Angel Oak Mortgage房地產業信託公司(連同其附屬公司“公司”、“我們”或“我們的”)是一家專注於在美國房屋貸款市場中收購和投資首位貸款非合格居住房屋抵押貸款(“non-QM”)和其他與抵押貸款相關資產的房地產金融公司。公司的策略是主要在新發放的首位非合格居住房屋抵押貸款中進行具信用敏感性的投資,這些貸款主要提供給高品質的非合格居住房屋抵押貸款借款人,並主要來自其聯屬公司Angel Oak Mortgage Solutions LLC的專有抵押貸款平台(連同其他非營運的附屬原始債權人“Angel Oak Mortgage Lending”),該平台目前主要透過批發管道運作,並擁有全國性的發放範圍。該公司還可能投資其他居住抵押貸款、居住抵押支持證券(“RMBS”)和其他與抵押貸款相關資產。公司的目標是為股東獲取具吸引力的風險調整回報,透過現金分配和資本升值,跨越利率和信貸周期。

本公司是一家馬里蘭州的公司,成立於2018年3月20日。該公司通過將其部分資產投資於其全資擁有的應課稅REIT附屬公司Angel Oak Mortgage REIT TRS,於2018年3月21日成立,實現其某些投資目標;該附屬公司投資其資產於Angel Oak Mortgage基金TRS,於2018年6月15日成立的一家特許信託。

公司由Falcons I, LLC(以下簡稱“管理者”)外部管理和顧問,管理者是一家獲證券交易委員會註冊的投資顧問,為Angel Oak Capital Advisors, LLC(以下簡稱“Angel Oak Capital”)的聯屬公司。公司已選擇按照1986年修訂的《內部稅收法典》(以下簡稱“法典”)選擇以股權房地產投資信托(以下簡稱“REIT”)的身份為其於2019年12月31日結束的課稅年度納稅。

在正常的業務過程中,公司會進行衍生金融工具的交易,以管理其對市場風險的曝險,包括對於整筆貸款投資的利率風險和提前還款風險。公司投資的衍生工具以及經濟避險所旨在減輕的市場風險在下文中將進一步討論。截至2024年9月30日和2023年12月31日的衍生工具包括待公告(“TBA”)證券和利率期貨合約。與利率期貨的保證金抵押有關的受限制現金,截至2024年9月30日和2023年12月31日均包含$2.3百萬和$2.5百萬美元,分別為。 no 截至2024年9月30日或2023年12月31日,所需的TBA保證金抵押為。對於截至2024年9月30日的三個月和九個月,我們確認了與我們的TBA收入相關的所得稅費用及相應的負債。

截至2024年9月30日,我們的估值政策和程序與年結日為2023年12月31日的基本報表所述的相同,該報表包含在10-K表格中的年度報告中。附註10中包含了其他金融工具的詳細描述 Fair Value Measurements 在截至2023年12月31日的年度基本報表中包括在10-K表格中的【其他】金融工具以公平價值計量及其重要輸入項,以及根據1級、2級和3級估值層次分類這些工具的一般描述。

管理層對財務狀況和運營結果的討論與分析旨在幫助讀者理解Angel Oak Mortgage REIt, Inc.的運營結果和財務狀況。以下內容應與未經審計的簡明合併基本報表及其附註一起閱讀。文中提到的我們「公司」、「我們」、「我們」、「我們的」是指Angel Oak Mortgage REIt, Inc.及其子公司,包括Angel Oak Mortgage Operating Partnership, LP(「運營合夥企業」),通過該合夥企業我們持有幾乎所有資產並進行運營。除非另有說明,術語「Angel Oak」統稱爲Angel Oak Capital Advisors, LLC(「Angel Oak Capital」)及其附屬機構,包括我們的外部管理人Falcons I, LLC(「我們的管理人」)、Angel Oak Companies, LP(「Angel Oak Companies」)以及附屬機構Angel Oak Mortgage Solutions LLC的專有抵押貸款平台(連同其他非運營附屬起源者,「Angel Oak Mortgage Lending」)。

Angel Oak Mortgage REIt, Inc. 是一家房地產金融公司,專注於收購和投資美國抵押市場中的第一留置權非合格抵押貸款和其他抵押相關資產。我們的策略是主要在新發放的第一留置權非合格抵押貸款中進行信用敏感投資,這些貸款主要面向高質量的非合格貸款借款人,主要通過Angel Oak的專有抵押貸款平台——Angel Oak Mortgage Lending獲得,該平台目前主要通過批發渠道運營,並具有全國性的發放能力。我們還可以投資其他住宅抵押貸款、住宅抵押貸款支持證券(「RMBS」)和其他抵押相關資產,這些資產與非合格貸款一起構成我們的目標資產。此外,當市場條件和資產價格適合進行有吸引力的購買時,我們也可能通過二級市場識別並收購我們的目標資產。我們的目標是通過現金分配和資本增值,在利率和信用週期中爲我們的股東產生有吸引力的風險調整回報。

我們由外部管理和提供建議的經理Falcons I, LLC管理,該公司是1940年投資顧問法案下注冊的投資顧問,並且是Angel Oak Capital的關聯公司,Angel Oak Capital是一家領先的替代信用管理公司,在抵押貸款信用市場中佔據領導地位,涉及資產管理、貸款和資本市場。Angel Oak Mortgage Lending,作爲Angel Oak的一個關聯抵押貸款發起平台,是非Qm貸款生產的市場領導者。

“Economic book value” is a non-GAAP financial measure of our financial position. To calculate our economic book value, the portions of our non-recourse financing obligation held at amortized cost are adjusted to fair value. These adjustments are also reflected in the table below in our end of period total stockholders’ equity. Management considers economic book value to provide investors with a useful supplemental measure to evaluate our financial position as it reflects the impact of fair value changes for our legally held retained bonds, irrespective of the accounting model applied for GAAP reporting purposes. Economic book value does not represent and should not be considered as a substitute for book value per share of common stock or stockholders’ equity, as determined in accordance with GAAP, and our calculation of this measure may not be comparable to similarly titled measures reported by other companies.

The following table sets forth a reconciliation from GAAP total stockholders’ equity and book value per share of common stock to economic book value and economic book value per share of common stock as of September 30, 2024 and December 31, 2023:

September 30, 2024

December 31, 2023

(in thousands except for share and per share data)

GAAP total stockholders’ equity

$

265,098

$

256,106

Adjustments:

Fair value adjustment for securitized debt held at amortized cost

64,522

81,942

Stockholders’ equity including economic book value adjustments

$

329,620

$

338,048

Number of shares of common stock outstanding at period end

23,511,272

24,965,274

Book value per share of common stock

$

11.28

$

10.26

Economic book value per share of common stock

$

14.02

$

13.54

30

Results of Operations

Three Months Ended September 30, 2024 and 2023

The following table sets forth a summary of our results of operations for the three months ended September 30, 2024 and 2023:

Three Months Ended

September 30, 2024

September 30, 2023

(in thousands)

INTEREST INCOME, NET

Interest income

$

27,444

$

23,900

Interest expense

18,424

16,490

NET INTEREST INCOME

$

9,020

$

7,410

REALIZED AND UNREALIZED GAINS (LOSSES), NET

Net realized gain (loss) on mortgage loans, derivative contracts, RMBS, and CMBS

$

(6,335)

$

(12,044)

Net unrealized gain (loss) on trading securities, mortgage loans, portion of debt at fair value option, and derivative contracts

35,172

17,299

TOTAL REALIZED AND UNREALIZED GAINS (LOSSES), NET

$

28,837

$

5,255

EXPENSES

Operating expenses

$

1,287

$

1,370

Operating expenses incurred with affiliate

472

599

Due diligence and transaction costs

254

115

Stock compensation

604

447

Securitization costs

—

416

Management fee incurred with affiliate

1,204

1,445

Total operating expenses

$

3,821

$

4,392

INCOME (LOSS) BEFORE INCOME TAXES

$

34,036

$

8,273

Income tax expense

2,832

—

NET INCOME (LOSS) ALLOCABLE TO COMMON STOCKHOLDERS

$

31,204

$

8,273

Other comprehensive income (loss)

2,706

(1,607)

TOTAL COMPREHENSIVE INCOME (LOSS)

$

33,910

$

6,666

31

Net Interest Income

The following table sets forth the components of net interest income for the three months ended September 30, 2024 and 2023:

Three Months Ended

September 30, 2024

September 30, 2023

(in thousands)

Interest income

Interest income / expense

Average balance

Interest income / expense

Average balance

Residential mortgage loans

$

4,659

$

263,095

$

4,272

$

289,916

Residential mortgage loans in securitization trusts

18,580

1,454,736

15,208

1,228,074

Commercial mortgage loans

81

5,246

58

6,329

RMBS and Majority-Owned Affiliate

3,251

117,965

3,067

171,128

CMBS

417

6,239

147

6,453

U.S. Treasury securities

65

6,000

541

46,607

Other interest income

391

40,919

607

42,669

Total interest income

27,444

23,900

Interest expense

Notes payable

2,830

176,159

4,117

205,915

Non-recourse securitization obligation, collateralized by residential mortgage loans

13,731

1,362,039

10,956

1,191,406

Repurchase facilities

900

57,842

1,417

87,279

Senior unsecured notes

963

40,538

—

—

Total interest expense

18,424

16,490

Net interest income

$

9,020

$

7,410

Net interest income for the three months ended September 30, 2024 and 2023 was $9.0 million and $7.4 million, respectively. Net interest income increased in the three months ended September 30, 2024 as compared to the same period in 2023, primarily due to higher net interest income from our residential mortgage loans portfolio (residential mortgage loan interest income less notes payable interest expense) during the three months ended September 30, 2024 . We observed net interest income associated with our residential mortgage loan portfolio of $1.8 million in the three months ended September 30, 2024 compared to $0.1 million in the comparable period of 2023. This was primarily driven by an increase in the weighted average coupon rate of our residential mortgage loans portfolio versus the comparative period, as well as holding more unlevered loans, resulting in a proportionally lower notes payable balance.

32

Total Realized and Unrealized Gains (Losses)

The components of total realized and unrealized gains (losses), net for the three months ended September 30, 2024 and 2023 are set forth as follows:

Three Months Ended

September 30, 2024

September 30, 2023

(in thousands)

Realized and unrealized gain (loss) on securitization, net of unrealized gain (loss) on non-recourse securitization obligation

$

25,228

$

4,352

Realized gain (loss) on RMBS

(565)

(598)

Unrealized gain (loss) on Whole Pool Agency RMBS

(2,138)

(12,367)

Realized gain (loss) on CMBS

(67)

(101)

Realized gain (loss) on interest rate futures

(4,461)

2,828

Realized and unrealized gain (loss) on TBAs

1,880

12,349

Realized and unrealized gain (loss) on residential mortgage loans

7,789

(856)

Realized and unrealized gain (loss) on commercial mortgage loans

—

(35)

Realized and unrealized loss on U.S. Treasury securities

(13)

47

Unrealized appreciation (depreciation) on interest rate futures

1,184

(364)

Total realized and unrealized gains (losses), net

$

28,837

$

5,255

For the three months ended September 30, 2024 and 2023, total realized and unrealized gains (losses), net resulted in gains of $28.8 million and $5.3 million, respectively. During the three months ended September 30, 2024, gains on securitization, net of unrealized gain (loss) on non-recourse securitization obligation drove the majority of the overall gain to our portfolio as valuations increased during the quarter. Similarly, during the three months ended September 30, 2023 gains on securitization, net of unrealized gain (loss) on non-recourse securitization obligation drove the majority of the overall gain to our portfolio as well.

Expenses

Operating Expenses

For the three months ended September 30, 2024 and 2023, our operating expenses were $1.3 million and $1.4 million, respectively. Our operating expenses decreased slightly compared to the comparative period due to continued cost savings actions such as in-sourcing of key accounting functions, vendor contract negotiations, and a decrease in servicing fees associated with servicing our whole loan portfolio.

Operating Expenses Incurred with Affiliate

For the three months ended September 30, 2024 and 2023, our operating expenses incurred with affiliate were $0.5 million and $0.6 million, respectively. These expenses, which are substantially comprised of payroll reimbursements to our Manager, decreased slightly in the third quarter of 2024 compared to the same period of 2023 as a result of additional cost savings actions.

Due Diligence and Transaction Costs

For the three months ended September 30, 2024 and 2023, our due diligence and transaction costs were $254 thousand and $115 thousand, respectively. Our due diligence and transaction expenses increased over the comparative period due to increased purchases of whole loans during the three months ended September 30, 2024 as compared to the three months ended September 30, 2023.

Stock Compensation

For the three months ended September 30, 2024 and 2023, our stock compensation expense was $0.6 million and $0.4 million, respectively. Our stock compensation expense increased for the three months ended September 30, 2024 due to an increase in the estimated impact for outstanding performance-based restricted stock unit awards.

Securitization Costs

For the three months ended September 30, 2024 and 2023, we incurred $0.0 million and $0.4 million of securitization costs, respectively. There was no securitization activity in the third quarter of 2024, and the securitization costs in the comparative period in 2023 were driven by our participation in the AOMT 2023-5 securitization.

