美國

證券交易委員會

華盛頓特區20549

Form

截至2024年6月30日季度結束

或

從 過渡到 的過渡期間。

委員會檔案編號

(依憑章程所載的完整登記名稱)

| (依據所在地或其他管轄區) 成立或組織) |

編號) 身份證號碼) |

|

|

||

| (總部辦公地址) | (郵遞區號) |

+

(註冊人的電話號碼,包括區號)

根據《證券法》第12(b)條註冊的證券:

| 每種類別的名稱 | 交易標的(s) | 每個註冊交易所的名稱 | ||

| N/A | N/A | N/A |

請用勾勾標示表明:

公司已在過去12個月(或公司被要求提交此類報告的較短期間)依照1934年證券交易法第13或15(d)條的規定提交所有必須提交的報告,並且公司在過去90天內一直受到此類提交要求的影響。 ☒

請勾選表示:在過去12個月內,是否公司已按照Regulation S-T第405條的規定電子提交了每一個互動數據檔案(本章第232.405條)(或公司在要求提交此類文件的更短期間內)。☒

選擇是否為大型快速申報法人、加速申報法人、非加速申報法人、較小型報表申報公司或新興成長公司。於 交換法案的第1202條中參閱對於「大型快速申報法人」、「加速申報法人」、「較小型報表申報公司」和「新興成長公司」的定義。

| 大型加速歸檔人 | ☐ | 加速歸檔人 | ☐ |

| ☒ | 小型報告公司 | ||

| 新興成長型企業 |

如果一家新興成長型公司, 請勾選√表示登記人已選擇不使用依照交易所法第13(a)條提供的任何新的或修訂財務 會計準則的延長過渡期遵守。 ☐

請勾選表示,公司是否屬於貝殼公司(根據《交易所法》第120億2條的定義) ☐ 是

截至2024年10月25日,公司傑出的負債 股普通股。

MARVION INC.

季度報告

2024年9月30日止季度

目錄

| 第一部分 - 財務信息 | 頁面 | |

| 項目1。 | 基本報表 | 10 |

| 未經審核的簡化合併資產負債表 | 10 | |

| 未經審計的綜合損益及綜合損益表 | 11 | |

| 未經審計的股東權益變動表 | 12 | |

| 未經審核之現金流量表 | 13 | |

| 基本報表未經審核簡明合併財務報表註腳 | 14 | |

| 項目2。 | 管理層對財務狀況和業績的討論與分析 | 33 |

| 第三項。 | 市場風險的定量和定性披露。 | 45 |

| 第四項。 | 內部控制及程序 | 45 |

| 第二部分 - 其他信息 | 46 | |

| 項目1。 | 法律訴訟 | 46 |

| 项目1A。 | 風險因素 | 46 |

| 項目2。 | 股票權益的未註冊銷售和資金用途 | 46 |

| 第三項。 | 優先證券違約 | 46 |

| 第四項。 | 礦業安全披露 | 46 |

| 项目5。 | 其他資訊 | 46 |

| 第6項。 | 展品 | 47 |

| 簽名 | 48 |

| 2 |

介紹評論

我們並非一家在香港經營的公司,而是一家在內華達州持有公司,通過我們完全擁有的子公司在香港和新加坡進行業務。我們的投資者持有Marvion Inc.的普通股,這是一家在內華達州的持有公司。這種架構存在獨特的風險,因為我們的投資者可能永遠不會直接持有我們在香港子公司的股權,而將依賴於我們子公司的貢獻來支持我們的現金流需求。我們從子公司獲得貢獻的能力受到香港和新加坡當局制定的法規的顯著影響。對現行規則和法規的解釋變化,或者新規則和法規的頒布,都可能對我們的業務和證券價值產生重大影響,包括導致我們的證券價值大幅下降或變得一文不值。有關與我們架構相關的公司面臨風險的詳細描述,請參考公司於2024年4月16日提交給美國證券交易委員會(SEC)的10-K形式的年度報告。風險因素 與在香港經營業務相關的風險。”公司年報中關於在香港經營業務風險的描述

Marvion Inc.及我們的香港附屬公司無需從中國證監會、網絡安全概念管理委員會或其他中國機構獲得許可或批准來運營我們的業務或向外國投資者發行證券。然而,鑒於中華人民共和國(“中華人民共和國”)政府最近的聲明和監管行動,例如與香港國家安全有關的聲明,禁止在特定行業營運的中國公司外資持股的法規的頒布,這些情況不斷演變,以及反壟斷疑慮,我們可能受到中華人民共和國政府未來行動的不確定性風險,包括我們在錯誤地得出這種批准不需要,相關法律、法規或解讀的變更導致我們未來需要獲得批准,或中華人民共和國政府可能禁止我們的控股公司結構,這可能導致我們業務重大變動,包括我們是否能繼續採用現有的控股公司結構、經營現有業務、接受外國投資,以及向投資者提供或繼續提供證券。這些負面行動可能導致我們的普通股價值大幅下降或變得毫無價值。如果我們未能遵守該等規則和法規,我們也可能會受到中華人民共和國監管機構(包括中華人民共和國證監會)實施的罰款和制裁,這可能會對公司證券繼續在場外交易板上交易的能力產生不利影響,這可能會導致我們證券價值大幅下跌或變得毫無價值。

我們在香港營運存在突出的法律和業務風險。例如,作為一家在美國上市的香港公開公司,我們可能面臨加強的監督、批評和負面宣發,這可能導致我們的業務和普通股價值出現重大變化。這也可能顯著限制或完全阻礙我們向投資者提供或繼續提供證券的能力,並導致此類證券的價值大幅下跌或變成無價之寶。我們面臨著來自中國法律制度的風險,在中國的法律執行方面存在風險和不確定性,中國政府可以在任何時候以極少或幾乎沒有事先通知的方式修改中國和香港的法規,包括對其執行和解釋的規定,并且可以在極少或幾乎沒有事先通知的情況下隨時介入。中國內部監管法規的變化,例如M&A規則、反壟斷法和數據安全法等,可能針對公司的公司結構,影響我們在香港開展業務、接受外國投資或在美國或其他國外匯率期貨上市。例如,中國政府啟動了一系列監管行動和聲明來規範中國內的業務運作,其中包括打擊證券市場非法活動,加強對海外上市中國公司使用變量利益實體結構的監管,在擴大材料安全評估範圍上采取新措施,以及加大反壟斷執法力度。2020年4月,中國網信辦及中國民政等中國監管機構頒佈了網絡安全評審辦法,並於2020年6月生效。根據網絡安全評審辦法,重要信息基礎設施的運營商在購買會影響國家安全的網絡產品和服務時,必須通過網絡安全評審。2021年7月10日,中國網信辦發布了網絡安全評審辦法的修訂草案,要求在“重要信息基礎設施運營商”之外,執行影響或可能影響國家安全的數據處理活動的“數據處理者”也應受到網絡安全評審,並進一步闡述評估相關活動的國家安全風險時應考慮的因素,包括(i)核心數據、重要數據或大量個人信息被竊取、洩露、毀壞和非法使用或出境的風險;以及(ii)核心信息基礎設施、核心數據、重要數據或大量個人信息在海外上市後被外國政府影響、控制或惡意使用的風險。中國網信辦表示,根據拟議的規定,持有100萬用戶數據的公司現在在尋求海外上市時必須申請網絡安全審批,因為該等數據和個人信息可能被“受影響、控制和惡意利用”而進行調查。網絡安全審查還將調查來自境外已上市新股的潛在國家安全風險。2022年1月4日,中國網信辦聯同其他12個政府部門發佈了新的網絡安全審查辦法。新措施)。新措施修訂了2021年7月10日發布的草案措施,並於2022年2月15日生效。

| 3 |

我們附屬公司的業務並不受中國網絡安全概念管理局的審查,原因是:(i) 我們在香港沒有一百萬個線上用戶;(ii) 我們的業務操作中沒有大量個人信息。此外,由於我們的收入水平是來自我們並經我們的審計師審核的,而且我們目前不打算或實施收購中國收入超過人民幣(“RMB”)40000萬的公司的控制權或決定性影響,因此我們也不受中國反壟斷執法機構的合併審查。目前,這些聲明和監管行動對我們的日常業務操作、接受外國投資並在美國或其他國外匯率期貨上市的能力沒有影響。然而,由於這些聲明和監管行動是新的,立法或管理規定機構將如何響應,現有或新的法律或規定或具體的實施和財報解讀將如何修改或頒布,如果有的話,以及這些修改或新的法律和規定將對我們的日常業務操作、接受外國投資以及在美國或其他國外匯率期貨上市的能力產生的潛在影響,都有很高程度的不確定性。關於公司在香港業務遇到的風險詳細描述和與我們業務相關的發行情況,請參閱“詳見年度報告。”風險因素 - 有關在香港從事業務的風險。

美國證券交易委員會和上市公司會計監督委員會(“PCAOB”)最近聯合聲明,以及《Holding Foreign Companies Accountable Act》(“HFCAA”),皆要求對新興市場公司的稽核資格進行更嚴格的評估標準,特別是非美國、未受PCAOB檢查的稽核師。若PCAOB判斷無法完全檢查或調查我們的稽核師,且交易所因此認為我們的證券應予以從交易所下市,我們的證券可能會受到HFCAA禁止交易的規定。2021年6月22日,美國參議院通過《Accelerating Holding Foreign Companies Accountable Act》,將觸發HFCAA禁令所需的連續未檢查年數從三年降為兩年,從而縮短我們的證券可能被禁止交易或下市的時間。2021年12月2日,美國證券交易委員會通過了實施HFCAA的規則。根據HFCAA,PCAOB發布了其報告,通知委員會,由於中國內地和香港當局的立場,無法完全檢查或調查總部位於中國內地或香港的會計事務所。我們的稽核師位於馬來西亞吉隆坡,受PCAOB的檢查。然而,如果馬來西亞當局隨後做出不允許PCAOB檢查我們稽核師的立場,那麼我們將需要更換稽核師,以避免我們的證券被下市。此外,由於HFCAA實施相關發展,我們無法保證在考慮我們稽核師的審計程序和質量控制程序、人員和培訓的適當性、資源的足夠性、地理覆蓋範圍或經驗與我們財務報表審計有關時,美國證券交易委員會或其他監管機構是否會對我們應用進一步更嚴格的標準。HFCAA規定PCAOB必須允許在兩年或三年內檢查發行人的會計事務所,如果未來PCAOB無法在那個時間檢查我們的會計事務所,則可能導致我們的證券在美國的交易市場遭到下市。請參閱:“風險因素- 外國公司負責法案要求公開公司會計監督委員會(PCAOB)被允許在三年內檢查發行人的會計師。如果《加速裁決外國公司負責法案》生效,這個三年期限將縮短為兩年。根據中國證券法,美國證券監管機構在中國境內進行調查和收集證據的程序和必要時間存在不確定性。如果美國證券監管機構無法進行此類調查,他們可以暫停或取消我們在美國證券交易市場的註冊,並將我們的證券從適用的交易市場退市。” 請參見年度報告。

