盛頓特區20549

形式

日終了的財政年度

或

過渡時期 從__

委員會文件號:

(註冊人的確切名稱 如其章程中規定)

| (州或其他司法管轄區 成立或組織) | (國稅局僱主 識別號) |

| (主要行政辦公室地址) | (Zip代碼) |

註冊人的電話號碼,包括

地區代碼:

根據第12(b)條登記的證券 該法案的:

| 每個班級的標題 | 交易符號 | 註冊的每個交易所的名稱 | ||

根據該法第12(g)條登記的證券: 沒有一

如果註冊人是知名經驗豐富的,則通過勾選標記進行驗證

發行人,定義見《證券法》第405條。是的

如果不要求註冊人提交報告,請勾選標記

根據《交易法》第13條或第15(d)條。是的

通過檢查註冊人(1)是否已提交所有

1934年《證券交易法》第13條或第15(d)條要求的前12個月(或

註冊人被要求提交此類報告的較短期限),以及(2)已遵守此類提交要求

在過去的90天裏。

用複選標記表示註冊人是否已以電子方式提交

根據S-T規則第405條(本章第232.405節),在

在12個月之前(或註冊人被要求提交此類檔案的較短期限)。

通過勾選註冊人是否是大型加速器 歸檔者、加速歸檔者、非加速歸檔者、小型報告公司或新興成長型公司。查看定義 「大型加速文件人」、「加速文件人」、「小型報告公司」和“新興 《交易法》第120亿.2條中的成長型公司。

| 大型加速文件夾 | ☐ | 加速編報公司 | ☐ |

| ☒ | 小型上市公司 | ||

| 新興成長型公司 |

項目2.性能

項目3.法律訴訟

第二部分

項目6. [保留]

項目7.管理層對財務狀況和運營結果的討論和分析

項目8.財務報表和補充數據

項目9A.控制和程序

項目90亿。其他信息

項目9 C。關於阻止檢查的外國司法管轄區的披露

第三部分

項目10.董事、執行人員和企業治理

i

與以下任何情況相關的處罰和市場退出 產品候選出現意想不到的問題,以及未能遵守標籤和其他限制;

●

總的經濟狀況,我們目前的低庫存 價格和其他因素影響我們的運營,我們業務的連續性,包括我們的臨床前和臨床試驗,以及我們的 籌集額外資本的能力;

●

與持續監管合規相關的費用 義務和成功的持續監管審查;

| ● | 市場對我們候選產品的接受度和能力 確定或發現其他候選產品; |

| ● | 我們獲得特定噬菌體高滴度的能力 臨床前和臨床試驗所需的雞尾酒; |

| ● | 特殊原材料的可用性和全球 供應鏈挑戰; |

| ● | 我們的候選產品展示的能力 藥品必須具備安全性和有效性,或者生物製品必須具有安全性、純度和效力而不會產生不良影響; | |

| ● | 預期未來高級臨床試驗的成功 我們的候選產品; |

| ● | 我們有能力獲得所需的監管批准; |

| ● | 在爲我們的製造工藝開發方面的延遲 候選產品; |

| ● | 來自類似技術、產品的競爭 比我們的候選產品或在我們的產品之前獲得市場批准的產品更有效、更安全或更實惠 候選人; |

| ● | 不利定價法規的影響,第三方 報銷做法或醫療改革倡議,以提高我們銷售候選產品或療法的盈利能力; | |

| ● | 保護我們的知識產權和 與第三方遵守當前和未來許可證的條款和條件; |

| ● | 侵犯知識產權的行爲 第三人和受讓職務發明權的報酬或者使用費請求權; |

ii

| ● | 我們獲得、授權或使用專有技術的能力 第三方擁有我們的產品候選或未來開發候選所必需的權利; |

| ● | 關於人工合成的倫理、法律和社會問題 可能會對我們的候選產品的市場接受度產生不利影響的生物和基因工程; |

| ● | 依賴第三方合作者; |

| ● | 我們吸引和留住關鍵員工或 執行與員工簽訂的競業禁止協議條款; |

| ● | 不遵守適用的法律和法規 藥品生產合規性以外的; |

| ● | 潛在的安全漏洞,包括網絡安全 事件;以及 |

| ● | 本報告這一節討論的其他因素 標題爲「風險因素」,從第28頁開始。 |

| 前瞻性陳述受制於已知 以及未知的風險和不確定性,並基於我們管理層可能不準確的假設,這些假設可能會導致實際 結果與前瞻性陳述中預期或暗示的結果大不相同。雖然這些陳述是基於 截至本年度報告提交之日我們可獲得的信息,儘管我們認爲這些信息構成合理的基礎 對於此類聲明,此類信息可能是有限的或不完整的,我們的聲明不應被閱讀以表明我們進行了 對所有可能獲得的相關信息進行詳盡的調查或審查。這些陳述本身就是不確定的 告誡投資者不要過度依賴這些聲明。實際結果可能與前瞻性預測的結果大相徑庭 許多原因,包括本年度報告題爲「風險因素」一節所討論的因素。 除非適用法律要求,否則我們不承擔公開修改任何前瞻性陳述以反映情況的義務。 或在本年度報告日期之後發生的事件,或反映意外事件的發生。但是,您應該查看 我們將不時向美國證券交易委員會提交的報告中描述的因素和風險, 美國證券交易委員會,在本年度報告日期之後。 | 風險因素摘要 |

| 下面的摘要提供了許多 關於該公司面臨的風險,更詳細的討論見項目1A。「風險因素」如下。你 在投資我們的證券時,應仔細考慮這些風險和不確定性。影響的主要風險和不確定性 我們的業務包括但不限於以下內容: | ● |

| 我們是一家臨床階段的公司,已經蒙受了損失 從我們一開始就是。我們預計,我們將繼續招致巨額開支,我們將繼續招致巨額開支。 可預見的未來的損失。 | ● |

| 我們將來需要籌集更多的資金。 支持我們的業務,這些業務可能無法以對我們有利的條款提供,並可能導致我們的業務嚴重稀釋 股東或增加我們對第三方的債務。 | ● |

| 我們的財務報表包含一個解釋性段落。 關於對我們作爲持續經營企業的持續經營能力的嚴重懷疑,這可能會阻止我們獲得新的融資 在合理的條件下,或者根本沒有。 | ● |

| 我們正在尋求使用以下技術開發候選產品 噬菌體技術,這是一種很難預測潛在成功以及開發時間和成本的方法。致我們的 據了解,到目前爲止,還沒有噬菌體在美國或歐盟被批准作爲藥物。 | ● |

| 我們的候選產品必須經過臨床測試 可能不能證明藥品所需的安全性和有效性,或生物製品的安全性、純度和效力, 我們的任何候選產品都可能導致不良影響,這將大大推遲或阻止監管部門的批准和/或 商業化。 | ● |

| 我們還沒有完成我們的構圖開發 候選產品。 | ● |

| 我們的成功在一定程度上取決於我們留住 並吸引、留住和激勵合格的人員。 | 第一部分 |

| 項目1.業務 | 概述 |

我們是一家臨床階段的產品發現公司 使用天然和工程噬菌體技術開發產品,旨在靶向和殺死相關的特定有害細菌 患有慢性疾病,如囊性纖維化,或CF和糖尿病足骨髓炎,或DFO。噬菌體或噬菌體是細菌, 特定物種的、菌株受限的病毒,感染、放大和殺死目標細菌,被認爲是哺乳動物細胞的惰性病毒。 通過利用自然產生的噬菌體的專利組合和使用合成生物學創造新的噬菌體,我們開發了基於噬菌體的 旨在解決大市場和孤兒疾病的療法。

iii

基於治療感染的緊迫性 (無論是急性還是慢性),目標細菌對噬菌體的敏感性(例如,識別將 針對廣泛的細菌菌株)和其他考慮因素,我們提供兩種基於噬菌體的產品類型:

固定雞尾酒療法-在這種方法中, 含有固定數量的選定噬菌體的產品被開發成覆蓋廣泛的細菌菌株,從而允許治療 使用相同產品的廣大患者群體。固定式雞尾酒是使用我們專有的Bolt平台開發的,其中高 利用吞吐量篩選、定向進化和生物信息學方法來生產最佳的噬菌體雞尾酒。

| 個性化治療--在這種方法中, 開發了噬菌體文庫,其中單個最優噬菌體被個人匹配來治療特定的患者。匹配最優 使用專有的噬菌體敏感性測試或PST對患者進行噬菌體敏感性測試,其中分析了多種考慮因素 同時-允許高效篩選噬菌體文庫,同時保持較短的週轉時間。 | 在我們的治療計劃中,我們專注於使用 針對與疾病相關的特定病原菌的噬菌體療法。我們基於噬菌體的候選產品 都是利用我們博爾特專有的研發平台開發的。博爾特平台是獨一無二的,採用了尖端的方法 和跨學科的能力,包括計算生物學、微生物學、噬菌體合成工程及其生產 細菌宿主,生物分析化驗開發,製造和配方,使天然的靈活和高效的發展 或者經過改造的噬菌體組合,或者雞尾酒。雞尾酒包含功能互補的噬菌體,並針對多個 具有靶向寄主範圍廣、耐藥能力強、生物被膜滲透、穩定性好、易於製造等特點。 |

| 我們的目標是開發多種基於 關於噬菌體準確定位有害細菌的能力,以及我們篩選、鑑定和結合不同噬菌體的能力,兩者都 自然發生和使用合成工程創造的,以開發這些治療方法。 | 我們的產品線 |

| 下面的圖表確定了我們的候選產品 管道、它們的當前狀態和即將到來的里程碑的預期時間。我們沒有任何經批准或可供銷售的產品, 我們的候選產品仍處於臨床前和臨床開發階段,我們還沒有從產品中獲得任何收入 銷售。 | 正在進行的計劃 | |

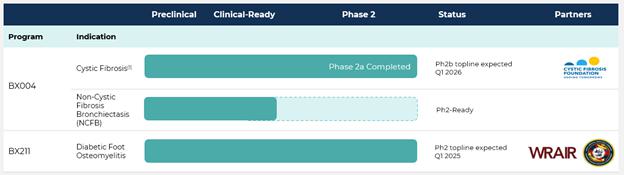

| BX004-治療囊性纖維化 | BX004是我們的候選治療噬菌體產品 正在開發由以下原因引起的慢性肺部感染 |

| 銅綠假單胞菌,或銅綠假單胞菌, | 導致發病率的主要因素 和病死率。由於廣泛使用藥物,對抗生素的耐藥性增強,特別是在CF患者中 由長時間和重複的廣譜抗生素療程組成,通常從童年開始,並導致出現 耐多藥菌株。在臨床前階段 | |

| 體外培養 | 研究表明,BX004對抗生素耐藥菌株具有活性 的 |

| 銅綠假單胞菌 | 並展示了穿透生物膜的能力,生物膜是封閉的表面相關微生物細胞的集合 這是一種胞外聚合物,也是抗生素耐藥性的主要原因之一。 | |

| 慢性充血性心力衰竭患者的1b/2a期試驗 由以下原因引起的呼吸道感染 | 銅綠假單胞菌。 |

| 由兩部分組成。這項研究的設計是基於來自 囊性纖維化治療發展網絡。 | 2023年2月底,我們公佈了積極成果 從評估BX004的1b/2a階段試驗的第1部分開始。第1部分評估了安全性、耐受性、藥代動力學或PK,以及微生物學。 BX004在9例慢性充血性心力衰竭患者(7例服用BX004,2例服用安慰劑)7天遞增治療期間的活性 | |

| 銅綠假單胞菌 | 肺部感染按單次遞增劑量和多次給藥設計。 |

| 1b/2a階段試驗第一部分的結果包括 以下發現:沒有發生與使用BX004治療有關的安全事件;平均銅綠假單胞菌集落形成單位,或CFU,在 第15天(與基線相比):-1.42對數(BX004)與-0.28對數(安慰劑)。這種減少是在吸入護理標準的基礎上看到的 抗生素;在給藥期間,所有接受BX004治療的患者中都檢測到噬菌體,包括幾名患者 15(治療結束一週後);在接受安慰劑的患者中沒有檢測到噬菌體;沒有證據表明與治療有關 與安慰劑相比,在治療期間或治療後對BX004的耐藥性;正如預期的那樣,由於治療持續時間較短,存在 對預測的1秒用力呼氣量百分比或FEV1無明顯影響。 | 2023年11月,我們宣佈了正背線 評估BX004的1b/2a階段試驗的第二部分結果。1b/2a階段試驗的第二部分的目標是評估 與研究第一部分相比,BX004在服用更長時間的CF患者中的安全性和耐受性, 預期較長時間的治療可能會產生比第一部分更大的效果。在第二部分,34名慢性充血性心力衰竭患者被隨機分組 以2:1的比例,23名CF患者接受BX004治療,11名患者通過霧化吸入接受安慰劑治療,連續10天,每天兩次。 |

| 1b/2a階段試驗第二部分的主要結果 包括以下調查結果: | ● |

iv

| 研究中的藥物是安全的 耐受性好,沒有相關的SAE(嚴重不良事件)或相關的APE(急性肺加重)研究藥物。 | ● | |

| 在BX004臂中,3個輸出 在21例(14.3%)基線定量CFU的患者中,痰培養轉爲陰性。 | 銅綠假單胞菌 | |

| 在此之後 10天的治療(包括4天后的2名患者)與安慰劑組的0/10(0%)相比。 | ● |

| BX004與安慰劑對比顯示 在基線肺功能下降(FEV1<70%)的預先確定的亞組患者中有積極的臨床效果。兩者之間的差異 第17天組:FEV1相對改善5.67%(基線爲+1.46比-4.21),囊性纖維化改善+8.87分 問卷修訂版呼吸症狀量表(CFQR)(較基線變化+2.52比-6.35)。 | ● |

| 在全人口中,BX004 與安慰劑相比 | 銅綠假單胞菌 | |

| 痰中的激素水平變化更大,可能是由研究的啓動所驅動的 藥物管理與啓動標準護理抗生素治療方案。在預先指定的患者亞組中 在連續方案吸入抗生素的護理標準方面,BX004與安慰劑相比減少了痰中銅綠假單胞菌的水平。 第10天:-2.8log10cfu/g痰的組與基線的變化差異(與基線的變化-2.91vs-0.11), 超過第1部分的結果。 | ● | |

| 交替/循環背景 抗生素方案可能與血糖波動有關 | 銅綠假單胞菌 | |

| 這些水平可能會混淆這種能力 觀察銅綠假單胞菌在這一亞組中的減少。 | ● | |

| 在研究期間, 根據目前可用的數據,與BX004治療的患者相比,沒有觀察到與治療相關的噬菌體耐藥性的證據 敬安慰劑。 | 2023年8月,FDA批准BX004快速通道 由以下原因引起的慢性呼吸道感染的治療名稱 | |

| 銅綠假單胞菌 | 慢性萎縮性胃炎患者的細菌分離株。 此外,2023年12月,BX004獲得了FDA的孤兒藥物指定。 |

| BiomX預計將啓動一項隨機的、雙重的 慢性充血性心力衰竭患者20期億多中心盲法安慰劑對照研究 | 銅綠假單胞菌 |

| 中國的肺部感染 2025年第二季度。這項研究的目的是招募大約60名患者,按2:1的比例隨機與BX004或安慰劑進行比較。 治療預計每天吸入兩次,持續8周。這項研究旨在監測該藥物的安全性 和BX004的耐受性,旨在證明在微生物減少 | 銅綠假單胞菌 |

| 包袱 並評估對臨床參數的影響,如FEV1測量的肺功能和患者報告的結果。BX004階段2b 預計2026年第一季度將公佈TOPLINE結果。 | BiomX一直在與FDA溝通,並 其他監管機構關於使用真實世界證據或RWE來探索 | |

| 銅綠假單胞菌 | 減少和改善臨床結果。RWE是關於從以下來源獲得的醫療產品的使用、益處或風險的臨床證據 真實世界數據,包括電子健康記錄、索賠數據、患者登記、可穿戴設備和觀察數據等來源 學習。我們預計在2025年與FDA和歐洲人用藥品委員會(CHMP)進行進一步討論,以 討論我們提出的使用萊茵集團支持未來可能的監管申報的計劃。 | |

| BX211-治療糖尿病足骨髓炎 | BX211是一種針對 合併DFO的治療 |

v

金黃色葡萄球菌,

或

金黃色葡萄球菌

。個性化的噬菌體治療爲特定的 根據金黃色葡萄球菌的特定菌株從專有噬菌體庫中挑選噬菌體,從每個患者身上進行活組織檢查和分離。DFO 是一種骨骼的細菌感染,通常由感染的足部潰瘍發展而來,是患者截肢的主要原因。 患有糖尿病。我們相信科學文獻證明了在動物體內使用噬菌體治療骨髓炎的潛在益處。 模型以及許多成功的使用噬菌體療法治療DFO患者的同情心案例支持我們使用噬菌體療法的方法 治療DFO的療法。

隨機、雙盲、安慰劑對照、 研究BX211對金黃色葡萄球菌相關性DFO患者的安全性、耐受性和有效性的多中心2期研究 入選的41名受試者按2:1的比例隨機加入BX211或安慰劑。BX211或安慰劑被設計爲每週一次,局部使用 在第1周靜脈注射或靜脈注射,並在第2-12周每週只用局部途徑。在12周的治療期間,所有受試者 將按照護理標準進行治療,其中包括適當的抗生素治療。研究背線結果的讀數 預計在第13周評估與骨髓炎相關的傷口的癒合情況,預計在2025年第一季度。

| (1) | 非CF型支氣管擴張症 |

| (2) | NCFB是一種慢性、進行性炎症肺。 一種以支氣管永久性擴張爲特徵的疾病。影響美國、歐洲和日本的100多名萬確診患者 (據Weycker稱,Chron Respir Dis.2017年,昆特,歐洲呼吸學雜誌,2016,林豪森,歐洲呼吸學雜誌,2019年, 亨克爾,胸部,2018年,淺倉,美國呼吸與危重護理醫學雜誌2024,Insmed商業演示,6月4日, 2024),NCFB由多種原因引起,但表現出類似的衰弱症狀,包括慢性咳嗽、排痰、 和反覆感染。慢性 |

銅綠假單胞菌

NCFB患者的感染是#年發病率和死亡率的主要貢獻者 這種病。在臨床前階段

體外培養

研究表明,BX004對耐藥菌株具有活性。

銅綠假單胞菌

並展示了穿透生物膜的能力,生物膜是包裹在細胞外聚合物中的表面相關微生物細胞的集合。 這是一種重要的物質,也是抗生素耐藥性的主要原因之一。

BX004在我們的CF階段的待定正數據 20NCFB研究,我們將探索在億進行第二階段研究作爲BX004的額外適應症的可行性。美國國立衛生研究院或NIH對囊性纖維化的研究 我們支持美國國立衛生研究院進行的一項研究 和抗菌素耐藥性領導小組靶向銅綠假單胞菌FDA緊急調查中的慢性萎縮性胃炎患者感染情況 新藥或EIND津貼。1b/2期多中心、隨機、雙盲、安慰劑對照試驗正在評估安全性 在囊性纖維化患者中單次靜脈注射噬菌體療法的微生物學活性銅綠假單胞菌保留的節目

1

假體關節感染,簡稱PJI我們治療PJI的個性化噬菌體療法 針對多種細菌,如金黃色葡萄球菌、表皮葡萄球菌和糞腸球菌。這種治療方法 於2020年7月被FDA授予孤兒藥物稱號。截至本年度報告發布之日,我們已暫停開發工作 由於將資源優先分配給我們的CF和DFO計劃,我們無法提供關於恢復其發展的指導。停產計劃

BX005-治療特應性皮炎,或公元三年BX005是我們的熱門目標噬菌體產品

金黃色葡萄球菌,

或

金黃色葡萄球菌

| ,一種與AD炎症的發展和加劇有關的細菌。 | 金黃色葡萄球菌 |

| 阿爾茨海默病患者的皮膚比正常人的皮膚更豐富,皮損的皮膚比非皮損的皮膚更豐富 皮膚。當患者出現紅斑時,它的數量也會增加,成爲優勢細菌。通過減輕工作人員的負擔 | S. 金星,BX005的設計目的是將皮膚微生物組組成轉移到「耀斑前」狀態,並潛在地提供 臨床益處。在臨床前階段體外培養 |

| 研究表明,BX005可以根除90%以上的菌株,包括抗生素耐藥性 菌株,來自一組 | 金黃色葡萄球菌 |

| 菌株(從美國和歐洲受試者的皮膚中分離出120株)。4月8日, 2022年,FDA批准了該公司的BX005研究新藥或IND申請。 | 2024年,我們停止了BX005的開發, 相反,我們選擇將資源集中在囊性纖維化和DFO項目上。除了專利,我們還依賴於商業祕密 以及如何發展和保持我們的競爭地位。我們通常依靠商業祕密來保護我們業務的各個方面。 不受專利保護,或我們認爲不適合專利保護的產品。我們保護商業祕密和專有技術通過建立 與我們的員工、顧問、科學顧問、承包商和 合作者。這些協議規定,在個人 或實體與我們的關係必須在關係期間和之後保密。這些協議還規定 爲我們工作或與我們的業務有關,並在受僱期間構思或完成的所有發明 或轉讓,如適用,應爲我們的專有財產。此外,我們還採取了其他適當的預防措施,如身體和 技術安全措施,以防止其專有信息被第三方挪用。儘管我們採取措施保護我們的專有 信息和商業祕密,包括通過與我們的員工和顧問簽訂合同,第三方可以獨立 開發實質上同等的專有信息和技術,或以其他方式獲取我們的商業祕密或披露我們的 技術因此,我們可能無法有意義地保護我們的商業祕密並從其獨家使用中受益。了解更多信息 有關與我們的知識產權有關的風險,請參閱“ |

| 風險因素-與我們的許可和共有的風險相關 知識產權 | 競爭生物技術和製藥業 其特點是技術進步迅速,競爭激烈,強調專有產品。雖然我們相信 我們的技術、知識和經驗爲我們提供了競爭優勢,我們面臨着來自許多不同方面的激烈競爭 消息來源,包括擁有更多資源的較大製藥公司。專業生物技術公司、學術研究機構、 政府機構以及公共和私營機構也是有競爭力的產品和技術的潛在來源。 我們相信,影響我們任何候選產品成功的關鍵競爭因素將包括有效性、安全性、 上市時間、成本、促銷活動水平和知識產權保護。我們知道有一些生物技術公司 開發治療疾病的噬菌體產品。據我們所知,幾家生物技術公司,如Locus Biosciences,Inc., Armata PharmPharmticals,Inc.和SNIPR Biome以及學術機構都有自然利用的發現階段或臨床計劃 出現噬菌體或合成生物學方法。此外,我們知道有幾種研究和上市的產品需要治療。 我們針對我們的候選產品的跡象,包括但不限於: |

| ● | Cf: |

Trikafta,Symdeco, Pulmozyme、妥布黴素、氨曲南●DFO

:TP-102是 由Technphage開發,這是由Phaxiam開發的基於噬菌體的產品我們的許多競爭對手,無論是單獨的還是與 他們的戰略合作伙伴比我們擁有更多的財政、技術和人力資源,經驗也要豐富得多。 在候選產品的發現和開發中,獲得FDA和其他監管機構對產品的批准和商業化 這些產品。因此,我們的競爭對手可能比我們更成功地發現候選產品,獲得批准 並獲得廣泛的市場接受度。我們競爭對手的產品可能更有效,甚至更多 有效地營銷和銷售,比我們可能商業化的任何產品都要好,並可能使我們的候選產品過時或沒有競爭力 在我們能夠收回開發和商業化我們的任何候選產品的費用之前。我們預計我們將面臨激烈的 隨着新藥進入市場和先進技術的出現,競爭也越來越激烈。這些第三方在招聘方面與我們競爭 留住合格的科研、臨床、製造、銷售、營銷和管理人員,建立臨床試驗 用於臨床試驗的網站和患者註冊,以及獲取與我們的計劃互補或必要的技術。銷售和市場營銷我們打算將我們的產品商業化 通過建立內部銷售和營銷能力,或通過與其他人合作,候選藥物產品。