33

Management Fee Incurred with Affiliate

For the three months ended September 30, 2024 and 2023, our management fee incurred with affiliate was $1.2 million and $1.4 million, respectively. The decrease is due to the decrease in our average Equity as defined in the Management Agreement for the three months ended September 30, 2024 as compared to the same period in 2023. A key driver of the decrease in the three months ended September 30, 2024 versus the comparative period of 2023 is the repurchase of 1,707,922 million shares of our common stock owned by Xylem Finance, LLC, an affiliate of Davidson Kempner Capital Management, LP, for an aggregate repurchase price of approximately $20 million. The calculation of Equity for the purposes of the Management Agreement includes the addition of Distributable Earnings, which is the primary departure from the calculation of equity in accordance with GAAP.

Nine Months Ended September 30, 2024 and 2023

The following table sets forth a summary of our results of operations for the nine months ended September 30, 2024 and 2023:

Nine Months Ended

September 30, 2024

September 30, 2023

(in thousands)

INTEREST INCOME, NET

Interest income

$

78,558

$

71,403

Interest expense

51,495

50,742

NET INTEREST INCOME

$

27,063

$

20,661

REALIZED AND UNREALIZED GAINS (LOSSES), NET

Net realized gain (loss) on mortgage loans, derivative contracts, RMBS, and CMBS

$

(14,527)

$

(27,056)

Net unrealized gain (loss) on trading securities, mortgage loans, portion of debt at fair value option, and derivative contracts

48,514

27,868

TOTAL REALIZED AND UNREALIZED GAINS (LOSSES), NET

$

33,987

$

812

EXPENSES

Operating expenses

$

4,619

$

5,788

Operating expenses incurred with affiliate

1,444

1,672

Due diligence and transaction costs

663

136

Stock compensation

1,864

1,195

Securitization costs

1,583

2,326

Management fee incurred with affiliate

3,810

4,460

Total operating expenses

$

13,983

$

15,577

INCOME (LOSS) BEFORE INCOME TAXES

$

47,067

$

5,896

Income tax expense (benefit)

3,261

781

NET INCOME (LOSS) ALLOCABLE TO COMMON STOCKHOLDERS

$

43,806

$

5,115

Other comprehensive income (loss)

4,534

12,955

TOTAL COMPREHENSIVE INCOME (LOSS)

$

48,340

$

18,070

34

Net Interest Income

The following table sets forth the components of net interest income for the nine months ended September 30, 2024 and 2023:

Nine Months Ended

September 30, 2024

September 30, 2023

(in thousands)

Interest income

Interest income / expense

Average balance

Interest income / expense

Average balance

Residential mortgage loans

$

13,925

$

284,211

$

18,457

$

467,538

Residential mortgage loans in securitization trusts

51,851

1,357,840

39,753

1,106,621

Commercial mortgage loans

258

5,231

458

8,215

RMBS and Majority Owned Affiliate

9,613

148,677

9,225

164,244

CMBS

1,097

6,428

790

6,394

U.S. Treasury securities

548

14,528

1,201

32,981

Other interest income

1,266

39,239

1,519

37,482

Total interest income

78,558

71,403

Interest expense

Notes payable

9,928

199,644

21,222

366,032

Non-recourse securitization obligation, collateralized by residential mortgage loans

37,624

1,285,118

26,121

1,080,156

Repurchase facilities

2,980

64,431

3,399

89,726

Senior unsecured notes

963

35,681

—

—

Total interest expense

51,495

50,742

Net interest income

$

27,063

$

20,661

Net interest income for the nine months ended September 30, 2024 and 2023 was $27.1 million and $20.7 million, respectively. Net interest income increased in the nine months ended September 30, 2024 as compared to the same period in 2023, primarily due to higher net interest income from our residential mortgage loans portfolio (residential mortgage loan interest income less notes payable interest expense) during the nine months ended September 30, 2024. We observed net interest income associated with our residential mortgage loan portfolio of $4 million in the nine months ended September 30, 2024 compared to a loss of $(2.8) million in the comparable period of 2023. This was primarily driven by an increase in the weighted average coupon rate of our residential mortgage loans portfolio versus the comparative period, as well as holding more unlevered loans, resulting in a proportionally lower notes payable balance.

35

Total Realized and Unrealized Gains (Losses)

The components of total realized and unrealized gains (losses), net for the nine months ended September 30, 2024 and 2023 are set forth as follows:

Nine Months Ended

September 30, 2024

September 30, 2023

(in thousands)

Realized and unrealized gain (loss) on securitization, net of unrealized gain (loss) on non-recourse securitization obligation

$

25,607

$

(7,948)

Realized loss on RMBS

(2,469)

(1,545)

Realized and unrealized gain (loss) on Whole Pool Agency RMBS

(6,355)

(12,627)

Realized gain (loss) on CMBS

(186)

(241)

Realized gain (loss) on interest rate futures

(622)

8,599

Realized and unrealized gain (loss) on TBAs

5,992

(479)

Realized and unrealized (loss) gain on residential mortgage loans

9,839

17,268

Realized and unrealized (loss) gain on commercial mortgage loans

48

113

Realized and unrealized loss on U.S. Treasury securities

(99)

88

Unrealized appreciation on interest rate futures

2,232

(2,416)

Total realized and unrealized gains (losses), net

$

33,987

$

812

For the nine months ended September 30, 2024 and 2023, total realized and unrealized gains (losses), net resulted in a net gain of $34 million and a loss of $0.8 million, respectively. During the nine months ended September 30, 2024, gains on residential mortgage loans in securitization trust, net of unrealized gain (loss) on non-recourse securitization obligation, residential mortgage loans, TBAs, and interest rate futures were offset by losses on RMBS and whole pool agency RMBS. In the nine months ended September 30, 2023, market volatility caused the valuation of our residential mortgage loans in securitization trust and whole pool agency RMBS to decrease, which was offset by gains in our residential mortgage loans portfolio and interest rate futures.

Expenses

Operating Expenses

For the nine months ended September 30, 2024 and 2023, our operating expenses were $4.6 million and $5.8 million, respectively. Our operating expenses decreased during the comparative period due to continued cost savings actions such as in-sourcing of key accounting functions, vendor contract negotiations, and a decrease in servicing fees associated with servicing our whole loan portfolio.

Operating Expenses Incurred with Affiliate

For the nine months ended September 30, 2024 and 2023, our operating expenses incurred with affiliate were $1.44 million and $1.7 million, respectively. These expenses, which are substantially comprised of payroll reimbursements to our Manager, decreased versus the comparative period as a result of additional cost savings actions.

Due Diligence and Transaction Costs

For the nine months ended September 30, 2024 and 2023, our due diligence and transaction costs were $663 thousand and $136 thousand, respectively. Our due diligence and transaction expenses increased versus the comparative period as we purchased more whole loans during the nine months ended September 30, 2024 than the nine months ended September 30, 2023.

Stock Compensation

For the nine months ended September 30, 2024 and 2023 our stock compensation expense was $1.9 million and $1.2 million, respectively. Stock compensation expense increased for the nine months ended September 30, 2024 due to an increase in the estimated impact for outstanding performance-based restricted stock unit awards.

36

Securitization Costs

Securitization costs of $1.6 million were incurred for the nine months ended September 30, 2024 in connection with the AOMT 2024-3, AOMT 2024-4, and AOMT 2024-6 securitization transactions. There were $2.3 million of securitization costs incurred for the comparable period in 2023, representing costs incurred in connection with the AOMT 2023-1, AOMT 2023-4, and AOMT 2023-5 securitizations.

Management Fee Incurred with Affiliate

For the nine months ended September 30, 2024 and 2023, our management fee incurred with affiliate was $3.8 million and $4.5 million, respectively. The decrease is due to the decrease in our average Equity as defined in the Management Agreement for the nine months ended September 30, 2024 as compared to the same period in 2023. A key driver of the decrease in the nine months ended September 30, 2024 versus the comparative period of 2023 is the repurchase of 1,707,922 million shares of our common stock owned by Xylem Finance, LLC, an affiliate of Davidson Kempner Capital Management, LP, for an aggregate repurchase price of approximately $20 million. The calculation of Equity for the purposes of the Management Agreement includes the addition of Distributable Earnings, which is the primary departure from the calculation of equity in accordance with GAAP.

37

Our Portfolio

As of September 30, 2024, our portfolio consisted of approximately $2.2 billion of residential mortgage loans, RMBS, and other target assets. Certain of these portfolio assets are located in states such as Florida and California where natural disasters such as hurricanes and earthquakes may occasionally occur. We require all of our collateral to be adequately insured. The graphs in the subsequent detail of residential mortgage loans, residential mortgage loans held in securitization trusts, and residential mortgage loans underlying RMBS issuances show the percentage of residential mortgage loans held in each state where there is a concentration of loans.

The following table sets forth additional information regarding our portfolio, including the manner in which our equity capital was allocated among investment types, as of September 30, 2024:

Fair Value

Collateralized Debt

Allocated Capital

% of Total Capital

Portfolio:

($ in thousands)

Residential mortgage loans

$

428,909

$

333,042

$

95,867

36.2

%

Residential mortgage loans in securitization trust

1,452,907

1,353,758

$

99,149

37.4

%

Total whole loan portfolio

$

1,881,816

$

1,686,800

$

195,016

73.6

%

Investment securities

RMBS

$

283,105

$

53,164

$

229,941

86.7

%

U.S. Treasury securities

49,971

49,712

259

0.1

%

Total investment securities

$

333,076

$

102,876

$

230,200

86.8

%

Investment in Majority-Owned Affiliate

$

18,720

$

—

$

18,720

7.1

%

Total investment portfolio

$

2,233,612

$

1,789,676

$

443,936

167.5

%

Target assets (1)

$

2,183,641

$

1,739,964

$

443,677

167.4

%

Cash

$

42,052

$

—

$

42,052

15.8

%

Other assets and liabilities (2)

(220,889)

—

(220,889)

(83.3)

%

Total

$

2,054,775

$

1,789,676

$

265,099

100.0

%

(1) “Target assets” as defined by us excludes U.S. Treasury securities, and includes our investment in a Majority-Owned Affiliates.

(2) Other assets and liabilities presented is calculated as a net liability substantially comprised of $194.7 million due to broker for our quarter-end purchase of certain Freddie Mac and Fannie Mae-issued whole pool agency residential mortgage-backed securities (“Whole Pool Agency RMBS”), and excluding the portion of “other assets” which includes our investment in a Majority-Owned Affiliate, which is considered a target asset.

38

As of December 31, 2023, our portfolio consisted of approximately $2.1 billion of residential mortgage loans, RMBS, and other target assets. The following table sets forth additional information regarding our portfolio including the manner in which our equity capital was allocated among investment types, as of December 31, 2023:

Fair Value

Collateralized Debt

Allocated Capital

% of Total Capital

Portfolio:

($ in thousands)

Residential mortgage loans

$

380,040

$

290,610

$

89,430

34.9

%

Residential mortgage loans in securitization trust

1,221,067

1,169,154

51,913

20.3

%

Total whole loan portfolio

$

1,601,107

$

1,459,764

$

141,343

55.2

%

Investment securities

RMBS

$

472,058

44,643

$

427,415

166.9

%

Investment in Majority-Owned Affiliates

16,232

—

16,232

6.3

%

U.S. Treasury Securities

149,927

149,013

914

0.4

%

Total investment securities

$

638,217

$

193,656

$

444,561

173.6

%

Total investment portfolio

$

2,239,324

$

1,653,420

$

585,904

228.8

%

Target assets (1)

$

2,089,397

$

1,504,407

$

585,904

228.8

%

Cash

$

41,625

$

—

$

41,625

16.2

%

Other assets and liabilities (2)

(371,423)

—

(371,423)

(145.0)

%

Total

$

1,909,526

$

1,653,420

$

256,106

100.0

%

(1) “Target assets” as defined by us excludes U.S. Treasury securities, and includes our investment in a Majority-Owned Affiliates.

(2) Other assets and liabilities presented is calculated as a net liability substantially comprised of $392.0 million due to broker for our quarter-end purchase of certain Freddie Mac and Fannie Mae-issued Whole Pool Agency RMBS, and excluding the portion of “other assets” which includes our investment in a Majority-Owned Affiliates, which is considered a target asset. Additionally, other assets includes $5.2 million of commercial loans and $6.6 million of CMBS.