除上述風險外,我們還面臨著來自於在香港從事業務的各種法律和運營風險和不確定性,如下總結和 “風險因素 — 有關在香港從事業務的風險。 記載於年度報告中。

| · | 中華人民共和國政府經濟和政治政策的不利變化可能對中國和香港的整體經濟增長產生重大和不利影響,這可能對我們的業務產生重大和不利影響。請參見「風險因素-我們面臨著中華人民共和國政府政策變化可能對我們在香港進行的業務以及該業務的盈利能力產生重大影響的風險。」與「Controlled」有相關的含義。中華人民共和國政府政治和經濟政策以及中華人民共和國法律和法規方面存在重大不確定性和限制可能對我們可能在中華人民共和國進行的業務以及因此對我們的營運和財務狀況產生重大影響。」記載於年度報告中。 |

| 4 |

| · | 我們是一家持有公司,通過位於香港和新加坡的全資子公司進行業務。這種結構帶來獨特的風險,因為我們的投資者可能永遠不會直接持有我們在香港和新加坡的子公司的權益,將依賴子公司的貢獻來為我們的現金流需求提供資金。我們的子公司能力受限,無法向我們支付款項可能對我們的業務進行有實質不利影響。我們不預期在可預見的將來支付股息;如果你期望分紅,應該不買我們的股票。請參見“風險因素-由於我們的控制項結構對支付股息或其他現金支付創造了限制,我們支付股息或作其他支付的能力受限。” 請參見年度報告。 | |

| · | 中國可能阻止我們在香港保留的現金流出,或中國可能限制將現金投入我們的業務或用於支付股息的情況。我們依賴我們香港子公司的股息來滿足我們的現金和融資需求,如支付我們可能負擔的任何債務所需的資金。任何此類管制或限制可能對我們籌集資金的能力,償還債務或支付股息或其他分配給股東的款項產生不利影響。詳情請參閱隨附代理聲明中的「風險因素 -我們的香港子公司可能受到限制,無法向我們支付股息或作其他支付,這可能制約其能夠滿足流動性需求,進行業務並向我們的普通股持有人支付股息。”;“風險因素-中國大陸對離岸控股公司向中國大陸實體提供貸款和直接投資以及政府管制貨幣兌換可能會延遲或阻止我們利用來自離岸融資活動所得款項向我們的香港子公司提供貸款或進行額外的資本注入英順控制項 - 可能會重大且不利地影響我們的流動性及資助和擴展業務的能力。風險因素 - 由於我們的控股公司結構導致支付分紅或其他現金支付受限,我們支付分紅或作其他支付的能力有所限制。以及「將資金轉移至和從我們的子公司」 記載於年度報告中。 | |

| · | 中國對境外控股公司向香港經營子公司提供貸款和直接投資的監管可能會延遲或阻礙我們使用本次發行所得款項向在香港的經營子公司提供貸款或增加資本。對於中國境外投資法的解釋以及它對我們當前的公司結構、公司治理和業務運作的影響可能性存在重大不確定性。請參閱「風險因素」風險因素 - 中國對境外控股公司向中國境內實體提供貸款和直接投資的監管以及政府對貨幣兌換的控制,可能會延遲或阻礙我們使用通過境外籌資活動獲得的款項向我們在香港的子公司提供貸款或增加資本,進而對我們的流動性和資助和擴展業務的能力產生重大且不利的影響。記載於年度報告中。」記載於年度報告中。 | |

| · | 鑒於中國將其權限擴展至香港,中國政府可以隨時毫無預先通知地改變香港的規則和規定,並能干預和影響我們在香港的營運和業務活動。目前我們無需獲得中國當局批准在美國交易所上市。但如果我們的子公司或控股公司將來需要獲得批准,或者我們錯誤地認為不需要批准,或者我們被中國當局拒絕營運或在美國交易所上市的許可,我們將無法繼續在美國交易所上市,我們的普通股價值可能會大幅下降或變得毫無價值,這將對投資者的利益造成實質影響。存在中國政府可能隨時干預或影響我們業務的風險,或對海外進行的企業融資活動產生更多控制以及對在香港上市發行人的外國投資的影響,可能會導致我們業務運作和/或證券價值發生重大變化。此外,中國政府可能採取更多監管措施和控制措施,限制或完全阻止我們向投資者發行或繼續發行證券,並造成該等證券價值大幅下降或變得毫無價值。請參閱「」風險因素-我們面臨中國政府政策變化可能對我們在香港進行業務及業務盈利能力產生重大影響的風險」和「中國政府的政治和經濟政策、中國法律和法規方面存在重大不確定性和限制可能會對我們在中國進行業務以及我們的營運和財務狀況產生重大影響。和"中國政府對我們必須進行業務活動的方式施加很大影響。目前,我們沒有被要求獲得中國當局批准在美國交易所掛牌。然而,如果中國政府對境外發行和/或對中國發行人的外國投資進行更嚴格控制,並且如果我們的中國子公司或控股公司日後被要求取得中國當局批准並且被中國當局拒絕在美國交易所掛牌,我們將無法繼續在美國交易所掛牌,我們的普通股價值可能大幅下降或變為無價值,這將對投資者利益產生實質影響。 載於年度報告中。 |

| 5 |

| · | 政府對貨幣兌換的控制可能會限制我們有效利用收入的能力,並影響您的投資價值。 | |

| · | 我們可能會受中國關於隱私、數據安全、網絡安全和數據保護的各種法律和法規的約束。我們可能對我們客戶提供的個人信息的不當使用或盜用承擔法律責任。請參見“風險因素- 中國政府對我們的業務活動進行了很大程度的影響。目前,我們無需獲得中國當局的批准在美國交易所上市。然而,如果中國政府對境外交易和/或對中國發行人的外國投資在未來施加更多控制,且我們的中國子公司或控股公司將來需要獲得中國當局的批准並被拒絕在美國交易所上市,我們將無法繼續在美國交易所上市,我們的普通股價值可能會大幅下跌或變得毫無價值,這將對投資者的利益產生重大影響。”詳見年度報告中訂明的內容。 | |

| · | - 根據中國企業所得稅法,我們可能被歸類為中國的“居民企業”。這種分類可能對我們和非中國股東產生不利的稅務後果。請參見“風險因素- 我們的全球收入可能根據中國企業所得稅法而須繳納中國稅款,這可能對我們的業務運營產生重大不利影響。” 請參見年度報告。 | |

| · | 未能遵守中國大陸有關中國大陸居民設立境外特殊目的公司的規定可能使我們的中國大陸居民股東承擔個人責任,可能限制我們收購香港和中國大陸公司或向我們的香港子公司注入資本的能力,可能限制我們的香港子公司向我們分配利潤,或可能對我們產生重大負面影響。 | |

| · | 您可能需就從我們獲得的分紅或我們普通股轉讓所獲利润支付中國大陸所得稅。請參閱《風險因素》風險因素- 分配給我們外國投資者的股息和我們外國投資者出售普通股所獲利潤可能被中國大陸徵收稅項。附載於年度報告中的內容。 | |

| · | 對於非中國大陸控股公司間接轉讓中國大陸居民企業的所有權可能會帶來不確定性。請參閱《風險因素》風險因素- 對於非中國控股公司間接轉讓中國內地居民企業的股權,我們和股東面臨著不確定性。” 規定於年度報告中。 | |

| · | 我們依據內華達州法律組建成為一家控股公司,並通過在香港、新加坡和英屬維京群島等外國司法管轄區組建的多個子公司從事業務。這可能對美國投資者強制執行在美國法院對這些實體獲得的判決、在香港對我們或我們管理層提起訴訟或為國外子公司的董事會成員進行送達帶來負面影響。請參見“風險因素- 我們幾乎所有的資產和大多數的高級職員和董事都設在香港。餘下的董事和高級職員位於新加坡。因此,股東可能難以強制執行在美國獲得的對我們、我們的高級職員或董事的判決,這可能限制股東本應可享有的救濟措施。。” 規定於年度報告中。 | |

| · | 美國監管機構可能會受到在中國進行調查或檢查的能力的限制。 | |

| · | 對於我們中國子公司的源對源扣繳稅負的不確定性很大,我們中國子公司支付給我們境外子公司的股息可能無法符合享有某些條約優惠的條件。請參見“風險因素- 我們的全球收入可能會根據中國企業所得稅法律受到中國稅收的影響,這可能會對我們的業務成果產生重大不利影響。載列於年度報告中。 |

本登記聲明中對「公司」、「MVNC」、「我們」、「我們」和「我們的」的引用指的是內華達州的Marvion Inc.公司及其所有子公司的合併基礎。在需要提及特定實體的情況下,將引用該特定實體的名稱。

| 6 |

與我們的子公司之間的現金轉移

Marvion Inc.是一間位於內華達州的控股公司,自身沒有營運。我們主要通過在香港和新加坡的子公司進行業務。我們可能依賴香港和新加坡的子公司通過分紅或其他資金轉移來籌措現金及融資需求,包括支付股東們分紅和其他現金分配所需的資金,還有支付我們可能產生的任何債務以及支付我們的營業費用。如果我們的香港和新加坡子公司將來為自己負債,則管理債務的工具可能限制他們支付股息或向我們進行其他分配的能力。迄今為止,我們的子公司尚未將任何現金流或其他資產的轉移、分紅或分配給Marvion Inc.,而Marvion Inc.也未將任何現金流或其他資產的轉移、分紅或分配給我們的子公司。

Marvion Inc.根據內華達法律被允許向我們在香港和新加坡的子公司提供資金,並通過貸款或資本出資收到資金,並且不受基金金額限制,但在符合相關政府登記、批准和申報要求的前提下。我們的香港子公司Marvion(香港)有限公司、Marvion Studios有限公司(MSL)(前稱Typerwise有限公司)和Marvel Multi-dimensions有限公司(MMDL),以及我們的新加坡子公司Marvion Private Limited,根據香港和新加坡法律也被允許通過分紅派息向Marvion Inc.提供和獲取資金,並且基金金額沒有限制。截至本報告日期,控股公司或子公司之間沒有進行分紅或派息,我們也不預期在可預見的將來控股公司與其子公司之間會發生此類分紅或派息。

我們目前打算保留所有可用資金和未來盈利(如果有的話),用於控制項和擴大我們的業務,並且不預計在可預見的將來宣布或支付任何分紅派息。有關我們股息政策的任何未來決定將由我們的董事會酌情考慮我們的財務狀況、營運結果、資本需求、合同需求、業務前景和董事會認為相關的其他因素後做出,並受制於未來任何融資工具中包含的限制。

根據內華達修訂法案和我們的章程,我們的董事會可以在他們認為適當的時間和金額下,授權並宣佈向股東支付股利,如果他們有合理理由相信,在分紅後,我們的資產價值將超過我們的負債,並且我們將能夠按期支付債務。對我們通過股息分派的資金額沒有進一步的內華達法定限制。

根據香港稅務局目前的實務,我們支付的分紅在香港不須納稅。中華人民共和國的法律法規目前對將現金從Marvion Inc.轉至我們的香港子公司或從我們的香港子公司轉至Marvion Inc.沒有實質影響。根據香港法律,對香港元(「HKD」)轉換為外幣及匯款離港或跨境匯款至美國投資者均沒有限制。

中华人民共和国有可能阻止我们在香港维护的现金流出,或限制将现金投入我们的业务或用于支付分红派息。任何此类管制或限制可能会对我们融资需求的能力,偿还债务或向股东分红或其他派息产生不利影响。 请参阅“风险因素 - 我们的香港子公司可能受限于支付分红或向我们作出其他付款,这可能限制其满足流动性需求,开展业务并向我们的普通股持有人支付股息。”;“风险因素 - 中华人民共和国对离岸控股公司向中华人民共和国实体发放贷款和直接投资以及货币兑换的政府控制可能会延迟或阻止我们利用其从离岸融资活动中获得的收益,向我们的香港子公司发放贷款或做出追加资本贡献,这可能会对我们的流动性和资金和扩展业务的能力产生重大和不利影响。”;“风险因素 - 因为我们的控股公司结构对分红或其他现金支付造成限制,我们支付分红或做其他支付的能力受到限制。”

| 7 |

Current PRC regulations permit PRC subsidiaries to pay dividends to Hong Kong subsidiaries only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation. As of the date of this report, we do not have any PRC subsidiaries.

The PRC government imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency to finance our cash requirements, service debt or make dividend or other distributions to our shareholders. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our common stock.

Cash dividends, if any, on our common stock will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%.