政府監管美國政府當局和 除其他外,其他國家對研究、開發、測試、製造、質量控制、批准、標籤、包裝、 儲存、記錄保存、促銷、廣告、分發、審批後監測和報告、營銷和進出口 藥品和生物製品。一般來說,在新藥或生物可以在人體臨床試驗中進行研究或上市之前,需要相當長的時間 必須獲得證明其質量、安全性、有效性、純度和/或效力的數據,並將其組織成特定於每種類型的格式 監管機構,提交審查,並由產品擬研究或銷售的監管機構批准。美國生物製品開發流程

2

在美國,FDA對藥品進行監管 根據聯邦食品、藥物和化妝品法案,或FDCA,及其在FDCA下的實施條例,公共衛生服務 法案,或PHSA及其實施條例。藥品和生物製品也受到其他聯邦、州和地方法規的約束。 和規定。獲得監管批准以及隨後遵守適當的聯邦、州和地方法規的過程 法律法規需要花費大量的時間和財力。未能遵守適用的美國 在產品開發、審批或上市後過程中的任何時候,申請者都可能受到行政管理的約束 或司法制裁。除其他行動外,這些制裁可能包括FDA拒絕批准未決申請、撤回 批准或執照吊銷,臨床保留,無標題或警告信,產品召回或市場撤回,產品扣押, 完全或部分暫停生產或分銷、禁令、罰款、拒絕政府合同、恢復原狀、歸還 以及民事或刑事處罰。任何機構或司法執法行動都可能對我們產生實質性的不利影響。

我們目前的某些候選產品和 未來的候選產品必須通過生物製品許可證申請或BLA程序獲得FDA的批准,然後才能合法使用 在美國銷售。這一過程通常涉及以下幾個方面。然而,特朗普新政府可能會發生變化或進行徹底改革 現有的藥品法規,這將導致更多的時間和金錢來遵守:●按照規定完成廣泛的臨床前研究 遵守適用的法規,如有必要,包括按照GLP要求進行的研究;●向FDA提交IND,它必須成爲 在人體臨床試驗開始前有效;

●

由機構審查委員會或IRB批准, 在每個臨床試驗開始之前,在每個臨床試驗地點;

●充分和良好控制的人類臨床表現 符合適用的IND法規、良好的臨床實踐或GCP要求的試驗以及其他與臨床試驗相關的試驗 爲每個建議的適應症確定研究產品的安全性、純度、效力和功效的法規;●向食品和藥物管理局提交了一份BLA;●FDA在收到後60天內做出的決定 接受有關覆核申請;●

令人滿意地完成FDA批准前的檢查 生產生物製劑的一個或多個生產設施,以評估符合cGMP要求的情況,以確保 設施、方法和控制足以保持生物的特性、強度、質量和純度;

●

FDA可能對符合以下條件的臨床試驗地點進行審計 生成了支持BLA的數據;●支付FDA審查BLA的使用費(除非 豁免收費);以及●.

兒科學

兒科人群中的強制性檢測 在越來越多的司法管轄區被要求。歐盟頒佈了一項複雜而非常嚴格的制度,激勵了其他國家 司法管轄區,包括美國和瑞士。任何要求批准以下內容的申請:(I)含有新的 活性物質或(二)已經授權的藥物的新的治療適應症、藥物形式或給藥途徑 含有仍受附加保護證書或SPC或符合以下條件的專利保護的活性物質的產品 對於SPC,必須包括兒科數據。否則,主管監管當局不會批准該申請。意見書 在這些情況下,兒科數據的使用是強制性的,即使應用程序涉及成人使用。不需要提交兒科數據 或者,如果EMA分別批准了對兒科開發的全部或部分豁免,則完全要求。此外,該提交可以 如果EMA批准推遲提交MAA,以不延誤提交成年人口的MAA,則推遲提交。

兒科數據是通過實現生成的 該公司在成人PK研究完成後提出並同意的兒科調查計劃或PIP 由EMA執行,通常在一些修改之後。PIP列出了爲證明安全性而進行的所有研究和採取的措施 以及未來藥品在兒童中使用時的療效。EMA可以應公司的要求同意修改PIP。 PIP的範圍是成人的治療適應症或成人應用是其一部分甚至是機制的條件 活性物質的行動,在環境管理協會的準自由裁量權。這一非常廣泛的自由裁量權使EMA能夠要求公司 開發不同於成人的兒童適應症。

完成PIP後,該公司符合資格 對於兒科獎勵,可以是將最高法院的期限延長六個月,或者在孤兒藥品的情況下,再增加兩個 多年的市場排他性。除了其他條件外,獎勵還取決於PIP完全完成、兒科醫療 產品在所有成員國獲得批准,以及以這樣或那樣的方式提到的兒科研究結果(用於 例如,兒科適應症的批准),在產品的產品特性摘要中。

上市後要求許多國家都有上市後的要求 與美國實施的類似,特別是安全監測或藥物警戒。在歐盟,藥物警戒 數據是主管監管當局實施批准後安全性或有效性研究的基礎,包括 在標籤外使用。不遵守這些要求可能會導致重大的經濟處罰,以及暫停或撤回 行銷授權書。

補充保護證書和監管排除在美國以外的一些國家, 我們的一些專利可能有資格獲得有限的專利期延長,這取決於監管的時間、期限和細節 批准我們的候選產品和任何未來的候選產品。此外,授權的藥物和生物製品可能受益於監管 排他性(除了專利產生的專利保護之外)。在歐洲聯盟,條例(EC)469/2009 研究所SPC。SPC是專利期限的延伸,用於補償因法律糾紛而喪失的專利保護 在將醫藥產品投放市場之前,要求進行安全性和有效性測試並獲得營銷授權。 可以將SPC申請到受「基礎專利」(由專利持有人選擇的專利, 其可以是產品、方法或應用專利),並且在獲得 符合歐盟藥劑法的上市授權。最高法院的任期最長爲五年, 專利和SPC保護不得超過自歐洲經濟區首次營銷授權之日起15年。SPC權利是 受基本專利和營銷授權的限制,即SPC授予與基本專利授予的權利相同的權利 專利,但僅限於上市授權所涵蓋的活性物質(以及後來批准的任何醫藥產品用途)。雖然SPC在歐洲層面受到監管, 它們是由國家專利局授予的。授予SPC需要國家專利局授予的基本專利,並且 上市授權書,這是全國首個將活性物質作爲醫藥產品的上市授權書。 此外,活性物質不得已被授予任何SPC,申請SPC必須向國家 專利局在歐洲經濟區第一次市場授權或授予基礎專利後六個月內,以最新的爲準。在未來,我們可能會申請一臺SPC 或更多我們目前擁有或許可的歐洲專利,以延長其當前到期日期之後的專利壽命,具體取決於 臨床試驗的預期時長和提交相關MAA所涉及的其他因素。此外,在歐洲聯盟,醫療保健 產品可能受益於以下法規排他性:數據排他性、市場保護、市場排他性和兒科 獎勵。一種含有一種新活性物質的醫藥產品 物質(參考藥品)被授予八年的數據獨佔權,然後是兩年的市場保護。數據獨佔性 防止其他公司在參考藥品的上市授權檔案中引用非臨床和臨床數據 用於提交仿製藥MAA目的的產品,市場保護防止其他公司將仿製藥推向市場。根據 對於全球營銷授權的概念,該醫藥產品的任何進一步開發(例如,新的適應症,新的形式, 對活性物質的更改)不會觸發任何新的或額外的保護。授權書 任何新的發展被認爲是「落入」在監管保護方面的初始銷售授權; 因此,新開發項目只有在獲得授權後才能受益於監管保護。唯一的例外是一個新的 與現有療法相比,被認爲能帶來顯著臨床益處的治療適應症。如此新奇 如果在第一年內獲得授權,指示將在全球營銷授權中增加一年的市場保護 八年的授權(即在數據獨佔期內)。此外,一種新的治療適應症是一種“公認的 物質“受益於一年的數據獨佔性,但僅限於支持新適應症的非臨床和臨床數據。 在歐洲環保局批准至少十年的任何活性物質都符合良好的物質標準。生物仿製藥可通過縮寫的 批准途徑在八年數據獨佔期結束後,並可能在10年或11年市場保護之後上市 句號。批准生物仿製藥需要申請人證明生物仿製藥與生物藥用藥之間的相似性。 並提交EMA定義的非臨床和臨床數據。生物相似的法律制度主要是通過 EMA的適用於生物活性物質類別的科學指南。與美國不同,可互換性 由每個成員國進行監管。市場排他性是一種監管保護 獨家提供給孤兒身份的醫藥產品。市場排他性排除了EMA或國家監管機構 批准另一個MAA,以及歐盟委員會或國家監管機構授予另一個營銷授權, 對於相同或類似的醫藥產品和相同的治療適應症,自批准之日起十年內(見上文)。兒科獎勵是另一種監管排他性。 完成PIP使公司有資格獲得兒科獎勵,這可以是最高法院期限的六個月延長,或者, 在孤兒藥品的情況下,額外兩年的市場排他性(見上文)。如果在自願的情況下完成了PIP 在此基礎上,即對於不再或不再受SPC或基礎專利保護的經批准的醫藥產品,兒科獎勵將 形式的「兒科用藥上市授權」,或PUMA。這一特殊授權不屬於全球 市場授權,因此受益於八年的數據獨佔性,然後是兩三年的市場保護。其他美國醫保法和合規性要求除了FDA對市場的限制外 對於醫藥產品,我們可能會受到針對醫療保健行業欺詐和濫用的各種聯邦和州法律的約束。 這些法律可能會影響我們的業務或財務安排以及我們通過其進行營銷、銷售和 經銷我們批准的產品(如有)。可能影響我們運作能力的法律包括:●

聯邦反回扣法規禁止, 明知而故意索取、收受、提供或支付任何報酬(包括任何回扣、賄賂、 或回扣)直接或間接、公開或隱蔽地、以現金或實物形式,誘使或作爲回報,轉介 個人,或購買、租賃、訂購或推薦任何可以付款的物品、設施、物品或服務, 全部或部分,根據聯邦醫療保健計劃,如聯邦醫療保險和醫療補助計劃;個人或實體不 需要實際了解聯邦反回扣法規或違反該法規的具體意圖才能實施違規。 此外,政府可以主張,包括因違反聯邦反回扣而產生的物品或服務的索賠 就聯邦虛假索賠法案或FCA或聯邦民事罰款而言,法規構成虛假或欺詐性索賠 法規;

3

美國《反海外腐敗法》

美國《反海外腐敗法》 我們是主體,禁止公司和個人從事某些活動以獲得或保留業務或影響 以官方身份工作的人。向任何外國人支付、提出支付或授權支付任何有價值的東西都是非法的 政府官員、政府工作人員、政黨或政治候選人企圖獲得或保留業務或 以其他方式影響以官方身份工作的人。類似的規則也適用於世界上許多其他國家,如法國(“

| 意向書 薩平“ | )或英國(英國《反賄賂法》)。 |

| 美國醫療改革 | 美國醫療保健行業的主要趨勢 其他方面則是成本控制。政府當局和其他第三方付款人試圖通過限制覆蓋範圍來控制成本 以及特定醫療產品的報銷金額。例如,2010年3月頒佈了《ACA》,除其他外 在醫療補助藥品退稅計劃下,增加了大多數製造商所欠的最低醫療補助退稅;引入了一種新的方法 製造商在醫療補助藥品退稅計劃下欠下的回扣是根據該回扣計算吸入、輸注、滴注、 植入或注射;將醫療補助藥品退稅計劃擴大到使用參加醫療補助的個人的處方 管理式醫療計劃;對某些聯邦醫療保險D部分受益人強制折扣,作爲製造商門診的條件 聯邦醫療保險D部分下的藥品保險;要求製藥商根據製藥公司的份額支付新的年費 向聯邦醫療保健計劃銷售;創建了一個新的以患者爲中心的結果研究所,以監督、確定優先事項 並進行臨床療效比較研究,併爲此類研究提供資金;併成立了醫療保險中心 和醫療補助創新在CMS測試創新的支付和服務交付模式,以降低醫療保險和醫療補助支出。 |

| 自該法案頒佈以來,已經有一些 ACA的重大變化。2021年6月17日,美國最高法院駁回了對該法案的最新司法挑戰 ACA沒有具體裁決ACA的合憲性。在美國最高法院做出裁決之前,總裁·拜登 發佈行政命令,啓動2021年2月15日至2021年8月15日的特殊招生期限 通過ACA市場獲得醫療保險覆蓋範圍。行政命令還指示某些政府機構 審查和重新考慮限制獲得醫療保健的現有政策和規則。最近,在2021年3月11日,總裁 拜登簽署了《2021年美國救援計劃法案》,取消了目前設定的法定醫療補助藥品退稅上限 從2024年1月1日開始,以藥品製造商平均價格的100%計算。 | 此外,《2011年預算控制法》和 2015年的兩黨預算法案導致向醫療保險提供者支付的醫療保險總金額每財年減少2%,並將繼續 有效期到2030年,除非國會採取額外行動。此外,2013年1月2日,美國納稅人救濟法 簽署成爲法律,其中包括減少向幾種類型的提供者支付的醫療保險,包括醫院、成像 中心和癌症治療中心,並增加了政府追回向提供者多付款項的訴訟時效期限 從三年到五年。最近,政府加強了對製造商定價方式的審查 他們的上市產品,這導致了最近的幾次國會調查和提出的法案,旨在,等等 提高產品定價的透明度,審查定價與製造商耐心計劃之間的關係,並進行改革 針對藥品的政府計劃報銷方法。2022年8月,《通貨膨脹率降低法》授權醫療保險 爲談判某些高額支出的藥品價格,單一來源的醫療保險B部分或D部分藥品。美國的各個州 也越來越積極地通過立法和實施旨在控制藥品定價的法規, 包括價格或患者報銷限制、折扣、對某些產品准入的限制以及營銷成本披露 和透明度措施,在某些情況下,旨在鼓勵從其他國家進口和大宗採購。 |

我們預計會有更多的外國、聯邦和 未來將採取州醫療改革措施,其中任何一項都可能限制聯邦和州政府 將爲醫療產品和服務買單,這可能會導致覆蓋範圍和報銷範圍有限,並減少對我們產品的需求, 一旦獲得批准,或額外的定價壓力。

承保和報銷

覆蓋範圍存在很大的不確定性 以及我們獲得監管部門批准的任何產品的報銷狀態。在美國,化妝品一般不符合資格 承保和報銷,因此任何作爲化妝品銷售的產品都不在承保或報銷之列。在美國 國家和其他國家的市場,我們獲得監管批准進行商業銷售的任何產品的銷售將取決於, 在一定程度上,這取決於承保範圍和第三方支付者的補償。第三方付款人包括政府當局、 管理型醫療服務提供者、私人健康保險公司和其他組織。確定付款人是否將提供保險的過程 可以與設置付款人將爲該產品支付的償還率的過程分開。第三方 付款人可以將承保範圍限制在批准的清單或配方表上的特定產品,其中可能不包括FDA批准的所有產品 尋找一種特殊的跡象。第三方付款人決定不承保我們的產品可能會減少醫生對我們產品的使用 一旦獲得批准,將對我們的銷售、經營業績和財務狀況產生實質性的不利影響。此外,付款人的 決定爲產品提供保險並不意味着將批准足夠的報銷率。充足的第三方 報銷可能無法使我們維持足夠的價格水平,以實現適當的投資回報 在產品開發方面。

此外,產品的承保和報銷 不同的付款人可以有很大的不同。第三方付款人決定承保特定的醫療產品或服務 不確保其他付款人也將爲醫療產品或服務提供保險,或將以適當的 報銷率。

因此,覆蓋範圍確定過程 將要求我們爲每個付款人分別提供使用我們的產品的科學和臨床支持,這將是一個耗時的過程 進程。

第三方付款人正面臨越來越大的挑戰 價格和檢查醫療產品和服務的醫療必要性和成本效益,以及它們的安全性和 功效。爲了獲得和維持任何產品的承保和報銷,我們可能需要進行昂貴的臨床試驗 爲了證明這種產品的醫療必要性和成本效益,除了獲得監管規定所需的費用外, 批准。如果第三方付款人不認爲一種產品與其他可用的療法相比具有成本效益,他們可能不會覆蓋 產品作爲他們計劃下的一項福利,或者,如果他們這樣做了,付款水平可能不足以允許公司出售其 盈利的產品。

4

在美國以外,藥品的定價 在許多國家,產品受到政府的管制。例如,在歐洲聯盟,定價和補償計劃 成員國之間的差異很大。一些國家規定,產品只能在報銷價格後才能銷售。 已經達成一致。一些國家可能要求完成額外的研究,以比較特定方案的成本效益 將現有的治療方法或所謂的保健技術評估用於治療,以便獲得報銷或定價批准。 其他國家可能允許公司爲產品定價,但監控產品數量併發布指導意見 要求醫生限制處方。控制藥品和醫療器械價格和使用的努力可能會 隨着各國試圖管理醫療支出,這一趨勢仍在繼續。

數據隱私和安全法

許多州、聯邦和外國法律,包括 消費者保護法律和法規,管理個人信息的收集、傳播、使用、獲取、保密和安全 信息,包括與健康有關的信息。在美國,包括數據在內的衆多聯邦和州法律法規 違反通知法、健康信息隱私和安全法,包括HIPAA,以及聯邦和州消費者保護法 和條例(例如,聯邦貿易委員會法案第5條),管理與健康有關的和其他 個人信息可能適用於我們的運營或我們合作伙伴的運營。此外,某些州和非美國法律,如 正如加州消費者保護法、加州隱私權法案和一般數據保護法規(GDPR)所管轄的那樣 個人信息的隱私和安全,包括在某些情況下與健康有關的信息,其中一些情況 比HIPAA更嚴格,其中許多在顯著方面彼此不同,可能沒有相同的效果,因此使情況複雜化 合規努力。如果不遵守這些法律,可能會造成重大的民事和/或刑事處罰。 處罰和私人訴訟。隱私和安全法律、法規和其他義務是不斷演變的,可能會發生衝突 使合規工作複雜化,並可能導致調查、訴訟或導致重大 民事和/或刑事處罰以及對數據處理的限制。

材料協議

許可協議

與業達的許可協議

5

我們研究和開發的成本、時間和進度 發展和臨床活動;

●

與我們的目標噬菌體相關的製造成本, 或噬菌體、治療策略等研發活動;●”

任何協作、許可、 收購或我們可能建立的其他安排;

●

與員工相關的費用以及外部成本 例如支付給外部顧問的費用;

●尋求監管批准的成本和時間 並與遵守監管要求有關;以及●

立案、起訴、辯護和執行的費用 任何專利申請、權利要求、專利和其他知識產權。

6

國內和國際股票和債務市場 已經經歷並可能繼續經歷基於國內和國際經濟狀況的高度波動和動盪 和顧慮。如果這些經濟狀況和擔憂持續或惡化,市場繼續波動,或 美國股市接踵而至的是熊市或衰退,或者市場受到以色列等因素的負面影響 與哈馬斯和真主黨的戰爭,俄羅斯入侵烏克蘭,以及由此導致的對俄羅斯、白俄羅斯和相關各方的世界制裁 或地緣政治不確定性和不穩定的其他來源,我們的經營業績和流動性可能會受到這些 很多方面的因素,包括使我們在必要時更難籌集資金,我們的股價可能會下跌。

不能保證有足夠的資金 將在需要時或在可接受的條件下提供給我們,如果有的話。我們無法獲得額外的資金可能會有一種材料 對我們的業務、財務狀況和經營結果產生不利影響。此外,如果我們無法獲得額外的資金, 隨着時間的推移,人們將極大地懷疑我們是否有能力繼續作爲一個持續經營的企業,並增加破產的風險 以及我們股東的全部投資損失。

我們的財務報表包含一個關於以下方面的解釋性段落 對我們作爲一家持續經營企業的持續經營能力存在很大懷疑,這可能會阻止我們在合理的基礎上獲得新的融資 條件或者根本不是。

我們的財務報表 包含一段解釋性段落,說明對我們作爲持續經營企業的持續經營能力的嚴重懷疑。我們得出的結論是 人們對我們作爲一家持續經營的企業繼續下去的能力有很大的懷疑。我們已經積累了18070美元的萬赤字,因爲我們 盜夢空間。到目前爲止,我們還沒有從我們的運營中產生收入,我們預計不會從以下方面產生任何重大收入 未來12個月的產品銷售情況。在可預見的未來,我們的現金需求可能會增加。截至2024年12月31日,我們有18美元 百萬美元的現金和現金等價物。

我們相信我們手頭的現金和現金等價物, 包括在2025年2月融資中籌集的現金,如第7項「流動資金和資本資源」所述 這份年度報告將足以滿足我們在#年第一季度的營運資本和資本支出需求。 2026年。我們的持續經營取決於許多因素,包括我們籌集額外資金的能力、成功 我們對CF和DFO的臨床試驗以及我們在到期時償還債務的能力。我們不能肯定我們將能夠獲得 未來的任何資金,以及我們可能獲得的任何此類資金,都可能不足以爲我們的運營提供資金。如果我們不能獲得足夠的 資金,我們可能無法繼續作爲一個持續經營的企業。

我們正在尋求利用噬菌體技術開發候選產品, 一種很難預測開發時間和成本的方法。據我們所知,截至本年度報告發布之日, 到目前爲止,還沒有噬菌體在美國或歐盟被批准作爲藥物。

我們正在開發我們的候選藥物產品 利用噬菌體技術。我們還沒有,據我們所知,也沒有任何其他公司獲得FDA的監管營銷批准, 或同等的外國監管機構對基於這種方法的藥品(噬菌體技術)進行監管。而當

體外培養

7

和

在……裏面 活體

研究已經表徵了噬菌體在細胞培養和動物模型中的行爲,並且有大量關於 關於噬菌體療法在人類中的應用,噬菌體療法在人類中的安全性和有效性還沒有得到廣泛的研究和很好的對照 現代臨床試驗。此前對噬菌體療法的大部分研究都是在前蘇聯進行的,在此之前和之後 第二次世界大戰後,缺乏適當的控制組設計或根本沒有控制組。此外,護理標準還包括 在這些研究進行後的幾十年裏發生了很大的變化,削弱了以前聲稱的改善的相關性 治癒率。我們開發的任何候選產品都不能在實驗室向患者展示其治療特性。 以及其他臨床前研究,它們可能以不可預見的、無效的甚至有害的方式與人類生物系統相互作用。我們 不能確定我們的方法將導致可批准或可銷售的藥物產品的開發。此外,細菌 隨着時間的推移,噬菌體的目標可能會對我們的候選產品產生抵抗力,我們可能能夠也可能不能通過開發克服這一點 新的噬菌體雞尾酒,否則我們可能無法構建一個對我們的目標病原體世界有足夠覆蓋的雞尾酒。如果我們的候選產品獲得監管部門的批准 但如果沒有達到醫生、醫療保健支付者和患者足夠的接受度,我們可能不會產生產品收入 足以實現盈利。我們的成功將取決於專門治療我們所針對的疾病的醫生 我們追求的候選產品作爲藥物,開出潛在的治療方法,涉及使用我們的候選產品來代替, 或者,除了他們更熟悉的、可能有更多臨床數據的現有治療方法。我們的成功 還將取決於消費者對我們商業化產品的接受和採用。臨床前研究中的不良事件和 我們候選產品的臨床試驗或其他開發類似產品的臨床試驗以及由此產生的宣傳,如 以及噬菌體療法領域的任何其他不良事件,都可能導致對我們可能 發展。市場對任何經批准的產品的接受程度將取決於多個因素,包括:.”