Residential Mortgage Loans

The following table sets forth additional information on the residential mortgage loans in our portfolio as of September 30, 2024:

Portfolio Range

Portfolio Weighted Average

($ in thousands)

Unpaid principal balance (“UPB”)

$75 - $3,403

$481

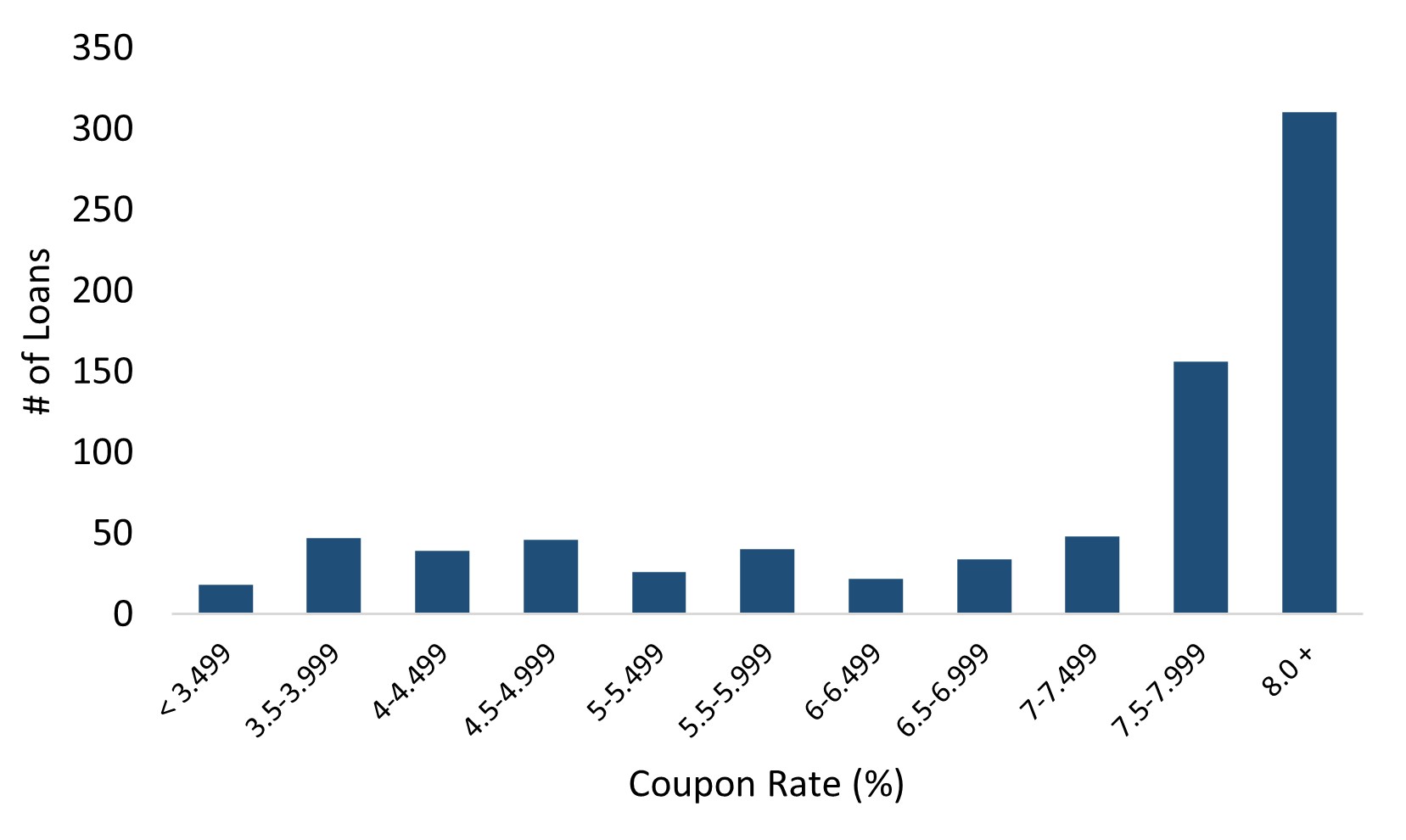

Interest rate

3.63% - 11.88%

7.73%

Maturity date

6/27/2044 - 8/15/2064

July 2054

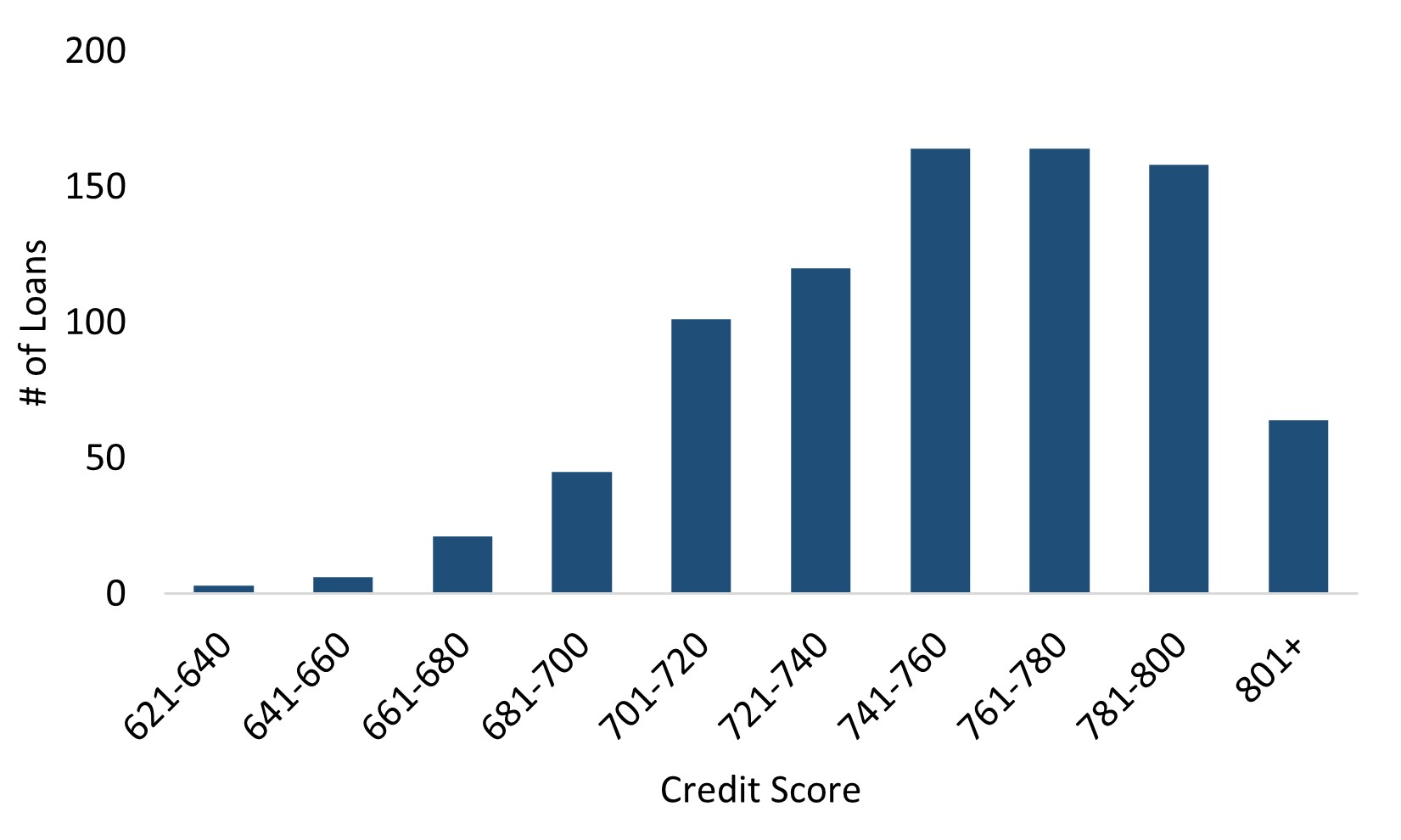

FICO score at loan origination

628 - 823

754

LTV at loan origination

7.1% - 90.0%

70.6%

DTI at loan origination

1.94% - 52.0%

31.6%

Percentage of first lien loans

N/A

98.9%

Percentage of loans 90+ days delinquent (based on UPB)

N/A

0.7%

39

The following table sets forth additional information on the residential mortgage loans in our portfolio as of December 31, 2023:

Portfolio Range

Portfolio Weighted Average

($ in thousands)

Unpaid principal balance (“UPB”)

$18 - $3,410

$492

Interest rate

2.99% - 12.50%

6.8%

Maturity date

9/27/2048 - 11/27/2063

December 2053

FICO score at loan origination

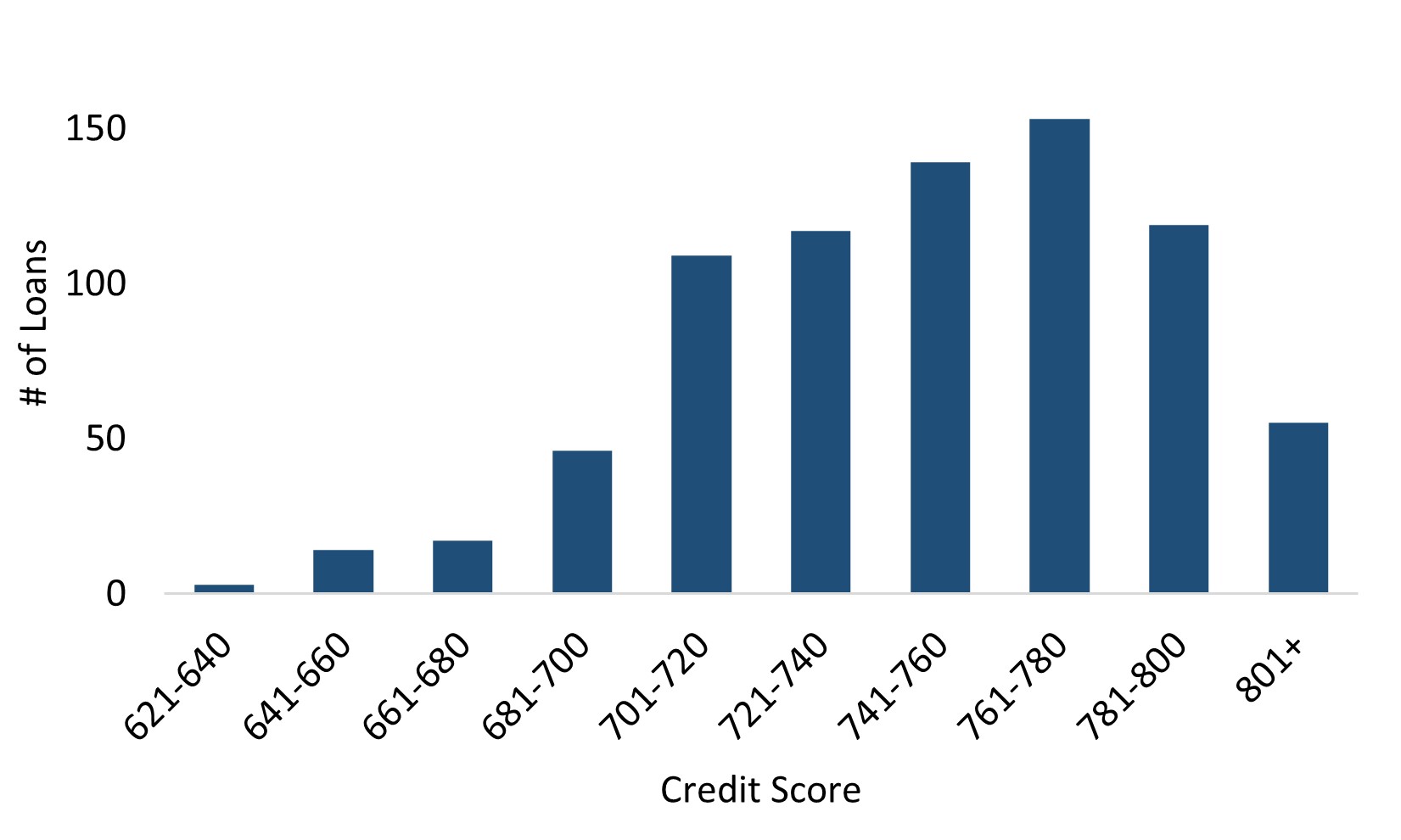

624 - 825

748

LTV at loan origination

9.00% - 90.00%

69.4%

DTI at loan origination

1.90% - 59.10%

30.9%

Percentage of first lien loans

N/A

100%

Percentage of loans 90+ days delinquent (based on UPB)

N/A

0.9%

The following charts illustrate the distribution of the credit scores and coupon rates by the number of loans in our residential mortgage loan portfolio as of September 30, 2024:

40

The following charts illustrate the distribution of the credit scores and coupon rates by the number of loans in our residential mortgage loan portfolio as of December 31, 2023:

41

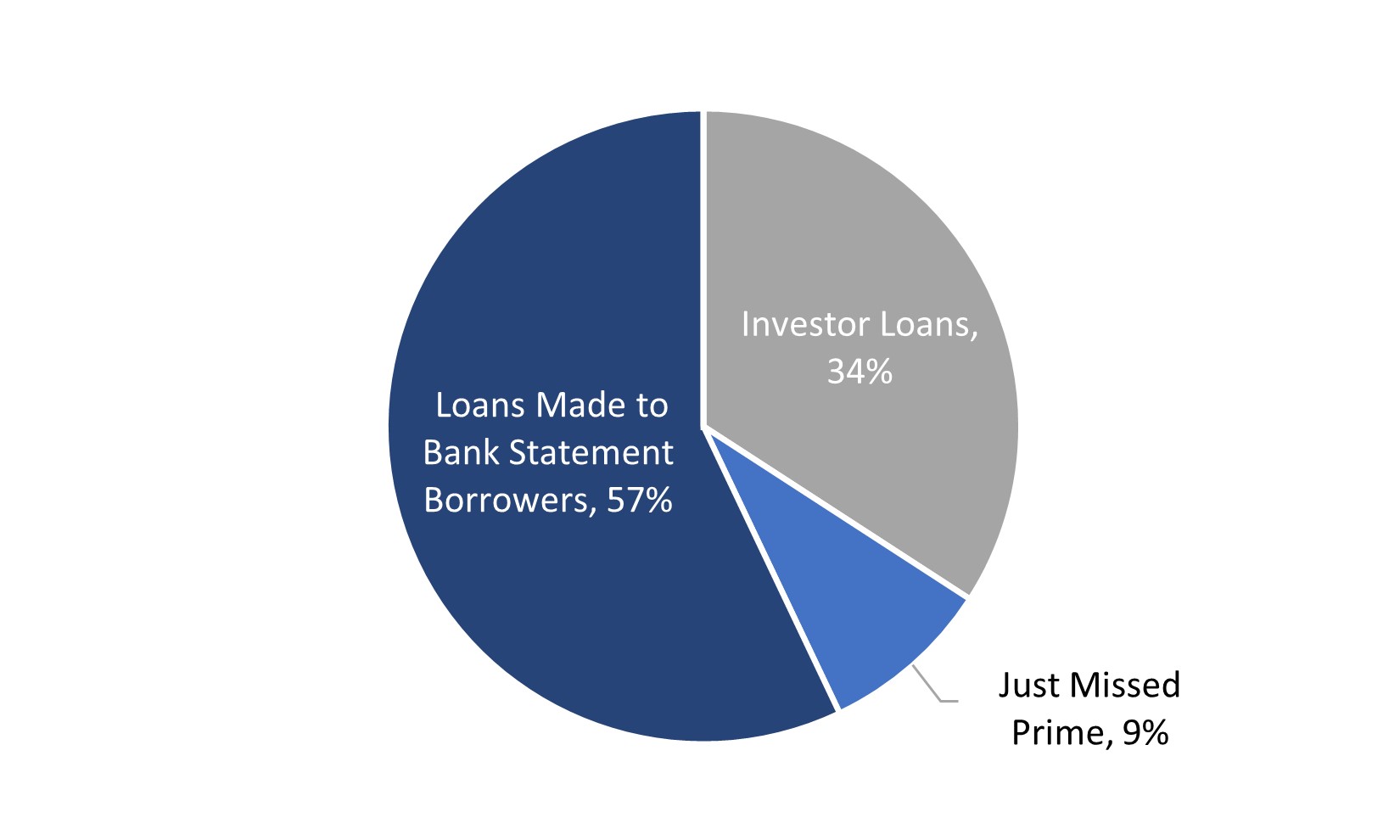

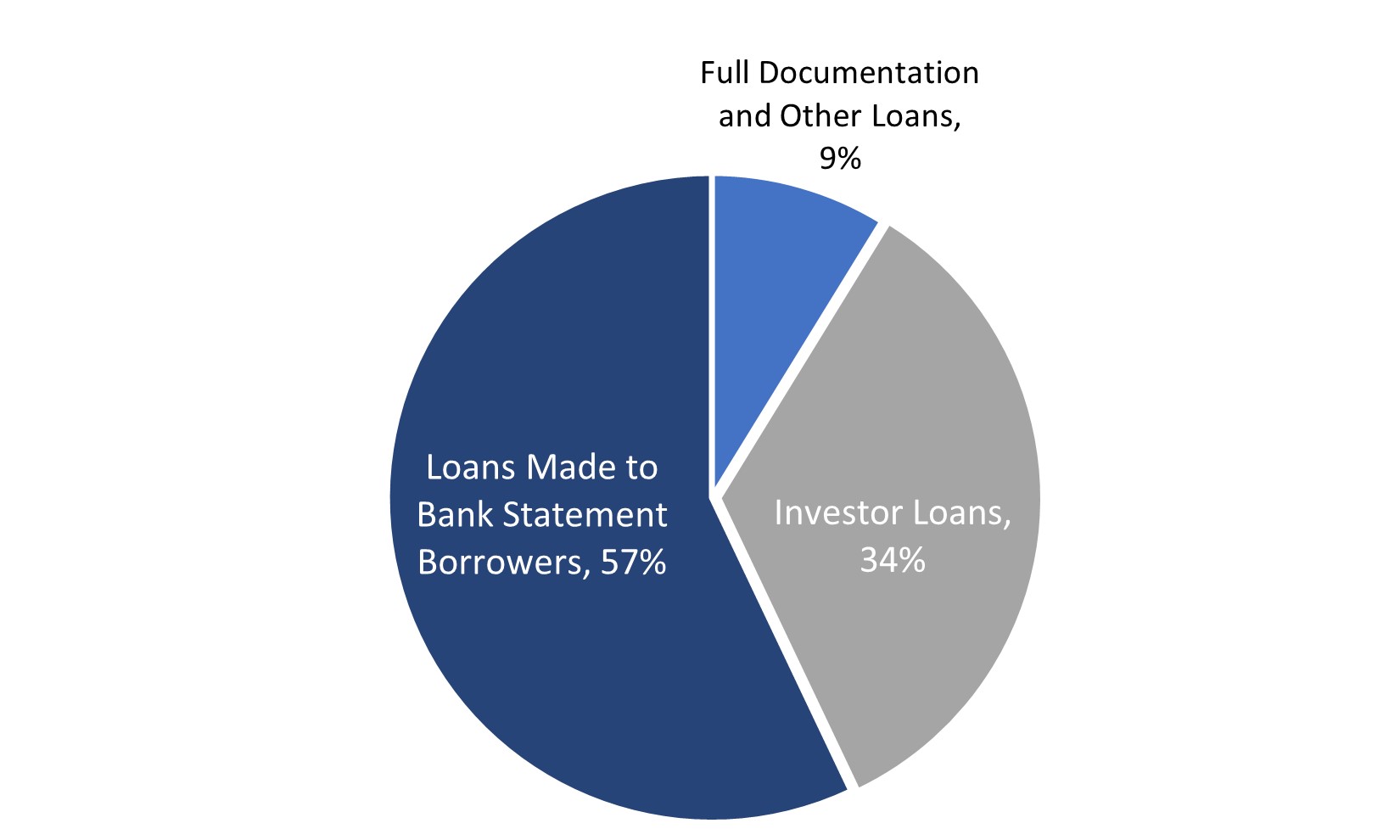

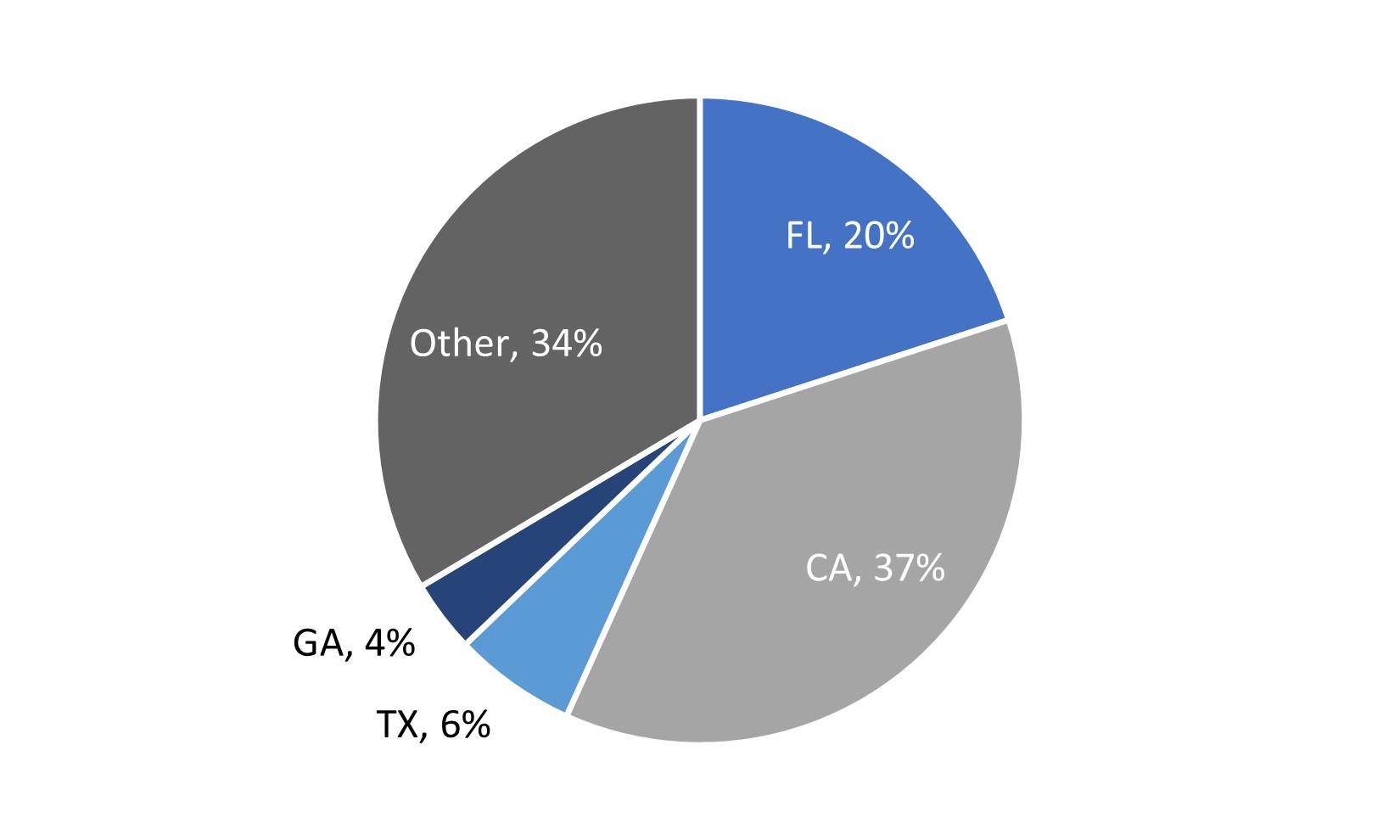

The following charts illustrate additional characteristics of our residential mortgage loans in our portfolio that we owned directly as of September 30, 2024, based on the product profile, borrower profile, and geographic location (percentages are based on the aggregate unpaid principal balance of such loans):

Characteristics of Our Residential Mortgage Loans as of September 30, 2024:

Note: No state in “Other” represents more than a 3% concentration of the residential mortgage loans in our portfolio that we owned directly as of September 30, 2024. Numbers presented may add to more than 100% due to rounding.