In order for us to pay dividends to our shareholders, we will rely on payments made from our Hong Kong and Singapore subsidiaries to Marvion Inc. If in the future we have PRC subsidiaries, certain payments from such PRC subsidiaries to Hong Kong subsidiaries will be subject to PRC taxes, including business taxes and VAT. As of the date of this report, we do not have any PRC subsidiaries and our Hong Kong and Singapore subsidiaries have not made any transfers, dividends or distributions nor do we expect to make such transfers, dividends or distributions in the foreseeable future.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC entity. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including, without limitation, that (a) the Hong Kong entity must be the beneficial owner of the relevant dividends; and (b) the Hong Kong entity must directly hold no less than 25% share ownership in the PRC entity during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by a PRC subsidiary to its immediate holding company. As of the date of this report, we do not have a PRC subsidiary. In the event that we acquire or form a PRC subsidiary in the future and such PRC subsidiary desires to declare and pay dividends to our Hong Kong subsidiary, our Hong Kong subsidiary will be required to apply for the tax resident certificate from the relevant Hong Kong tax authority. In such event, we plan to inform the investors through SEC filings, such as a current report on Form 8-K, prior to such actions. See “Risk Factors – Risks Relating to Doing Business in Hong Kong.” set forth in the Annual Report.

| 8 |

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended that are not historical facts, and involve risks and uncertainties that could cause actual results to differ materially from those expected and projected. All statements, other than statements of historical facts, included in this Quarterly Report on Form 10-Q including, without limitation, statements in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” regarding the Company’s market projections, financial position, business strategy and the plans and objectives of management for future operations, events or developments which the Company expects or anticipates will or may occur in the future, including such things as future capital expenditures (including the amount and nature thereof); expansion and growth of the Company’s business and operations; and other such matters are forward-looking statements. These statements are based on certain assumptions and analyses made by the Company in light of its experience and its perception of historical trends, current conditions and expected future developments, as well as other factors it believes are appropriate under the circumstances. However, whether actual results or developments will conform with the Company’s expectations and predictions is subject to a number of risks and uncertainties, including general economic, market and business conditions; the business opportunities (or lack thereof) that may be presented to and pursued by the Company; changes in laws or regulation; and other factors, most of which are beyond the control of the Company.

這些前瞻性聲明可以通過使用預測、未來式或前瞻性術語來識別,例如「相信」、「預期」、「期望」、「估計」、「計劃」、「可能」、「將會」或類似術語。這些聲明出現在本申報書的許多地方,包括有關公司意向、信念或當前期望以及董事會或高管對公司財務狀況或營運結果的趨勢(第一);公司的業務和增長戰略(第二);公司的融資計劃(第三)。投資者應當注意,任何這類前瞻性聲明並非未來業績的保證,涉及重大風險和不確定因素,實際結果可能與前瞻性聲明預期的有所不同,這是由於各種因素導致的。可能對實際結果和表現產生不利影響的因素包括公司的有限經營歷史、季度營運結果和費用的潛在波動,政府監管、技術變革和競爭。關於識別可能導致實際結果與前瞻性聲明預期有顯著差異的重要因素的信息,請參閱公司年度報告中的風險因素部分。

因此,本季度10-Q表格中提出的所有前瞻性陳述都受到這些警語陳述的限制,公司無法保證實際結果或預期發展將被實現,即使實際實現,也不能確保對公司或其業務或運營的預期後果產生預期影響。該公司不承擔更新任何此類前瞻性陳述的義務。

| 9 |

第一部分 - 財務信息

項目1. 基本報表

馬維恩公司及其附屬公司

未經核數的簡明合併資產負債表

(货币以美元(“US$”)表示,股份数量除外)

2024年9月30日 | 2023年12月31日 | |||||||

| (重申) | ||||||||

| 資產 | ||||||||

| 流動資產: | ||||||||

| 應收賬款 | $ | $ | ||||||

| 現金及現金等價物 | ||||||||

| 預付費用及其他流動資產 | ||||||||

| 全部流動資產 | ||||||||

| 非流動資產: | ||||||||

| 在建工程 | ||||||||

| 物業及設備,扣除折舊後淨值 | ||||||||

| 淨使用權資產 | ||||||||

| 非流動資產總額 | ||||||||

| 總資產 | $ | $ | ||||||

| 負債和股東資本赤字 | ||||||||

| 流動負債: | ||||||||

| 應付賬款 | $ | $ | ||||||

| 應計費用及其他應付款 | ||||||||

| 應付董事款項 | ||||||||

| 應付施工款 | ||||||||

| 可轉換票據應付款 | ||||||||

| 本票 | ||||||||

| 租賃負債 | ||||||||

| 應付期票 | ||||||||

| 應交稅項 | ||||||||

| 流動負債合計 | ||||||||

| 非流動負債: | ||||||||

| 租賃負債 | ||||||||

| 负债合计 | ||||||||

| 合約和可能負債 | ||||||||

| 股東的赤字: | ||||||||

| 優先股,面額 $, 授權股份 和 截至2024年9月30日和2023年12月31日,分別有未指定的股份。 | ||||||||

| 優先股,A系列,面值$, 設定的股份, 和 於2024年9月30日和2023年12月31日分別發行並持有股份 | ||||||||

| 優先股,乙系列,面值 $, 指定的股份, 和 股份於2024年9月30日及2023年12月31日分別註冊發行並完全實收 | ||||||||

| 優先股,丙系列,面值 $, 股 指定的, 和 股於2024年9月30日及2023年12月31日分別註冊發行並完全實收 | ||||||||

| 普通股,面額 $, 已授權股份為 和 已發行並流通股份截至2024年9月30日和2023年12月31日 | ||||||||

| 資本公積額額外增資 | ||||||||

| 其他綜合收益累計額 | ||||||||

| 累積虧損 | ( | ) | ( | ) | ||||

| 股東赤字總額 | ( | ) | ( | ) | ||||

| 負債總額和股東權益赤字 | $ | $ | ||||||

請參閱未經審核的簡明綜合基本報表附註。

| 10 |

馬維恩公司及其附屬公司

未經審核的總體綜合狀況 營運報告

全面(虧損)收益

(货币以美元(“US$”)表示,股份数量除外)

截至三個月結束 九月三十日, | 截至九個月結束時 九月三十日, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| 營業收入 | $ | $ | $ | $ | ||||||||||||

| 銷貨成本 | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| 毛利潤 | ||||||||||||||||

| 營業費用: | ||||||||||||||||

| 總部開支 | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| 總營業費用 | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| 營運(虧損)收入 | ( | ) | ( | ) | ||||||||||||

| 其他收入: | ||||||||||||||||

| 利息收入 | ||||||||||||||||

| 其他收益合計 | ||||||||||||||||

| 稅前(虧損)收入 | ( | ) | ( | ) | ||||||||||||

| 所得税費用 | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| 淨(虧損)利益 | ( | ) | ( | ) | ||||||||||||

| 其他綜合收益: | ||||||||||||||||

| 外幣兌換調整(損失)收益 | ( | ) | ||||||||||||||

| 綜合(虧損)收益 | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| 每股純損益: | ||||||||||||||||

| 基本 (1) | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| 稀釋 (1) | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| 加權平均普通股股本: | ||||||||||||||||

| 基本 # | ||||||||||||||||

| 稀釋 # | ||||||||||||||||

| (1) |

參見未經審核簡明綜合基本報表附註。

| 11 |

馬維昂公司及其子公司

未經審核的簡明綜合合併財務報表 股東權益變動表

(货币以美元(“US$”)表示,股份数量除外)

| 優先股 | 普通股票 | 額外 | 累计資產 其他 全面性 | (累積損失 赤字) | 總計 股東的 | |||||||||||||||||||||||||||

| 數量 股份 | 金額 | 股數 股 | 金額 | 實收資本 資本 | 收入 (失敗) | 保留盈餘 收益 | (deficit) 股東權益 | |||||||||||||||||||||||||

| 截至2024年9月30日三個月和九個月結束的情況 | ||||||||||||||||||||||||||||||||

| 2024年1月1日的結餘(經過調整) | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||||||

| 外匯翻譯調整 | – | – | ||||||||||||||||||||||||||||||

| 期間淨利潤 | – | – | ||||||||||||||||||||||||||||||

| 截至2024年3月31日的餘額 | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| 外匯翻譯調整 | – | – | ( | ) | ( | ) | ||||||||||||||||||||||||||

| 期間凈利潤 | – | – | ||||||||||||||||||||||||||||||

| 截至2024年6月30日的餘額 | ||||||||||||||||||||||||||||||||

| 發行股份用於收購法律收購方 | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| 法律收購方資本重組 | – | – | ( | ) | ||||||||||||||||||||||||||||

| 外幣翻譯調整 | – | – | ||||||||||||||||||||||||||||||

| 本期淨虧損 | – | – | ( | ) | ( | ) | ||||||||||||||||||||||||||

| 截至2024年9月30日的餘額 | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||||||

| 截至2023年9月30日的三個月和九個月 | ||||||||||||||||||||||||||||||||

| 2023年1月1日的結餘(重新整理) | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||||||

| 外匯換算調整 | – | – | ||||||||||||||||||||||||||||||

| 期間淨利潤 | – | – | ||||||||||||||||||||||||||||||

| 截至2023年3月31日之結餘 | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| 外匯換算調整 | – | – | ( | ) | ( | ) | ||||||||||||||||||||||||||

| 期間凈利潤 | – | – | ||||||||||||||||||||||||||||||

| 截至2023年6月30日的結餘 | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| 外幣換算調整 | – | – | ( | ) | ( | ) | ||||||||||||||||||||||||||

| 期間凈利潤 | – | – | ||||||||||||||||||||||||||||||

| 2023年9月30日的結餘 | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||||||

請參閱未經審核的簡明綜合財務報表附註。

| 12 |

馬維恩公司及其附屬公司

未經核數的簡明合併現金流量表

(以美元("US$")表示的货币)

| 截至9月30日止九個月 | ||||||||

| 2024 | 2023 | |||||||

| 經營活動現金流量: | ||||||||

| 淨(虧損)利益 | $ | ( | ) | $ | ||||

| 調整以協調淨(虧損)收入和營業活動提供的(使用的)净現金 | ||||||||

| 固定資產及設備折舊 | ||||||||

| 使用資產攤銷 | ||||||||

| 租賃負債利息開支 | ||||||||

| 營運資產及負債的變動: | ||||||||

| 應收賬款 | ( | ) | ( | ) | ||||

| 應付賬款 | ( | ) | ||||||

| 應付施工款 | ( | ) | ||||||

| 預付費用及其他流動資產 | ( | ) | ( | ) | ||||

| 應計負債及其他應付款 | ||||||||

| 运营租赁负债 | ( | ) | ( | ) | ||||

| 應付所得稅 | ||||||||

| 營運活動產生的淨現金流量 | ( | ) | ||||||

| 投資活動之現金流量: | ||||||||

| 購買不動產和設備 | ( | ) | ( | ) | ||||

| 投資活動中使用的淨現金 | ( | ) | ( | ) | ||||

| 來自籌資活動的現金流量: | ||||||||

| 董事預付款 | ||||||||

| 籌資活動提供的淨現金 | ||||||||

| 匯率對現金及現金等價物的影響 | ( | ) | ||||||

| 現金及現金等價物淨變動 | ( | ) | ||||||

| 本期初現金及現金等價物 | ||||||||

| 本期末現金及現金等價物 | $ | $ | ||||||

| 現金流量資訊的補充披露: | ||||||||

| 支付所得稅現金 | $ | $ | ||||||

| 支付利息的現金 | $ | $ | ||||||

| 非現金投資和融資活動: | ||||||||

| 通過分享交易發行應收盈餘負債的本票 | $ | $ | ||||||

請參閱未經審核的簡明綜合財務報表附註。

| 13 |

馬維恩公司及其附屬公司

未經審計的簡明合併財務報表附註

截至2024年9月30日三個月和九個月

1. 報告 之基礎

這些附屬的未經審核的簡明會 計基本報表 ,是根據美國通行的會計原則(“美國通行會計準則”)編製的,用於根據證券及 交易所 委員會(“SEC”)的規則和法規編制中期財務信息。因此,它們不含所有美國通行會計準則所需的所有信息和附註,以製備完整的財務報表。據管理層認為,已包括使財務報表不會誤導的所有必要調整(包括正常的週期性應計項目)。截至2024年9月30日的期間營運結果,不一定代表預期到2024年12月31日財政年度的結果。本季度10-Q表中所包括的信息應與公司截至2023年12月31日財政年度的年報10-K中所包括的管理層討論與分析以及 財務報表 和附註共同閱讀,該年報於2024年4月16日向SEC提交。