●

產品的有效性;

●

| 任何副作用的流行率和嚴重程度; | ●替代方案的潛在優勢或劣勢 治療; |

| ● | 相對方便和容易管理;● |

有實力的營銷和分銷支持;

●

8

產品的價格,包括絕對價格和 相對於替代療法;以及

●

足夠的第三方承保或報銷。

在商業廣告中開發我們的候選產品 擴大規模將需要大量的技術、財政和人力資源。我們和我們的第三方合作伙伴可能會遇到延遲 爲我們的候選產品開發製造能力,並且可能無法達到有效實施所需的規模 臨床試驗需要獲得監管機構的批准,我們的候選產品需要它,或生產商業 我們的產品數量,如果獲得批准或以其他方式允許上市。

我們的候選產品必須經過臨床測試,這可能會 未能證明藥品所需的安全性和有效性,或生物製品的安全性、純度和效力,以及我們的任何 候選產品可能會造成不利影響,這將大大推遲或阻止監管部門的批准和/或商業化。

在我們能夠獲得監管部門的批准之前 產品候選或以其他方式獲得允許我們將產品作爲藥物或生物產品進行市場的證據,我們必須進行廣泛的臨床前研究 和臨床試驗,以證明安全性和有效性,或在生物製品的情況下,令人滿意的安全性、純度和效力 FDA或其他監管機構。候選產品的臨床試驗足以獲得監管市場批准或 否則,在營銷前展示安全性,成本高昂,需要數年時間才能完成。此外,這些臨床試驗的結果 可能不會顯示我們候選產品的安全性或有效性足以導致批准或保證進一步開發。我們的方法 旨在設計噬菌體組合或雞尾酒,以針對特定的病原菌菌株,以改變微生物組 成分,並賦予患者潛在的治療或美容益處。然而,不能保證根除 選定的靶點將對潛在疾病產生臨床上有意義的影響,例如在以下情況下 這種疾病的定義不是很清楚。此外,我們針對的細菌可能與疾病有關,但可能不是致病原因。 或對疾病的病理有貢獻,或者可能存在我們的候選產品沒有針對的其他細菌,這些細菌 潛在疾病的有意義的驅動因素。此外,我們的候選產品要求使用有效的遞送工具來到達 目標器官或組織,並且不能保證我們的預期遞送系統將允許我們的候選產品到達 病人身上的理想位置。安全性必須首先通過臨床前試驗和早期臨床試驗來確定,然後才能有效 可以被評估和建立,從而導致FDA或其他監管機構獲得上市批准。我們的臨床試驗可能會產生 不良副作用或負面或不確定的結果,我們可能決定,或監管機構可能要求我們進行額外的 臨床和/或臨床前試驗或放棄計劃。

持續的地緣政治不穩定對 並可能繼續對我們的業務產生不利影響,包括我們的臨床試驗。

| 一般經濟、政治、人口和商業 世界各地的局勢,包括地緣政治的不確定性和不穩定,如以色列與哈馬斯和真主黨的戰爭以及 俄羅斯和烏克蘭的衝突,可能會間接中斷我們的供應鏈,損害我們的能力,從而對我們的業務產生不利影響 以我們可以接受的條件籌集資金,以及其他影響。我們可能會進一步經歷其他中斷,這可能會嚴重影響 我們的業務、臨床前研究和臨床試驗,包括: | ● |

| 在我們的計劃中招募患者的延遲或困難 臨床試驗; | ● |

| 臨床站點啓動的延遲或困難, 包括招聘臨床現場調查員和臨床現場工作人員的困難; | ● |

| 供應中斷或延遲接收 由於人手短缺、生產速度減慢或停產,我們的代工生產組織中的候選產品 以及輸送系統的中斷;以及 | ● |

| 中斷或延遲我們的來源發現和 臨床活動。 | 貿易政策的變化,包括徵收關稅, 可能會對我們的業務、經營結果和財務狀況產生不利影響。 |

| 美國和多個外國政府已經 確立了一定的貿易和關稅要求。美國政府不時表示願意修改或重新談判 對進口到美國的某些商品徵收關稅,因爲我們依賴來自歐盟某些國家的某些組件,例如 如果採取這些措施,可能會對我們的業務產生不利影響,增加我們的成本,並降低我們產品的競爭力。 | 2025年2月1日,總裁·特朗普宣佈 對中國進口商品加徵10%關稅,並已表示可能對歐盟進口商品加徵關稅 還有印度。此外,2025年2月13日,總裁·特朗普宣佈了一項計劃,與徵收關稅的國家建立互惠關稅 對美國產品徵收關稅,並指示美國政府相關部門評估非互惠貿易安排和 在180天內生成該評估報告。可在報告完成前徵收互惠關稅。那裏也有 一直是特朗普政府關於對藥品徵收25%關稅的聲明。截至12月31日止年度, 到2025年,我們估計目前對我們從中國進口的商品徵收的關稅的影響不會很大。我們無法估計 美國政府尚未徵收的任何關稅的影響。 |

| 如果我們無法獲得,或者如果在獲得過程中出現延誤, 對於我們的治療適應症候選產品,如果需要監管部門的批准,我們將無法商業化或將 延遲商業化,我們的候選產品,以及我們未來創造收入的能力將受到實質性的損害。 | 我們的候選產品和相關活動 隨着治療適應症的開發和商業化,包括它們的設計、測試、製造、安全性、有效性, 記錄保存、標籤、儲存、批准、廣告、促銷、銷售、分銷、進出口受 FDA和美國的其他監管機構以及同等的外國監管機構。在我們可以商業化之前 我們的任何產品作爲治療適應症的候選產品,我們都必須獲得市場批准。我們還沒有獲得上市批准 我們的任何候選產品都來自任何司法管轄區的監管機構,並且有可能我們的任何候選產品 或者,我們未來可能尋求開發的任何候選產品都將獲得監管部門的批准。 |

9

| 獲得監管部門批准的過程 對於治療適應症,在美國和其他國家都是昂貴的,如果額外的臨床應用可能需要很多年 試驗是必需的,可以根據各種因素而有很大的不同,包括產品的類型、複雜性和新穎性 涉及的候選人。開發期間市場審批政策的變化、附加條款的變更或頒佈 法規或法規,或對每個提交的IND或同等申請類型的監管審查的更改,可能會導致延遲 批准或拒絕一項申請。FDA和同等的外國監管機構在以下方面擁有相當大的自由裁量權 審批流程,並可能拒絕接受任何申請,或可能決定我們的數據不足以進行審批並需要額外的 臨床前、臨床或其他研究。圍繞特朗普政府實施的新預算和裁員存在不確定性 這可能會影響新藥的及時開發、批准和商業化。此外,特朗普政府可能會 改變或徹底改革現有的藥品法規,這將導致更多的時間和金錢來遵守。此外,特朗普 政府的關稅可能會增加臨床手術的成本或影響供應鏈。我們的候選產品可以 因多種原因延遲收到或未能收到監管批准,包括以下原因: | ● |

| FDA或同等的外國監管機構 可能不同意設計,包括研究人群、劑量水平、劑量方案和生物分析分析方法或實施 我們的臨床試驗; | ● |

| 我們可能無法證明令人滿意的結果 FDA或同等的外國監管機構證明候選藥物對於其建議的適應症是安全和有效的,或 相關的伴隨診斷適用於確定合適的患者群體; | ● |

臨床試驗結果可能達不到標準 FDA或同等的外國監管機構要求批准的統計意義,例如 我們的痤瘡候選產品;

●我們可能無法證明產品候選者的 臨床和其他益處超過其安全風險;●

FDA或同等的外國監管機構 可能不同意我們對臨床前研究或臨床試驗數據的解釋;

●

從我們產品的臨床試驗中收集的數據 候選人可能不足以支持提交營銷申請或其他提交或獲得監管 在美國或其他地方獲得批准;

| ● | FDA或同等的外國監管機構 可能無法批准與我們簽訂臨床和醫療合同的第三方製造商的製造工藝或設施 商業用品;以及 |

10

| ● | FDA的批准政策或法規或 同等的外國監管機構可能會發生重大變化,導致我們的臨床數據不足以獲得批准。 |

| 在大量正在開發的藥物中,只有 一小部分人成功地完成了FDA或同等的外國監管批准程序,並已商業化。漫漫長路 審批過程以及未來臨床試驗結果的不可預測性可能導致我們無法獲得監管部門的批准 推銷其候選產品,這將嚴重損害我們的業務、運營結果和前景。 | FDA還可能需要一個專家小組,由 作爲一個諮詢委員會,審議安全性和有效性數據是否充分,以支持治療適應症的批准。 諮詢委員會的意見雖然不具約束力,但可能會對我們獲得批准任何產品的能力產生重大影響 我們根據已完成的臨床試驗開發的候選藥物。在歐盟,任何產品的安全性和有效性數據 EMA認爲符合高級治療藥物資格的候選人必須經過EMA的審查,委員會 先進療法,一批先進療法的專家醫療產品。 |

此外,根據PREA,在美國,以及 在歐盟、FDA或同等的外國監管機構中,兒科法規可能要求在 兒科人口。在美國或歐盟的批准申請必須包含評估安全性的數據 以及在所有相關兒科亞群中對所聲稱的適應症的生物有效性,並支持劑量和給藥 對於該產品安全有效的每個兒科亞群。FDA或同等的外國監管機構可以, 酌情批准對兒科受試者提交數據給予全部或部分豁免或延期。如果FDA需要數據 對於兒科患者,將不得不投入更多的資金來進行強制性的兒科臨床試驗。 和研究,但用於成人的醫藥產品的批准通常不應受到影響。如果這樣的結果 兒科研究不呈陽性,我們的產品候選將不會被批准用於兒童。

另外,即使我們得到批准, 監管機構可能會批准我們的任何候選產品,其治療適應症少於或超過我們的要求, 可能包括限制合適患者人數的使用限制或禁忌症,可能不會批准我們計劃的價格 對我們的產品收費,可能會根據昂貴的上市後臨床試驗的表現給予批准,或者可能批准 候選產品的標籤不包括成功商業化所必需或需要的標籤聲明 該產品的候選產品。上述任何一種情況都可能對我們的候選產品的商業前景造成實質性損害。如果我們在獲得批准方面遇到延誤 或者如果我們不能獲得我們的候選產品的批准,我們的候選產品的商業前景可能會受到損害,我們的 未來創造收入的能力將受到嚴重損害。我們從未從產品銷售中獲得任何收入,並可能 永遠不要盈利,否則,如果實現了,可能無法持續盈利。

我們能夠創造有意義的收入和 實現盈利取決於我們的能力,以及我們可能與之合作的任何第三方成功完成的能力 制定並滿足監管要求,包括(但不限於)獲得任何必要的監管批准,以 將我們的候選產品商業化。我們目前不符合法規要求,也沒有所需的批准來銷售我們的產品 候選人,可能永遠不會遇到或接待他們。在可預見的未來,我們預計不會從產品銷售中獲得收入, 如果有的話。如果我們的任何候選產品在臨床試驗中失敗,或者如果我們的任何候選產品不符合監管要求, 包括在需要時獲得監管部門的批准,或者如果我們的任何候選產品在上市時未能獲得市場認可, 我們可能永遠不會盈利。即使我們在未來實現盈利,我們也可能無法在隨後的 句號。我們未來從產品銷售中獲得收入的能力在很大程度上取決於我們在以下方面的成功:

●

11

完成研究以及臨床前和臨床開發 我們的候選產品;

●

尋求並獲得監管和營銷批准 對於我們完成臨床試驗的候選產品;

●

滿足營銷產品的監管要求;

●

開發可持續、可擴展、可複製和 我們候選產品的可轉移製造流程;

12

●

推出並商業化候選產品 我們獲得監管和營銷批准或以其他方式允許營銷,無論是通過建立銷售隊伍,營銷 和分銷基礎設施或與合作伙伴合作;

●

獲得市場對任何批准產品的認可;

●

應對任何相互競爭的技術和市場發展;

13

●

實施額外的內部系統和基礎設施, 根據需要;

●

識別和驗證新候選產品;

●

在任何合作、許可中談判有利的條款 或我們可能達成的其他安排;

14

●

維護、保護和擴大我們的投資組合 知識產權,包括專利、商業祕密和專有技術;以及

●

吸引、聘用和留住人才。

即使一個或多個候選產品 我們開發的被批准用於商業銷售或以其他方式被允許用於營銷的產品,我們預計會產生大量相關成本 將任何經批准的產品商業化。如果FDA或EMA要求我們,我們的費用可能會超出預期, 或其他同等的外國監管機構,在我們目前預期的基礎上進行臨床試驗和其他研究。 即使我們能夠從銷售任何經批准的產品中獲得收入,我們也可能無法盈利,可能需要獲得額外的 爲繼續運營提供資金。如果我們不能盈利,或者如果我們無法彌補持續的虧損,我們的業務,財務 運營的條件和結果可能會受到實質性的不利影響。

我們正在尋求開發治療醫療的候選產品 與某些細菌的存在有關的條件。我們的成功在很大程度上取決於市場的廣泛接受度,以及 就藥物產品而言,醫生的採用和使用是商業成功所必需的。

即使我們獲得了FDA或外國監管機構的批准 對於我們的候選藥物產品,我們候選產品的商業成功將取決於消費者對 我們商業化的產品。我們候選產品的臨床前研究和臨床試驗或臨床試驗中的不良事件 其他人開發類似的產品,由此產生的宣傳可能會導致對我們可能開發的任何產品的需求減少。

15

此外,我們藥物的商業成功 候選產品將在很大程度上取決於兒科醫生和其他內科醫生對其批准的治療方法的廣泛採用和使用 適應症,以及我們可能尋求批准的任何其他適應症。我們不能肯定我們的方法會導致 開發可批准的或可銷售的產品。

獲得特定噬菌體雞尾酒的高滴度是必要的 對於我們的臨床前和臨床測試可能是困難和耗時的。

我們的候選產品是噬菌體雞尾酒 我們的設計符合特定的特點。我們和我們的合同製造商生產多種噬菌體的雞尾酒,它可能 要獲得高滴度或高水平的噬菌體,以滿足我們的臨床前和臨床測試,是困難或耗時的。在一些 在某些情況下,它可能需要多次運行產品才能獲得臨床測試所需的數量。這可能會導致 在我們的臨床試驗時間表的延遲,這可能會增加生產成本和相關費用。此外,可能很難做到 在一定程度上覆制製造過程,以便隨着我們的候選產品的進步而需要更多的數量 臨床發展過程。

我們候選產品的臨床前研究結果可能 不能預測臨床試驗或後期臨床開發的結果。

我們候選產品的臨床前研究, 例如BX004和BX211,包括在動物疾病模型中的研究可能無法準確預測候選產品的安全性 進一步的人體臨床試驗將被允許進行。特別是,前景看好的臨床前試驗表明, 原型噬菌體產品的有效性可能不能預測這些產品在人類臨床環境中處理條件的能力。 例如,當我們研究噬菌體的活性時

體外培養

和

體內

16

,這些結果可能不會被複制,當我們的噬菌體 雞尾酒是給人類受試者服用的。儘管在任何臨床前研究中都有很有希望的數據,但我們的噬菌體技術可能會發現 在臨床試驗中研究時是有效的。

滿足FDA或同等的外國監管機構的要求 批准標準,我們必須在充分和良好控制的臨床試驗中證明我們的候選藥物是安全和 對它們的預期用途有效。臨床前試驗和早期臨床試驗的成功並不能確保以後的臨床試驗 審判將會成功。我們臨床前試驗的初步結果也可能不會被後來的分析或隨後的更大規模所證實 臨床試驗。製藥行業的一些公司在高級臨床試驗中遭受了重大挫折, 即使在早期的臨床試驗中獲得了有希望的結果,而且大多數開始臨床試驗的候選產品從未 批准用於商業銷售。

如果我們在招募患者方面遇到困難,我們的臨床 在臨床試驗期間,我們的臨床開發活動可能會被推遲或受到其他不利影響。

臨床試驗的完成取決於其他因素 情況取決於我們招收足夠數量的患者的能力,這是許多因素的函數,包括:

●

選擇用於評估的治療終點;

●

17

議定書中規定的資格標準;

●

| 產品候選產品在以下條件下的感知優勢 學習; | ● |

| 分析所需的患者數量 臨床試驗的治療終點; | ● |

我們招募臨床試驗研究人員的能力 以及具有適當能力和經驗的網站;

| ● | 我們獲得和維護患者同意的能力; 和 |

| ● | 其他臨床試驗對患者的競爭 治療。 |

| 我們已經經歷了,也可能會繼續經歷 在我們的臨床試驗中招募患者的困難,包括最近與我們的DFO第二階段研究的招募有關的困難,這 可能會增加成本或影響這些臨床試驗的時間或結果。在疾病方面尤其如此 患者人數相對較少。此外,我們試驗的潛在患者可能沒有得到充分的診斷或識別。 我們所針對的疾病,或者可能不符合我們研究的入學標準。 | 我們可能無法啓動或繼續臨床 如果我們找不到足夠數量的符合條件的患者參加FDA要求的臨床試驗 或同等的外國監管機構。此外,發現和診斷患者的過程可能會被證明是昂貴的。我們的無能 招募足夠數量的患者參加我們的任何臨床試驗都會導致嚴重的延誤,或者可能需要我們放棄 一項或多項臨床試驗。 |

| 延誤 在我們的臨床試驗中,可能導致我們無法達到預期的發展里程碑,增加成本和延誤 我們有能力獲得監管部門對我們候選產品的批准並將其商業化。 | 延誤 可能導致我們無法達到預期的臨床里程碑,並可能對我們的產品開發產生重大影響 成本和延遲監管部門對我們的候選產品的批准。計劃中的臨床試驗可能無法如期開始或完成, 或者根本就不是。 |

臨床 審判可能會因各種原因而被推遲,包括:

●

發展中的延誤 爲我們的候選產品提供製造能力,使其能夠在臨床試驗規模上實現一致的生產;

●

18

我們內部製造業務中的故障 導致我們無法持續和及時地生產足夠數量的噬菌體來支持我們的臨床試驗;

●

財政資源的可獲得性 並完成我們計劃的臨床試驗;

●

拖延與臨床研究人員達成共識 關於書房設計;

●

拖延與監管機構達成共識 進行試驗設計或獲得監管部門批准開始試驗的;

●

延誤臨床材料的獲取;

19

●

慢於預期的患者招募參與 在臨床試驗中;

●

監管限制或禁令(例如, 在不遵守網絡安全和數據隱私法的情況下來自監管當局);

●

臨床試驗地點、其他第三方的失敗 或我們遵守臨床試驗協議和/或試驗方案;