42

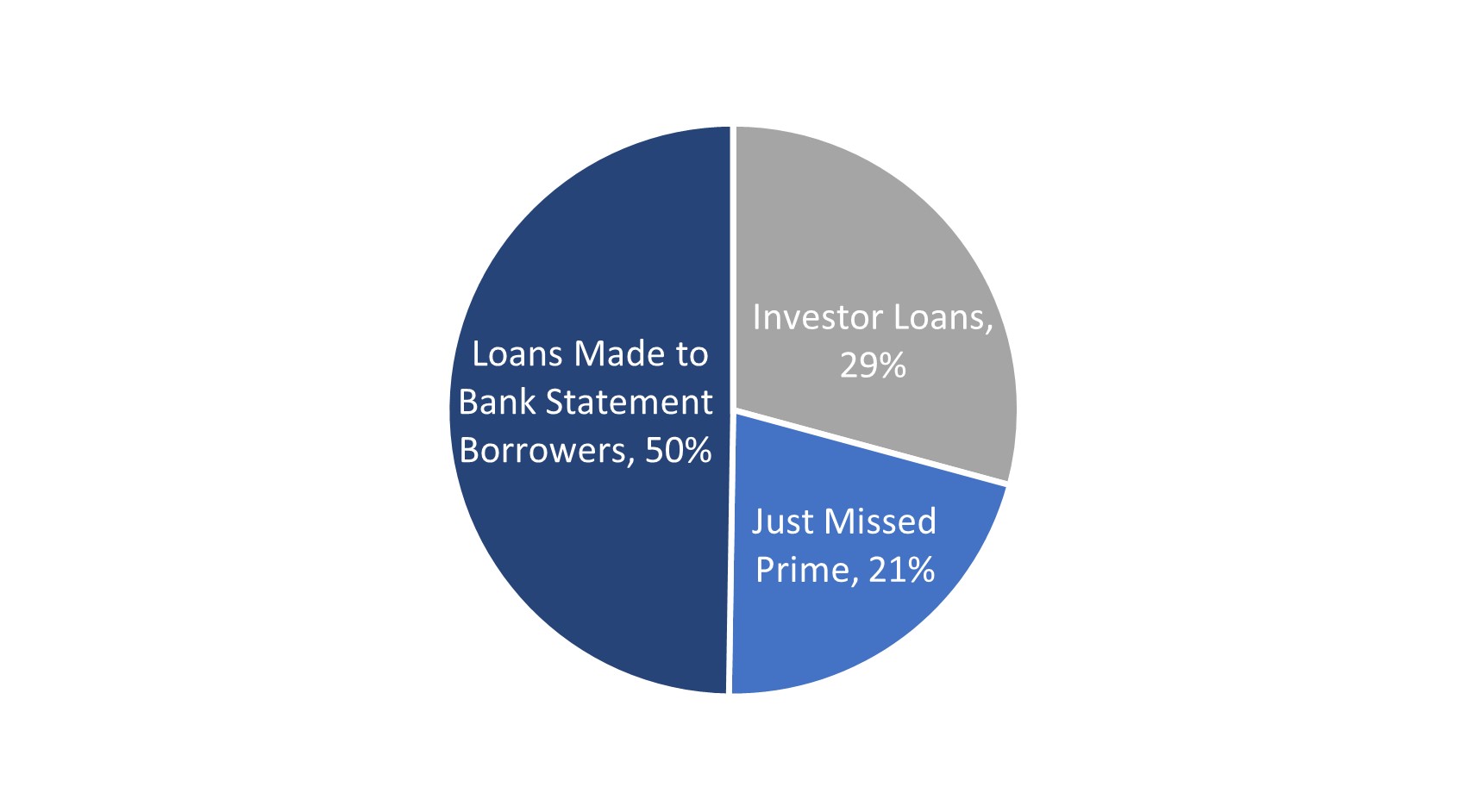

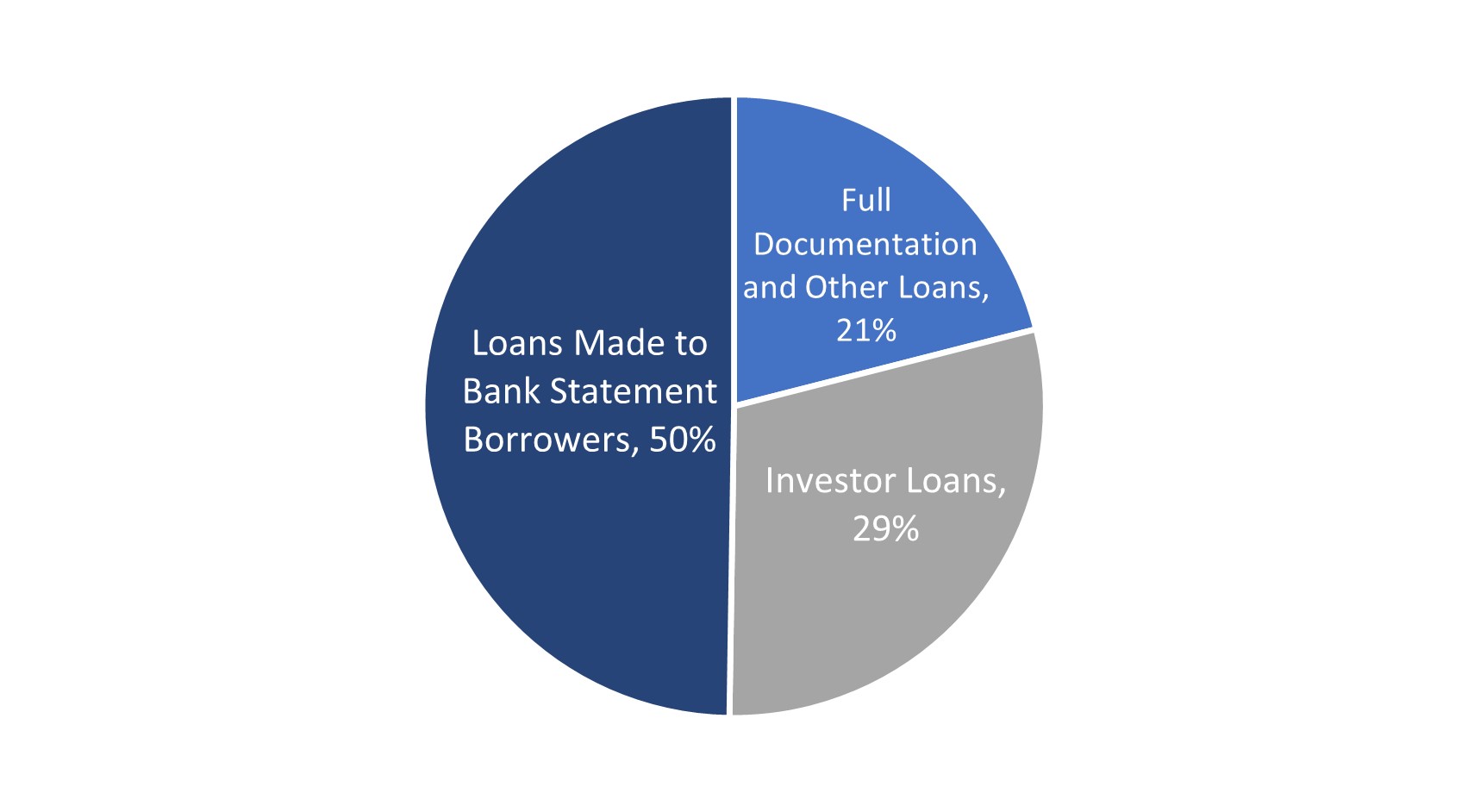

The following charts illustrate additional characteristics of the residential mortgage loans in our portfolio that we owned directly as of December 31, 2023, based on the product profile, borrower profile, and geographic location (percentages are based on the aggregate unpaid principal balance of such loans):

Characteristics of Our Residential Mortgage Loans as of December 31, 2023:

Note: No state in “Other” represents more than a 3% concentration of the residential mortgage loans in our portfolio that we owned directly as of December 31, 2023. Numbers presented may add to more than 100% due to rounding.

43

Residential Mortgage Loans Held in Securitization Trusts

The following table sets forth the information regarding the underlying collateral of our residential mortgage loans held in securitization trusts as of September 30, 2024:

($ in thousands)

UPB

$1,512,722

Fair Value

$1,452,907

Number of loans

3,594

Weighted average loan coupon

5.12%

Average loan amount

$422

Weighted average LTV at loan origination and deal date

67.0%

Weighted average credit score at loan origination and deal date

741

Current 3-month constant prepayment rate (“CPR”) (1)

7.8%

Percentage of loans 90+ days delinquent (based on UPB)

1.9%

(1) CPR is a method of expressing the prepayment rate for a mortgage pool that assumes that a constant fraction of the remaining principal is prepaid each month or year.

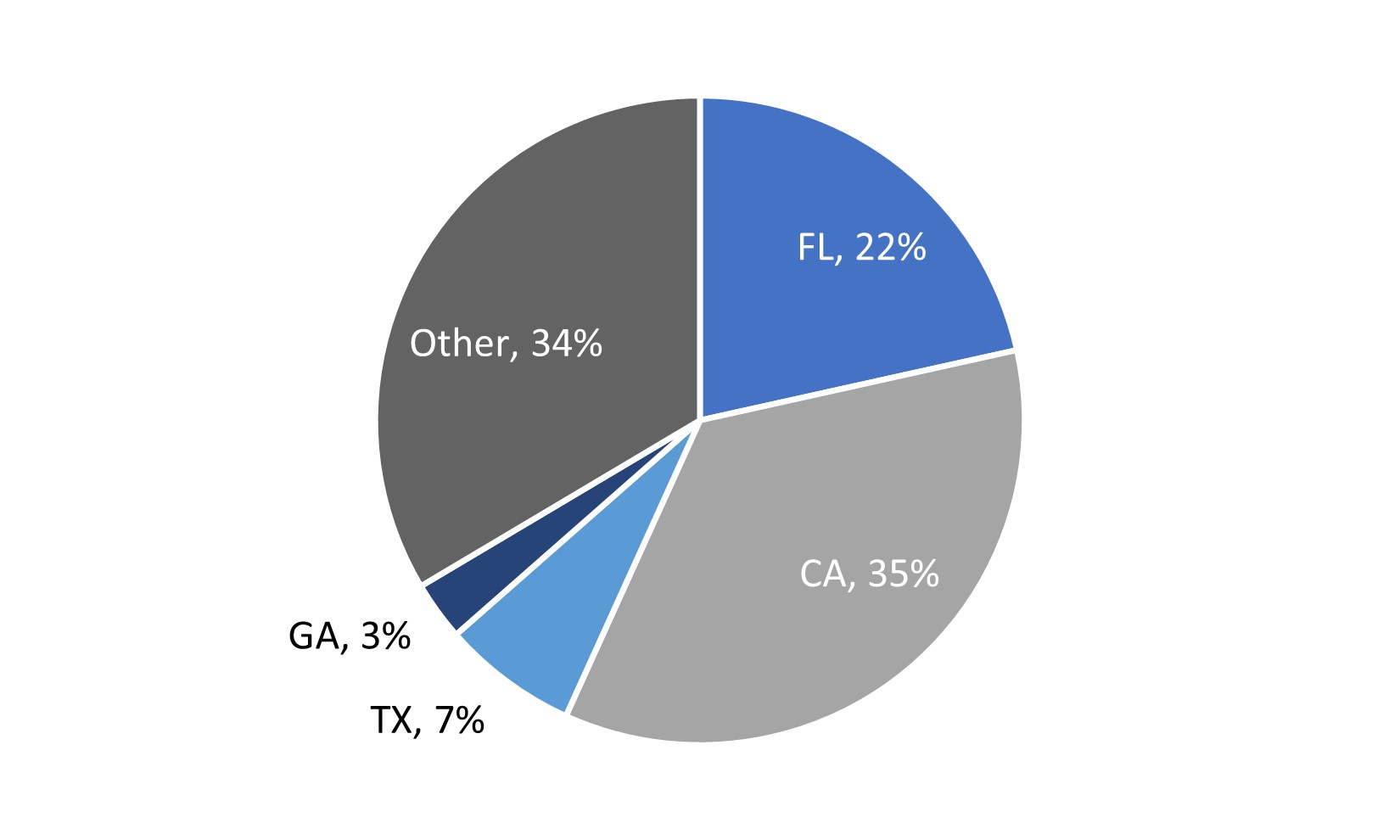

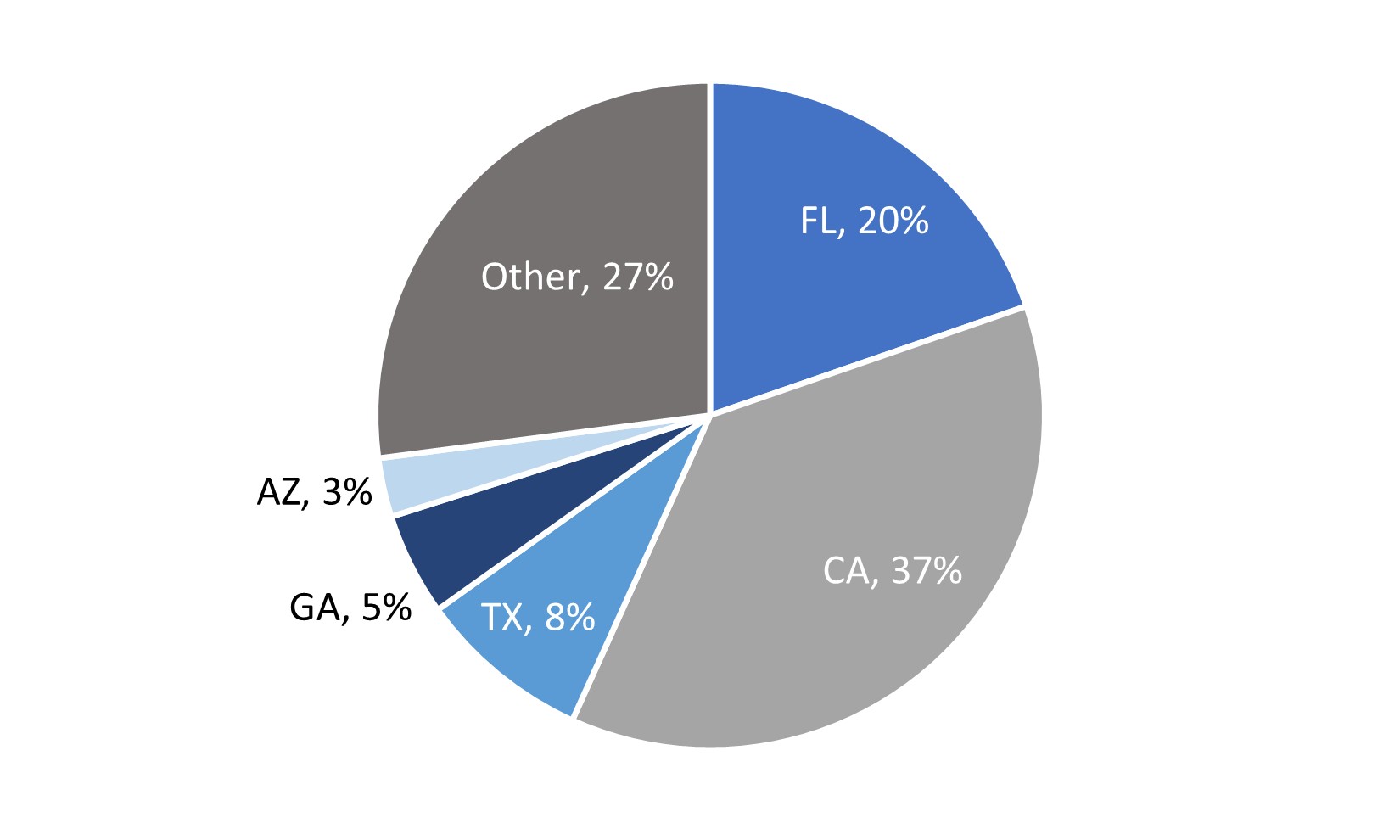

The following chart illustrates the geographic distribution of the underlying collateral of our residential mortgage loans held in securitization trusts as of September 30, 2024 (percentages are based on the aggregate unpaid principal balance of such loans):

Note: No state in “Other” represents more than a 3% concentration of the underlying collateral of our residential mortgage loans held in securitization trusts as of September 30, 2024. Numbers presented may add to more than 100% due to rounding.