2. 組織 及業務背景

Marvion Inc.於2008年3月6日在內華達州成立。本公司及其附屬公司以下簡稱為(“公司”)。

於2024年8月15日,公司及總部設於英屬維爾京群島的United Warehouse Management Corp股份公司(以下簡稱“UWMC”)及UWMC的十一位股東達成了一項股份交換協議(即“SEA”),根據該協議,UWMC的股東同意將股份轉讓給公司。 UWMC股份的所有擁有人與公司交換,而這些擁有人擁有的是UWMC所有已發行及流通的證券。 公司每股面值$的普通股作為交換條件。 每股$的普通公司股份交易。

就股份交換交易而言,公司所有先前的高級管理人員和董事已辭職,新的高級管理人員和董事已被任命為公司的高級管理人員和董事。這種股份交換交易被記入為反向合併和公司重資,根據這種交易,UWMC被視為會計收購方(法律上的獲收購方),而公司被視為會計被收購方(法律上的收購方)。因此,公司的合併資產、負債和營運結果將成為UWMC的歷史基本報表,公司的資產、負債和營運結果將自股份交換交易之日起與UWMC合併。在這項交易中不承認商譽。股份交換交易之前的歷史基本報表為會計收購方(UWMC)的基本報表。逆向合併之前的會計收購方歷史股東權益(由於重資而被重新計算)按照合併所獲得的股份數額進行遞延重述。合併之前的營運屬於收購方。在完成股份交換交易後,公司隨附的截至2024年9月30日和2023年9月30日九個月未經審計的簡明合並財務報表已根據所呈現的所有期數進行重新編製。

除了股份交易外,公司同意根據每六個月期間結束於6月30日和12月31日的每個「績效期間」,根據UWMC達成特定淨利潤表現里程碑而支付總金額為$的「平均」付款。 (合稱為「維持付款」)。總共九個績效期間。維持支付將以無息本票形式支付,由UWMC的股東平均共享。

| 14 |

目前,該公司主要從事香港的物流服務、倉儲服務和財務諮詢服務。

子公司的說明:

| 姓名 |

註冊地點 and kind of 法律實體種類 |

主要活動 and place of operation |

已註冊/付清細項 普通股資本的部分 |

持有的有效利益 股份 | ||||

| United Warehouse Management corp.(“UWMC”) | ||||||||

| KSk物流有限公司(“KSK”) | ||||||||

| Propose企業有限公司(“PEL”) | ||||||||

| 聯合倉儲管理有限公司(“UWML”) |

本公司及其附屬公司以下簡稱(「本公司」)。

3. SUMMARY OF SIGNIFICANt ACCOUNTING POLICIES

隨附的未經審核 簡明綜合基本報表反映了本註解中描述的某些重要會計政策的應用 以及隨附的未經審核簡明綜合基本報表和附註中其他地方。

合併基礎

未經審計的簡明綜合基本報表包括MVNC及其子公司的賬戶。公司內所有重要的關聯公司餘額和交易在合併時已予以消除。

使用估計和假設

在準備這些未經審核的簡明合併基本報表時,管理層需作出影響資產和負債數額以及報告期間內收入和支出的估計和假設。 實際結果可能與這些估計不同。如果實際結果與公司的估計顯著不同,公司的財務狀況和營運結果可能會受到重大影響。 本期內的重大估計包括數碼資產的減損損失、無形資產的估值和使用年限,以及逆向所得稅賦免許。

| 15 |

現金及現金等價物

現金及現金等價物按成本列報,代表手頭現金、存放在銀行或其他金融機構的活期存款以及所有具有原始期限三個月或以下的高流動性投資,截至該等投資購買日期為止。

應收帳款

應收賬款按客戶應付的毛額賬單金額記錄,扣除預期信用損失的賬項。應收賬款不帶利息,在發票日期後30天被視為逾期。公司定期評估應收賬款的預期信用損失,根據應收賬款的回收能力和個別賬戶分析,包括每位客戶的當前信用狀況、過往收款歷史以及當前的經濟行業趨勢。當有客觀證據表明餘額可能無法收回時,就會出現損失。特別是在損失事件方面,需要運用判斷和估計,包括對個別敞口的具體損失的估計以及對歷史收款趨勢的預備。根據對客戶信用和持續關係的分析,管理層會就是否任何期末未償還的餘額單獨及根據帳齡分析來決定是否視為不可收回。預期信用損失的備抵金額記錄在應收賬款餘額中,並在損益表中記錄相應費用。在管理層確定無法收回的可能性不很高後,逾期賬戶餘額將被扣除預期信用損失備抵金。

截至2024年9月30日

及2023年12月31日,

財產和設備

資產和設備按成本減除累計折舊和累計減損費用(如有)。折舊乃根據直線法按照以下預期使用年限自完全投運後開始計算,並考慮其估計殘值:

| 預期使用壽命 | ||

| 倉庫設施 | ||

| 設備 | ||

| 機動車 |

維護和修理支出,不會實質延長資產的使用壽命,將在發生時記入費用。將大規模更新和改善支出資本化,因為它們實質延長了資產的使用壽命。已退出或出售的資產的成本及相關的累計折舊將從相應帳戶中移除,任何收益或損失將於經營報告書中作為其他收入或費用確認。

在建工程

施工中主要包括尚未投入使用的倉儲設施的施工。在資產完成並投入使用之前,施工中不提供折舊。

| 16 |

無形資產減損

根據ASC 360號準則的規定,所有長壽命資產,如財產、廠房和設備以及公司持有的所有在建工程,均在公司所擁有並持有的情況下,當出現事件或情況發生變化指示資產帶入價值可能無法收回時,均會進行損耗測試。對於持有並使用的資產的可收回性是通過將資產的帶入金額與預計由資產產生的未來未折抵現金流量進行比較來進行評估。如果這些資產被認為有損耗,則將認可的損耗量是通過資產的帶入金額超過資產公平價值的金額來衡量。到截止日期,對截至2024年和2023年9月三個和九個月的長壽命資產進行了損耗認定。

租賃

公司採用FASB會計準則更新(ASU)2016-02「租賃(842號題)」以呈現所有期間。該準則要求承租人在未經審計的簡明合併資產負債表上,辨認租賃資產(使用權)和相關租賃負債(租賃負債),對於超過十二個月的租賃期。對於十二個月或更短期的租賃期,承租人可以選擇採用會計政策,不辨認租賃資產和負債。

公司在合約起初確定是否為租賃。營運租賃包括在未經審計的總體資產負債表中的營運租賃使用權資產和營運租賃負債。財務租賃包括在未經審計的總體資產負債表中的財務租賃使用權資產和財務租賃負債。

ROU資產代表公司在租賃期間使用基礎資產的權利,而租賃負債代表公司根據租約發生的租金支付義務。根據租賃支付的現值在租賃期間的折現,確認營運租賃和融資租賃的ROU資產和負債,以租約中的隱含利率折現計算。在無法輕易確定隱含利率的情況下,公司將在起始日期根據可用資訊使用其增量借貸利率確定租賃支付的現值。增量借貸利率是指公司為了借入相等於租金的金額,以抵押方式在類似經濟環境和相似期限內需要支付的利率。公司將ROU資產從租約起始日期按直線法提撥,直至ROU資產的可用年限結束或租約期滿早期。租金支付的租約支出將在租約期間按直線方式確認。

所有板塊的房地產業租賃均屬於營運租賃,並且沒有租賃期少於十二個月。

營業收入認列

公司採納《會計準則更新(ASU)》2014-09號。 客戶合同的營業收入 (主題606)《ASU 2014-09》全面追溯過渡法。公司採用ASU 2014-09對未經審查的簡明綜合財務報表中承認的收入金額和時間並無實質影響。

公司遵循以下五個步驟,以判斷在履行各項協議時應確認的適當營業收入金額:

| · | 判斷與客戶的合約; |

| · | 判斷合約中的履行義務; |

| · | 確定交易價格; |

| · | 將交易價格分配至合約中的履行義務;以及 |

| · | 當履行義務得以滿足時,才能確認營業收入。 |

| 17 |

當公司將承諾的產品轉移給取得產品控制權且收款合理得到保證的客戶時,營業收入將予以認列。履行義務是合約中向客戶轉移一個明確的產品或服務的承諾。公司大部分的合同僅包含一個履行義務,當履行義務完成時,相應費用將向客戶開具帳單。公司在確定金額已確定且履行義務已完成的期間內確認此類營業收入,並且公司完成履行義務時。

營業收入是按公司預期收到的交易對價為基準計量的,以換取產品或提供服務。因此,營業收入扣除了退貨、折讓、客戶折扣和獎勵後記錄。銷售稅和其他稅項不包含在營業收入中。

隨著2023年10月新倉庫建設的進展,公司將專注於向客戶提供物流和倉儲服務,通過在倉庫設施中存儲商品,以及從倉庫運輸至客戶指定的國內目的地的包裝、交付和運輸服務。

物流服務

從物流解決方案收入中,該般地方交通、送貨和包裝服務於商品由公司打包並運送到客戶指定的國內目的地之際予以確認。一般而言,公司按月開出發票並在信用期為30天的情況下收取應收款項。

倉儲服務

從儲存服務產生的收入將按照合約或安排的任期均衡認列,因為公司通過持續將控制權轉移給客戶而執行合同義務,客戶同時也可以在公司履行過程中即時接受和消費公司的表現所帶來的好處。公司通常每月月底向客戶開具按月事後服務費帳單。當服務提供完畢時,履行責任即告完成。倉儲合約通常包括1-6年的繼續存儲服務,可選擇續約。

財務諮詢服務

該公司還向客戶提供財務諮詢服務,一般情況下,在履行完履行義務後向客戶開具發票。服務期限較短,通常在3個月內。待提供的財務諮詢服務的成交價通常基於合同價格。公司從協助向不同信貸機構提供融資方案收取的費用在服務完成並交付給客戶時被認可,並於當時計入收入。

公司作為提供前述服務的主要方,在公司自行決定價格並自行選擇承運人或服務提供商的情況下,根據公司的判斷基礎上按毛額確認營業收入。

| 18 |

所得稅

公司採納了ASC 740基本報表 “所得稅” 根據第740-10-25-13段的規定,公司應留意於基本報表中是否應記錄聲稱了或預期會在稅務申報中聲稱的稅務利益。根據第740-10-25-13段的規定,公司僅當不確定的稅務立場在稅務檢查中更有可能被稅務機構接受,且是基於該立場的技術優勢時,方可承認來自不確定稅務立場的稅務利益。基於尚未經計算的合併財務報表,應根據那筆可能性大於百分之五十(50%)的最大利益來衡量該立場認可的稅務利益,此利益應在最終比對中被實現的可能性大於百分之五十(50%)。第740-10-25-13段也提供有關取消認列、歸類、利息和所得稅的罰款、分期帳等方面的指導,並要求增加披露。根據第740-10-25-13段的規定,公司對於未認列所得稅利益的負債沒有重大調整。

資產和負債的稅基之間的暫時差異的未來估計稅收影響,以及稅款抵扣和抵消在附帶的未經審計簡明綜合資產負債表上報告。公司定期審查其未經審計的簡明綜合資產負債表上記錄的遞延所得稅資產的回收情況,並根據管理層認為必要時提供估值準備。

分部報告

會計標準編碼 (“ASC”)第280號主題,分節報告建立了一套關於據公司內部組織架構報告營運部門信息的標準,以及關於地理區域、業務部門和重要客戶在未經查核的簡明綜合基本報表中的信息。目前,公司在香港經營兩個業務部門。

合約和可能負債

公司遵循ASC 450-20,承諾記錄負債的會計處理。在未經審計的簡明綜合財務報表發行之日可能存在某些條件,這可能會導致公司損失,但只有在一個或多個未來事件發生或未發生時才會解決。公司評估此類可能負債,這種評估固有地涉及判斷的運用。在評估與針對公司所面臨的未結案訴訟或可能導致此類訴訟的未主張索賠相關的損失條件時,公司評估任何訴訟或未主張索賠的認為價值以及在其中尋求或預計尋求的救濟金額的認為價值。

如果對一項潛在損失的評估顯示該損失很可能已經發生,並且可以估計到責任金額,那麼該估計的責任金額將納入公司未經審核的簡明綜合基本報表中。如果評估顯示一項潛在重大損失條款並不大可能發生,但存在合理可能性;或者很可能發生但無法估算金額,則應在可能確定且重大的範圍內,披露應急責任的性質和可能損失範圍的估計。