●

20

延遲就可接受的臨床治療達成協議 與預期地點簽訂試驗協議條款,或獲得IRB或獨立道德委員會的批准;以及

●

| 在我們的臨床過程中所經歷的不良安全事件 審判。 | 如果 如果我們不能如期成功開始或完成我們的臨床試驗,我們的證券價格可能會下跌。重要的臨床前研究 或者,臨床試驗延遲可能會縮短我們可能獨家擁有將我們的候選產品商業化的任何期限 或者允許我們的競爭對手在我們之前將產品推向市場,這可能會削弱我們成功實現商業化的能力 產品候選並損害我們的業務和運營結果。 |

| 我們的 當前或未來的候選產品可能會造成不良影響,可能會阻止其臨床開發,阻止其批准或 營銷,限制了他們的商業潛力,或導致嚴重的負面後果。 | 不利的 影響可能發生,並導致我們或監管機構中斷、推遲或停止臨床試驗,並可能導致更具限制性的 標籤或FDA或同等的外國監管機構延遲或拒絕上市批准。我們的試驗結果可能 表現出不可接受的嚴重程度和普遍的副作用或意外特徵。 |

| 如果 在我們的候選產品的開發過程中會產生不利影響,我們、FDA或同等的外國監管機構、IRBs或 我們進行研究的機構的獨立道德委員會,或者數據安全監測委員會可以暫停 或終止我們的臨床試驗,或者FDA或同等的外國監管機構可能拒絕批准我們的候選產品 任何或所有有針對性的適應症。 | 我們 打算繼續以第一階段臨床試驗的形式評估我們的候選產品的安全性和耐受性。雖然我們目前 未來的候選產品將在可能的範圍內,並在適用的情況下,在討論的條件下進行安全測試 有了監管部門,並不是所有藥物的副作用都是可以預測或預期的。可能會出現不可預見的不利影響 無論是在臨床開發期間,還是在我們的產品獲得監管部門批准後,如果這種不良反應較爲罕見, 批准的產品已經上市,導致更多患者暴露。例如,當我們篩選我們的噬菌體時 在試圖將安全問題降至最低的過程中,不能保證我們會消除出現毒力基因的風險, 我們噬菌體中的抗生素抗性基因、溶源基因、整合酶基因或其他毒性基因,或對我們噬菌體的不良反應 在病人的免疫系統中。到目前爲止,我們還沒有證明,我們也不能預測正在進行的或未來的臨床試驗是否會 證明我們的任何候選產品在人體內是安全的。此外,我們的候選產品還進行了臨床試驗。 在精心定義的同意進入臨床試驗的患者組中。因此,我們的臨床試驗有可能 可能表示候選產品的明顯正面效果大於實際正面效果(如果有的話),或者 未能識別不良的不利影響。 |

| 最終, 我們的部分或所有候選產品可能被證明對人類使用是不安全的。此外,如果發生以下情況,我們可能會承擔重大責任 任何志願者或患者因參與我們的臨床試驗而遭受或似乎遭受不良健康影響。任何 這些事件可能會阻止我們實現或保持市場對我們候選產品的接受度,並可能大幅增加 商業化成本。 | 我們 還沒有完成我們候選產品的成分開發。 |

| 這個 開發我們的候選產品需要我們分離、選擇、優化和組合許多針對所需目標的噬菌體 細菌是該產品的候選產品。爲我們的任何候選產品選擇噬菌體是基於各種因素,包括, 沒有限制,所選噬菌體組合成功殺死目標細菌的能力,交叉反應的程度 具有相同部分細菌靶標的單個噬菌體,組合噬菌體滿足監管要求的能力, 我們生產足夠數量的噬菌體的能力、第三方的知識產權等因素。而當 我們已經選擇了BX004的初始配方,不能保證這個初始配方將是最終配方 如果獲得批准,該產品的商業化候選名單。如果我們不能完成我們候選產品的配方開發 在我們預期的時間範圍內,然後是我們的產品開發時間表,以及我們產品候選的監管批准, 可能會被推遲。 | 我們 必須繼續爲我們的候選產品開發製造工藝,任何延誤或我們無法做到這一點,都將 導致我們臨床試驗的延遲。 |

| 這個 我們候選產品的製造工藝,以及臨床試驗中此類工藝的擴大,可能會帶來挑戰,以及 不能保證我們能夠及時完成這項工作,如果可以的話。開發或擴大過程中的任何延遲 這些製造過程中的一部分可能會推遲臨床試驗的開始,並損害我們的業務。爲了擴大我們的生產規模 爲了提高產能,我們需要建立更多的內部製造能力,與一個或多個合作伙伴簽訂合同,或者兩者兼而有之。我們的技術 而且我們的設備和工具的生產過程很複雜,我們在製造我們的 候選產品。例如,我們用來生產噬菌體的製造宿主可能包含一個或多個整合的噬菌體 它們的基因組,如果我們無法去除,可能會給生產出的噬菌體的生產帶來挑戰。不能保證 我們將能夠繼續在內部建設製造能力,或找到一個或多個合適的合作伙伴,或兩者兼而有之,以滿足 必要的數量和質量要求。隨着我們擴大生產規模,可能會出現製造和產品質量問題。 在建立或擴大我們的製造能力方面的任何延誤或無力,都可能削弱我們開發候選產品的能力。 | 2019年,我們建立了自己的製造工廠 在我們位於以色列內斯齊奧納的總部,我們已經執行了cGMP製造,這是我們第一次進行人類臨床研究。2021年3月, 我們搬進了位於以色列內斯齊奧納總部的一個新的製造工廠。在2024年期間,製造設施的使用 作爲公司戰略決策的一部分被擱置,臨床試驗材料被轉移到一家外包公司。我們有 如果需要,並在資金充足的情況下,可以選擇將我們自己的設施全面恢復GMP活動。在這種情況下,我們可能需要資助 對我們的製造工藝進行額外的修改,並進行額外的驗證研究。作爲備份,我們相信我們可以找到 可供選擇的製造設施。上述選項中的每一個都可能導致我們的巨額成本以及長達幾個月的延遲 獲得此類產品候選產品批准的時間長達數年。 |

| 如果 我們爲在該工廠生產的任何候選產品提交營銷申請,該製造工廠將是 接受持續的定期檢查,以了解是否符合歐洲、FDA和cGMP法規。遵守這些規定,並 標準是複雜和昂貴的,而且不能保證我們將能夠遵守。任何未能遵守適用的 法規可能導致實施制裁(包括罰款、禁令和民事處罰)、監管當局失職 對我們的候選產品授予市場批准、延遲、暫停或撤回批准、吊銷許可證、扣押或 召回候選產品或產品、運營限制和刑事起訴。 | 如果 我們的競爭對手能夠開發和銷售比我們更有效、更安全或更實惠的產品,或者獲得營銷 在我們批准之前,我們的商業機會可能是有限的。 |

21

競爭 在生物技術和製藥行業的投資非常激烈,而且還在繼續增加。一些規模更大、擁有顯著 比我們更多的資源正在積極地尋求我們正在尋求的適應症的開發計劃,包括傳統療法 以及具有新作用機制的治療方法。此外,其他公司正在開發基於噬菌體的治療性和非治療性產品。 用途,並可能選擇利用他們在噬菌體開發和製造方面的專業知識來嘗試開發與 我們的產品。

我們 還面臨來自學術機構、政府機構以及私營和公共研究機構的潛在競爭 在藥物和療法的發現和發展方面。我們的許多競爭對手擁有明顯更多的財務資源和專業知識 在研發、臨床前測試、進行臨床試驗、獲得監管批准、製造、銷售和 比我們做的更好。規模較小或處於早期階段的公司也可能被證明是重要的競爭對手,特別是通過協作 與大型和老牌製藥公司的安排。

在……裏面 在歐洲聯盟,潛在的競爭也來自醫院或藥劑師製造的藥物製劑,在沒有 營銷授權,通常指的是「複利」。在一些成員國,國家當局通常會促進 複方藥,以減少醫療費用。

我們的 競爭對手可能會成功地開發出更有效、副作用更少、更安全或更實惠的產品 我們的候選產品,這將使我們的候選產品競爭力降低或沒有競爭力,並將阻止授予或 被指定爲孤兒。這些競爭對手還與我們競爭,招聘和留住合格的科學和管理人員 人員,建立臨床試驗場地和臨床試驗病人登記,以及獲得技術和技術 許可證與我們的計劃相輔相成或對我們的業務有利。而且,能夠實現專利保護的競爭對手, 在我們之前獲得監管部門的批准並開始其產品的商業銷售,已經這樣做的競爭對手可能 享有顯著的競爭優勢。

我們 在確定或發現其他候選產品的努力中可能不會成功。

雖然 我們打算利用我們的技術來評估除了我們目前的候選產品之外的其他治療機會。 在開發過程中,我們可能會由於多種原因而無法確定其他可用於臨床開發的產品。例如,我們的研究 方法可能不能成功地確定潛在的候選產品,或者我們確定的那些可能被證明有有害的一面 使其無法銷售或不太可能獲得監管批准的效果或其他特徵。另外,我們可能無法 識別根除目標細菌的噬菌體,包括由於缺乏多樣性、無法 及時或完全獲取樣本,或樣本中的污染。我們在設計噬菌體雞尾酒時也可能會遇到困難 符合研究療法的要求,包括由於細菌對我們的噬菌體的抵抗力增強, 受噬菌體影響的宿主細菌的範圍,不同細菌生長狀態下活性的變化,毒性問題 在我們的噬菌體中,以及我們候選產品的穩定性、健壯性和製造簡易性方面。此外,還介紹了綜合佈線的設計。 工程噬菌體可能無法產生具有所需特性或適合使用的行爲的噬菌體 作爲可行的治療方法,或者可能導致包含免疫原性、毒性和其他安全問題等不良特徵的噬菌體。

22

一個 我們戰略的關鍵部分是利用我們的篩選技術來確定臨床開發中要追求的候選產品。如果 我們不能識別和開發其他潛在的候選產品,我們可能無法發展我們的業務和我們的運營結果 可能會造成物質上的傷害。這樣的候選產品在商業銷售之前將需要額外的、耗時的開發工作, 包括臨床前研究、臨床試驗和FDA和/或適用的外國監管機構的批准。所有候選產品 容易出現藥品開發固有的失敗風險。

法律 對合成生物學和基因工程的要求以及倫理和社會關切可能限制或阻止使用 我們的技術和限制我們的收入。

我們的 技術可能包括使用合成生物學和基因工程。在一些國家,使用轉基因藥物生產的藥物 生物體可能受到更嚴格的法律制度的約束,這可能被證明是複雜和非常具有挑戰性的,特別是對於 生命科學公司。例如,在歐洲聯盟,關於轉基因生物的規則除了適用於 關於藥品或者化妝品的一般規定。關於高級治療藥品的規定也可能適用。

另外, 公衆對合成生物學和基因工程的安全和環境危害的認知以及對其倫理問題的關注 可能會影響公衆對我們的技術、候選產品和工藝的接受程度。如果我們和我們的合作者不能 克服與合成生物學和基因工程有關的法律挑戰以及倫理和社會關切,我們的技術, 候選產品和工藝可能不被接受。這些挑戰和擔憂可能會導致費用增加、監管審查 以及加強監管,對我們候選產品的進口進行貿易限制,延遲或其他對我們計劃或 公衆對我們產品的接受程度和商業化程度。我們設計和生產具有可比或可比特性的候選產品 優於在自然產生的生物體或受控實驗室中發現的酶;然而,這種生物體的釋放 進入不受控制的環境可能會產生意想不到的後果。這種釋放產生的任何不利影響都可能產生一種物質 對我們的業務、財務狀況或經營結果產生不利影響,並可能對由此產生的任何後果承擔責任 傷害。我們 可能會花費我們有限的資源來追求特定的候選產品或適應症,但無法利用候選產品 或可能更有利可圖或更有可能成功的適應症。因爲 我們的財務和管理資源有限,我們打算專注於爲特定的適應症開發候選產品 我們認爲,從市場批准和商業化的潛力來看,它們最有可能成功。因此,我們 可能放棄或推遲尋求其他候選產品的機會或其他可能被證明具有更大商業價值的跡象 潛力。例如,我們花了大量的時間和資源開發BX005,但我們停止了。

我們的 資源分配決策可能導致我們無法利用可行的商業產品或有利可圖的市場機會。我們的 在當前和未來的研發計劃和特定適應症候選產品上的支出可能不會產生任何商業收益 可行的候選產品。如果我們不能準確評估特定候選產品的商業潛力或目標市場, 在下列情況下,我們可能會通過協作、許可或其他版稅安排向該候選產品放棄有價值的權利 對我們來說,保留候選產品的獨家開發權和商業化權利會更有利。

那裏 在我們的業務中,產品責任索賠是一個很大的風險。如果我們沒有獲得足夠的責任保險,就會產生產品責任 索賠可能會給我們帶來很大的債務。

我們的 業務使我們面臨開發、製造和營銷過程中固有的重大潛在產品責任風險 人類治療產品。無論是非曲直或最終結果,產品責任索賠都可能導致:

23

●

延遲或未能完成我們的臨床試驗;

●

臨牀試驗參與者的退出;

●

對我們的候選產品的需求減少;

●

24

損害我們的聲譽;

●

訴訟費用;

●

對我們不利的巨額金錢獎勵;以及

●

挪用關鍵部門的管理或其他資源 我們業務的各個方面。

如果 我們成功地營銷了產品,產品責任索賠可能會導致FDA或同等外國監管機構的調查 我們產品的安全性或有效性、我們的製造工藝和設施或我們的營銷計劃。這樣的調查可能 也可能導致召回我們的產品或更嚴重的執法行動,或對其適應症的限制 可以使用,或者暫停或撤回批准。我們 目前只有有限的臨床試驗保險單涵蓋某些地區的臨床試驗。我們打算擴大規模 我們的保險範圍包括商業產品的銷售,如果我們的候選產品或任何 我們可能開發的其他化合物。然而,保險覆蓋範圍很昂貴,我們可能無法將保險覆蓋範圍維持在 合理的成本或根本不合理,以及我們擁有或獲得的保險範圍可能不足以支付潛在的索賠或損失。我們的 僱員、獨立承包商、顧問、商業合作伙伴和供應商可能從事不當行爲或其他不正當活動, 包括不遵守監管標準和要求。

我們 暴露於我們的員工、獨立承包商、顧問、商業 合作伙伴和供應商。這些當事人的不當行爲可能包括故意、魯莽和/或疏忽的行爲,這些行爲不遵守 FDA和其他類似外國監管機構的法律,向FDA和其他機構提供真實、完整和準確的信息 類似的外國監管機構,遵守我們建立的製造標準,遵守醫療欺詐和濫用法律 在美國和類似的外國欺詐性不當行爲法律或報告財務信息或數據準確或披露 向我們提供未經授權的活動。如果我們的任何候選產品獲得了FDA的批准,並開始在 在美國,我們在此類法律下的潛在風險將顯著增加,我們與遵守 這樣的法律也可能會增加。除其他外,這些法律可能會影響我們目前與主要調查員的活動 和研究患者,以及建議和未來的銷售、營銷和教育計劃。

25

我們的 與開發基於噬菌體的產品所需的長時間相比,有限的運營歷史可能會使評估成功變得困難 評估我們目前的業務狀況,並評估我們未來的生存能力。

自.以來 BiomX Ltd.成立於2015年,幾乎將所有資源都投入到通過以下途徑開發具有噬菌體技術的候選產品上 其臨床前計劃,建立其知識產權組合,開發供應鏈,規劃其業務,籌集資金 併爲這些行動提供一般和行政支助。這樣的開發工作需要很長一段時間才能 他們可以被證明是成功的。我們還沒有證明我們有能力成功地完成任何臨床研究或其他關鍵的 臨床試驗,獲得監管批准,製造商業規模的產品,或安排第三方代表我們這樣做, 或進行成功的產品商業化所必需的銷售和營銷活動。因此,任何關於 如果我們有更長的運營歷史,我們未來的成功或生存能力可能不會像它們可能的那樣準確。

在……裏面 此外,作爲一家處於早期階段的公司,我們可能會遇到不可預見的費用、困難、併發症、延誤等已知和未知的情況 情況。當我們推進我們的候選產品時,我們需要從一家專注於研究的公司過渡到一家有能力的公司 支持臨床開發,如果成功,還可以支持商業活動。在這樣的過渡中,我們可能不會成功。

我們 可能需要擴大我們組織的規模,並且在管理這種增長時可能會遇到困難。

AS 我們的研究、開發、製造和商業化計劃和戰略,我們可能需要額外的管理、運營、 銷售、市場、財務等人員。未來的增長將使管理層成員承擔大量額外的責任, 包括:

●

確定、招聘、補償、整合、 維持和激勵更多的員工;

●

26

管理我們的內部研發工作 有效,包括確定臨床候選對象、擴展我們的製造流程以及在臨床和FDA之間導航 對我們的候選產品的審查流程;以及

●改善我們的運營、財務和管理 控制、報告系統和程序。, 我們的 未來的財務業績和我們將候選產品商業化的能力將部分取決於我們有效地 管理未來的任何增長,我們的管理層也可能不得不將不成比例的注意力從日常工作中轉移出去 活動,以便投入大量時間來管理這些增長活動。, 如果 我們無法通過僱傭更多的員工和擴大我們的顧問和承包商群體來有效地擴大我們的組織, 我們可能無法成功執行進一步開發和商業化我們的候選產品所需的任務,因此, 可能無法實現我們的研究、開發和商業化目標。, 風險 與政府管制和政府有關我們的 候選產品必須遵守嚴格的監管審批要求,這可能會推遲、阻止或限制我們的市場能力 或者開發我們的候選產品。我們頒發的專利可能不會提供商業化的基礎 可行的產品,或可能不爲我們提供任何競爭優勢,或可能受到第三方的挑戰;●其他人可能會繞過我們的專利要求來設計生產 超出我們專利範圍的有競爭力的產品;●

我們可能不會開發額外的可申請專利的專利 與我們的候選產品相關的技術;以及

●

我們依賴於被任命的人的勤奮。 國家管轄範圍內的代理人,代表我們行事,控制未決的國內和外國專利的起訴 申請和維護已授權的國內外專利。

一個 已頒發的專利並不保證我們有權實施專利技術或將專利產品商業化。第三方 可能擁有阻止我們將專利產品商業化和實踐專利技術的專利。 我們已頒發的專利和未來可能頒發的專利可能會受到挑戰、無效或規避,這可能會限制我們的能力 防止競爭對手銷售相同或相關的候選產品,或可能限制專利保護期的長度 我們的候選產品。此外,由於開發、測試和監管審查潛在技術需要大量時間 產品,在我們的任何候選產品可以商業化之前,任何相關的專利都可能到期或保留在 僅在商業化後的一小段時間內有效,從而削弱了專利的任何優勢。專利期限延長可能不會 可以獲得這些專利。

我們的 我們的候選產品和專有產品平台的開發和商業化權利可能在一定程度上受制於條款和 其他人授予我們的當前和未來許可證的條件。

一些人 我們被許可的權利可以爲我們的產品和服務的各個方面提供運營的自由。我們可能需要獲得額外的 從其他公司獲得許可,以推進我們的研究、開發和商業化活動。

糾紛 在遵守許可協議的前提下,我們和我們的許可人之間可能會產生知識產權問題,包括:

●

根據許可協議授予的權利範圍 和其他與口譯有關的問題;

●

27

我們的產品、服務、 技術和工藝侵犯許可方不受許可協議約束的知識產權的;

●

我們將專利和其他權利再許可給 合作發展關係下的第三方;

●

我們在許可協議下的盡職義務 以及哪些活動滿足這些勤勉義務;

●

| 我們 依靠商業祕密等形式的非專利知識產權保護。如果我們不能保護我們的商業祕密, 其他公司或許能夠更有效地與我們競爭。 | 我們 依靠商業祕密來保護我們技術的某些方面,包括我們製造和提純的專有工藝 噬菌體。商業祕密很難保護,特別是在製藥行業,那裏的許多信息都是關於 產品必須在監管審批過程中公開。儘管我們盡了合理的努力來保護我們的商業祕密, 我們的員工、顧問、承包商、外部科學合作者和其他顧問可能無意或故意披露 將我們的信息提供給競爭對手。執行第三方非法獲取和使用我們的商業祕密信息的索賠是 費用昂貴,耗時長,結果難以預料。此外,美國以外的法院可能不太願意 或者可能不保護商業祕密。此外,我們的競爭對手可以自主開發同等的知識、方法和訣竅。 |

| 如果 我們被起訴侵犯第三方的知識產權,或者如果我們被迫進行干預程序, 這將是昂貴和耗時的,訴訟或干預中的不利結果將產生實質性的不利影響 在我們的生意上。 | 我們的 我們將候選產品商業化的能力取決於我們開發、製造、營銷和銷售我們候選產品的能力 而不侵犯第三方的專有權。擁有大量美國和外國專利和專利申請 存在於抗感染產品的一般領域或可能與我們的候選產品相關的領域。 如果我們被證明侵犯了專利權,如果我們不能證明專利 是無效的。此外,由於專利申請可能需要很多年的時間才能發佈,因此目前可能有正在審理的專利申請, 我們不知道,這可能會導致我們的候選產品可能會侵犯已頒發的專利,或者可能會觸發干擾程序 關於我們擁有或許可的某項專利或申請。也可能有我們不知道的現有專利,我們的 候選產品可能無意中侵權或可能捲入干擾程序。 |

| 這個 生物技術和製藥行業的特點是大量專利的存在和頻繁的訴訟基礎 關於專利侵權的指控。只要我們的候選產品處於臨床試驗階段,我們就相信我們的臨床活動 屬於美國《美國法典》第35編第271(E)條規定的豁免範圍,該條款免除專利侵權 合理地與開發和向FDA提交信息相關的責任活動。因爲我們的臨床研究 候選藥品走向商業化,對我們提出專利侵權索賠的可能性增加。而當 我們試圖確保我們的活性臨床研究藥物和我們用於製造它們的方法以及方法 對於它們的使用,我們打算推廣,不侵犯他人的專利和其他專有權,我們不能確定它們 否則,競爭對手或其他方可能會聲稱我們在任何情況下侵犯了他們的專有權。 | 我們 可能會面臨未來的訴訟,因爲我們的候選產品、我們使用的製造方法或用途 爲此,我們打算推動他們侵犯他人的知識產權。我們製造和商業化的能力 我們的候選產品可能取決於我們是否有能力證明我們採用的製造工藝和我們產品的使用 候選人不侵犯第三方專利。如果第三方專利被發現涵蓋我們的候選產品或其使用或製造, 我們可能會被要求支付損害賠償金或被禁止,因此無法將我們的候選產品商業化,除非我們獲得了 駕照。我們可能無法以可接受的條款獲得許可證(如果有的話)。 |

| 我們 可能會受到我們員工對轉讓的服務發明權的報酬或特許權使用費的索賠,這可能會導致 並對我們的業務造成不利影響。 | 一個 我們的很大一部分知識產權是我們的員工在爲我們工作的過程中開發的。在……下面 以色列專利法,5727-1967,或專利法,由僱員在期限內構思的發明,作爲 他或她受僱於一家公司被認爲是「職務發明」,屬於僱主,沒有特定的 僱員和僱主之間授予僱員職務發明權的協議。專利法還規定,如果有 在僱主和僱員之間沒有這樣的協議,以色列補償和特許權使用費委員會,一個由 專利法將確定勞動者是否有權因其發明而獲得報酬。我們一般都會進行轉讓 與我們的員工簽訂的發明協議,根據該協議,這些個人向我們轉讓在 他們受僱或受僱於我們的範圍。雖然我們的員工已同意轉讓我們的職務發明權,但我們可能 面臨要求對指定發明支付報酬的索賠。作爲此類索賠的結果,我們可能被要求 向我們的現任或前任僱員支付額外的報酬或特許權使用費,或被迫就此類索賠提起訴訟,這可能會帶來負面影響 影響我們的業務。 |

| 風險 與我們對第三方的依賴有關 | 我們 依賴並繼續依賴第三方進行我們的臨床試驗,這些第三方的表現可能不令人滿意, 包括未能在最後期限前完成這類審判。 |

| 我們 繼續依賴第三方,如合同研究組織或CRO和臨床研究人員進行和管理 我們的臨床試驗。 | 我們的 依賴這些第三方進行研發活動將減少我們對這些活動的控制,但不會減輕 讓我們明白我們的責任。例如,我們仍然有責任確保我們的每一項臨床試驗都是按照 以及審判的總體調查計劃和方案。此外,FDA要求我們遵守GCPs進行, 記錄和報告臨床試驗的結果,以確保數據和報告的結果是可信和準確的,並且 審判參與者的權利、安全和福利受到保護。其他國家的監管機構也有要求 我們必須遵守的臨床試驗。我們還被要求登記正在進行的臨床試驗並公佈已完成的結果 在指定的時間框架內,在政府贊助的數據庫Clinicaltrials.gov中進行臨床試驗。如果不這樣做,可能會導致 罰款、負面宣傳以及民事和刑事制裁。 |

| 此外, 這些第三方也可能與其他實體有關係,其中一些可能是我們的競爭對手。如果這些第三方這樣做 未成功履行合同職責、未在預期的最後期限前完成工作、遭遇停工、終止合同 與我們合作或需要更換,或未根據法規要求或我們聲明的方案進行臨床試驗, 我們可能需要與替代的第三方達成新的安排,這可能是困難、昂貴或不可能的,而我們的臨床 審判可能會延長、推遲、終止或需要重複。如果發生上述任何一種情況,我們可能無法獲得或 在獲得我們的候選產品的營銷批准方面可能會被推遲,並且可能無法或可能在我們的努力中被推遲 成功地將我們的候選產品商業化。 | 我們 我們的臨床試驗也依賴於其他第三方來存儲和分發藥品供應。在以下方面出現性能故障 我們的經銷商可能會推遲我們候選產品的臨床開發或營銷批准,或者我們產品的商業化, 造成額外的損失,剝奪了我們潛在的產品收入。 |

| 第三方 關係對我們的業務很重要。如果我們無法維持我們的協作或建立新的關係,或者如果這些 如果關係不成功,我們的業務可能會受到不利影響。 | 我們 產品開發能力有限,尚無任何銷售、營銷或分銷能力。因此, 我們與其他公司和學術機構建立關係,爲我們提供重要的技術,我們可能會收到 未來在這些和其他合作下的更多技術和資金。我們進入的關係可能會帶來許多 風險,包括以下方面: |