44

The following table sets forth the information regarding the underlying collateral of our residential mortgage loans held in securitization trusts as of December 31, 2023:

($ in thousands)

UPB

$1,334,963

Fair Value

$1,221,067

Number of loans

3,112

Weighted average loan coupon

4.7%

Average loan amount

$429

Weighted average LTV at loan origination and deal date

68.0%

Weighted average credit score at loan origination and deal date

742

Current 3-month CPR

5.6%

Percentage of loans 90+ days delinquent (based on UPB)

1.0%

The following chart illustrates the geographic distribution of the underlying collateral of our residential mortgage loans held in securitization trusts as of December 31, 2023 (percentages are based on the aggregate unpaid principal balance of such loans):

Note: No state in “Other” represents more than a 3% concentration of the underlying collateral of our residential mortgage loans held in securitization trusts as of December 31, 2023. Numbers presented may add to more than 100% due to rounding.

45

RMBS

We have participated in numerous securitization transactions pursuant to which we contributed to a securitization trust under the purview of AOMT I, LLC, non‑QM loans that we had accumulated and held on our balance sheet. These loans were purchased from affiliated and unaffiliated entities. In return, we received bonds from these securitization trusts, and cash. At times, we were allocated certain risk retention securities as part of these transactions. Risk retention securities represent at least 5% of a horizontal or vertical slice of the bonds issued as part of the transaction.

Certain information regarding the mortgage loans underlying our portfolio of RMBS issued in such securitization transactions is set forth below as of September 30, 2024:

AOMT 2019 Securitizations

AOMT 2020 Securitizations

AOMT 2023 Securitizations

AOMT 2024 Securitizations

($ in thousands)

UPB of loans

$295,926

$154,043

$1,119,064

$882,348

Number of loans

1,081

477

2,165

2,032

Weighted average loan coupon

7.21

%

5.81

%

5.25

%

5.28

%

Average loan amount

$274

$323

$517

$434

Weighted average LTV at loan origination and deal date

69.0

%

74.1

%

68.7

%

68.4

%

Weighted average credit score at loan origination and deal date

707

719

731

731

Current 3-month CPR (1)

13.4

%

8.7

%

7.0

%

8.3

%

90+ day delinquency (as a % of UPB)

8.1

%

2.9

%

1.4

%

1.2

%

Weighted Average 90+ Delinquency (as a % of Original Balance)

1.2

%

1.0

%

1.3

%

1.1

%

Weighted Average LTV of 90+ Delinquent Loans (FHFA HPI Estimate) (2)

49.5

%

—

%

68.8

%

68.0

%

Fair value of first loss piece (3,4)

19,383

23,676

11,500

3,109

Investment thickness (5)

21.45

20.14

7.60

10.05

(1) CPR is a method of expressing the prepayment rate for a mortgage pool that assumes that a constant fraction of the remaining principal is prepaid each month or year.

(2) AOMT 2020-3 does not have LTV or Federal Housing Finance Agency Home Price Index Estimates (“FHFA HPI Estimates”); accordingly, original LTV is used.

(3) Represents the fair value of the securities we hold in the first loss tranche in each securitization.

(4) The fair value of the first loss pieces presented for AOMT 2023-1, AOMT 2023-5, AOMT 2023-7, AOMT 2024-3, and AOMT 2024-6 is the total at risk for the Majority-Owned Affiliates.

(5) Represents the average size of the subordinate securities we own as investments in each securitization relative to the average overall size of the securitization.

46

Certain information regarding the mortgage loans underlying our portfolio of RMBS issued in AOMT securitization transactions is set forth below as of December 31, 2023, unless otherwise stated:

AOMT 2019 Securitizations

AOMT 2020 Securitizations

AOMT 2023 Securitizations

($ in thousands)

UPB of loans

$331,376

$167,028

$1,192,450

Number of loans

1197

512

2288

Weighted average loan coupon

6.90

%

5.80

%

5.30

%

Average loan amount

$277

$326

$521

Weighted average LTV at loan origination and deal date

70

%

74

%

70

%

Weighted average credit score at loan origination and deal date

707

720

733

Current 3-month CPR (1, 6)

14.3

%

5.4

%

4.3

%

90+ day delinquency (as a % of UPB)

9.0

%

3.0

%

1.6

%

Weighted Average 90+ Delinquency (as a % of Original Balance)

1.5

%

1.1

%

1.3

%

Weighted Average LTV of 90+ Delinquent Loans (FHFA HPI Estimate) (2)

50.8

%

74.1

%

72.8

%

Fair value of first loss piece (3,5)

$18,057

$21,389

$13,003

Investment thickness (4)

19.15

%

18.57

%

3.78

%

(1) CPR is a method of expressing the prepayment rate for a mortgage pool that assumes that a constant fraction of the remaining principal is prepaid each month or year.

(2) AOMT 2020-3 does not have LTV or Federal Housing Finance Agency Home Price Index Estimates (“FHFA HPI Estimates”); accordingly, original LTV is used.

(3) Represents the fair value of the securities we hold in the first loss tranche in each securitization.

(4) Represents the average size of the subordinate securities we own as investments in each securitization relative to the average overall size of the securitization.

(5) The fair value of the first loss pieces presented for AOMT 2023-1, AOMT 2023-5, and AOMT 2023-7 is the total at risk for the Majority-Owned Affiliates.

(6) AOMT 2023-5 reflects one-month CPR.

47

The following table provides certain information with respect to our RMBS portfolio both received in AOMT securitization transactions and acquired from other third parties as of September 30, 2024:

RMBS

Repurchase Debt (1)

Allocated Capital

AOMT

Third Party RMBS

Total

AOMT

Third Party RMBS

Total

AOMT

Third Party RMBS

Total

(in thousands)

Mezzanine

$

13,463

$

—

$

13,463

$

5,292

$

—

$

5,292

$

8,171

$

—

$

8,171

Subordinate

62,223

—

$

62,223

20,175

—

$

20,175

$

42,048

$

—

$

42,048

Interest only / excess

13,055

—

$

13,055

—

—

$

—

$

13,055

$

—

$

13,055

Whole pool (2)

—

194,364

$

194,364

—

—

$

—

$

—

$

194,364

$

194,364

Retained RMBS in VIEs (3)

—

—

$

—

27,697

—

$

27,697

$

(27,697)

$

—

$

(27,697)

Subtotal

$

88,741

$

194,364

$

283,105

$

53,164

$

—

$

53,164

$

35,577

$

194,364

$

229,941

Investment in Majority Owned Affiliates

$

18,720

$

—

$

18,720

$

—

$

—

$

—

$

18,720

$

—

$

18,720

Total

$

107,461

$

194,364

$

301,825

$

53,164

$

—

$

53,164

$

54,297

$

194,364

$

248,661

(1) Repurchase debt includes borrowings against retained bonds received from on-balance sheet securitizations (i.e., consolidated VIEs).

(2) The whole pool RMBS presented as of September 30, 2024 were purchased from a broker to whom the Company owes approximately $194.7 million, payable upon the settlement date of the trade. See Note 6 — Due to Broker in our unaudited condensed consolidated financial statements included in this report.

(3) A portion of repurchase debt includes borrowings against retained bonds received from on-balance sheet securitizations (i.e., consolidated VIEs). These bonds, with a fair value of $143.5 million, are not reflected in the condensed consolidated balance sheets, as the Company reflects the assets of the VIE (residential mortgage loans in securitization trusts - at fair value) on its condensed consolidated balance sheets.

48

The following table provides certain information with respect to our RMBS portfolio both received in AOMT securitization transactions and acquired from other third parties as of December 31, 2023:

RMBS

Repurchase Debt (1,3)

Allocated Capital

AOMT

Third Party RMBS

Total

AOMT

Third Party RMBS

Total

AOMT

Third Party RMBS

Total

(in thousands)

Mezzanine

$

10,972

$

—

$

10,972

$

844

$

—

$

844

$

10,128

$

—

$

10,128

Subordinate

55,665

—

55,665

19,812

—

19,812

35,853

—

$

35,853

Interest only / excess

13,059

—

13,059

1,871

—

1,871

11,188

—

$

11,188

Whole pool (2)

—

392,362

392,362

—

—

—

—

392,362

$

392,362

Retained RMBS in VIEs (3)

—

—

—

22,116

—

22,116

(22,116)

—

(22,116)

Subtotal

$

79,696

$

392,362

$

472,058

$

44,643

$

—

$

44,643

$

35,053

$

392,362

$

427,415

Investment in Majority Owned Affiliates

$

16,232

$

—

16,232

$

—

$

—

—

$

16,232

$

—

16,232

Total

$

95,928

$

392,362

$

488,290

$

44,643

$

—

$

44,643

$

51,285

$

392,362

$

443,647

(1) Repurchase debt includes borrowings against retained bonds received from on-balance sheet securitizations (i.e., consolidated VIEs).

(2) The whole pool RMBS presented as of December 31, 2023 were purchased from a broker to whom the Company owes approximately $392.0 million, payable upon the settlement date of the trade. See Note 6 — Due to Broker in our unaudited condensed consolidated financial statements included in this report.

(3) A portion of repurchase debt includes borrowings against retained bonds received from on-balance sheet securitizations (i.e., consolidated VIEs). These bonds, with a fair value of $124.1 million, are not reflected in the condensed consolidated balance sheets, as the Company reflects the assets of the VIE (residential mortgage loans in securitization trusts - at fair value) on its condensed consolidated balance sheets.

49

The following table sets forth information with respect to our RMBS ending balances, at fair value, for the period ended September 30, 2024:

Senior

Mezzanine

Subordinate

Interest Only

Whole Pool

Total

(in thousands)

Beginning fair value as of June 30, 2024

$

—

$

13,100

$

60,107

$

13,027

$

180,518

$

266,752

Acquisitions:

Retained bonds received in securitizations

—

—

—

—

—

$

—

Third party securities

—

—

—

—

194,697

$

194,697

Effect of principal payments / sales

—

(280)

—

(178,702)

$

(178,982)

IO and excess servicing prepayments

—

—

—

(565)

—

$

(565)

Changes in fair value, net

—

644

2,115

593

(2,149)

$

1,203

Ending fair value as of September 30, 2024

$

—

$

13,464

$

62,222

$

13,055

$

194,364

$

283,105

The following table sets forth information with respect to our RMBS ending balances, at fair value, for the year ended December 31, 2023:

Senior

Mezzanine

Subordinate

Interest Only

Whole Pool

Total

(in thousands)

Beginning fair value as of December 31, 2022

$

—

$

1,958

$

49,578

$

10,424

$

993,378

$

1,055,338

Acquisitions:

Retained bonds received in securitizations

—

9,831

4,880

3,530

—

18,241

Third party securities

—

—

—

—

1,741,864

1,741,864

Effect of principal payments / sales

—

(869)

—

—

(2,339,028)

(2,339,897)

IO and excess servicing prepayments

—

—

—

(1,396)

—

(1,396)

Changes in fair value, net

—

52

1,207

501

(3,852)

(2,092)