損失條件被視為遠程的情況通常不會被揭露,除非它們涉及保證,在這種情況下,保證將被揭露。根據目前可用的信息,管理層認為這些事項不會對公司的財務狀況、經營結果或現金流量產生重大不利影響。然而,無法保證此類事項不會對公司的業務、財務狀況、經營結果或現金流量產生重大不利影響。

不確定稅務項目

本公司於截至2024年6月30日止的六個月期間並未作出任何實質性的資本投資貢獻。

| 19 |

本公司根據ASC 260“ ”進行凈利潤(損失)每股計算。每股盈利基本每股收入(損失)是通過將凈收入(損失)除以期間內流通普通股平均股份數進行計算。稀釋每股收入(損失)的計算方式與基本每股收入(損失)相似,唯一不同的是分母包括了已發行的潛在普通股等當沖股份數,以及若該額外普通股份數將導致股數稀釋而增加的。

外匯貨幣翻譯

以非功能貨幣計價的交易,將以交易當日的匯率換算為功能貨幣。以非功能貨幣計價的貨幣資產和負債,將以資產負債表日期的適用匯率換算為功能貨幣。由此產生的匯兌差額將記錄在未經審計的簡明綜合綜合獲利及虧損表中。

的報告貨幣 本公司為美元(「美元」),隨附的未經審核簡明合併財務報表有 以美元表示。此外,本公司亦在香港營運,並以本地貨幣保存其帳目及記錄, 港元(「HKD」)是其各自的功能貨幣,是經濟環境的主要貨幣 在其中進行他們的操作。一般而言,為合併目的,其功能性的附屬公司的資產和負債 根據 ASC 主題 830-30,貨幣不是美元兌換為美元,」財務報表翻譯」, 使用資產負債表日期的匯率。收入和支出以期間的平均匯率計算。 由外國子公司財務報表轉換而產生的收益和虧損被記錄為單獨的組成部分 在未經審核簡明合併股東赤字變動報表內累積其他綜合收益。

已根據截至2024年和2023年9月30日的匯率,將金額從港元轉換為美元:

| 2024年9月30日 | 2023年9月30日 | |||||||

| 期末港幣:美元匯率 | ||||||||

| 期間平均港元:美元 交換率 | ||||||||

綜合收益(損失)

ASC第220條“建立了有關綜合收益、其元件和累計餘額的報告和蘋果-顯示屏標準。所定義的綜合收益包括來自非業主來源的所有權益變動。在附帶的股東權益變動綜合表中呈現的累計其他綜合收益包括外匯貨幣折算未實現收益和損失的變動。該綜合收益不包括在所得稅費用或利益的計算中。綜合收益建立了有關全面收入、其元件和累計餘額的報告和顯示標準。全面收益(損失)的定義包括期間內來自非擁有者來源的所有權益變動。如附表所示的未經審核簡明綜合股東權益變動財務報表中呈報的其他累計收益,包括對外匯貨幣翻譯的未實現利得和損失變動。這種全面收益(損失)不包含在所得稅費用或利益的計算中。

| 20 |

關係人

公司遵循ASC 850-10規定。 「相關方披露」 以識別相關方並披露相關方交易,公司遵循 ASC 850-10 規定。

根據850-10-20條款,相關方包括a) 公司的聯屬公司;b) 若未選擇公平值選項下的《825-10-15條款》中的公平值選項,其股權投資將由投資實體按權益法記賬的實體;c) 員工受益的信託,如由管理層管理或受管理層託管的退休金和收益共享信託;d) 公司的主要擁有者;e) 公司管理層;f) 若一方控制或能夠對另一方的管理或營運政策產生重大影響,則公司可能與之打交道的其他方;以至於交易方之一可能被阻止充分追求其自身的獨立利益;以及g) 其他可能對交易雙方的管理或營運政策產生重大影響,或對一方擁有持股權益並可能對另一方產生重大影響,以至於其中一方或多方可能會被阻止充分追求其自身的獨立利益。

未經審核的簡明綜合基本報表應包括與相關方交易有關的披露,除了報酬安排、費用津貼和業務常規進行中的其他類似項目。但是,在編製合併或組合基本報表時消除的交易無需在這些報表中披露。這些披露應包括:a) 涉及的關係性質;b) 對於所呈現的各期收益表,包括未歸屬金額或名義金額的交易描述,以及為了理解交易對基本報表影響的其他必要信息;c) 對於所呈現的各期收益表交易的金額,以及建立條款的方法與前期不同所產生的影響;以及d) 欠相關方款項或相關方欠款項截至每份呈現資產負債表日期的金額,如果不明顯,則條款及清算方式。

合約和可能負債

公司遵循ASC 450-20,以報告處理條款。 公司基本報表對應至ASC 450-20,稽核疑問事項。 截至未經審計的簡明合併基本報表發行日期,公司可能遭受損失,但僅有未來之一或多個事件發生或未發生時才解決。公司評估此類擔保責任,而此評估本質上涉及判斷的過程。在評估與公司有擔保的待定訴訟或可能導致此類訴訟的未主張索賠相關的損失應變時,公司評估任何待有關訴訟或未主張索賠之法律程序的明確處所,以及所要求或預計在其中所要求之救濟金額的明確處。

如果對一項潛在損失的評估顯示該損失很可能已經發生,並且可以估計到責任金額,那麼該估計的責任金額將納入公司未經審核的簡明綜合基本報表中。如果評估顯示一項潛在重大損失條款並不大可能發生,但存在合理可能性;或者很可能發生但無法估算金額,則應在可能確定且重大的範圍內,披露應急責任的性質和可能損失範圍的估計。

損失條件被視為遠程的情況通常不會被揭露,除非它們涉及保證,在這種情況下,保證將被揭露。根據目前可用的信息,管理層認為這些事項不會對公司的財務狀況、經營結果或現金流量產生重大不利影響。然而,無法保證此類事項不會對公司的業務、財務狀況、經營結果或現金流量產生重大不利影響。

| 21 |

金融工具的公允價值

本公司遵循FASB會計準則編碼825-10-50-10進行有關財務工具公允價值披露,並採納FASB會計準則編碼820-10-35-37(“段落820-10-35-37”)來衡量其財務工具的公允價值。FASB會計準則編碼的820-10-35-37段落建立了一個在普遍公認會計原則(GAAP)中測量公允價值的框架,並擴大了有關公允價值衡量的披露。為提高公允價值測量及相關披露的一致性和可比性,FASB會計準則編碼820-10-35-37段落確立了一個優先考慮輸入的公平值層級,用於將用於衡量公允價值的估值技術的輸入分為三(3)個廣泛層級。公平值層級將最優先考慮在活躍市場上對相同資產或負債的報價價格(未調整), 並最低優先考慮不可觀察的輸入。由FASB會計準則編碼820-10-35-37段落定義的三(3)個公允值層級如下所述:

| 一級 | 報告日當日有活躍市場能提供相同資產或負債的報價市場價格。 | |

| 二級 | 報告日當日包含於第1層的除了活躍市場報價以外的價格輸入,這些價格輸入可以直接或間接地觀察。 | |

| 三級 | 這些價格輸入通常是可觀察到的,但未經市場數據證實。 |

財務資產被視為 Level 3,當其公平價值是使用定價模型、貼現現金流量方法或類似技術來確定,並且至少一個重要的模型假設或輸入是不可觀察的。

公允價值層次給予在活躍市場中相同資產或負債的報價價格(未調整)最高優先權,並給予不可觀察的輸入最低優先權。如果用於衡量金融資產和負債的輸入屬於上述多於一個層次,則分類是基於對工具的公允價值衡量具有重要性的最低層級輸入。

公司財務資產和負債的攜帶金額,如現金及現金等價物、應收賬款、應收款項、預付款項和其他流動資產、應付賬款、應計負債和其他應付款、應付董事、施工應付款項和應交所得稅等,因這些工具的短期到期,大致等同於其公平價值。

最近的會計宣告

不時地,由財務會計準則委員會(FASB)或其他標準設定機構頒布新的會計宣告,並在指定的生效日期採納該公司。除非另有討論,公司相信尚未生效的最新發布標準在採納後對其財務狀況或營運結果不會造成實質影響。

2016年6月,FASB發布了《會計準則更新(ASU)2016-13》, 金融工具-信貸損失(326號專題)。 新標準修訂了關於報告按攤銷成本計價的資產和可供出售債券信貸損失的指導。 2020年2月,FASB發布了ASU 2020-02, 金融工具-信貸損失(326號專題)和租賃(842號專題)—根據SEC工作人員會計公報第119號和SEC章節更新的修改

| 22 |

2023年6月,FASB發布了《會計準則更新(ASU)2022-03》。 公平值衡量(主題820):承受合約銷售限制的股票的公平值衡量。這些修訂澄清了對股票銷售上的合約限制並非被視為股票單位的一部分,因此在衡量公平值時不予考量。本指引適用於2023年10月15日後開始的公開業務實體的財政年度,包括該財政年度內的中期時段。允許提前採用。公司已評估了ASU 2023-03並在2023年第二季提前採納了指引。該採納對公司的未經審計簡明合併財務報表沒有實質影響。

在2023年3月,FASB發布了ASU No. 2023-01。 租賃(主題842)- 共同控制安排此指南修改了關於共同控制安排中租賃改善的會計處理,要求共同控制安排中的承租人按照擁有的租賃改善物的使用年限分攤,無論租約期限如何,如果承租人繼續透過租賃控制底層資產的使用。新標準將於2025財政年度生效。公司目前正在評估此標準對其未經審計的簡明綜合財務報表的影響。 財務報表和披露。

In October 2023, the FASB issued ASU 2023-06, Disclosure Improvements: Codification Amendments in Response to the SEC’s Disclosure Update and Simplification Initiative, which incorporates certain SEC disclosure requirements into the FASB Accounting Standards Codification. This update will improve disclosure and presentation requirements of a variety of topics and align the requirements in the FASB codification with the SEC’s regulations. The Company is currently evaluating the potential effect of this ASU on its unaudited condensed consolidated financial statements, but does not expect the impact to be material.

In November 2023, the FASB issued Accounting Standards Update (“ASU”) No. 2023-07, Segment Reporting (Topic 280), Improvements to Reportable Segment Disclosures. The purpose of the update was to improve financial reporting by requiring disclosures of incremental segment information on an annual and interim basis for all public entities to enable investors to develop more decision-useful financial analyses. The amendments in this ASU are effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024, with early adoption permitted and requires retrospective application to all periods presented in the unaudited condensed consolidated financial statements. Management is evaluating the impact on the Company’s unaudited condensed consolidated financial statements.

In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures (ASU 2023-09), which requires disclosure of incremental income tax information within the rate reconciliation and expanded disclosures of income taxes paid, among other disclosure requirements. ASU 2023-09 is effective for fiscal years beginning after December 15, 2024. Early adoption is permitted. The Company’s management does not believe the adoption of ASU 2023-09 will have a material impact on its unaudited condensed consolidated financial statements and disclosures.

In March 2024, the FASB issued ASU 2024-02, which removes references to the Board’s concepts statements from the FASB Accounting Standards Codification (the “Codification” or ASC). The ASU is part of the Board’s standing project to make “Codification updates for technical corrections such as conforming amendments, clarifications to guidance, simplifications to wording or the structure of guidance, and other minor improvements.” The Company’s management does not believe the adoption of ASU 2024-02 will have a material impact on its unaudited condensed consolidated financial statements and disclosures.

Except for the above-mentioned pronouncements, there are no new recently issued accounting standards that will have a material impact on the unaudited condensed consolidated balance sheets, statements of operations and cash flows.

| 23 |

4. GOING CONCERN UNCERTAINTIES

The accompanying unaudited condensed consolidated financial statements have been prepared using the going concern basis of accounting, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business.

The Company has a recurring

loss of $

These and other factors raise substantial doubt about the Company’s ability to continue as a going concern. These unaudited condensed consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets and liabilities that may result in the Company not being able to continue as a going concern.