28

●

第三方已經和未來的第三方合作者 在確定他們將應用的努力和資源方面可能有很大的自由裁量權;

●

| 當前和未來的第三方可能不會履行其 如預期的義務; | 我們 目前依靠外部供應商提供原材料和其他重要零部件,如實驗室設備。此外,我們的臨床 由於我們目前的GMP設施被擱置,試驗材料正在通過外包合同製造操作進行生產。我們 尚未導致任何候選產品進行商業規模的製造或加工,並且可能無法對任何 我們的候選產品。我們將在工作中進行更改,以優化我們的候選產品的製造過程,我們 不能確定即使是過程中的微小變化也會導致安全有效的治療。 |

| 這個 用於生產我們候選產品的設施必須得到fda或同等的外國監管機構的批准。 在我們向FDA或同等的外國監管機構提交營銷申請後,將進行檢查。另外, 任何用於生產用於非治療用途的商業候選產品的設施將受到 FDA和外國監管機構。我們目前並不控制製造過程的所有方面,目前主要是 依賴於我們的合同製造合作伙伴遵守法規要求,稱爲cGMP要求,用於製造 我們的候選產品。如果我們的生產設施開始運作,我們將負責遵守cGMP。 要求。如果我們或我們的合同製造商不能成功地按照我們的規格和嚴格的 FDA或其他監管機構的監管要求,我們和他們將無法確保和/或維持監管 批准他們的製造設施來製造我們的候選產品。此外,我們無法控制 我們的合同製造商是否有能力保持足夠的質量控制、質量保證和合格的人員。如果 FDA或同等的外國監管機構不批准這些設施用於生產我們的候選產品,或者如果 它撤回了未來的任何此類批准,我們可能需要尋找替代的製造設施,這將嚴重影響 如果我們的候選產品獲得批准,我們有能力開發、獲得監管部門的批准或將其推向市場。 | 我們 生產我們的候選產品用於治療適應症或非治療性臨床試驗的經驗有限 臨床研究或試驗。2019年,我們在以色列內斯齊奧納的總部開設了自己的製造工廠,但目前 已經被擱置了。我們不能向您保證,我們可以按照規定生產我們的候選產品,成本或 使它們在商業上可行所需的數量。 |

| 我們的 候選產品依賴於特殊原材料的可用性,這些原材料可能無法以可接受的條款提供給我們,或者根本無法獲得。 | 我們的 候選產品需要特定的特殊原材料,其中一些是從資源和經驗有限的小公司那裏獲得的 來支持一個商業產品。這些第三方供應商可能無法滿足我們的需求,特別是在非常規情況下 比如FDA的檢查或醫療危機,比如大範圍的污染。我們目前還沒有與所有 我們可能在任何時候需要的供應商,如果需要,可能無法以可接受的條款或根本無法與他們簽訂合同。 因此,我們可能會在接收支持臨床或商業生產的關鍵原材料方面遇到延誤。 |

| 風險 與我們的普通股相關 | 一個 本公司相當數量的普通股在行使已發行認股權證和期權或轉換時須予發行 在行使或轉換(視情況而定)我們的可轉換優先股時,可能會導致我們的證券持有人的股權被稀釋。 |

| 截至2024年12月31日,我們有未償還的認股權證 購買總計12,296,430股普通股,加權平均行權價爲4.34美元,或全部購買, 未清償認股權證,每種情況下均可進行調整。在行使該等未償還認股權證的範圍內,額外股份 將發行我們的普通股,這將導致普通股的現有持有者被稀釋,並增加普通股的數量 有資格在公開市場上轉售的股票。在公開市場上出售大量此類股票可能會對 影響我們普通股的市場價格。 | 在……裏面 此外,截至2024年12月31日,我們擁有購買2,002,365股普通股的未歸屬和未歸屬期權。至 只要這些選項中的任何一個被行使,普通股的額外股份將被髮行,這些普通股通常有資格轉售 在公開市場上(受證券法第144條對我們關聯公司持有的股票的限制), 這將導致我們的證券持有人的股權被稀釋。 |

| 自2025年3月20日起及之後的2025年2月SPA(定義爲 ),我們擁有已發行的認股權證,以加權平均方式購買總計14,391,386股普通股 售價2.97美元。 | 我們 可能在未來發行額外的期權、認股權證和優先股。此外,增發 我們的普通股在行使此類證券時,將導致對當時普通股現有持有人的攤薄 也可能對我們普通股的市場價格產生不利影響。 |

我們 我們從未對我們的普通股支付過股息,並且我們預計在可預見的時間內不會對我們的普通股支付任何現金股息 未來。

29

我們 從未在我們的普通股上宣佈或支付現金股息。我們預計不會在年內就我們的普通股支付任何現金股息 可預見的未來。我們目前打算保留所有可用資金和任何未來收益,爲發展和增長提供資金 我們的生意。因此,我們普通股的資本增值,如果有的話,將成爲我們股東的唯一收益來源 可預見的未來。

我們 未來可能無法維持我們證券的上市。

我們的 普通股在紐約證券交易所美國證券交易所交易,該交易所對上市股票施加持續上市要求。如果我們不能滿足 繼續上市的標準,例如,我們的股票在很長一段時間內不得交易的要求 或未能滿足股東權益要求,以及其他要求,紐約證券交易所美國人可能會發行 不合規函或啓動退市程序。如果我們的普通股退市,我們可能面臨重大不利因素 後果,包括:

●

我們的市場報價有限 證券;

●我們證券的流動性減少;●我們 高度依賴我們的首席執行官喬納森·所羅門以及我們管理層的其他主要成員,科學 和臨床團隊。雖然我們已經與我們的執行人員簽訂了僱傭協議,但他們每個人都可以終止他們的 任何時候都可以和我們一起工作。我們不爲我們的任何高管或其他員工提供「關鍵人物」保險。這個 失去我們的任何高管、其他關鍵員工和其他科學和醫療顧問的服務,以及我們無法 尋找合適的替代品可能會導致產品開發的延誤,並損害我們的業務。此外,我們最近收購的 APT的合併及其與公司業務的整合可能會增加員工在可預見的未來離職的可能性。我們的 繼續吸引、留住和激勵高素質的管理、臨床和科學人員,以及我們發展的能力 與領先的學術機構、臨床醫生和科學家保持重要的關係對我們的成功至關重要。競爭 對生物技術領域的合格人員的需求很大,特別是在我們總部所在的以色列。我們面臨着競爭 對於來自其他生物技術和製藥公司、大學、公共和私營研究機構以及其他機構的人員 組織。我們還面臨着來自其他資金更雄厚、更成熟的企業的競爭,我們也可能被視爲風險更高的企業 從工作穩定性的角度進行選擇,因爲我們的地位相對較新,而不是那些存在時間較長的生物技術和製藥公司。 考慮到對人才的競爭,我們可能無法以可接受的條件吸引和留住合格的人員。如果我們是 如果我們的留住、激勵和招聘努力不成功,我們可能無法執行我們的業務戰略。

30

期望值 與環境、社會和治理(ESG)項目相關的項目可能會增加成本,並使我們面臨新的風險。

| 那裏 某些投資者和其他主要利益相關者對公司責任的關注日益增加,特別是與 環境、社會和治理,或ESG,因素。因此,企業責任評級越來越受到重視。 一些第三方提供關於公司的報告,以衡量和評估公司的責任表現。此外, 評估公司企業責任實踐的ESG因素可能會發生變化,這可能會導致更大的期望 並導致我們採取代價高昂的舉措來滿足這些新標準。或者,如果我們不能滿足這種新的 投資者可能會得出這樣的結論,即我們在企業責任方面的政策不夠充分。我們冒着損害我們品牌的風險 如果我們的企業責任程序或標準不符合不同選民設定的標準,我們就會受到損害。我們可以 需要在與ESG相關的事項上進行投資,這可能是重大的,並對我們的運營結果產生不利影響。 此外,如果我們的競爭對手的企業責任表現被認爲比我們的更大,無論是潛在的還是目前的 投資者可能會選擇與我們的競爭對手一起投資。此外,如果我們傳達有關ESG的某些倡議和目標 我們可能在實現這些倡議或目標的過程中失敗,或者被認爲失敗,或者我們可能因爲範圍太廣而受到批評 這樣的倡議或目標。如果我們未能滿足投資者和其他關鍵利益相關者的期望,或者我們的倡議不是 如果按計劃執行,我們的聲譽和財務業績可能會受到實質性的不利影響。 | 如果 我們從事未來的收購或戰略合作,這可能會增加我們的資本要求,稀釋我們的股東,導致 使我們招致債務或承擔或有債務,並使我們面臨其他風險。 |

| 在……上面 2024年3月15日,我們收購了APT。我們可能會評估各種額外的收購機會和戰略伙伴關係,包括許可 或獲得互補的產品、知識產權、技術或業務。任何潛在的收購或戰略 夥伴關係可能會帶來許多風險,包括: | ● |

| 業務費用和現金需求增加; | ● |

| 承擔額外的債務或或有債務 負債; | ● |

| 發行我們的股權證券; | ● |

| 業務同化、知識產權和 被收購公司的產品,包括與整合新人員有關的困難; | ● |

| 我們管理層的注意力從 我們現有的產品計劃和倡議,以尋求這樣的戰略合併或收購; | ● |

留住關鍵員工,流失關鍵人員 以及我們維持關鍵業務關係的能力的不確定性;

31

●

與另一方相關的風險和不確定性 此類交易,包括該締約方及其現有產品或候選產品的前景和營銷批准; 和

欲了解更多信息 信息,請參閱“

風險因素-我們的業務和運營將在計算機系統故障、網絡攻擊的情況下受到影響 或者我們的網絡安全方面的缺陷。

| “在本年度報告第1A項中。我們維持一份網絡責任保險單。然而, 我們的網絡責任保險單可能不包括對我們提出的所有索賠,而爲訴訟辯護,無論其是非曲直,都可能是 成本高昂,分散了管理層對我們業務和運營的注意力。 | 項目 2.物業 |

| 我們的公司總部設在內斯。 齊奧納,以色列。我們的設施有28,610平方英尺的辦公和實驗室空間,其中包括6,500平方英尺的製造 區域。租賃協議將於2025年11月到期,有權將租期延長五年。該設施的設計採用了 具有臨床批量生產臨床開發所需的候選產品的能力。2022年8月,BiomX以色列 簽訂了一份轉租協議,將其在以色列內斯齊奧納的部分辦公空間轉租出去。轉租協議於2024年9月結束。 | 在……裏面 除了我們在以色列的辦公場所外,我們還在馬里蘭州蓋瑟斯堡租賃了一個25,894平方英尺的辦公和實驗室設施, 包括6,100平方英尺的製造設施。租賃協議將於2034年7月到期,並有權在2月份終止 2029年,以12個月通知和提前解約費爲準。2024年12月,我們決定停止使用這處房產 馬里蘭州蓋瑟斯堡,並將其轉租。 |

| 我們 相信我們的設施足以滿足我們目前的需求。 | 項目 3.其他法律程序 |

| 我們 可能會不時受到法律程序、調查和與我們的業務運作相關的索賠。我們不是 目前是針對我們提起的任何重大訴訟或其他重大法律程序的一方。 | 項目 4.披露礦場安全情況 |

不 適用。

零件 第二部分:

項目 5.註冊人普通股票市場、相關股東事項和發行人購買股票證券

32

我們的 普通股在紐約證券交易所美國證券交易所交易,代碼爲PHGE。

持有者 記錄的

AS 截至2025年3月20日,77名登記在冊的股東持有24,966,053股我們普通股的已發行和流通股。數字 記錄持有者的數量是根據我們的轉讓代理的記錄確定的,不包括普通股的受益所有者 其股份以各種證券經紀人、交易商和註冊結算機構的名義持有。

| 分紅 | 我們沒有對我們的普通股支付任何現金股息 到目前爲止的股票,不打算支付現金股息。未來現金股利的支付將取決於我們的收入 以及收益(如果有的話)、資本要求和一般財務狀況。任何現金股利的支付將在酌情權之內。 在這個時候,我們的董事會,或者說董事會。此外,如果我們負債累累,我們宣佈分紅的能力可能會進一步 受到我們可能同意的與之相關的限制性契約的限制。 |

| 項目 6.[保留。] | 項目 7.管理層對財務狀況和運營結果的討論和分析 |

| ● | 與臨床前相關的費用 我們候選產品的臨床開發,包括與第三方的協議,如CRO和合同製造 各組織以及提供科學發展服務的顧問、分包商和主要意見領袖; |

| ● | 製造規模擴大費用和採購成本 並製作臨床前和臨床試驗材料; |

| ● | 許可證維護費和里程碑費用 與各種許可協議有關的; |

| ● | 與員工相關的費用,包括工資,相關 從事研發職能的員工以及外部員工的福利、差旅和基於股票的薪酬支出 費用,如向從事這類活動的外部顧問支付的費用; |

| ● | 與遵守法規要求有關的成本 以及與專利事宜有關的法律費用;以及 |

| ● | 折舊及其他費用。 |

我們 根據使用所提供的信息對完成特定任務的進展情況的評估,確認外部開發成本 由我們的服務提供商提供給我們。

33

我們 不要將員工成本或設施費用(包括折舊或其他間接成本)分配給特定計劃,因爲這些成本 成本部署在多個計劃中,因此不單獨分類。我們主要使用內部資源來監督 研究和發現以及管理我們的臨床前開發、工藝開發、製造和臨床開發 活動。這些員工在多個計劃中工作,因此,我們不會按計劃跟蹤他們的成本。

這個 下表彙總了我們按計劃產生的研發費用:

年 告一段落

十二月三十一日,

以千爲單位的美元

BX004

| BX211 | 收入 私募股權證公允價值的變化反映了私募股權會計導致的重新估值 根據2024年3月PIPE發出的令。 |

| 金融 費用,淨額 | 金融 淨費用主要包括與外幣重新估值相關的收入或費用以及銀行存款的利息收入 和貨幣市場基金。 |

| 結果 運營部 | 比較 截至2024年和2023年12月31日的年份 |

| 的 下表總結了截至2024年和2023年12月31日止年度的綜合經營業績: | 年 結束 |

34

| 12月31日, | 以千爲單位的美元 |

| 研發費用,淨 | 一般和行政費用 |

| 商譽減值 | IPR & D損害 |

| 長期資產減損 | 經營虧損 |

| 其他收入 | 利息支出 |

| 財務費用(收入),淨額 | 私人公允價值變動收入 安置令 |

| 稅費用 | 政府 贈款和相關版稅 |

| 這個 以色列政府通過國際投資協會,通過提供贈款來鼓勵研究和發展項目。我們可能會從 研究委員會規定的研究和開發費用的20%至50%的比率 國際保險業協會。截至2024年12月31日,我們已收到國際保險業協會以贈款形式提供的總計800美元的萬。BiomX有限公司是 作爲FutuRx孵化器的一部分成立的孵化器公司,在2017年前,其大部分資金來自IIA贈款和 由孵化器提供資金,該孵化器得到國際投資協會的支持。離開孵化器後,我們繼續申請和接受IIA贈款。 對這類資助的要求和限制見《研究法》。根據研究法,版稅爲3%至3.5% 銷售全部或部分使用這些內部投資協定贈款開發的產品或服務所得的收入應支付給以色列政府。 我們開發了我們的兩種平台技術,至少部分是用這些贈款的資金開發的,因此,我們將有義務 對我們任何獲得監管部門批准的候選產品的銷售支付這些版稅。 | 以下 描述了我們根據《研究法》從IIA獲得的撥款方面的義務: |

本地 製造義務

AS 只要我們候選產品的製造是在以色列進行的,並且沒有任何由IIA贈款資助的技術被出售或獲得許可 向非以色列實體支付的特許權使用費的最高總額一般不會超過向我們提供的贈款的100%,外加年息。 相當於適用於美元存款的12個月SOFR,在每個日曆年的第一個工作日公佈。

在……下面 根據《研究法》的條款,產品可以由我們或其他實體在以色列境外製造,前提是事先獲得批准 從IIA收到(轉移總計不超過10%的製造產能不需要這種批准,在 在這種情況下,必須向國際保險業協會提供通知,而國際保險業協會不得在通知後30天內提出反對)。

專有技術 轉賬限制

這個 《研究法》限制了將IIA資助的技術訣竅轉移到以色列境外的能力。將國際投資機構資助的專有技術轉移到國外 必須事先獲得國際投資協定的批准,並可能需要向國際投資協定支付款項,按照下列條款提供的公式計算 《研究法》。贖回費的上限是國際保險業協會贈款總額的6倍,外加應計利息。 (即對國際保險業協會的總負債,包括應計利息,乘以6)。如果我們希望轉讓IIA資助的技術訣竅, 批准條款將根據交易的性質和向我們支付的與以下項目有關的對價而確定 這樣的轉移。

批准 只有在接受者遵守研究規定的情況下,才能批准將IIA資助的專有技術轉讓給另一家以色列公司 法律和相關條例,包括對向以色列境外轉讓專有技術和製造權的限制。

35

變化 的控制力

任何 非以色列公民、居民或實體,除其他外,(I)成爲我們5%或更多股本或投票權的持有者, (Ii)有權委任本公司董事或行政總裁,或(Iii)擔任本公司董事或行政總裁 高級職員(包括在該直接持有人中擁有25%或以上投票權、股權或提名董事的權利(如適用的話)) 必須通知國際保險業協會,並承諾遵守適用於國際保險局贈款計劃的規則和條例,包括 上述對轉讓的限制。批准 在以色列境外製造產品或同意轉讓IIA資助的專有技術,如有要求,可由 內審局。此外,國際投資協會可能會對它允許我們轉讓國際投資協會資助的專有技術的任何安排施加某些條件。 或者是以色列的製造業。這個 我們的股東在未來的交易中可獲得的對價,涉及向以色列境外轉讓與 國際投資協會的資金(如合併或類似交易)可能會減少我們需要向國際投資協會支付的任何金額。AS 截至2024年12月31日,並未產生任何銷售,以及我們對未來承諾的本金和利息餘額 向國際保險局支付的款項總額約爲830万,而截至2023年12月31日,支付給IIA的萬爲790美元。作爲資助我們目前 和計劃的產品開發活動,我們可以提交後續的撥款申請,以獲得新的撥款。展望

我們 預計我們與正在進行的活動相關的費用將基本保持在相同的水平。我們的開支仍將相當可觀 並且還可能隨着我們:

●

繼續發展…… 我們的產品候選;

| ● | 完成支持IND的活動 並準備爲我們的候選產品啓動臨床試驗; |

| 項目 90亿。和其他信息 | 發放花紅 |

| 2025年3月24日,董事會批准支付應支付的獎金 現金,相當於我們的首席執行官、首席財務官和首席開發部每個人三個月的工資 幹事,數額分別爲102 000美元、55 000美元和64 000美元。在支付獎金時,非法定遣散期 根據與公司達成的協議,每名這類人員的任期將縮短三個月。 | 交易 安排 |

| 在.期間 截至2024年12月31日的三個月,我們的董事或高級管理人員 | 通過 |

| 或 | 終止 |

| 《規則10b5-1交易安排》 或「非規則10b5-1交易安排」,因爲每個術語在S-K條例第408(A)項中定義 | 項目 9C。關於妨礙檢查的外國司法機關的披露 |

| 不 適用因 | 零件 (三) |

項目 10.董事、行政人員及公司管治

以下列出的是這些人的姓名、年齡和職位 截至2025年3月25日,擔任我們的執行幹事和董事會成員的每一位個人。

36

名字

年齡

位置

| 行政人員 | 喬納森·所羅門 |

| 首席執行官兼董事 | 瑪麗娜·沃爾夫森 |

| 首席財務官 | Merav Bassan博士 |

| 首席發展官 | 非僱員董事 |

| 拉塞爾·格雷格博士(1)(2)(3) | 董事兼董事長 |

| 蘇珊·布魯姆(1) | 董事 |

| 傑西·古德曼博士(3) | 董事 |

| 喬納森·萊夫(2) | 董事 |

| 格雷戈裏·梅里爾(3) | 董事 |

| 艾倫·摩****(2) | 主任 |

| 愛德華·威廉姆斯(1) | 董事 |

審核委員會成員

37

每位非員工董事還將獲得一份年度 授予購買我們普通股的期權。每個年度期權獎的四分之一在授予之日的一週年時授予, 年度期權獎勵的剩餘部分分12個等額的季度分期付款,但須受董事的持續服務限制 在董事會上。該公司的政策是根據薪酬顧問的建議等授予期權。

2024年,公司向董事授予期權 根據以下結構:17,600份期權發給連續的非僱員董事,26,400份期權(上述贈款的150%)發給 新任命的非僱員董事,以及董事會主席的35,200項選擇。

這個 下表列出了有關本公司獨立非僱員董事於 截至2024年12月31日止年度,以表揚他們在本公司董事會的服務。董事的喬納森·所羅門先生也是我們的員工,他沒有收到額外的 他作爲董事服務的補償,沒有列在下表中:

名字

賺取的費用或

以現金支付

選項

38

獎

所有其他

補償

總計

拉塞爾·格里格博士

蘇珊·布魯姆

邁克爾·丹巴赫

傑西·古德曼

喬納森·萊夫

39

傑森·馬克斯

格雷格·梅里爾

艾倫·摩****

林恩·沙利文

董事和指定執行官

喬納森·所羅門

瑪麗娜·沃爾夫森

梅拉夫·巴桑博士

蘇珊·布魯姆

40

傑西·古德曼博士

羅素·格里格博士

| 喬納森·萊夫 | 格雷戈裏·梅里爾 |

| 阿蘭·摩西醫生 | 愛德華·威廉姆斯 |

| 全體董事和高級管理人員(10人) | 不到1%。 |

| 除非另有說明,否則 每個人的營業地址是c/o BiomX Inc.,愛因斯坦大街22號,4號 | 日 |

| 內斯·齊奧納7414003號,以色列。 | 基座 關於向公司提供的某些信息以及2025年3月4日提交給美國證券交易委員會的附表13G/A。代表2,494,109 普通股,不包括(I)轉換X系列13,088股優先股後可發行的1,308,800股普通股 股票(受9.99%的受益所有權限制),(2)1,081,750股可在私人公司行使時發行的普通股 配售普通權證(受9.99%的實益所有權限制),(3)1,174,859股普通股 行使新認股權證(受制於9.99%的實益所有權阻滯權)。(四)行使可發行普通股375,399股 經修訂及重訂的認股權證(受惠所有權阻止人規限);(V)可於行使時發行的583,237股普通股 私募預籌資權證(受惠所有權限制爲9.99%)及(Vi)591,622股普通股 可在行使已登記的預融資權證時發行(受9.99%的實益所有權限制)。這樣的私募 普通權證、新權證和私募預籌資權證只有在股東批准後才可行使。 |

| 這個 囊性纖維化基金會的地址是蒙哥馬利大道4550號。馬里蘭州貝塞斯達1100N套房,郵編:20814。 | 基座 關於向本公司提供的某些信息以及在2024年11月13日提交給美國證券交易委員會的附表13G上,由 南塔哈拉資本管理公司,或南塔哈拉,威爾莫特·B·哈基和Daniel·麥克。代表2,494,109股普通股。不包括 (I)在行使新認股權證時可發行的普通股865,300股(實益擁有權限制爲9.99%), (Ii)424,191股可在行使私募普通權證時發行的普通股(以實益擁有權爲準 (Iii)101,791股可於行使經修訂及重訂的認股權證後發行的普通股(受惠 所有權限制),(Iv)210,582股可在行使私募預籌資權證時發行的普通股(主題 至9.99%的實益所有權限制),以及(V)213,609股可在行使登記預籌資金時發行的普通股 認股權證(受限於9.99%的實益所有權限制)。這種定向增發普通權證、新權證和定向增發 預先出資的認股權證只有在股東批准後才能行使。 |

| AS 南塔哈拉的管理成員、Harkey先生和Mack先生可能被視爲報告的證券的實益擁有人 在此由南塔哈拉持有。南塔哈拉、哈基和麥晉桁對報告的證券擁有處置權和投票權 在這裏。南塔哈拉的地址。南塔哈拉、哈基和麥克住在康涅狄格州新嘉楠科技大街130號,郵編:06840。 | 基座 關於向本公司提供的某些信息以及於2025年3月3日聯合提交給美國證券交易委員會的附表13D/A,由(I) Deerfield Private Design Fund V,L.P.或Deerfield Private Design V,(Ii)Deerfield Management V,L.P.或Deerfield Management V,(Iii)Deerfield 醫療保健創新基金II,L.P.,或Deerfield HIF II,(Iv)Deerfield Management HIF II,L.P.,或Deerfield Management HIF II,(V)Deerfield 管理公司,L.P.或Deerfield Management,以及(Vi)詹姆斯·E·弗林,或統稱爲Deerfield。代表(I)1,247,054 由Deerfield Private Design V和Deerfield HIF II直接持有的普通股,或統稱爲這兩個基金,以及(Ii) 轉換X系列優先股後可發行的普通股總數爲1,385,463股(受制於9.99% 受益所有權限制)由基金直接持有,以及在行使某些認股權證後可發行的普通股 (受9.99%的受益所有權限制),可在2025年3月20日行使,或將在 60天后,由基金持有。 |

不包括 轉換X系列優先股後可發行的普通股總數爲5,146,706股(受惠9.99% 所有權限制),以及在行使某些認股權證時可發行的普通股。其中一些認股權證將僅可行使 在股東批准後,或受9.99%的受益所有權限制。

先生。 弗林是Deerfield Management V、Deerfield Management HIF II和Deerfield Management各自的普通合夥人的管理成員。 Deerfield Management V是Deerfield Private Design Fund V的普通合夥人,L.P.Deerfield Management HIF II是 Deerfield Healthcare Innovation Fund II,L.P.和Deerfield Management是每個基金的投資經理。因此,迪爾菲爾德 管理層和弗林對這些基金持有的證券擁有共同的投票權和處置權,Deerfield Management V對Deerfield Private Design V和Deerfield Management持有的證券擁有共同投票權和共同處置權 HIF II對Deerfield HIF II持有的證券共享投票權和共享處置權。Deerfield的地址是 紐約公園大道南345號,12樓,郵編:10010。

41

基座 關於向公司提供的某些信息以及OrbiMed於2024年7月17日向美國證券交易委員會聯合提交的附表13G/A 以色列生物基金GP Limited Partnership,或OrbiMed Biofund,OrbiMed以色列GP Ltd.,或OrbiMed以色列,卡爾·L·戈登和Erez Chimovits。 代表(I)OrbiMed以色列合夥人有限合夥公司(OIP)持有的1,787,765股普通股,以及(Ii)合計 轉換OIP持有的X系列優先股後可發行的59,800股普通股(受惠9.99% 所有權限制)和在行使OIP持有的某些認股權證時可發行的普通股股份(受惠9.99% 所有權限制),可在2025年3月20日行使,或將在此後60天內行使。

OrbiMed Biofund是OIP的普通合夥人,OrbiMed以色列是OrbiMed Biofund的普通合夥人。OrbiMed以色列行使投資 通過一個由戈登和奇莫維茨組成的投資委員會,擁有對OrbiMed Biofund所持證券的控制權。作爲一名 結果,OrbiMed以色列公司、OrbiMed Biofund公司、戈登先生和奇莫維茨先生分享了投票權和處置權 本文中報告的證券由OIP持有。OrbiMed以色列公司、OrbiMed Biofund公司、戈登先生和奇莫維茨先生可能被直接視爲 或間接地成爲OIP所持證券的實益所有人,包括因爲它們相互隸屬。地址 OrbiMed Biofund、OrbiMed以色列和Chimovits先生的成員是89 Medinat Hayehudim St.Building E Herzliya 4614001以色列。地址 戈登的住處是列剋星敦大道601號,地址:紐約54層,郵編:10022。

基於某些信息 提供給本公司。代表Alyeska Master Fund或Alyeska持有的1,590,738股普通股,不包括 在行使某些認股權證時可發行的普通股總數爲725,338股(受實益所有權限制), 因此,認股權證只有在股東批准後才能行使。Alyeska的地址是77 W.Wacker,Suite 700,Chicago, IL 60601。

基於向本公司提供的某些信息。代表由AIGH Investment Partners,LP或AIGH持有的1,590,738股普通股,不包括在行使某些認股權證時可發行的普通股總數725,338股(受實益所有權限制),因爲該等認股權證只有在股東批准後才可行使。AIGH的地址是馬里蘭州巴爾的摩伯克利大道6006號,郵編21209。

代表(一)53,056股普通股,(二)1,875股普通股 在行使某些認股權證時可發行的普通股;及(Iii)購買129,123股普通股的某些認購權 自2025年3月20日起歸屬,或將在此後60天內歸屬。

代表(I)375股普通股,(Ii)281股可在行使若干認股權證時發行的普通股,及(Iii)於2025年3月20日,即歸屬日期或將於其後60天內歸屬的購買16,431股普通股的若干購股權。

代表(I)31,749股普通股和(Ii)某些期權 購買截至2025年3月20日已歸屬或將在此後60天內歸屬的35,294股普通股。

| 代表(I)375股普通股,(Ii)281股可在行使某些認股權證時發行的普通股,以及(Iii)購買13,415股普通股的某些期權,這些股票已於2025年3月20日歸屬,或將於此後60天內歸屬。 | 代表(I)500股普通股,(Ii)375股可在行使某些認股權證時發行的普通股,以及(Iii)購買於2025年3月20日已歸屬或將於其後60天內歸屬的6,707股普通股的某些期權。 |

| 代表購買截至2025年3月20日已歸屬或將在此後60天內歸屬的1,537股普通股的某些期權。 | 項目 13.某些關係和相關交易,以及董事的獨立性 |

| 董事 獨立 | 這個 紐約證券交易所美國證券交易所要求董事會的大多數成員都是「獨立董事」,這通常被定義爲 除本公司或其附屬公司的高級人員或僱員或任何其他與以下情況有關係的個人外, 由董事會決定,將干擾其客觀判斷的行使,並將達到以下要求的標準 獨立性,由紐約證券交易所美國證券交易所和美國證券交易委員會的適用規則和規定建立。 |

Dr。 拉塞爾·格雷格、艾倫·摩****、愛德華·威廉姆斯先生、喬納森·萊夫先生、傑西·古德曼博士、格雷戈裏·梅里爾先生和布魯姆女士是我們的 獨立董事。

在… 董事會至少每年評估我們與每個董事之間的所有關係,考慮以下相關事實和情況 確定是否存在可能存在潛在利益衝突或其他干擾的實質性關係的目的 這樣的董事有能力履行作爲一個獨立董事的責任。基於這一評估,我們的董事會 將每年確定每個董事是否在紐約證券交易所美國證券交易所和美國證券交易委員會獨立性的意義下是獨立的 標準。

42

政策 和與關聯方進行交易的程序

我們的 關聯人交易政策要求我們儘可能避免所有可能導致實際 或潛在的利益衝突,除非根據董事會(或審計委員會)批准的指導方針。只要公司 符合《交易法》第120億.2條所界定的「較小申報公司」的資格,即關聯人交易 在我們的關聯人交易政策中被定義爲交易、安排或關係(或任何一系列類似的交易、 安排或關係),而我們及任何有關人士(如保單所界定)是、曾經或將會參與 所涉及的金額超過120亿元或公司於#年年底總資產平均值的百分之一,兩者以較少者爲準 過去兩個已完成的財政年度,而任何關連人士在該兩個財政年度內有或將有直接或間接的重大利益。如果 公司不再是較小的報告公司,關聯人交易將被定義爲交易、安排或關係 (或任何一系列類似的交易、安排或關係),而該等交易、安排或關係是、曾經或將會涉及的 所涉金額超過120,000美元的參與者,以及任何相關人士曾經或將會有直接或間接 物質利益。作爲員工、顧問或董事向我們提供的服務涉及補償的交易不被考慮。 本政策下的關聯人交易。

在……裏面 公司擬訂立或重大修改關聯人交易時,公司管理層應 將該關聯人交易提交審計委員會審查、審議和批准或批准。演示文稿 在合理可用的範圍內,必須包括以下說明:(A)所有當事人,(B)直接或間接的利益, 對交易中的任何關聯人(S)提供足夠詳細的信息,使審計委員會能夠充分評估該等利益; (C)交易的目的;。(D)擬議的關係人交易的所有重要事實,包括擬議的 此類交易的總價值,或在負債的情況下,將涉及的本金數額;(E)利益 (F)如果適用,是否有其他來源的可比產品 或服務,(G)評估擬議的關聯人交易的條款是否與現有條款相當 與本應保持一定距離談判的無關第三方之間的往來,視情況而定;以及(H)管理層的 在知道存在潛在或實際衝突的情況下,就擬議的關聯人交易提出建議 這件事的出現是有結果的。如果審計委員會被要求考慮是否批准正在進行的相關人員 交易,除上述信息外,演示文稿還必須包括(I)對所執行工作範圍的描述 (2)對終止的潛在風險和費用的評估 以及(Iii)在適當的情況下,修改交易的可能性。

這個 委員會在批准或否決建議的關聯人交易時,會考慮所有相關的事實和情況。 委員會認爲相關並可供委員會使用的資料,包括但不限於:(A)公司面臨的風險、成本和收益;(B) 對董事獨立性的影響如果關係人是董事、董事的直系親屬或 與董事有關聯的實體,(C)交易的條款和時間,(D)可獲得的其他來源 可比服務或產品;(E)提供給無關第三方或從無關第三方獲得的條款;以及(F)相關人員如何 根據關聯人交易政策的要求,實現了交易並將其傳達給審計委員會。《審計》 委員會將只批准那些根據已知情況屬於或不矛盾的關聯人交易 在符合本公司及其股東最佳利益的情況下,由審計委員會真誠行使其酌情決定權確定。

其他

一個 薪酬、解僱、控制權變更和其他安排,這些安排在項目11--高管薪酬和 第12項-某些實益所有人的擔保所有權以及管理層和相關股東事項,我們唯一的相關人員 自2024年1月1日以來的交易包括:(I)我們於2024年3月6日與某些投資者簽訂的證券購買協議, 包括CFF、Orbimed和Telmina Limited,或Telmina,各自持有我們已發行普通股的5%以上,根據 我們出售了總計216,417股可轉換優先股和私募認股權證,以購買總計 108,208,500股普通股,合計收購價爲X系列優先股和附屬私人股每股231.10美元 配售許可。此次發行的總收益約爲5,000美元萬。私募認股權證具有 行權價爲0.2311美元,2026年7月6日到期。私募認股權證的行使價受慣例所限 股票分紅、股票拆分、重新分類等調整。在這些收益中,總計21,635股可轉換 優先股和10,817,500份私募認股權證被出售給CFF,總收益爲500美元萬,總計4,327股 的可轉換優先股和2,163,500份私募認股權證出售給Orbimed,總收益爲100美元萬和總計 向Telmina出售了2,596股可轉換優先股和1,298,000份私募認股權證,總收益爲0.6美元 百萬美元和(Ii)2025年2月SPA和誘因函協議以及與2025年2月融資有關的其他協議 (如項目5「管理層對財務狀況和業務成果的討論和分析」中所述 -流動性和資本資源“)與某些投資者,包括Deerfield、CFF、Nantahala Capital Management,LLC或 南塔哈拉和AIGH Investment Partners,LP或AIGH,每一家都持有我們已發行普通股的5%以上。收益的一部分 從2025年2月的融資中,(A)CFF的總收益爲210萬,總計2,256,609股 行使新認股權證可發行普通股375,399股行使新認股權證可發行普通股修訂及重訂 認股權證,以及1,174,859股可在行使預融資認股權證時發行的普通股;(B)Deerfield的萬爲300美元 合共3,223,728,000股可於行使新認股權證時發行的普通股;(C)南塔哈拉爲120萬, 合共763,509股普通股、1,289,491股行使新認股權證可發行普通股、101,791股普通股 在行使修訂和重新認股權證時可發行的普通股,以及在行使預融資認股權證時可發行的普通股213,609股; 和(D)AIGH約爲70萬,總計432,700股普通股和725,338股普通股 可在行使新認股權證時發行。

項目 14.首席會計師費用及服務

這個 以下是我們向Kesselman&Kesselman會計師事務所(ISR)收取的費用的摘要和說明。對於 截至2024年12月31日和2023年12月31日的財年。

財政年度結束

12月31日,

43

財政年度結束

十二月三十一日,

審計費用

審計相關費用

稅費

所有其他費用

44

總費用

審計費

包括 爲中期綜合財務報表及年度財務報表季度審核提供的專業服務費用 審計我們年度報告Form 10-K中包含的合併財務報表。

審計相關費用

45

包括與本會計年度年度綜合財務報表審計業績合理相關的服務費用,但審計費用除外,例如與收購、銷售協議有關的服務,以及通過在2024年3月和2023年2月通過出售股東的方式再出售某些普通股而提交的登記聲明。

稅費

包括 稅務合規和稅務諮詢的費用。

| 前置審批 政策和程序 | 這個 審計委員會批准我們的獨立註冊會計師事務所提供的所有審計和預先批准的所有非審計服務 在我們聘請它提供非審計服務之前。這些服務可能包括審計相關服務、稅務服務和其他服務。 | |

| 這個 在下列情況下,上述預先審批要求不適用於非審計服務: | ● |

46

| 並不是所有這樣的服務都是如此, 合共佔我們向獨立註冊會計師事務所支付費用總額的5%以上。 提供服務的財政年度; | ● | |

| 這些服務並不是 在相關聘用時被確認爲非審計服務;以及 | ● | |

| 這樣的服務是及時的 在完成年度審計之前提請審計委員會(或其代表)注意並得到其批准。 | 前置審批 政策和程序 | |

| 這個 審計委員會批准我們的獨立註冊會計師事務所提供的所有審計和預先批准的所有非審計服務 在我們聘請它提供非審計服務之前。這些服務可能包括審計相關服務、稅務服務和其他服務。 | 這個 在下列情況下,上述預先審批要求不適用於非審計服務: | |

| ● | 並不是所有這樣的服務都是如此, 合共佔我們向獨立註冊會計師事務所支付費用總額的5%以上。 提供服務的財政年度; |

●

47

這些服務並不是 在相關聘用時被確認爲非審計服務;以及

●

這樣的服務是及時的 在完成年度審計之前提請審計委員會(或其代表)注意並得到其批准。

零件 IV

註冊權協議表格(參照公司於2023年2月22日提交的當前8-K表格報告的附件10.2併入)。

自適應噬菌體治療公司和美利堅合衆國之間的獨家許可證,由海軍部長代表,日期爲2017年3月16日(根據公司於2024年4月4日提交的Form 10-K年度報告附件10.22合併)

第一修正案,日期爲2019年1月10日,由海軍部長代表的自適應噬菌體治療公司和美利堅合衆國之間的獨家許可(通過引用公司於2024年4月4日提交的公司10-K表格年度報告的附件10.23合併)

48

自適應噬菌體治療公司與Walter蘆葦陸軍研究所簽訂和簽訂的非獨家許可協議,日期爲2021年8月24日(根據公司於2024年4月4日提交的Form 10-K年報附件10.24合併)

許可證修改1,日期爲2022年8月31日,由自適應噬菌體治療公司和Walter蘆葦陸軍研究所簽訂或之間的非獨家許可協議(根據公司於2024年4月4日提交的Form 10-K年報附件10.25合併)

BiomX Inc.與附件A所列每位購買者簽訂的、日期爲2024年3月6日的證券購買協議(根據公司於2024年3月6日提交的當前8-K報表附件10.1合併而成)

| 公司與某些購買者之間的登記權協議格式,日期爲2024年3月6日(參照公司於2024年3月6日提交的公司當前8-K表格報告的附件10.2成立爲法團) | 租賃協議,日期爲2019年8月9日,由ARE-708 Quince Orchard,LLC和Adapted Phage Treateutics,Inc.簽訂(通過引用公司於2024年4月4日提交的Form 10-K年報附件10.28併入) |

| 截至2020年10月28日,對ARE-708 Quince Orchard,LLC和Adapter Phage Treateutics,Inc.之間的租賃協議的第1號修正案(通過引用公司於2024年4月4日提交的公司年度報告Form 10-K的附件10.29併入) | 第2號修正案,日期爲2021年7月8日,對ARE-708 Quince Orchard,LLC和Adapter Phage Treateutics,Inc.之間的租賃協議(通過引用公司於2024年4月4日提交的公司年度報告Form 10-K的附件10.30而併入) |

| 日期爲2021年7月15日的第3號修正案,對ARE-708 Quince Orchard,LLC和Adapter Phage Treateutics,Inc.之間的租賃協議(通過引用公司於2024年4月4日提交的公司年度報告Form 10-K的附件10.31併入) | 日期爲2022年9月27日的第4號修正案,對ARE-708 Quince Orchard,LLC和Adapter Phage Treateutics,Inc.之間的租賃協議(通過引用公司於2024年4月4日提交的公司年度報告Form 10-K的附件10.32併入) |

| 第5號修正案,日期爲2023年2月2日,對ARE-708 Quince Orchard,LLC和Adapted Phage Treateutics,Inc.之間的租賃協議(通過引用公司於2024年4月4日提交的公司年度報告Form 10-K的附件10.33併入) | 第6號修正案,日期爲2024年3月5日,對ARE-708 Quince Orchard,LLC和Adaptive Phage Treateutics,Inc.之間的租賃協議(通過參考公司於2024年4月4日提交的公司年度報告Form 10-K的附件10.34而合併) |

| BiomX Inc.與買方於2025年2月25日簽署的證券購買協議表格(根據本公司於2025年2月27日提交的當前8-K表格報告附件10.1註冊成立) | BiomX Inc.和買方於2025年2月25日簽署的註冊權協議表格(根據公司於2025年2月27日提交的當前8-K表格報告附件10.2合併) |

BiomX Inc.與持有人於2025年2月25日簽署的認股權證行使和重新加載協議

49

(參照本公司於2025年2月27日提交的現行8-K表格報告的附件10.3)

BiomX Inc.與Laidlaw and Company(UK)Ltd.於2025年2月25日簽訂的配售代理協議(通過引用本公司於2025年2月27日提交的當前8-K表格報告的附件10.4合併而成)

MTEC基礎協議號2019-532,日期爲2019年8月22日,由先進技術國際公司(MTEC財團經理)與自適應噬菌體治療公司簽訂,日期爲2019年8月22日,並對其進行如下修改:(I)日期爲2019年9月30日的修改編號1;(Ii)日期爲2020年7月22日的修改編號2;(Iii)日期爲2021年9月27日的修改編號3;(Iv)日期爲2022年9月8日的修改編號4;(V)日期爲2022年12月16日的修改編號5;(Vi)修改編號6,日期爲2023年12月19日;(Vii)修改編號7,日期爲2024年1月16日;及(Viii)修改編號8,日期爲2024年9月11日

BiomX Inc.內幕交易政策

公司子公司(參考公司於2024年4月4日提交的10-K表格年度報告附件21.1註冊成立)

Kesselman & Kesselman,註冊會計師(Isr.)的同意,普華永道國際有限公司的成員公司

根據規則13 a-14和規則15 d-14(a)認證首席執行官。

根據規則13 a-14和規則15 d-14(a)認證首席財務官。

根據USC 18認證首席執行官和首席財務官第1350條。

50

追回政策(參考公司於2024年4月4日提交的10-K表格年度報告的附件97.1合併)

101.INS

內聯MBE實例文檔

101.SCH

內聯MBE分類擴展架構文檔101.CAL

內聯MBE分類擴展計算Linkbase文檔

101.DEF

內聯XBRL分類擴展定義Linkbase文檔

51

101.LAB

內聯MBE分類擴展標籤Linkbase文檔

101.PREInline MBE分類擴展演示Linkbase文檔”