Ending fair value as of December 31, 2023

$

—

$

10,972

$

55,665

$

13,059

$

392,362

$

472,058

50

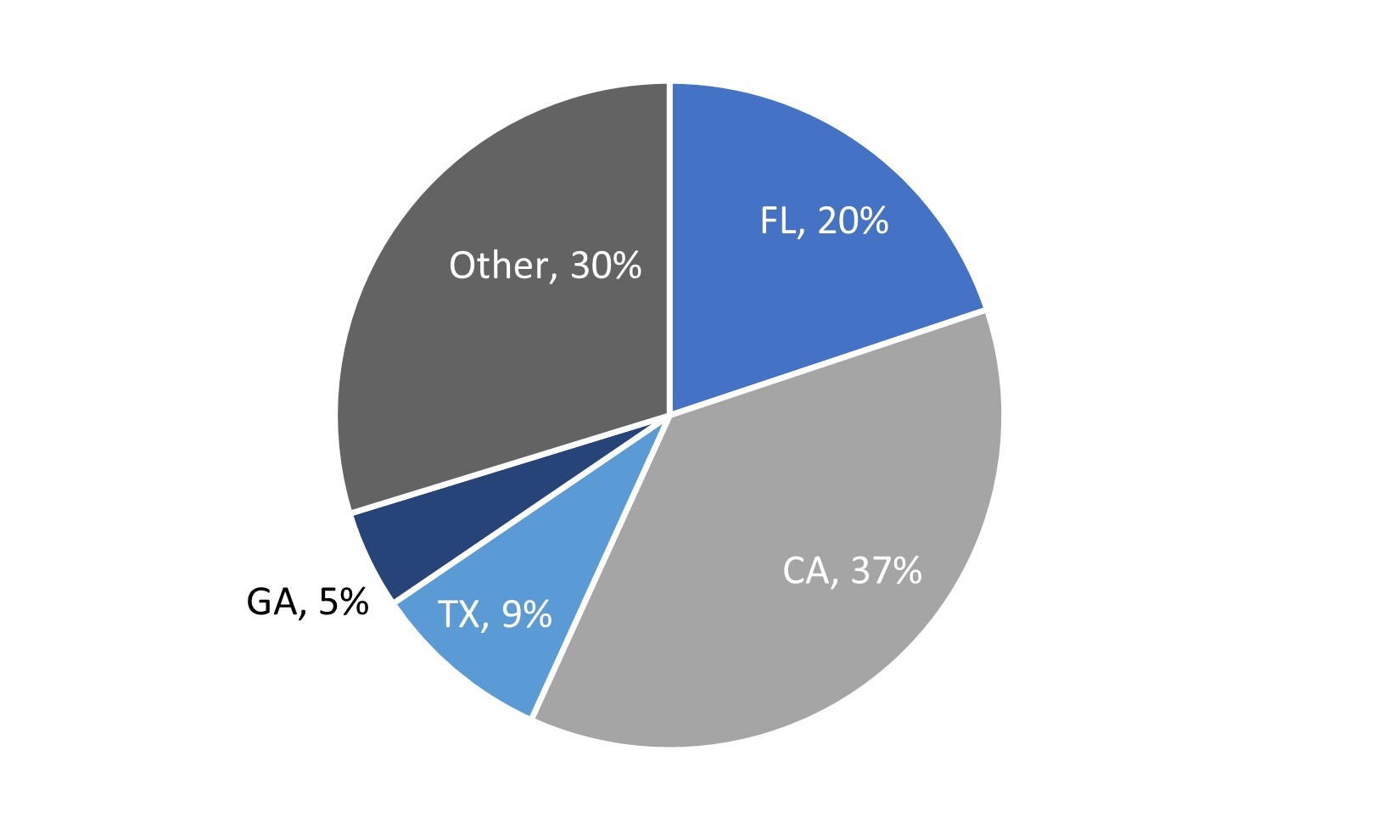

The following chart illustrates the geographic diversification of the loans underlying our portfolio of RMBS issued in AOMT securitization transactions as of September 30, 2024 (percentages are based on the aggregate unpaid principal balance of such loans):

Geographic Diversification of Loans Underlying Our Portfolio

of RMBS Issued in AOMT Securitization Transactions

(as of September 30, 2024)

Note: No state in “Other” represents more than a 4% concentration of the loans underlying our portfolio of RMBS issued in AOMT securitization transactions as of September 30, 2024. Numbers presented may add to more than 100% due to rounding.

The following chart illustrates the geographic diversification of the loans underlying our portfolio of RMBS issued in AOMT securitization transactions as of December 31, 2023 (percentages are based on the aggregate unpaid principal balance of such loans):

Geographic Diversification of Loans Underlying Our Portfolio

of RMBS Issued in AOMT Securitization Transactions

(as of December 31, 2023)

Note: No state in “Other” represents more than a 4% concentration of the loans underlying our portfolio of RMBS issued in AOMT securitization transactions as of December 31, 2023. Numbers presented may add to more than 100% due to rounding.

51

CMBS

Certain information regarding the commercial mortgage loans underlying our portfolio of CMBS issued in the AOMT 2020-SBC1 securitization transaction is shown below as of September 30, 2024 and December 31, 2023:

September 30, 2024

December 31, 2023

($ in thousands)

UPB of loans

$104,138

$112,302

Number of loans

134

145

Weighted average loan coupon

7.9

%

7.5

%

Average loan amount

$777

$774

Weighted average LTV at loan origination and deal date

56.2

%

56.2

%

The following table provides certain information with respect to the CMBS we received in connection with the AOMT 2020-SBC1 securitization transactions as of September 30, 2024 and December 31, 2023:

September 30, 2024

December 31, 2023

CMBS

Repurchase Debt

Allocated Capital

CMBS

Repurchase Debt

Allocated Capital

(in thousands)

Subordinate

2,674

—

2,674

2,706

—

2,706

Interest only / excess

3,262

—

3,262

3,886

—

3,886

Total

$

5,936

$

—

$

5,936

$

6,592

$

—

$

6,592

Liquidity and Capital Resources

Overview

Liquidity is a measurement of our ability to meet potential cash requirements, including ongoing commitments to repay borrowings, fund our investments and operating costs, make distributions to our stockholders, and satisfy other general business needs. Our financing sources currently include payments of principal and interest we receive on our investment portfolio, unused borrowing capacity under our in‑place loan financing lines and repurchase facilities, securitizations of our whole loans, and our ATM Program (as defined below). Additionally, on July 25, 2024, we closed an underwritten public offering and sale of, and issued, $50 million in aggregate principal amount of our 9.500% Senior Notes due 2029. We have deployed the majority of the net proceeds from the offering of the Notes for general corporate purposes, which included the acquisition of non-QM loans and other target assets primarily sourced from our affiliated proprietary mortgage lending platform and other target assets through the secondary market in a manner consistent with our strategy and investment guidelines. Additionally, we used the net proceeds from the offering of the Notes to repurchase 1,707,922 shares of our common stock owned by Xylem Finance LLC, an affiliate of Davidson Kempner Capital Management LP, for an aggregate repurchase price of approximately $20.0 million. See “—Trends and Recent Developments—Notes offering” in this report. Our financing sources historically have included the foregoing, as well as capital contributions from our investors prior to our IPO, and the proceeds from our IPO and concurrent private placement (which capital has all been deployed). Going forward, we may also utilize other types of borrowings, including bank credit facilities and warehouse lines of credit, among others. We may also seek to raise additional capital through public or private offerings of equity, equity-related, or debt securities, depending upon market conditions. The use of any particular source of capital and funds will depend on market conditions, availability of these sources, and the investment opportunities available to us.

We have used and expect to continue to use loan financing lines to finance the acquisition and accumulation of mortgage loans or other mortgage‑related assets pending their eventual securitization. Upon accumulating an appropriate amount of assets, we have financed and expect to continue to finance a substantial portion of our mortgage loans utilizing fixed-rate term securitization funding that provides long‑term financing for our mortgage loans and locks in our cost of funding, regardless of future interest rate movements.

Securitizations may either take the form of the issuance of securitized bonds or the sale of “real estate mortgage investment conduit” securities backed by mortgage loans or other assets, with the securitization proceeds being used in part to repay pre-existing loan financing lines and repurchase facilities. We have sponsored and participated in securitization transactions with other entities that are managed by Angel Oak, and may continue to do so in the future, along with sponsoring sole securitization transactions.

We believe these identified sources of financing will be adequate for purposes of meeting our short‑term (within one year) and our longer‑term liquidity needs. We cannot predict with certainty the specific transactions we will undertake to generate sufficient liquidity to meet our obligations as they come due. We will adjust our plans as appropriate in response to changes in our expectations and any potential changes in market conditions.

52

Description of Existing Financing Arrangements

As of September 30, 2024, we were a party to three warehouse loan financing lines, which permitted borrowings in an aggregate amount of up to $1.1 billion. During the quarter ended September 30, 2024, we renewed our loan financing facility with Multinational Bank 1 in accordance with the mechanism for six-month renewal periods. Subsequent to the end of the quarter, we (i) amended our loan financing facility with Global Investment Bank 2 to, among other changes, reduce the interest rate pricing spread to a range from 1.75% to 3.35% and (ii) amended our loan financing facility with Global Investment Bank 3 to, among other changes, extend the termination date to (a) November 1, 2025; (b) reduce the interest rate pricing spread to a range from 1.90% to 4.75% based on collateral type, loan status, dwell time and other factors; and (c) eliminate the 20 basis point index spread adjustment. Borrowings under warehouse loan financing lines (in general, each a “loan financing facility”) may be used to purchase whole loans for securitization or loans purchased for long‑term investment purposes.

Our financing facilities are generally subject to limits on borrowings related to specific asset pools (“advance rates”) and other restrictive covenants, as is usual and customary. As of September 30, 2024, the advance rates (when required) of our three active lenders ranged from 65% to 92%, depending on the asset type and loan delinquency status. Our most restrictive covenants (when covenants are required by any of our three active lenders) included (1) our minimum tangible net worth must not (i) decline 20% or more in the previous 30 days, 25% or more in the previous 90 days, or 35% or more in the previous year, or (ii) fall below $200.0 million of tangible net worth as of September 30, 2022 plus 50% of any capital contribution made or raised after September 30, 2022; (2) our minimum liquidity must not fall below the greatest of (i) the product of 5% and the aggregate repurchase price for a specific loan financing facility as of such date of determination, (ii) $10.0 million and (iii) any other amount of liquidity that we have covenanted to maintain in any other note, indenture, loan agreement, guaranty, swap agreement or any other contract, agreement or transaction (including, without limitation, any repurchase agreement, loan and security agreement, or similar credit facility or agreement for borrowed funds); and (3) the maximum ratio of our and our subsidiaries’ total indebtedness to tangible net worth must not be greater than 5:1. Our minimum liquidity requirement as of September 30, 2024 was $10.0 million.

A description of each loan financing facility in place during the quarter ended September 30, 2024 is set forth as follows:

Multinational Bank 1 Loan Financing Facility. On April 13, 2022, we and two of our subsidiaries entered into a master repurchase agreement with a multinational bank (“Multinational Bank 1”). Our subsidiaries are each considered a “Seller” under this agreement. From time to time and pursuant to the agreement, either of our subsidiaries may sell to Multinational Bank 1, and later repurchase, up to $600.0 million aggregate borrowings on mortgage loans.

Pursuant to the terms of the master repurchase agreement, the agreement may be renewed every three months for a maximum six-month term. As of September 30, 2024, the termination date of the master repurchase agreement was March 25, 2025.

The amount expected to be paid by Multinational Bank 1 for each eligible mortgage loan is based on an advance rate as a percentage of either the outstanding principal balance of the mortgage loan or the market value of the mortgage loan, whichever is less. Pursuant to the agreement, Multinational Bank 1 retains the right to determine the market value of the mortgage loans in its sole commercially reasonable discretion. The loan financing line is marked‑to‑market. Additionally, Multinational Bank 1 is under no obligation to purchase the eligible mortgage loans we offer to sell to them. The interest rate on any outstanding balance under the master repurchase agreement that the applicable subsidiary is required to pay Multinational Bank 1 is generally in line with other similar agreements that the Company or one or more of its subsidiaries has entered into, where the interest rate is equal to the sum of (1) a pricing spread generally ranging from 1.75% to 2.10% and (2) the average SOFR for each U.S. Government Securities Business Day (as defined in the master repurchase agreement) until two U.S. Government Securities Business Days prior to the date the applicable loan is repurchased by the applicable subsidiary.

The obligations of the subsidiaries under the master repurchase agreement are guaranteed by the Company pursuant to a guaranty executed contemporaneously with the master repurchase agreement. In addition, and similar to other repurchase agreements that the Company has entered into, the Company is subject to various financial and other covenants, including those relating to (1) maintenance of a minimum tangible net worth; (2) a maximum ratio of indebtedness to tangible net worth; and (3) minimum liquidity.

The agreement contains margin call provisions that provide Multinational Bank 1 with certain rights in the event of a decline in the market value of the purchased mortgage loans. Under these provisions, Multinational Bank 1 may require us or our subsidiaries to transfer cash sufficient to eliminate any margin deficit resulting from such a decline.

In addition, the agreement contains events of default (subject to certain materiality thresholds and grace periods), including payment defaults, breaches of covenants and/or certain representations and warranties, cross‑defaults, bankruptcy or insolvency proceedings and other events of default customary for this type of transaction. The remedies for such events of default are also customary for this type of transaction and include the acceleration of the principal amount outstanding under the agreement and Multinational Bank 1’s right to liquidate the mortgage loans then subject to the agreement.

We and our subsidiaries are also required to pay certain customary fees to Multinational Bank 1 and to reimburse Multinational Bank 1 for certain costs and expenses incurred in connection with its structuring, management, and ongoing administration of the master repurchase agreement.

Global Investment Bank 2 Loan Financing Facility. On March 28, 2024, two of our subsidiaries entered into a master repurchase agreement with a global investment bank (“Global Investment Bank 2”), replacing the existing master repurchase agreement with Global

53

Investment Bank 2 entered into on February 13, 2020. Our two subsidiaries are each considered a “Seller” under this agreement. Pursuant to the agreement, one of our subsidiaries may sell to Global Investment Bank 2, and later repurchase, up to $250.0 million aggregate borrowings on mortgage loans. The agreement is set to terminate on March 27, 2026, unless terminated earlier pursuant to the terms of the agreement.