5. REVENUE FROM CONTRACTS WITH CUSTOMERS

The table below presents our revenues by revenue source.

For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||||

| Type of revenue | Point of recognition | 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Financial consulting income | Point-in-time | $ | $ | $ | $ | |||||||||||||

| Logistic service income | Point-in-time | |||||||||||||||||

| Warehousing service income | Over time | |||||||||||||||||

| Total revenues | $ | $ | $ | $ | ||||||||||||||

6. CONSTRUCTION IN PROGRESS

The development costs of

$

This warehouse building is structurally completed in October 2024.

| 24 |

7. LEASES

The Company has entered into

commercial operating leases with various third parties for the use of leasehold land in Hong Kong. These leases have original terms ranging

from

Supplemental balance sheet information related to operating leases was as follows:

| As of | ||||||||

| September 30, 2024 | December 31, 2023 | |||||||

| Operating lease: | ||||||||

| Right-of-use asset, net | $ | $ | ||||||

| Lease liabilities: | ||||||||

| Current lease liabilities | $ | $ | ||||||

| Non-current lease liabilities | ||||||||

| Total lease liabilities | $ | $ | ||||||

Operating lease expense for the three months ended

September 30, 2024 and 2023 was $

Operating lease expense for the nine months ended

September 30, 2024 and 2023 was $

Other supplemental information about the Company’s operating lease as of:

| As of | ||||||||

| September 30, 2024 | December 31, 2023 | |||||||

| Weighted average discount rate | ||||||||

| Weighted average remaining lease term (years) | ||||||||

Operating lease commitments:

The following table summarizes the future minimum lease payments due under the Company’s operating leases in the next five years, as of September 30, 2024:

| Year ending December 31, | ||||

| 2024 (remaining three months) | $ | |||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| 2028 | ||||

| Thereafter | ||||

| Total minimum finance lease liabilities payment | ||||

| Less: imputed interest | ( | ) | ||

| Future minimum lease liabilities | $ | |||

| 25 |

8. AMOUNTS DUE TO DIRECTORS

As of September 30, 2024

and December 31, 2023, the amounts represented temporary advances made by a director, Mr. Chan to the Company for capital expenditure

and working capital purpose, which was unsecured, interest-free and repayable on demand. The balance was $

9. SHAREHOLDERS’ DEFICIT

Preferred stock

As of September 30, 2024 and December 31, 2023, the Company’s authorized shares were shares of preferred stock, with a par value of $0.0001.

As of September 30, 2024 and December 31, 2023, the Company had and shares of Series A Preferred Stock issued and outstanding, respectively.

As of September 30, 2024 and December 31, 2023, the Company had and shares of Series B Preferred Stock issued and outstanding, respectively.

As of September 30, 2024 and December 31, 2023, the Company had and share of Series C Preferred Stock issued and outstanding, respectively.

Common stock

As of September 30, 2024 and December 31, 2023, the Company’s authorized shares were shares of common stock, with a par value of $.

On March 11, 2024, the Company filed its Restated Articles of Incorporation with the Nevada Secretary of State (the “Articles of Incorporation”) to effect a 1-for-3000 reverse stock split of its issued and outstanding Common Stock (the “Reverse Stock Split”) which was approved by the Company’s stockholders at a special meeting in lieu of annual meeting held on February 29, 2023, and issue to all shareholders that directly as a result of the Reverse Stock Split would hold less than 100 shares of common stock of the Company (each, an “Affected Shareholder”) such number of additional shares of common stock so that each Affected Shareholder shall hold 100 shares of common stock of the Company after the Reverse Stock Split. On May 8, 2024, the Reverse Stock Split became effective upon the approval from FINRA. Accordingly, all common shares and per share amounts in these accompanying unaudited condensed consolidated financial statements have been adjusted retroactively to reflect the reverse stock split as if the split occurred at the beginning of the earliest period presented.

On August 15, 2024, the Company and United Warehouse Management Corp., a British Virgin Island corporation (“UWMC”) and eleven shareholders of UWMC entered into a Share Exchange Agreement (the “SEA”) pursuant to which the shareholders of UWMC agreed to transfer to the Company shares of UWMC, constituting all of the issued and outstanding securities of UWMC, in exchange for shares of common stock of the Company, par value $ per share.

As of September 30, 2024 and December 31, 2023, the Company had and shares of common stock issued and outstanding, respectively.

| 26 |

The calculation of the basic and diluted net (loss) income per share attributable to common stockholders of the Company is based on the following data (in dollars, except share data):

For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Net (loss) income attributable to common stockholders | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| Weighted average common shares outstanding: | ||||||||||||||||

| Basic | ||||||||||||||||

| Diluted | ||||||||||||||||

| Net loss per share: | ||||||||||||||||

| Basic # | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| Diluted # | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| # | For net loss per share during the three and nine months ended September 30, 2024, common stock equivalents were included in the computation of diluted net income (loss) per share since such inclusion would have been anti-dilutive. For net income per share during the three and nine months ended September 30, 2023, basic and diluted net income per share was less than $0.01. |

The shares amounts are presented on a retroactive basis, after the effect of Reverse Stock Split (see Note 9).

11. INCOME TAX

For the nine months ended September 30, 2024 and 2023, the local (“United States of America”) and foreign tax regime incurred loss before income taxes, which comprised of the following:

| For the Nine Months Ended September 30, | ||||||||

| 2024 | 2023 | |||||||

| Tax jurisdiction from: | ||||||||

| - Local | $ | ( | ) | $ | ||||

| - Foreign, including | ||||||||

| British Virgin Islands | ( | ) | ||||||

| Hong Kong | ||||||||

| (Loss) income before income taxes | $ | ( | ) | $ | ||||

| 27 |

The provision for income taxes consisted of the following:

| For the Nine Months Ended September 30, | ||||||||

| 2024 | 2023 | |||||||

| Current: | ||||||||

| - Local | $ | $ | ||||||

| - Foreign | ||||||||

| Deferred: | ||||||||

| - Local | ||||||||

| - Foreign | ||||||||

| Income tax expense | $ | $ | ||||||

The effective tax rate in the periods presented is the result of the mix of income earned in various tax jurisdictions that apply a broad range of income tax rate. The Company has operations in Hong Kong that are subject to taxes in the jurisdictions in which they operate, as follows:

United States of America

MVNC is registered in the State of Nevada and is subject to the tax laws of United States of America. The U.S. Tax Cuts and Jobs Act (the “Tax Reform Act”) was signed into law. The Tax Reform Act significantly revised the U.S. corporate income tax regime by, among other things, lowering the U.S. corporate tax rate from 35% to 21% effective January 1, 2018. The Company’s policy is to recognize accrued interest and penalties related to unrecognized tax benefits in its income tax provision. The Company has not accrued or paid interest or penalties which were not material to its results of operations for the periods presented. Deferred tax asset is not provided for as the tax losses may not be able to carry forward after a change in substantial ownership of the Company.

For the three and nine months ended September 30, 2024 and 2023, there were no operating incomes.

BVI

Under the current BVI law, the Company is not subject to tax on income.

| 28 |

Hong Kong

The Company and subsidiaries operating in Hong Kong is subject to the Hong Kong Profits Tax at the two-tiered profits tax rates from 8.25% to 16.5% on the estimated assessable profits arising in Hong Kong during the current year, after deducting a tax concession for the tax year. The reconciliation of income tax expense to income at applicable tax rates for the nine months ended September 30, 2024 and 2023 is as follows:

| For the Nine Months Ended September 30, | ||||||||

| 2024 | 2023 | |||||||

| Income before income taxes | $ | $ | ||||||

| Statutory income tax rate | $ | |||||||

| Income tax expense at statutory rate | ||||||||

| Tax effect of non-taxable items | ( | ) | ( | ) | ||||

| Tax effect of non-deductible items | ||||||||

| Income tax expense | $ | $ | ||||||

The following table sets forth the significant components of the deferred tax assets of the Company as of September 30, 2024 and December 31, 2023:

| As of | ||||||||

| September 30, 2024 | December 31, 2023 | |||||||

| Deferred tax assets: | ||||||||

| NOL – US tax regime | $ | $ | ||||||

| NOL – British Virgin Islands regime | ||||||||

| NOL – Hong Kong tax regime | ||||||||

| Less: valuation allowance | ( | ) | ( | ) | ||||

| Deferred tax assets, net | $ | $ | ||||||

As of September 30, 2024 and December 31, 2023, the Company had no unrecognized tax benefits. Interest and penalty charges, if any, related to income taxes would be classified as a component of the provision for income taxes in the consolidated statements of operations. The Company does not expect any significant change in its uncertain tax positions in the next twelve months.

The Company filed income tax returns in the United States federal tax jurisdiction and several state tax jurisdictions. Since the Company is in a loss carryforward position, it is generally subject to examination by federal and state tax authorities for all tax years in which a loss carryforward is available.

| 29 |

12. RELATED PARTY TRANSACTIONS

From time to time, the directors of the Company advanced funds to the Company for capital expenditures and working capital purpose. Those temporary advances are unsecured, non-interest bearing and have no fixed terms of repayment.

Apart from the transactions and balances detailed elsewhere in these accompanying unaudited condensed consolidated financial statements, the Company has no other significant or material related party transactions during the periods presented.

13. CONCENTRATIONS OF RISK

The Company is exposed to the following concentrations of risk:

| (a) | Major customers |

For the nine months ended September 30, 2024 and 2023, the individual customers who accounted for 10% or more of the Company’s revenues and its outstanding receivable balances at period-end dates, are presented as follows:

| Nine months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Customer A | $ | $ | ||||||||||

| Customer B | $ | $ | ||||||||||

| Nine months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Customer C | $ | $ | ||||||||||

| Customer D | $ | $ | ||||||||||

| Customer E | $ | $ | ||||||||||

For the three months ended September 30, 2024 and 2023, the individual customers who accounted for 10% or more of the Company’s revenues and its outstanding receivable balances at period-end dates, are presented as follows:

| Three months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Customer A | $ | $ | ||||||||||

| Customer B | $ | $ | ||||||||||

| Three months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Customer B | $ | $ | ||||||||||

| Customer C | $ | $ | ||||||||||

| Customer D | $ | $ | ||||||||||

| Customer F | $ | $ | ||||||||||

| 30 |

These customers are located in Hong Kong.

| (b) | Major vendors |

For the nine months ended September 30, 2024 and 2023, the individual vendors who accounted for 10% or more of the Company’s direct operating cost and its outstanding payable balances at period-end dates, are presented as follows:

| Nine months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| Vendor D | $ | $ | ||||||||||

| Vendor E | $ | $ | ||||||||||

| Nine months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| Vendor A | $ | $ | ||||||||||

| Vendor B | $ | $ | ||||||||||

| Vendor C | $ | $ | ||||||||||

For the three months ended September 30, 2024 and 2023, the individual vendors who accounted for 10% or more of the Company’s direct operating cost and its outstanding payable balances at period-end dates, are presented as follows:

| Three months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| Vendor F | $ | $ | ||||||||||

| Vendor D | $ | $ | ||||||||||

| Vendor E | $ | $ | ||||||||||

| Three months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| Vendor E | $ | $ | ||||||||||

| Vendor A | $ | $ | ||||||||||

| Vendor C | $ | $ | ||||||||||

| 31 |

These vendors are located in Hong Kong and China.

| (c) | Credit risk |

Financial instruments that

potentially subject the Company to credit risk consist of cash and cash equivalents and accounts receivable. Cash equivalents are maintained

with high credit quality institutions in Hong Kong, the composition and maturities of which are regularly monitored by the management.

| (d) | Economic and political risk |

The Company’s major operations are conducted in Hong Kong. Accordingly, the political, economic, and legal environments in Hong Kong, as well as the general state of Hong Kong’s economy may influence the Company’s business, financial condition, and results of operations.

| (e) | Exchange rate risk |

The Company cannot guarantee that the current exchange rate will remain steady; therefore there is a possibility that the Company could post the same amount of profit for two comparable periods and because of the fluctuating exchange rate actually post higher or lower profit depending on exchange rate of HKD converted to US$ on that date. The exchange rate could fluctuate depending on changes in political and economic environments without notice.

| (f) | Liquidity risk |

Liquidity risk is the risk that the Company will not be able to meet its financial obligations as they become due. The Company’s policy is to ensure that it has sufficient cash to meet its liabilities when they become due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Company’s reputation. A key risk in managing liquidity is the degree of uncertainty in the cash flow projections. If future cash flows are fairly uncertain, the liquidity risk increases.