封面交互式數據文件(格式爲Inline BEP,包含在附件101中)

/s/喬納森 所羅門

首席執行官

2025年3月25日

喬納森·所羅門

52

(首席執行官)兼董事

/s/瑪麗娜 沃爾夫森

首席財務官

2025年3月25日

瑪麗娜·沃爾夫森

53

(首席財務官兼校長

會計官)

/s/拉塞爾 Greig

董事局主席

| 2025年3月25日 | 拉塞爾·格里格博士 |

| /s/ Susan Blum | 董事 |

| 2025年3月25日 | 蘇珊·布魯姆 |

| /s/ Jesse 古德曼 | 董事 |

| 2025年3月25日 | 傑西·古德曼博士 |

| /s/喬納森 Leff | 董事 |

| 2025年3月25日 | 喬納森·萊夫 |

54

/s/格雷戈裏 Merril

董事

2025年3月25日

格雷戈裏·梅里爾

| /s/艾倫·摩西 | 董事 |

| 2025年3月25日 | 艾倫·摩**** |

| /s/愛德華 威廉姆斯 | 董事 |

| 2025年3月25日 | 愛德華·威廉姆斯 |

| BioMX Inc. | 合併財務報表 |

| 2024年12月31日 | 目錄 |

頁面

獨立註冊會計師事務所報告(PCAOB名稱:Kesselman&Kesselman C.P.A.,PCAOB ID:

F-2戰機

55

合併財務報表:

綜合資產負債表

F-4 -F-5

綜合經營報表

合併股東權益變動表

綜合現金流量表

F-8-F-9

56

合併財務報表附註

F-10-F-40

獨立註冊公共會計報告 堅定

致BiomX Inc.董事會和股東。

對財務報表的幾點看法

我們已經審計了隨附的合併文件 BiomX Inc.及其子公司(「本公司」)於2024年、2024年及2023年12月31日的資產負債表,以及相關的綜合 截至2024年12月31日止年度的經營報表、股東權益變動及現金流量,包括有關 附註(統稱「合併財務報表」)。我們認爲,合併財務報表 公平地列報本公司截至2024年、2024年及2023年12月31日的財務狀況及其業績 截至2024年12月31日止年度的業務及其現金流量符合公認會計原則 美利堅合衆國。

人們對該公司繼續經營的能力產生了極大的懷疑 作爲一家持續經營的企業

57

隨附的合併財務報表 已經準備好假設公司將作爲一家持續經營的公司繼續存在。如合併財務報表附註1C所述, 本公司經營出現重大虧損和負現金流,累計出現虧損,並已聲明 這些事件或情況使人對公司作爲持續經營企業的持續經營能力產生了極大的懷疑。管理層的計劃 關於這些事項,也見附註1C所述。合併財務報表不包括任何可能 這是這種不確定性的結果。

意見基礎

這些合併財務報表是 公司管理層的責任。我們的責任是就公司的綜合財務發表意見 基於我們審計的聲明。我們是一家在上市公司會計監督委員會(United)註冊的公共會計師事務所 各州)(PCAOB),並根據美國聯邦證券法和 美國證券交易委員會和PCAOB的適用規則和條例。

我們對這些合併的 根據PCAOB的標準編制財務報表。這些標準要求我們計劃和執行審核以獲得 關於合併財務報表是否沒有重大錯報的合理保證,無論是由於錯誤還是舞弊。 本公司並無被要求對其財務報告的內部控制進行審計,我們也沒有受聘進行審計。作爲一部分 在我們的審計中,我們被要求了解財務報告的內部控制,但不是爲了表達 關於公司財務報告內部控制有效性的意見。因此,我們不表達這樣的意見。

我們的審計包括執行程序以評估 合併財務報表出現重大錯報的風險,無論是由於錯誤還是舞弊,以及執行程序 對這些風險做出反應的公司。這些程序包括在測試的基礎上審查關於 合併財務報表。我們的審計還包括評估所使用的會計原則和所作的重大估計 管理,以及評價合併財務報表的整體列報。我們相信,我們的審計提供了 我們的觀點有一個合理的基礎。

關鍵審計事項

下面所述的關鍵審計事項是由以下原因引起的事項 對已通知或要求通知審計委員會的合併財務報表的當期審計 及(I)涉及對綜合財務報表有重大影響的賬目或披露,及(Ii)涉及我們的 具有挑戰性的、主觀的或複雜的判斷。關鍵審計事項的溝通不會以任何方式改變我們對 綜合財務報表,作爲一個整體,我們沒有,通過傳達下面的關鍵審計事項,提供一個單獨的 對關鍵審計事項或與之相關的賬目或披露的意見。

無形資產初始估值和減值評估

58

如合併財務報表附註1D和2R所述, 作爲業務合併的一部分,2024年3月15日,公司確認了一項無形資產,包括正在進行的研究和 開發(「知識產權研發」)價值1,530美元萬。截至2024年12月31日,知識產權研發餘額爲1,200美元萬。管理 至少每年、在財政年度第三季度的最後一天或任何有跡象表明的時候進行減值測試 該資產可能已減值。潛在減值通過將知識產權研發的公允價值與其賬面價值進行比較來識別。 截至2024年12月31日,管理層注意到,由於市值下降,存在潛在減值指標。 因此,管理層進行了量化評估,並記錄了320万美元的無形資產減值費用。公允價值 由管理層使用貼現現金流模型進行估計。管理層的現金流預測包括重要的判斷和假設 與預計未來現金流和貼現率的金額和時間有關。

我們決定執行的主要考慮因素是 與無形資產的初始估值和減值評估有關的程序是一項關鍵的審計事項:(一)重大 管理層在制定無形資產公允價值估計時的判斷;(2)核數師判斷的高度主觀性 以及執行程序和評估管理層與預測未來的數量和時間相關的重大假設的努力 現金流量和貼現率;(3)審計工作涉及使用具有專門技能和知識的專業人員。

處理這一問題涉及執行程序和評估 與形成我們對合並財務報表的整體意見有關的審計證據。這些程序包括 其他(一)測試管理層制定公允價值估計的程序;(二)評估貼現的適當性 管理層使用的現金流量模型;(3)測試貼現現金流量中使用的基礎數據的完整性和準確性 (4)評價管理層使用的與預測的數額和時間有關的重大假設的合理性 未來現金流和貼現率。評估管理層關於預計未來現金數額和時間的假設 流量和貼現率涉及評估管理層使用的假設是否合理,考慮到與 外部市場和行業數據。具有專業技能和知識的專業人員被用來協助評估(I)適當性 貼現現金流模型的合理性和(Ii)貼現率假設的合理性。

凱塞爾曼和凱塞爾曼

註冊會計師(Isr.)

普華永道國際有限公司的成員

特拉維夫,以色列

三月 2025年25月

| 我們自2021年以來一直擔任公司的核數師。 | BioMX Inc. |

| 合併資產負債表 | (美元以千爲單位,不包括每股和每股數據) |

| 截至12月31日, | 資產 |

59

| 流動資產 | 現金及現金等價物 |

| 受限現金 | 其他流動資產 |

| 流動資產總額 | 非流動資產 |

| 非流動限制現金 | 經營租賃使用權資產 |

| 財產和設備,淨值 | 在製品研發(「IPR & D」)資產 |

| 非流動資產總額 | 附註是完整的一部分。 合併財務報表的財務報表。 |

| BioMX Inc. | 合併資產負債表 |

| (美元以千爲單位,不包括每股和每股數據) | 截至12月31日, |

| 負債和股東權益 | 流動負債 |

| 貿易帳戶應付款 | 租賃負債的流動部分 |

| 其他應付賬款 | 流動長期負債部分 |

流動負債總額

60

非流動負債

合同責任

長期債務,扣除流動部分

經營租賃負債,扣除流動部分

其他負債

私募認購令

非流動負債總額

承諾和或有事項(注8)

61

股東權益

優先股,美元

面值;授權-

截至2024年12月31日和2023年12月31日的股票。已發佈且未完成-

截至2024年12月31日。

不是

截至2023年12月31日已發行和發行的股份。

經營虧損

其他收入

利息支出

62

財務費用(收入),淨額

私募股權證公允價值變動收入

稅前虧損

稅費用

淨虧損

每股普通股基本損失

63

每股普通股稀釋虧損

用於計算每股普通股基本損失的加權平均股數(*)

用於計算每股普通股稀釋虧損的加權平均股數(*)

所有股份金額均已追溯調整,以反映附註12 A中討論的1比10反向股份分割。

附註是完整的一部分。 合併財務報表的財務報表。

BioMX Inc.

股東權益變動合併報表

(美元以千爲單位,不包括每股和每股數據)

64

可贖回

可換股

優先股

普通股

額外

支付

積累

總計

65

股東’

股份

量

股份

量

資本

赤字

股權

截至2023年1月1日餘額

私人投資公開股權下發行普通股和認購證,扣除美元

| 發行成本(**) | 重新發行庫藏股(*) |

| 股票補償費用 | 根據公開市場銷售協議發行普通股(**) |

| 淨虧損 | 截至2023年12月31日餘額 |

| APT收購後發行普通股、合併證和可贖回可轉換優先股,扣除發行成本(**) | 預融資憑證行使爲普通股股份 |

| 根據公開市場發行協議發行普通股,扣除美元 | 發行成本(**) |

66

2024年3月起發行可贖回可轉換優先股PIPE,扣除發行成本(**)

可贖回可轉換優先股轉換爲普通股股份

受限制股票單位(「RSU」)歸屬後發行普通股

| 股票補償費用 | 淨虧損 | |

| 截至2024年12月31日餘額 | 不到1美元。 | |

| 見註釋12 A。 | 參見注釋7A。 | |

| 所有股份金額均已追溯調整,以反映附註12 A中討論的1比10反向股份分割。 | 附註是完整的一部分。 合併財務報表的財務報表。 | |

| BioMX Inc. | 綜合現金流量表 | |

| (USD單位:千,份額和每股除外 數據) | 截至十二月三十一日止的年度: | |

| 現金流-運營活動 | 淨虧損 | |

| 將淨虧損與經營活動中使用的現金流量進行對賬所需的調整 | 折舊 | |

| 股票補償 | 債務發行成本攤銷 | |

| 財務收入淨額 | 或有對價的重新評估 | |

| 定向增發權證公允價值變動收益 | 私募權證發行成本 | |

| 合同負債的變化 | 出售和處置固定資產損失淨額 | |

| 商譽減值 | IPR & D損害 |

長期資產減損

經營資產和負債變化:

67

其他流動資產

應付貿易賬款

其他應付賬款

經營租賃淨變化

經營活動所用現金淨額

現金流-投資活動

從APT收購中獲得的現金和限制性現金

短期存款收益

68

添置物業及設備

出售財產和設備的收益

| 投資活動提供的淨現金 | 現金流-融資活動 |

| 2023年2月PIPE下發行普通股和認購證 | 2023年2月起的發行成本PIPE |

| 預先資助的授權令練習 | 根據公開市場銷售協議發行普通股,扣除發行成本 |

| 償還長期債務 | 2024年3月PIPE下私募股權認購證的發行 |

| 2024年3月PIPE下發行可贖回可轉換優先股 | 2024年3月PIPE發行成本 |

| 融資活動提供的現金淨額 | 現金及現金等值物以及受限制現金增加(減少) |

| 匯率變化對現金和現金等值物以及受限制現金的影響 | 年初現金及現金等值物以及限制性現金 |

| 附註是完整的一部分。 合併財務報表的財務報表。 | BioMX Inc. |

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

注1-

一般信息

一般信息:

69

BiomX Inc.(單獨並與其子公司一起, BiomX有限公司(「BiomX以色列」),RondinX有限公司和自適應噬菌體治療有限責任公司(「APT」),「公司」 或「BiomX」)於2017年11月1日根據特拉華州法律註冊爲空白支票公司,用於 進行合併、證券交易所、資產收購、股票購買、資本重組、重組或類似業務的目的 與一個或多個企業或實體合併。

2019年10月29日,公司與BiomX以色列公司合併, 作爲BiomX Inc.的全資子公司,該公司收購了BiomX以色列的所有流通股。作爲交換, BiomX以色列公司的股東收到

公司普通股,代表

佔已發行股份總數的百分比

並在收購後未償還(「資本重組交易」)。BiomX以色列公司被認爲是「會計收購方」

由於本公司擁有最大的所有權權益。該公司的普通股在紐約證券交易所美國證券交易所掛牌交易。

符號PHGE。

。有關詳細信息,請參閱附註12A 關於2024年3月的管道。

2024年8月8日,董事會

已批准爲

現金及現金等價物

受限現金

其他流動資產

房及設備

經營租賃使用權資產

知識產權研發資產與商譽

總資產

應付賬款

70

其他應付款

經營租賃負債

總負債

總對價

所有可識別資產的公允價值估計 假設的資產和負債是基於市場參與者在爲資產定價時使用的假設,基於最有利的 資產的市場(即其最高和最佳用途)。

公司確認無形資產 與收購有關的知識產權研發,價值爲#美元

多期超額收益法估值方法的應用 以及商譽價值爲$

。商譽主要歸因於預期APT業務與 公司的運營和APT的全體員工。知識產權研發被認爲是無限期的生命,直到完成 或放棄相關的研究和開發努力。在項目成功完成後,知識產權研發資產將重新分類 用於開發技術,並在其估計使用壽命內攤銷。

71

BioMX Inc.

行權價(美元)

預期波動率(%)

預期期限(年)

無風險利率(%)

實際APT淨虧損包括在 公司截至2024年12月31日的年度綜合經營報表如下:

12月31日,

可歸因於APT的淨虧損*包括與商譽、知識產權研發和長期資產有關的減值損失#美元.

及$

72

,分別爲。

未經審計的備考財務信息 下面總結了BiomX Inc.(包括其全資子公司BiomX以色列和RondinX)的綜合運營結果 有限公司)而且恰如其分。未經審計的備考財務信息包括反映某些業務合併影響的調整,包括: 雙方產生的與收購相關的成本以及BiomX Inc.發生的某些本不會發生的成本的沖銷 如果收購發生在2023年1月1日。以下所列未經審計的備考財務信息僅供參考 僅限於目的,並不一定表明如果進行了收購就會取得的經營成果 放在2023財年開始時。

BioMX Inc.

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

注1-

一般(續)

合併協議(續)

以下未經審計的表格提供了 公司的某些形式財務信息,就好像收購發生在2023年1月1日:

| 12月31日, | 12月31日, | |

|

淨虧損 | 上述備考金額乃根據本公司及APT的歷史數字計算。 |

| 注2- | 重大會計政策 | |

| 編制過程中採用的重要會計政策 除採用新的會計準則外,以下是一致的財務報表: | 列報依據和合並原則 |

73

| 隨附的合併財務報表有 按照美國公認的會計原則(「公認會計原則」)編制,包括 公司及其全資子公司BiomX以色列、APT和RondinX Ltd.的帳戶。所有公司間帳戶和交易 已經在整合中被淘汰了。 | 在編制財務報表時使用估計數 | |

| 編制符合以下條件的財務報表 《公認會計原則》要求管理層作出估計和假設,以影響報告的資產和負債額以及披露 財務報表中的或有資產和負債以及報告年度的費用數額。最重要的 公司財務報表中的估計涉及研究和開發費用的應計項目、基於股票的估值 補償獎勵、與收購相關的購買價格分配、私募認股權證公允價值重估和估計 用於IPR&D減值評估以計算公司資產的公允價值。這些估計和假設 都是基於目前的事實、未來的預期以及其他各種因素認爲是合理的情況下得出的結果 它構成了判斷資產和負債賬面價值以及記錄下列費用的基礎 從其他來源看不是很明顯。實際結果可能與這些估計大相徑庭。 | 以色列與哈馬斯的戰爭的全面程度 而真主黨可能會直接或間接影響公司的業務,經營結果和財務狀況將取決於 關於不確定的未來發展以及對當地、區域、國家和國際市場的經濟影響。 | |

| 本位幣和外幣折算 | 公司的本位幣爲美元 (「美元」)因爲美元是公司經營和預期所處的主要經濟環境的貨幣 在可預見的未來繼續運營。最初以美元計價的交易和餘額按其原始金額列示 金額。非美元貨幣的餘額使用非貨幣和貨幣的歷史和當前匯率換算成美元。 餘額分別爲。對於非美元交易和綜合業務報表中的其他項目(如下所示),如下 匯率用於:(1)交易--交易日期的匯率或平均匯率;(2)其他 項目(源自折舊和攤銷等非貨幣資產負債表項目)--歷史匯率。貨幣 交易損益酌情在財務費用(收益)淨額中列報。 |

現金及現金等價物和限制性現金

公司認爲現金等價物都是短期的, 流動性高的投資,包括不受提款或使用限制的貨幣市場基金,以及短期銀行存款 自購買之日起三個月或以下的原始到期日,不受取款或使用限制,並隨時可以 可兌換成已知數量的現金。受限現金包括合同上受限於未償還的信用額度的資金 由於租賃協議,短期外匯合同和銀行擔保。該公司已單獨提交了受限現金 從合併資產負債表中的現金和現金等價物中扣除。該公司包括其現金和現金的受限銀行存款 在調整合並現金流量表上顯示的期初和期末總額時的等價物。

BioMX Inc.

| 合併財務報表附註 (美元以千爲單位,不包括每股和每股數據) |

||||||||

| 2024 | 2023 | |||||||

| 注2- | ||||||||

| 重大會計政策(續) | 10,495 | 8,853 | ||||||

| 信用風險集中 | 2,239 | - | ||||||

| 可能使我們受制於信貸的金融工具 風險主要由現金和現金等價物構成。這些金額有時可能會超過聯邦保險的限額。我們還沒有經歷過 任何此類帳戶的信用損失,並不認爲我們在這些資金上面臨任何重大的信用風險。該公司的大部分 現金和現金等價物以及銀行存款投資於美國和以色列的主要銀行。管理層認爲,信用風險 關於持有本公司現金和現金等價物以及銀行存款的金融機構,現金及現金等價物和銀行存款較低。參考 注2J。 | 8,006 | 6,004 | ||||||

| 物業及設備 | 1,488 | 782 | ||||||

| 財產和設備按成本減去累計列報 折舊。折舊以直線法爲基礎,計算相關資產或條款的估計使用年限。 有關租約的詳情如下: | 3,900 | 905 | ||||||

| 估計可使用年期 | 1,123 | 2,491 | ||||||

| 實驗室設備 | (2,588 | ) | (2,337 | ) | ||||

| 年份 | 24,663 | 16,698 | ||||||

計算機和軟件

年份

設備和傢俱

74

年

租賃權改進

租期或使用年限較短

長期資產

根據ASC 360-10《減值和處置 長期資產減值“,當事件或環境變化表明時,管理層審查長期資產的減值 根據估計的未來未貼現現金流,一項資產的賬面價值可能無法收回。如有說明,減值 將根據資產的賬面價值與其公允價值之間的差額確認損失。有關以下內容的信息,請參閱附註11 在截至2024年12月31日的年度內確認的減值費用。

所得稅

公司使用資產和資產來覈算所得稅 責任法。遞延稅項資產和負債是根據財務報表和稅項之間的差額入賬的 資產和負債的基礎以及這些差額預期發生逆轉時的有效稅率。遞延稅項資產減少 如果根據現有證據的權重,更有可能部分或全部遞延稅項資產 將不會實現。截至2024年12月31日和2023年12月31日,公司擁有針對遞延稅項資產的全額估值準備金。

本公司遵守ASC 740-10-25的規定, 「所得稅」(ASC 740)。ASC 740規定了一個更有可能的財務報表確認門檻 不確定的稅收狀況。ASC 740通過規定最低確認門檻和衡量標準來澄清所得稅的會計處理 用於確認和計量納稅申報單中已採取或預期採取的納稅頭寸的財務報表屬性。在……上面 本公司每年都會評估所得稅應計項目是否符合ASC 740關於不確定性的指引 稅收頭寸。截至2024年12月31日及2023年12月31日止年度,本公司並無就不確定稅務狀況記錄任何負債。 本公司將未確認的稅項優惠作爲遞延稅項資產的減值提出,而淨營業虧損、類似的稅項虧損或 根據適用司法管轄區的稅法,可用於抵銷任何額外所得稅的稅收抵免結轉 這將是稅務頭寸結清的結果。

衍生活動

公司使用外匯合同(期權和 遠期合約)對沖現金流的匯率敞口。這些外匯合約不被指定爲對沖工具。 出於會計目的。就該等外匯合約而言,本公司確認可抵銷重估的收益或虧損 在財務費用(收入)項下也記錄的現金流量中,淨額計入合併業務表。公司認識到 這些衍生工具按其公允價值在綜合資產負債表中作爲資產或負債。中的衍生品 收益頭寸在綜合資產負債表中的其他流動資產中報告,而衍生工具則記錄虧損頭寸。 作爲合併資產負債表中的其他流動負債。截至2024年12月31日,本公司有未償還的短期外匯 美元兌換新謝克爾的兌換合同,金額約爲#美元。

公允價值資產爲$

。截至12月 2023年3月31日,公司持有美元對新謝克爾兌換的未償還短期外匯合同,金額約爲 $

公允價值資產爲$

BioMX Inc.

75

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

注2-

| 重大會計政策(續) 金融工具的公允價值 | ||||||||

| 2024 | 2023 | |||||||

| 公司按照下列規定對金融工具進行會計處理 在ASC 820中,「公允價值計量和披露」(「ASC 820」)。ASC 820建立公允價值層次結構 這對用於衡量公允價值的估值技術的投入進行了優先排序。層次結構將最高優先級分配給未調整的 相同資產或負債的活躍市場報價(第1級計量),以及對不可觀察到的投入的最低優先級 (3級測量)。ASC 820規定的公允價值層次結構的三個層次如下: | ||||||||

| 級別1-活躍市場的未調整報價 在計量日期可獲得相同的、不受限制的資產或負債。 | 24,663 | 16,698 | ||||||

| 二級-在非活躍市場或非活躍市場報價 類似資產或負債的活躍市場,報價以外的可觀察到的投入,以及不可直接觀察到的投入 但得到了可觀察到的市場數據的證實。 | 11,776 | 8,650 | ||||||

| 第3級-需要投入的價格或估值 既對公允價值計量有重大意義又不可觀察的風險。 | 801 | - | ||||||

| 公允價值等級制沒有變化 在截至2024年和2023年12月31日的年度內。 | 3,237 | - | ||||||

| 下表彙總了我們的財務報告的公允價值 在公允價值層次結構內按公允價值按層級按經常性原則按公允價值覈算的資產和負債: | 4,046 | - | ||||||

| 2024年12月31日 | 44,523 | 25,348 | ||||||

| 1級 | (2,143 | ) | (357 | ) | ||||

| 2級 | 873 | 2,404 | ||||||

| 3級 | 919 | (1,249 | ) | |||||

| 公平值 | (26,458 | ) | - | |||||

| 資產: | 13 | 23 | ||||||

| 現金等價物: | 17,727 | 26,169 | ||||||

貨幣市場基金

| 應收外匯合同 | 負債: |

| 或有對價 | 私募認購令 |

| 2023年12月31日 | 1級 |

2級3級公平值

資產:

現金等價物:

貨幣市場基金

應收外匯合同

負債:

76

或有對價

公允價值的變化 公司的私募股權認購證按第3級計量,按經常性計算如下:

止年度

十二月三十一日,

止年度

十二月三十一日,

期初餘額

私募認購令公平值變動期末餘額

BioMX Inc.