14. COMMITMENTS AND CONTINGENCIES

Commitments

As of September 30, 2024, the Company had no material commitments or contingencies.

15. SUBSEQUENT EVENTS

根據ASC主題855,“”,該主題為在未經稽核的簡明綜合財務報表發布之前發生的事件或交易設立了會計和披露的一般準則,公司已評估所有在2024年9月30日之後至公司發布未經稽核的簡明綜合財務報表之日發生的事件或交易。公司自2024年9月30日以來沒有重大明顯的隨後事件。隨後的事件公司根據ASC主題855,“”,該主題為在未經稽核的簡明綜合財務報表發布之前發生的事件或交易設立了會計和披露的一般準則,已評估自2024年9月30日之後至公司發布未經稽核的簡明綜合財務報表之日發生的所有事件或交易。自2024年9月30日以來,公司並無重大可認知的隨後事件。

| 32 |

第二項。管理層討論和分析財務狀況和營運結果。

本公司的財務狀況和營運結果的以下討論和分析,應與我們未經審核的簡明合併財務報表和報告其他地方包含的相關附註一起閱讀。本討論包含涉及風險和不確定性的前瞻性陳述。由於各種因素的影響,實際結果和選定事件的時間可能與這些前瞻性陳述中預期的有重大不同。請參見"有關前瞻性陳述之注意事項" 第9頁上。

除非另有說明,所有貨幣數字引用的“美元”,“美元”或“$”均指美國的法定貨幣。在本報告中,公司子公司的資產和負債使用資產負債表日的匯率轉換成美元。收入和費用則以期間內盛行的平均匯率進行轉換。由外國子公司財務報表轉換所產生的利益和損失,記錄為未經審計的綜合損益表中股東權益變動的另一項組成部分。

除非另有說明,在本10-Q表格的季度報告中,我們稱Marvion Inc.及其合併子公司為“MVNC”,“我們”,“我們”和“我們”。

本報告中的數字信息以實際金額為基礎呈現,均已取整。由於四捨五入,合計和百分比計算可能存在小差異。

業務描述

Marvion Inc.於2008年3月6日在內華達州成立。本公司及其附屬公司以下簡稱為(“公司”)。

2024年8月15日,該公司及英屬維爾京群島的United Warehouse Management公司(UWMC)和UWMC的十一名股東簽署了股份交換協議(SEA),根據該協議,UWMC的股東同意將UWMC的4,000股股份轉讓給該公司,佔UWMC已發行和流通證券的全部,以換取公司每股面值$0.0001的常股148,148,150股(股份交換交易)。

In addition to the Acquisition Shares, the Company agreed to make earnout payments in the aggregate amount of $5.5 million (collectively, the “Earn Out Payments”) upon UWMC’s achievement of certain net income performance milestones during each six month period ending June 30 and December 31 (each, a “Performance Period”) for a total of nine Performance Periods. The Earn Out Payments will be payable in the form of interest free promissory notes and shared equally among Chan Sze Yu, Fong Hiu Ching and Young Chi Kin Eric who are also shareholders of UWMC. The Acquisition transactions contemplated by the SEA were consummated on September 12, 2024.

As a result of the Acquisition, Marvion became engaged in the business of logistics and warehousing services. Concurrently with the acquisition of UWMC, the Company also divested its ownership of Marvion Holdings Limited and all of its subsidiaries and ceased its the lifestyle, media and entertainment creation and distribution, and technology businesses.

Chan Sze Yu is our Chief Executive Officer, Chief Financial Officer, Secretary and Director. Young Chi Kin Eric holds 10,000,000 shares of the Company’s Series A Preferred Stock which entitles him to vote on all matters submitted to a vote of the shareholders together with the Common Stock holders with each one share of Series A Preferred Stock having 200 votes.

The foregoing descriptions of the SEA and the Promissory Notes are qualified in their entirety by reference to the SEA and the Promissory Notes, which are filed as Exhibits 10.1 through and including 10.4 and incorporated herein by reference.

| 33 |

The share exchange transaction has been accounted for as a reverse merger and recapitalization of the Company, whereby UWMC is deemed to be the accounting acquirer (legal acquiree) and the Company to be the accounting acquiree (legal acquirer). Accordingly, the consolidated assets, liabilities and results of operations of the Company will become the historical financial statements of UWMC, and the Company’s assets, liabilities and results of operations will be consolidated with UWMC beginning on the date of the share exchange transaction. No goodwill is recognized in this transaction. The historical financial statements prior to the share exchange transaction are those of the accounting acquirer (UWMC). Historical stockholders’ equity of the accounting acquirer prior to the reverse merger are retroactively restated (a recapitalization) for the equivalent number of shares received in the merger. Operations prior to the merger are those of the acquirer. After completion of the share exchange transaction, the Company’s accompanying unaudited condensed consolidated financial statements have been restated for all periods presented accordingly.

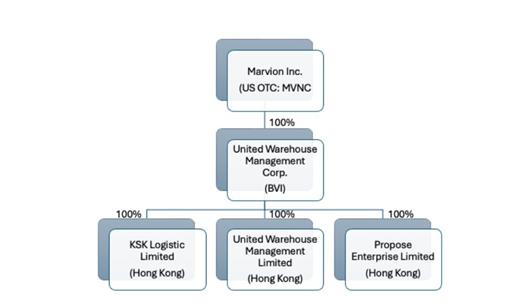

The Company, through its subsidiary UWMC, is principally engaged in the logistic services, warehousing service and financial consulting services in Hong Kong. UWMC’s businesses are operated through three subsidiaries organized in Hong Kong: KSK Logistic Limited (“KSK”), United Warehouse Management Limited (“UWML”) and Propose Enterprise Limited (“PEL”), which provide the following services:

| · | KSK: Last mile deliveries for retail and business customers; | |

| · | UWML: Provides warehousing and distribution services; and | |

| · | PEL: Provides business advisory solutions to customers which may provide a lead to our logistic and warehousing services. |

We are seeking to build our own furniture online store, providing a one-stop shopping experience to the Hong Kong furniture buyers. We may partner with some of our existing customers who are already in furniture retailing, since they already have connections with many of the furniture manufacturers in China. By listing out the catalogs of the partnered manufacturers, a lot more options will be available to the consumers to choose from. Once orders are made, our logistics arm KSK will be able to handle the delivery of the furniture to the door of the consumers. We will then build up our skillful furniture assemble team who will complete the assembly of the furniture at the time of delivery. In the long run, as we see a good local demand on certain furniture products, we can work with the manufacturers to stock up some products at our own UWML warehouses, this will further shorten the time between consumer placing the order online and the time when the furniture is delivered and assembled at their home.

Our corporate structure is described below:

| 34 |

We are authorized to issue up to 270,000,000,000 shares of our common stock, par value $0.0001. Our Board has also designated the following classes of preferred stock: (i) the Series A Preferred Stock,” par value $0.0001, with 10,000,000 authorized shares, all of which are issued and outstanding; (ii) “Series B Preferred Stock,” par value $0.0001, with 1,000,000 authorized shares, 366,346 of which are issued and outstanding; and (iii) the “Series C Convertible Preferred Stock,” par value $0.001, with 1 authorized share, all of which are issued and outstanding. The voting and conversion rights of each series of preferred stock and the beneficial ownership of such securities by insiders are summarized below:

| Stock | Voting Rights | Ownership |

| Common Stock | One vote per share |

7.16% held by Lee Ying Chiu Herbert. 8.78% held by Young Chi Kin Eric. 8.78% held by Chan Sze Yu. |

| Series A Preferred Stock | Holders of Series A Preferred Stock are entitled to vote on matters submitted to a vote of the shareholders with each one share having 200 votes. Series A Preferred Stock do not convert into Common Stock. | 100% held by Young Chi Kin Eric. |

| Series B Preferred Stock | Holders of Series B Preferred Stock have no voting rights, and Series B Preferred Stock do not convert into Common Stock. | Approximately 92% held by Lee Ying Chiu Herbert. |

| Series C Convertible Preferred Stock |

Holders of Series C Convertible Preferred Stock are generally not allowed to vote on an “as converted” basis on matters submitted to holders of the common stock, or any class thereof.

Each one share of Series C Convertible Preferred Stock converts into 9.99% of the outstanding shares of common stock less the number of shares of common stock held by the holder; provided that any such optional conversion must involve the conversion of all of the holder’s shares of Series C Convertible Preferred Stock. |

100% held by Lee Ying Chiu Herbert. |

Current Revenue Generating Operation

BUSINESS SEGMENT INFORMATION

The following table summarizes revenue from contracts with customers, disaggregated by revenue source and the related segments, for the nine months ended September 30, 2024 and 2023:

| Nine Months ended September 30, | ||||||||

| Types of segments/revenue sources | 2024 | 2023 | ||||||

| Supply chain segment: | ||||||||

| Logistic services | $ | 468,142 | $ | 34,541 | ||||

| Warehousing services | 403,229 | – | ||||||

| 871,371 | 34,541 | |||||||

| Financial segment: | ||||||||

| Financial consulting services | 148,222 | 372,066 | ||||||

| $ | 1,019,593 | $ | 406,607 | |||||

| 35 |

Revenue Generating Operation in the Near Future (Next 12 Months).

Over the next 12 months, we intend to continue to expand our logistics and warehousing businesses through more Business to Business (B2B) opportunities. We seek to provide business customers with a one-stop solution for their warehousing and distribution needs. While our current customers include key furniture retailers, we hope to expand our customer base both vertically and horizontally to other industries. We are in discussions with major cross-regional logistics companies to fill in their local distribution needs and potential clients who may need a additional warehousing space. We began construction of our third warehouse in Yuen Long, Hong Kong, and expect to finish sometime in the first quarter of 2025.

On October 2, 2024, our subsidiary United Warehouse Limited signed a Service Agreement with Starwarehouse Engineering Limited to install solar PV systems on the rooftops of our warehouses (the “Service Agreement”). The generated power will be sold to China Light and Power (CLP) at the defined tariff scheme rate, creating an additional long term stable revenue stream to the group, at the same time reducing our carbon footprint in the society. The partnership is expected to begin in early 2025 and continue until December 31, 2033. The foregoing description of the Service Agreement is qualified in its entirety by reference to the English translation of the Service Agreement, which is filed as Exhibit 10.10 and incorporated herein by reference.

Revenue Generating Operation in the Farther Future (Beyond the Next 12 Months)

In the future, we are looking into expanding more into the Business to Consumer (B2C) business opportunities.

Based on the market expertise of our management team in the furniture industry, and the cross-border ecommerce growth from China to Hong Kong, we are seeking to develop a furniture online ecommerce platform which can provide a one-stop furniture shopping experience for consumers. According to Statista, Hong Kong consumers prefer online shopping and the percentage of consumers choosing to shop online will reach 84.1% by 2027. China has a mature online furniture ecommerce market, with 50% of consumers in China already purchasing their furniture online. We plan to provide a rich selection of furniture from the already mature China ecommerce market to the consumers in Hong Kong, with integrated logistics, delivery and furniture assembly services with a simple press of a button on our future furniture ecommerce platform.

We are also looking into developing a one-stop ecommerce platform for Hong Kong consumers, providing them with niche products from big brands around the world that are not being offered locally in Hong Kong. By building up and utilizing logistic and warehousing partners in different countries, we seek to provide group shipping across different regions to Hong Kong to deliver products to Hong Kong using the most cost effective channels.

| 36 |

Results of Operations.

Three Months Ended September 30, 2024, as compared to Three Months Ended September 30, 2023

The following table sets forth selected financial information from our statements of comprehensive income for the three months ended September 30, 2024 and 2023:

| Three Months Ended September 30, | ||||||||

| 2024 | 2023 | |||||||

| Revenues | $ | 390,275 | $ | 212,502 | ||||

| Cost of revenues | (193,891 | ) | (88,893 | ) | ||||

| Gross profit | 196,384 | 123,609 | ||||||

| Operating expenses: | ||||||||

| General and administrative expenses | (573,438 | ) | (53,737 | ) | ||||

| Total operating expenses | (573,438 | ) | (53,737 | ) | ||||

| (Loss) income from operations | (377,054 | ) | 65,872 | |||||

| Other income | 612 | 108 | ||||||

| (Loss) income before income taxes | (376,442 | ) | 65,980 | |||||

| Income tax expense | (2,531 | ) | (19,887 | ) | ||||

| Net (loss) income | $ | (378,973 | ) | $ | 46,093 | |||

Revenues

The Company currently earns three types of income sources:

| Three Months Ended September 30, | ||||||||

| 2024 | 2023 | |||||||

| Logistic service income | $ | 204,333 | $ | 34,541 | ||||

| Warehousing service income | 134,638 | – | ||||||

| Financial consulting income | 51,204 | 177,961 | ||||||

| $ | 390,275 | $ | 212,502 | |||||

Revenues from logistic solution services to the customers, in which such local transportation, delivery and packaging services are recognized at the time the merchandise is packed and shipped by the Company to domestic destinations designed by the customers. Generally, the Company bills the invoices monthly and collects the receivable in a credit term of 30 days.

| 37 |

Revenues generating from storage services are recognized ratably over the term of the contract or arrangement, as the Company performs contractual obligations through continuous transfer of control to the customers, and they could simultaneously receive and consume the benefits of the Company’s performance as it occurs. The Company generally invoices customers monthly at the end of each month in arrear for services performed during the month. The performance obligation is satisfied when the services are performed. Warehousing contracts typically consist of ongoing storage service in a term of 1-6 years, subject to renewal option.

The Company also provides financial consulting services to the customers, and generally invoices customers when the performance obligation is satisfied. The duration of the service period is short, usually within 3 months. Transaction prices of financial consulting services to be rendered are typically based on contracted rates. The Company earns the fee arising from the facilitation of the placement of financing solutions among different credit institutions, which is recognized at a point in time when the service is completed and delivered to the customer.

Revenues of $390,275 for the three months ended September 30, 2024, increased by $177,773 or 83.66% from $212,502 in the same period of 2023, which was mainly due to introduction of new business in rendering logistics and warehousing services. Revenues of $212,502 for the three months ended September 30, 2023 consisted primarily financial consulting service.

For the three months ended September 30, 2024 and 2023, the individual customers who accounted for 10% or more of the Company’s revenues and its outstanding receivable balances at period-end dates, are presented as follows:

| Three months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Pro King International Warehouse Limited | $ | 134,638 | 34.50% | $ | 45,045 | |||||||

| Furniture Station Limited | $ | 138,982 | 35.61% | $ | 91,501 | |||||||

| Three months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Furniture Station Limited | $ | 31,069 | 14.62% | $ | 31,074 | |||||||

| Time Credit Limited | $ | 38,465 | 18.10% | $ | 4,991 | |||||||

| Easy Funding Limited | $ | 78,620 | 37.00% | $ | 32,529 | |||||||

| Golden Fields Finance Limited | $ | 27,444 | 12.91% | $ | 7,532 | |||||||

These customers are located in Hong Kong.

Cost of Revenues

Cost of revenues of $193,891 for the three months ended September 30, 2024 consisted primarily of the direct wages, telemarketing service charges, depreciation and amortization of right-of-use assets. Cost of revenues increased by $104,998 from $88,893 in the same period of 2023 which was mainly due to the increase in direct operating cost in connection with logistics and warehousing services. Cost of revenues of $88,893 for the three months ended September 30, 2023 consisted primarily of the associated costs in rendering the financial consulting service and depreciation and amortization of right-of-use assets.

| 38 |

For the three months ended September 30, 2024 and 2023, the individual vendors who accounted for 10% or more of the Company’s direct operating cost and its outstanding payable balances at period-end dates, are presented as follows:

| Three months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| Ten Month Limited | $ | 25,922 | 13.37% | $ | – | |||||||

| Ip Ming | $ | 22,667 | 11.69% | $ | – | |||||||

| Giant Winner Limited | $ | 44,726 | 23.07% | $ | – | |||||||

| Three months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| Giant Winner Limited | $ | 25,840 | 29.07% | $ | – | |||||||

| 廣州萬基斯投資顧問有限公司 (Guangzhou MKS Investment Consulting Co., Limited*) | $ | 17,251 | 19.41% | $ | – | |||||||

| Wong Ka Che | $ | 10,228 | 11.51% | $ | – | |||||||

* for identification purpose only

These vendors are located in Hong Kong and China.

Gross Profit

We achieved a gross profit of $196,384 and $123,609 for the three months ended September 30, 2024 and 2023, respectively. The increase in gross profit is attributable to an increase in new business in rendering logistics and warehousing services.

Operating Expenses:

General and Administrative Expenses (“G&A”): General and administrative expenses of $573,438 and $57,737 for the three months ended September 30, 2024, and 2023, respectively. These expenses primarily include payroll, office operating cost, as well as professional fees.

| 39 |

Nine Months Ended September 30, 2024 compared to Nine Months Ended September 30, 2023

The following table sets forth selected financial information from our statements of comprehensive income for the nine months ended September 30, 2024 and 2023:

| Nine Months Ended September 30, | ||||||||

| 2024 | 2023 | |||||||

| Revenues | $ | 1,019,593 | $ | 406,607 | ||||

| Cost of revenues | (517,252 | ) | (181,675 | ) | ||||

| Gross profit | 502,341 | 224,932 | ||||||

| Operating expenses: | ||||||||

| General and administrative expenses | (732,377 | ) | (144,610 | ) | ||||

| Total operating expenses | (732,377 | ) | (144,610 | ) | ||||

| (Loss) income from operations | (230,036 | ) | 80,322 | |||||

| Other income | 1,597 | 420 | ||||||

| (Loss) income before income taxes | (228,439 | ) | 80,742 | |||||

| Income tax expense | (36,045 | ) | (19,887 | ) | ||||

| Net (loss) income | $ | (264,484 | ) | $ | 60,855 | |||

Revenues

The Company currently earns three types of income sources:

| Nine Months Ended September 30, | ||||||||

| 2024 | 2023 | |||||||

| Logistic service income | $ | 468,142 | $ | 34,541 | ||||

| Warehousing service income | 403,229 | – | ||||||

| Financial consulting income | 148,222 | 372,066 | ||||||

| $ | 1,019,593 | $ | 406,607 | |||||

Revenues from logistic solution services to the customers, in which such local transportation, delivery and packaging services are recognized at the time the merchandise is packed and shipped by the Company to domestic destinations designed by the customers. Generally, the Company bills the invoices monthly and collects the receivable in a credit term of 30 days.

Revenues generating from storage services are recognized ratably over the term of the contract or arrangement, as the Company performs contractual obligations through continuous transfer of control to the customers, and they could simultaneously receive and consume the benefits of the Company’s performance as it occurs. The Company generally invoices customers monthly at the end of each month in arrear for services performed during the month. The performance obligation is satisfied when the services are performed. Warehousing contracts typically consist of ongoing storage service in a term of 1-6 years, subject to renewal option.

| 40 |

The Company also provides financial consulting services to the customers, and generally invoices customers when the performance obligation is satisfied. The duration of the service period is short, usually within 3 months. Transaction prices of financial consulting services to be rendered are typically based on contracted rates. The Company earns the fee arising from the facilitation of the placement of financing solutions among different credit institutions, which is recognized at a point in time when the service is completed and delivered to the customer.

Revenues of $1,019,593 for the nine months ended September 30, 2024, increased by $612,986 or 151% from $406,607 in the same period of 2023, which was mainly due to introduction of new business in rendering logistics and warehousing services. Revenues of $406,607 for the nine months ended September 30, 2023 consisted primarily financial consulting service.

For the nine months ended September 30, 2024 and 2023, the individual customers who accounted for 10% or more of the Company’s revenues and its outstanding receivable balances at period-end dates, are presented as follows:

| Nine months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Pro King International Warehouse Limited | $ | 403,229 | 39.55% | $ | 45,045 | |||||||

| Furniture Station Limited | $ | 348,898 | 34.22% | $ | 91,501 | |||||||

| Nine months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | |||||||||

| Time Credit Limited | $ | 101,935 | 25.07% | $ | 4,991 | |||||||

| Easy Funding Limited | $ | 172,911 | 42.53% | $ | 32,529 | |||||||

| Wings Finance Limited | $ | 46,898 | 11.53% | $ | 3,192 | |||||||

These customers are located in Hong Kong.

Cost of Revenues

Cost of revenues of $517,252 for the nine months ended September 30, 2024 consisted primarily of the direct wages, telemarketing service charges, depreciation and amortization of right of use assets. Cost of revenues increased by $335,577 from $181,675 in the same period of 2023 which was mainly due to the increase in direct operating cost in connection with logistics and warehousing services. Cost of revenues of $181,675 for the nine months ended September 30, 2023 consisted primarily of the associated costs in rendering the financial consulting service, such as, direct marketing costs.

| 41 |

For the nine months ended September 30, 2024 and 2023, the individual vendors who accounted for 10% or more of the Company’s direct operating cost and its outstanding payable balances at period-end dates, are presented as follows:

| Nine months ended September 30, 2024 | September 30, 2024 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| Ip Ming | $ | 57,909 | 11.20% | $ | – | |||||||

| Giant Winner Limited | $ | 134,793 | 26.06% | $ | – | |||||||

| Nine months ended September 30, 2023 | September 30, 2023 | |||||||||||

| Vendor | Cost of revenues | Percentage cost of revenues | Accounts payable | |||||||||

| 廣州萬基斯投資顧問有限公司 (Guangzhou MKS Investment Consulting Co., Limited*) | $ | 50,528 | 27.81% | $ | – | |||||||

| Wong Ka Che | $ | 38,933 | 21.43% | $ | – | |||||||

| My Sweetheart Company Limited | $ | 27,242 | 14.99% | $ | 27,245 | |||||||

* for identification purpose only

These vendors are located in Hong Kong and China.

Gross Profit

We achieved a gross profit of $502,341 and $224,932 for the nine months ended September 30, 2024 and 2023, respectively. The increase in gross profit is attributable to an increase in new business in rendering logistics and warehousing services.

Operating Expenses:

General and administrative expenses of $732,377 for the nine months ended September 30, 2024, increased by $587,767 or 406% from $144,610 in the same period of 2023, due to increase in consultancy fees and legal and professional fee related to the reverse merger transaction for the nine months ended September 30, 2024.

General and administrative expenses of $144,610 for the nine months ended September 30, 2023. These expenses primarily include payroll, office operating cost, as well as professional fees.

Income Tax Expense

We incurred income tax expense of $36,045 and $19,887 under Hong Kong tax regime during the nine months ended September 30, 2024 and 2023, respectively.

| 42 |

Liquidity and Capital Resources

Working Capital

As of September 30, 2024, we had cash and cash equivalents of $159,992, account receivables of $210,761 and prepaid expenses and other current assets of $17,125.

As of December 31, 2023, we had cash and cash equivalents of $120,319, accounts receivable of $74,263 and prepaid expenses and other current assets of $1,537.

As of September 30, 2024 and December 31, 2023, we had working capital deficit of $8,235,536 and $1,748,299, respectively.

Going Concern

Our continuation as a going concern is dependent upon improving our profitability and the continuing financial support from our stockholders. Our sources of capital may include the sale of equity securities, which include common stock sold in private transactions, capital leases and short-term and long-term debts. While we believe that we will obtain external financing and the existing shareholders will continue to provide the additional cash to meet our obligations as they become due, there can be no assurance that we will be able to raise such additional capital resources on satisfactory terms. We believe that our current cash and other sources of liquidity discussed below are adequate to support operations for at least the next 12 months.

We require additional funding to meet its ongoing obligations and to fund anticipated operating losses. Our auditor has expressed substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern is dependent on raising capital to fund its initial business plan and ultimately to attain profitable operations. These unaudited condensed consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets and liabilities that may result in the Company not being able to continue as a going concern.