合併財務報表附註

77

(美元以千爲單位,不包括每股和每股數據)

注2-

重大會計政策(續)

78

金融工具公允價值(續)

賬面價值接近的金融工具 公允價值包括現金和現金等價物、限制性現金、其他流動資產、應付貿易賬款和其他流動負債, 由於它們的短期性質。

公司決定了公平 基於概率貼現現金流分析的或有對價負債價值。這一公允價值 計量是基於市場中重大的不可觀察的投入,因此代表着交易會內的第三級計量。 價值層次結構。或有對價的公允價值基於幾個因素,例如:實現未來 與治療原發疾病的候選產品有關的臨床、開發、監管、商業和戰略里程碑 硬化性膽管炎(PSC)。適用的貼現率範圍爲

%至

%。或有對價爲 每季度評估一次,如果情況需要,也可以更頻繁地評估。或有對價的公允價值變動如下 記錄在合併經營報表中。不可觀察到的輸入的重大變化,主要是成功的概率和 預計的現金流可能導致或有對價負債發生重大變化。或有事項的變動 對截至2024年12月31日的年度的考慮主要是由於戰略計劃的成功概率發生變化 與JSR Corporation(「JSR」)終止的有關專利權的協議的里程碑事件 PSC的治療。有關詳細信息,請參閱附註8D。截至2023年12月31日的年度或有對價變動 產生於時間的推移和貼現率的重估。

| 公司確定了公允價值

私募認股權證的負債採用布萊克-斯科爾斯模型,這是公允價值層次中的一種3級衡量標準。 所用的主要假設如下: | ||||||||

| 2024 | 2023 | |||||||

| 12月31日, | ||||||||

| 12月31日, | (36,979 | ) | (21,286 | ) | ||||

| 在會計準則更新下,「租賃」 (「ASC 842」),本公司於開始時決定一項安排是否爲租約。經初步確認,本公司確認 按租賃期限內支付的租賃款項的現值計算的負債,同時確認使用權資產 按相同數額的負債,經任何預付或應計租賃付款調整後,加上因此而產生的初始直接費用 租約的一部分。本公司根據開業之日所得資料,以遞增借款利率厘定 租賃付款的現值。隨後的衡量取決於租賃是被歸類爲融資租賃還是 經營租賃。報告期內,本公司僅有營運租約。租賃條款包括延長租賃期限的選項 在合理確定公司將行使該期權的情況下。經營性租賃的租賃費用是按直線確認的 以租賃期爲基準。 | 715 | 1,951 | ||||||

| 該公司已做出政策選擇,不將資本 租期爲12個月或以下的租約。 | 38,374 | 2,899 | ||||||

| 根據ASC 360-10,管理層審查運行情況 當事件或情況變化表明某項資產的賬面價值可能無法收回時,租賃資產進行減值 基於估計的未來未貼現現金流。如有說明,減值損失應確認爲下列差額 資產的賬面價值及其公允價值。 | 1 | 6 | ||||||

| 對於租賃物業,公司 計劃停止使用該物業,以及有轉租該物業的意向和能力的,該公司測試使用權 資產減值,以確定是否發生了損失。使用權資產的賬面價值根據淨現值進行調整。 轉租協議在剩餘租賃期內預期的未來現金流價值。我們可能會記錄額外的減值損失 當我們最終敲定與轉租人簽署的協議時。 | 2,111 | (16,430 | ) | |||||

79

BioMX Inc.

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

注2-

重大會計政策(續)

業務合併

本公司分配公允價值 在企業合併中轉移到所收購資產的對價、根據其在收購時的公允價值承擔的負債 約會。與收購相關的費用從業務合併中單獨確認,並在發生時計入費用。過剩的 轉讓對價的公允價值高於被收購資產、被收購企業承擔的負債的公允價值 被記錄爲商譽。轉讓對價的公允價值包括股權證券。對價的分配 在某些情況下的轉移可能會根據公允價值在計量期間的最終確定進行修訂, 這可能是從收購日期起最長一年的時間。確認測算期內修訂的累積影響 在確定修訂的報告期內。公司包括它所經營的企業的經營結果 已於其綜合業績中預期自各自收購日期起收購。

無形資產

商譽

80

商譽反映了 在企業合併日轉移的對價超過所收購的可識別淨資產的公允價值。商譽是一種 代表在企業合併中收購的其他非單獨資產所產生的未來經濟利益的資產 已確認並單獨確認。產生商譽的主要項目包括被收購方之間協同效應的價值 公司和公司以及被收購的集合勞動力,兩者都不符合確認爲無形資產的資格。ASC 350, “

無形資產--商譽和其他“

允許實體首先評估定性因素以確定是否存在 量化商譽減值測試是必要的。只有當實體根據定性的 評估認爲,公允價值極有可能少於其賬面價值。否則,將不再進行進一步的減值測試 是必需的。該公司的商譽至少每年在第三季度的最後一天進行減值測試 會計年度以及當事件或情況變化表明報告單位的賬面價值可能無法收回時。 必要時,本公司將商譽減值費用計入各自賬面金額 報告單位超出其公允價值。但是,確認的損失不應超過分配給該報告的商譽總額。 單位。截至2024年12月31日止年度,本公司錄得全額商譽減值。有關詳細信息,請參閱附註11 信息。無形資產

在企業中收購的知識產權研發資產 合併在收購日按公允價值確認,隨後作爲無限期無形資產入賬。 直到完成或放棄相關的研發工作。未確定期限的無形資產至少要進行減值審查 每年,在財政年度第三季度的最後一天,或每當有跡象表明資產可能減值到。 進行知識產權研發減值測試時,知識產權研發資產的公允價值與其賬面價值進行比較。如果賬面價值 當知識產權研發資產的賬面價值超過其公允價值時,本公司計入減值損失 公允價值。公司使用貼現現金流量估值模型估計知識產權研發資產的公允價值,該模型要求使用 重大估計和假設,包括但不限於,估計在進行中完成的時間和預期成本 項目,預計監管批准,估計產品銷售的未來現金流,並制定適當的貼現率。 截至2024年12月31日止年度,本公司計入知識產權研發減值金額爲$

。有關詳細信息,請參閱附註11。

BioMX Inc.

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

注2-

重大會計政策(續)

新會計公告

81

最近採用的會計公告

2023年11月,財務會計準則委員會 (「FASB」)發佈的會計準則更新(「ASU」)2023-07“分部報告:對可報告的改進 分部披露「(」ASU 2023-07“)。本指南主要通過以下方式擴大公共實體的部門披露 要求披露定期提供給首席運營決策者幷包括在 每個已報告的分部損益計量、其他分部項目的金額和構成說明以及中期披露 可報告部門的損益和資產總額,目前每年都需要。 可報告分部需要提供新的披露和ASC 280分部報告要求的所有披露。 指導意見適用於2023年12月15日之後開始的財政年度,以及12月後開始的財政年度內的過渡期 2024年15日,允許提前領養。這些修正必須追溯適用於以前在 實體的財務報表。本公司於2024年12月31日起採用這一新標準。有關披露資料,請參閱附註18 爲ASU 2023-07的通過乾杯。

最近發佈的會計聲明,尚未採用

2023年12月,美國財務會計準則委員會發布了ASU 2023-09《收入 稅收(專題740):改進所得稅披露「(」ASU 2023-09“)。本指南旨在加強 所得稅披露的透明度和決策有用性。ASU 2023-09中的修正案解決了投資者對增加收入的要求 稅務信息主要是通過更改在美國和外國支付的稅率對賬和所得稅的披露 司法管轄區。ASU 2023-09在2024年12月15日之後的財政年度生效,並可選擇 追溯適用該標準。允許及早領養。該公司目前正在評估該指南,以確定其影響 它可能在其合併財務報表上有披露。

2024年11月,美國財務會計準則委員會發布了ASU 2024-03《收入 聲明:報告全面收入-費用分類披露,“這需要更詳細的信息 包括的特定費用類別(庫存採購、員工薪酬、折舊、攤銷和損耗) 損益表表面的某些費用標題,以及關於銷售費用的披露。這個ASU是有效的 2026年12月15日之後開始的財政年度和2027年12月15日之後開始的財政年度內的過渡期。早些時候 領養是允許的。這些修正可適用於(1)預期適用於以下報告期發佈的財務報表 本ASU的生效日期或(2)追溯至財務報表中列報的所有先前期間。本公司目前 評估這一指引,以確定它可能對其合併財務報表披露產生的影響。

BioMX Inc.

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

注3

其他流動資產

| 截至12月31日, | 政府機構 |

| 預付保險 | 其他預付費用 |

| 應收贈款 | 其他 |

82

| 附註4 | 財產和財產,淨 |

| 按主要類別分列的資產構成, 如下: | 截至12月31日, |

| 計算機和軟件 | 實驗室設備 | |

| 設備和傢俱 | 租賃權改進 | |

| 財產和設備總計 | 減:累計折舊和攤銷 |

財產和設備合計(淨額)

折舊費用爲美元及$

幾年 分別截至2024年和2023年12月31日。該公司對其租賃物改進產生了美元的損失

關聯 截至2024年12月31日止年度的使用權資產。有關更多信息,請參閱註釋11。

83

附註5

租賃

2020年9月,BiomX以色列簽訂租賃協議 以色列尼斯錫安納的辦公空間,自2020年9月1日起爲期五年,可選擇再延長一段時間 至2030年11月30日。租賃協議項下的每月租賃付款約爲美元

與經營相關的補充現金流信息 租約如下:

止年度

| 12月31日, | 止年度 |

| 12月31日, | 經營租賃的現金付款 |

| 截至2024年12月31日,BiomX以色列的經營租賃 加權平均剩餘租期爲 | 年,加權平均貼現率爲 |

%. APT的經營租賃 加權平均剩餘租期爲

年,加權平均貼現率爲

兩者運營的成熟度分析 截至2024年12月31日的租賃情況如下:

操作

84

租賃

經營租賃付款總額

扣除估算利息

經營租賃負債餘額總額

BioMX Inc.

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

附註6

其他應付賬款

截至12月31日,

員工及相關機構

應計費用

政府機構

其他

注7

85

與關聯方的交易

2019年10月,BiomX以色列公司簽訂了一項金額爲#美元的貸款協議。

與一名在以色列因資本重組交易而被徵稅的股東打交道。作爲貸款協議的一部分,

股東持有的普通股被限制並分配給公司,並被公司記爲收購庫存股,金額相當於貸款。2022年,這筆貸款由股東償還給公司。在截至2023年12月31日的年度內,普通股股份轉讓給股東,並作爲庫存股的再發行入賬。

有關授予關聯方的股票期權,請參閱附註120亿。

有關與機構投資者簽訂證券購買協議,請參閱附註12A。

注8-

承諾和連續性2021年5月,APT與Viatris Inc.的全資子公司Oyster簽訂了一項合作和選擇協議(「Oyster協議」),合作使用APT的專有噬菌體技術治療某些眼科疾病。協議簽署後,Oyster預付了#美元。向APT支付,APT聲稱其在履行《牡蠣協定》義務的過程中花費了其中的一部分。2022年4月和2023年9月,APT收到了來自Oyster和Viatris Inc.的信件,對APT的行爲表示擔憂,包括指控APT違反了Oyster協議。2024年12月18日,APT和Oyster簽署了和解協議(《和解協議》),其中包括支付$

從APT到Oyster。截至2024年12月31日,本公司已記錄的準備金爲#美元。

作爲合併資產負債表中的其他應付帳款。2025年1月13日,APT向Oyster支付了$

根據和解協議。

2022年3月,IIA批准了一項總額爲新謝克爾的預算申請

數千歐元(約合人民幣1400元)

)與該公司的囊性纖維化候選產品有關。IIA承諾提供資金

批准預算的%。該計劃的有效期爲2022年1月至2022年12月。截至2024年12月31日,該公司收到了NIS

數千歐元(約合人民幣1400元)

批准預算的%。該計劃的有效期爲2023年1月至2023年12月。截至2024年12月31日,該公司收到了NIS

數千歐元(約合人民幣1400元)

86

)與該方案有關的國際投資協定。

BioMX Inc.

合併財務報表附註

| (美元以千爲單位,不包括每股和每股數據) | 注8- | 承付款和或有事項(續) | ||

| 根據 根據與IIA的協議,BiomX以色列公司將支付 | ||||

| %至 | 48 | 未來銷售額的百分比,最高不超過累積的金額 收到的補助金包括於1日公佈的12個月有擔保隔夜融資利率(「SOFR」)的年息 每個日曆年的交易日。BiomX以色列可能會被要求在發生某些事件時支付額外的版稅 由IIA確定,由BiomX以色列公司控制。截至以下日期,尚未發生或可能發生此類事件 與這些特許權使用費相關的資產負債表日期。補助金的償還取決於BiomX的成功完成 以色列的研發計劃和創造銷售。如果研發項目失敗,BiomX以色列公司沒有義務償還這些贈款, 如果未成功或已中止,或者未生成任何銷售。截至2024年12月31日,公司尚未產生銷售額;因此, 這些合併財務報表中未記錄任何負債。國際投資協定的贈款被記爲研發費用的減少(淨額)。 -- | ||

| 穿過 2024年12月31日,IIA批准的贈款總額約爲$ | 41 | (NIS | ||

| 數千人)。一直到12月31日, 2024年,BiomX以色列公司收到的總金額爲#美元 | 59 | (NIS | ||

| 數以千計),以國際投資協會的贈款形式提供。贈款總額 受特許權使用費限制,支付總額約爲$ | ||||

| 。截至2024年12月31日,BiomX以色列公司有或有義務 向內部投資協定提供約#美元的款項 | 72 | 包括適用於美元存款的SOFR的年息。 | ||

| 在……裏面 2015年6月,BiomX以色列與Yeda簽訂了經修訂的研究和許可協議(「2015許可協議」) 研發有限公司(「YEDA」),根據該公司,BiomX以色列公司獲得了獨家全球許可證 與微生物組的開發、測試、製造、生產和銷售有關的某些技術訣竅和研究信息 候選治療產品,包括協議中指定的候選產品,以及對噬菌體的專利、研究和其他權利 候選產品。作爲回報,BiomX以色列公司有義務支付YEDA每年約#美元的許可費 | 53 | 和收入的特許權使用費 如2015年許可協議中所定義。2019年7月,本公司與業達修訂了2015年許可協議,根據該協議, 資本重組交易完成後,本公司有義務向業達支付修正案中所述的一次性付款 不會超過 | ||

| 在涉及公司的某些合併或收購的情況下收到的對價的%。合併 附註1D所述的協議並不構成修正案所界定的合併或收購。 | 73 | 在從RondinX有限公司獲得轉讓後,BiomX以色列公司是2016年3月20日與Yeda簽訂的許可協議的一方,根據該協議,該公司擁有Yeda的與公司的元基因組靶標發現平台相關的技術訣竅、信息和專利的全球獨家許可。作爲許可證的對價,該公司有義務每年支付#美元的許可費 | ||

| ,但須遵守協議的條款和條件。如協議所述,任何一方均有權隨時以通知另一方的方式終止協議。此外,公司有義務根據產品的收入支付較低的個位數的特許權使用費。由於該公司尚未從運營中產生收入,截至2024年12月31日和2023年12月31日的合併財務報表中沒有包括與該協議有關的準備金。-- | 56 | 2017年12月,BiomX以色列與日本慶應義烏大學和JSR簽署了專利許可協議。根據協議,BiomX以色列公司獲得了與炎症性腸病(IBD)相關的某些專利權的獨家專利許可,作爲回報,該公司將支付每年美元的許可費。 | ||

| 及$ | 59 | 受制於協議中規定的條款和條件。此外,公司有義務根據臨床和監管里程碑的實現情況支付額外款項,總額最高可達$ | ||

| 以及基於未來收入的特許權使用費支付。由於公司尚未從運營中產生收入,而且不太可能實現某些里程碑,截至2024年12月31日和2023年12月31日的綜合財務報表中沒有與該協議相關的撥備。 | 75 | 2019年4月,BiomX以色列公司又簽署了一項專利 與日本慶應義塾大學和JSR的許可協議。根據協議,BiomX以色列公司獲得了獨家再許可,由 JSR獲得了與治療原發性硬化性膽管炎相關的某些專利權。作爲回報,公司被要求(I)支付 發證費用爲$ | ||

| 和每年的許可費,從1美元到1美元不等 | 68 | 至$ |

| (1) | (2)根據以下成就支付額外付款 臨床和監管里程碑,總額高達$ |

| (2) | (「定期貸款安排」),分三批提供,但須受若干條款及條件規限。第一 $的一批 |

| (3) | 於貸款協議籤立當日預付予本公司。第二批和第三批的里程碑 沒有聯繫到,並且已經過期了。該公司被要求在2023年3月1日之前只支付利息,並從那時開始 按月等額分期付款償還本金餘額和利息。 |

貸款協議規定, 公司可在任何時間根據貸款協議預付全部或部分預付款,預付款費用相當於

百分比 在截止日期後24個月但在36個月之前。在提前還款或償還所有或部分定期貸款時 在定期貸款安排下,本公司須支付相當於%的用戶 預付或償還的定期貸款的總金額。於2024年3月19日,本公司預付 總額爲$的定期貸款安排

。預付款包括期末費用#美元。

及應累算利息$ 。「公司」(The Company) 從Hercules收到關於預付款費用的豁免,該費用本應是

87

預付本金中的%等於 至$ 與定期貸款有關的利息支出,包括 綜合業務報表中的利息支出爲#美元。

及$

分別截至2024年和2023年12月31日止年度。

注11-商譽、無形資產與長期資產減值

商譽

在收購APT之後,公司確認了商譽 價值$在上述附註1D所述的測量期內進行調整後。2024年第三季度,公司 對商譽減值進行了量化評估,原因是公司股價下跌,導致其市場 資本低於公司的股東權益,管理層認爲這是一項減值指標。 該評估利用了公司的市值加上適當的控制溢價。市值已確定 即普通股流通股數乘以公司股票價格。控制權溢價確定 通過利用上市公司類似交易研究中的公開數據。根據評估,該公司得出結論 其報告單位的公允價值低於其賬面價值。因此,公司確認了全額商譽減值 共$

截至2024年12月31日的年度。

88

無形資產2024年第三季度,公司實現了量化 對其知識產權研發資產的評估,原因是公司股價如上所述下跌。評估表明 其知識產權研發的公允價值高於其賬面價值,且未確認減值。

BioMX Inc.

合併財務報表附註 (美元以千爲單位,不包括每股和每股數據)

附註12-

89

股東權益(續)基於股票的薪酬:(續)

股票期權:

2023年3月1日,董事會批准了這筆贈款 的根據2019年計劃,向49名員工、5名高級管理人員和3名董事提供選項,無需考慮。這些選項包括 以行使價$

每股,歸屬期間爲

四年。董事和高級管理人員有權獲得 在發生公司控制權變更和合同終止時加速其未授期權 和公司在一起。

2023年8月21日,董事會批准了 授予

根據公司2019年計劃,向兩名董事授予選擇權,無需考慮。期權是在一次演習中授予的 價格:$

每股,歸屬期間爲

90

四年

。董事有權在下列情況下全面加速其未獲授權的期權 發生本公司控制權變更及終止與本公司的業務往來。

2023年10月19日,董事會批准了 授予

2019年計劃下的一個董事的選項,未經考慮。這些期權是以行權價#美元授予的。

每股,歸屬期間爲

四年

。這樣的董事有權在發生時完全加速他的未歸屬期權 本公司控制權的變更及其與本公司的僱傭關係的終止。

2023年10月29日,董事會批准了 授予

根據2019年計劃,向4名員工和1名高級官員提供選項,無需考慮。這些期權是在 行權價爲$

每股,歸屬期間爲

四年

91

。高級官員有權全面加速其未授權的 發生本公司控制權變更及其與本公司合約終止時的期權。

2023年10月29日,董事會批准了一項削減 在購買公司普通股股份的每一項已發行期權的行使價(「重新定價」)中 目前由BiomX的員工持有,原始行權價高於$

根據公司2015年員工授予的每股 股票期權計劃至$

每股。除行權價外,重新定價的期權的其他授予條款沒有變化;然而, 在此之前,不得行使選擇權

一年

在重新定價日期之後。考慮了降低期權的行權價。

根據ASC 718的類型I修改。由於重新定價,公司立即確認了增量公允價值

總金額爲$

合併財務報表附註

(美元以千爲單位,不包括每股和每股數據)

92

附註12-

股東權益(續)

基於股票的薪酬:(續)

| 股票期權:(續) | 研究與開發費用,淨 | 止年度 ($)(1) |

12月31日, ($)(1) | 專業服務和分包商 工資及相關費用 ($)(4) | 股票補償 折舊 ($)(2) | 材料和用品 租金及相關費用 ($)(1)(3) | 其他 ($)(1) | ||||||||||||||||||||

| 減或有負債變化(見附註8 E) | 2024 | 415,103 | 50,689 | 49,798 | 460,921 | 102,081 | 1,078,592 | ||||||||||||||||||||

| 減合作協議收入(見注10 E) | 2023 | 412,135 | 201,234 | - | 404,174 | 100,998 | 1,118,541 | ||||||||||||||||||||

| 減去來自EIA和MTEC的贈款(見註釋8A和9) | 2024 | 179,905 | - | - | 124,854 | 46,793 | 351,552 | ||||||||||||||||||||

| 注14- | 2023 | 214,727 | 76,209 | - | 90,742 | 46,578 | 428,256 | ||||||||||||||||||||

| 一般及行政開支 | 2024 | 265,809 | 31,833 | 31,273 | 130,859 | 73,208 | 532,982 | ||||||||||||||||||||

| 止年度 | 2023 | 264,105 | 101,145 | - | 153,218 | 72,463 | 590,931 | ||||||||||||||||||||

| (1) | 12月31日, |

| (2) | 工資及相關費用 |

| (3) | 股票補償 |

| (4) | 專業服務 |

93

使用權資產

IPR & D -無形資產

私募認購令

固定資產

遞延所得稅負債總額

估值免稅額

遞延稅項淨資產

研發稅收抵免將於年開始到期 2038.

BioMX Inc.

合併財務報表附註