The principal amount paid by Global Investment Bank 2 for each mortgage loan is based on a percentage of the market value, cost‑basis value, or unpaid principal balance of the mortgage loan (depending on the type of loan and certain other factors and subject to certain other adjustments). Pursuant to the agreement, Global Investment Bank 2 retains the right to determine the market value of the mortgage loan collateral in its sole good faith discretion. Additionally, Global Investment Bank 2 is under no obligation to purchase the eligible mortgage loans we offer to sell to them. Upon our or our subsidiary’s repurchase of the mortgage loan, our subsidiaries are required to repay Global Investment Bank 2 the principal amount related to such mortgage loan plus accrued and unpaid interest at a rate based on the sum of (1) the greater of (A) the greater of (i) 0.00% and (ii) Term SOFR (which is defined as the forward-looking term rate based on the Secured Overnight Financing Rate for a corresponding tenor of one month) and (B) a pricing spread generally ranging from, as of October 25, 2024, 1.75% to 3.35%.

The obligations of the subsidiaries under the master repurchase agreement are guaranteed by the Company pursuant to a guaranty executed contemporaneously with the master repurchase agreement. In addition, and similar to other repurchase agreements that the Company has entered into, the Company is subject to various financial and other covenants, including those relating to (1) maintenance of a minimum tangible net worth; (2) a maximum ratio of indebtedness to tangible net worth; and (3) minimum liquidity.

The agreement contains margin call provisions that provide Global Investment Bank 2 with certain rights in the event of a decline in the market value or cost‑basis value of the purchased mortgage loans. Under these provisions, Global Investment Bank 2 may require us or our subsidiary to transfer cash sufficient to eliminate any margin deficit resulting from such a decline.

In addition, the agreement contains events of default (subject to certain materiality thresholds and grace periods), including payment defaults, breaches of covenants and/or certain representations and warranties, cross‑defaults, bankruptcy or insolvency proceedings and other events of default customary for this type of transaction. The remedies for such events of default are also customary for this type of transaction and include the acceleration of the principal amount outstanding under the agreement and Global Investment Bank 2’s right to liquidate the mortgage loans then subject to the agreement.

We and our subsidiary are also required to pay certain customary fees to Global Investment Bank 2 and to reimburse Global Investment Bank 2 for certain costs and expenses incurred in connection with its structuring, management and ongoing administration of the agreement.

Global Investment Bank 3 Loan Financing Facility. On October 24, 2018, two of our subsidiaries entered into a master repurchase agreement with a global investment bank (“Global Investment Bank 3”) for which we serve as guarantor of our subsidiaries’ obligations. Our subsidiaries are each considered a “Seller” under this agreement. Pursuant to the initial agreement, our subsidiaries could sell to Global Investment Bank 3, and later repurchase, up to $200.0 million aggregate borrowings on mortgage loans, although Global Investment Bank 3 was under no obligation to purchase the loans our subsidiaries offered to sell to them.

On January 1, 2022, the facility was amended to transition the reference rate from a LIBOR-based index to Compound SOFR. Compound SOFR is determined on a one-month basis and is defined as a daily rate as determined by Global Investment Bank 3 to be the “USD-SOFR-Compound” rate as defined in the International Swaps and Derivatives Association, Inc. definitions.

On November 7, 2023, the facility’s termination date was extended to November 7, 2024. In addition, the base interest rate spread was reduced to 1.80% plus a 0.20% index spread adjustment. The advance rate for performing non-seasoned loans was increased to 85%.

On November 1, 2024, the facility’s termination date was extended to November 1, 2025. In addition, the base interest rate spread was reduced to a range from 1.90% to 4.75% and the index spread adjustment of 0.20% was eliminated.

The loan financing line is marked-to-market at fair value, where Global Investment Bank 3 retains the right to determine the market value of the mortgage loan collateral in its sole and good faith discretion and in a commercially reasonable manner and is under no obligation to purchase the eligible mortgage loans we offered to sell to them. Further, the principal amount paid by Global Investment Bank 3 for each eligible mortgage loan is based on a percentage of the outstanding principal balance of the mortgage loan or the market value of the mortgage loan, whichever is less.

The Agreement contains margin call provisions that provide Global Investment Bank 3 with certain rights in the event of a decline in the market value of the purchased mortgage loans. Under those provisions, Global Investment Bank 3 could require us or our subsidiaries to transfer cash sufficient to eliminate any margin deficit resulting from such a decline.

The agreement requires us to maintain various financial and other customary covenants. The agreement also sets forth events of default (subject to certain materiality thresholds and grace periods), including payment defaults, breaches of covenants and/or certain representations and warranties, cross‑defaults, bankruptcy or insolvency proceedings and other events of default customary for this type of transaction. The remedies for such events of default are also customary for this type of transaction and include the acceleration of the principal amount outstanding under the agreement and Global Investment Bank 3’s right to liquidate the mortgage loans then subject to the agreement.

54

We and our subsidiaries are also required to pay certain customary fees to Global Investment Bank 3 and to reimburse Global Investment Bank 3 for certain costs and expenses incurred in connection with its structuring, management, and ongoing administration of the agreement.

Institutional Investors A and B Static Loan Pool Financing. On October 4, 2022, the Company and a subsidiary entered into two separate master repurchase facilities with two affiliates of an institutional investor (“Institutional Investors A and B”) regarding a specific pool of whole loans with financing of approximately $168.7 million on approximately $239.3 million of unpaid principal balance. The Company repaid these financing facilities in full on January 4, 2023, at which time the facilities were terminated pursuant to their terms.

Regional Bank 1 Loan Financing Facility. On December 21, 2018, we and one of our subsidiaries entered into a master repurchase agreement with a regional bank (“Regional Bank 1”). This financing facility was substantially unused, and expired by its terms on March 16, 2023.

The following table sets forth the details of our loan financing facilities as of each of September 30, 2024 and December 31, 2023:

Interest Rate Pricing Spread

Drawn Amount

Note Payable

Base Interest Rate

September 30, 2024

December 31, 2023

($ in thousands)

Multinational Bank 1 (1)

Average Daily SOFR

1.75% - 2.10%

$

292,060

$

206,183

Global Investment Bank 2 (2)

1 month Term SOFR

2.10% - 3.45%

—

—

Global Investment Bank 3 (3)

Compound SOFR

2.00% - 4.50%

40,982

84,427

Institutional Investors A and B (4)

1 month Term SOFR

3.50%

N/A

—

Regional Bank 1 (5)

1 month SOFR

2.50% - 3.50%

N/A

—

Total

$

333,042

$

290,610

(1) On September 25, 2024, this financing facility was extended through March 25, 2025 in accordance with the terms of the agreement, which contemplates six-month renewals.

(2) On March 28, 2024 the amended and restated Master Repurchase Agreement was terminated and replaced with a new $250 million Master Repurchase Agreement which has a termination date of March 27, 2026. On October 25, 2024, this facility was amended, reducing the interest rate pricing spread to a range from 1.75% to 3.35%, based on loan status, dwell time and other factors. Prior to this extension the interest rate pricing spread ranged from 2.10% to 3.35%.

(3) On November 1, 2024, this facility was amended to (i) reduce the interest rate pricing spread to a range from 1.90% to 4.75%, based on loan status, dwell time and other factors, (ii) eliminate the 20 basis point index spread adjustment, and (iii) extend the facility’s termination date to November 1, 2025.

(4) These agreements expired by their terms on January 4, 2023.

(5) This agreement expired by its terms on March 16, 2023.

The following table sets forth the total unused borrowing capacity of each loan financing facility as of September 30, 2024:

Note Payable

Borrowing Capacity

Balance Outstanding

Available Financing

(in thousands)

Multinational Bank 1

$

600,000

$

292,060

$

307,940

Global Investment Bank 2

250,000

—

250,000

Global Investment Bank 3

200,000

40,982

159,018

Total

$

1,050,000

$

333,042

$

716,958

Although available financing is uncommitted for each of our financing facilities, the Company’s unused borrowing capacity is available if it has eligible collateral to pledge and meets other borrowing conditions as set forth in the applicable agreements.

Short‑Term Repurchase Facilities. In addition to our existing loan financing lines, we employ short‑term repurchase facilities to borrow against U.S. Treasury securities, securities issued by AOMT, Angel Oak’s securitization platform, and other securities we may acquire in accordance with our investment guidelines. The following table sets forth certain characteristics of our short-term repurchase facilities as of September 30, 2024 and December 31, 2023:

55

September 30, 2024

Repurchase Agreements

Amount Outstanding

Weighted Average Interest Rate

Weighted Average Remaining Maturity (Days)

($ in thousands)

U.S. Treasury securities

$

49,712

4.90

%

3

RMBS (1)

$

53,164

6.35

%

18

Total

$

102,876

5.65

%

11

December 31, 2023

Repurchase Agreements

Amount Outstanding

Weighted Average Interest Rate

Weighted Average Remaining Maturity (Days)

($ in thousands)

U.S. Treasury securities

$

149,013

5.57

%

10

RMBS (1)

44,643

7.04

%

16

Total

$

193,656

5.91

%

11

(1) A portion of repurchase debt outstanding as of both September 30, 2024 and December 31, 2023 includes borrowings against retained bonds received from on-balance sheet securitizations (i.e., consolidated VIEs).

The repurchase debt against the U.S. Treasury securities was repaid in full upon the maturity of the U.S. Treasury securities.

The following table presents the amount of collateralized borrowings outstanding under repurchase facilities as of the end of each quarter, the average amount of collateralized borrowings outstanding under repurchase facilities during the quarter and the highest balance of any month end during the quarter:

Quarter End

Quarter End Balance

Average Balance in Quarter

Highest Month-End Balance in Quarter

(in thousands)

Q4 2022

52,544

56,426

63,357

Q1 2023

442,214

180,165

442,214

Q2 2023

340,701

101,731

340,701

Q3 2023

188,101

87,279

188,101

Q4 2023

193,656

62,536

193,656

Q1 2024

193,493

69,254

193,493

Q2 2024

201,051

66,804

201,051

Q3 2024

102,876

57,842

102,876

We utilize short‑term repurchase facilities on our RMBS portfolio and to finance assets for REIT asset test purposes. Over time, the need to purchase securities for REIT asset test purposes will be reduced as we obtain and participate in additional securitizations and acquire assets directly for investment purposes. We will continue to use repurchase facilities on our RMBS portfolio to add additional leverage which increases the yield on those assets. Our use of repurchase facilities is generally highest at the end of any particular quarter, as shown in the table above, where the quarter-end balance and the highest month-end balance in each quarter are generally equivalent.

Securitization Transactions

Subsequent to the end of the quarter, in October 2024, we were the sole participant in asecuritization transaction of a pool of residential mortgage loans, secured exclusively by first liens on one‑to‑four family residential properties. In the transaction, AOMT 2024-10 issued approximately $316.8 million in face value of bonds. We used the proceeds of the securitization transaction to repay outstanding debt of approximately $260.4 million and retained cash of $39.4 million, which was used for new loan purchases and operational purposes.

We are the sole member of the Depositor and also own and hold the call rights on the XS tranche of bonds, which is the “controlling class” of the bonds. We will consolidate the AOMT 2024-10 securitization on our consolidated balance sheet, maintaining the residential mortgage loans held in the securitization trust and the related financing obligation thereto on our consolidated balance sheets in future reporting periods.

56

In June 2024, we and other affiliated entities participated in asecuritization transaction of a pool of residential mortgage loans, secured primarily by first liens on one‑to‑four family residential properties. In the transaction, AOMT 2024-6 issued approximately $479.6 million in face value of bonds. Our proportionate share of 4.51% of the retained bonds and investments in MOAs was approximately $2.5 million, including a retained discount on issuance of approximately $0.8 million. We used the proceeds of the securitization transaction to repay outstanding debt of approximately $15.8 million and retained cash of $1.8 million, which was used for operational purposes.

We derecognized the mortgage loans sold in AOMT 2024-6 and recorded an investment in majority-owned affiliates located within “other assets” on our consolidated balance sheet as of September 30, 2024.

In April 2024, we were the sole participant in asecuritization transaction of a pool of residential mortgage loans, secured exclusively by first liens on one‑to‑four family residential properties. In the transaction, AOMT 2024-4 issued approximately $299.8 million in face value of bonds. We used the proceeds of the securitization transaction to repay outstanding debt of approximately $235.9 million and retained cash of $39.1 million, which was used for new loan purchases and operational purposes.

We are the sole member of the Depositor and also own and hold the call rights on the XS tranche of bonds, which is the “controlling class” of the bonds. We have consolidated the AOMT 2024-4 securitization on our consolidated balance sheet, maintaining the residential mortgage loans held in the securitization trust and the related financing obligation thereto on our consolidated balance sheets as of September 30, 2024.

In March 2024, we and other affiliated entities participated in asecuritization transaction of a pool of residential mortgage loans, secured primarily by first liens on one‑to‑four family residential properties. In the transaction, AOMT 2024-3 issued approximately $439.6 million in face value of bonds. Our proportionate share of 10.98% of the retained bonds and investments in MOAs was approximately $4.8 million, including a retained discount on issuance of approximately $1.6 million. We used the proceeds of the securitization transaction to repay outstanding debt of approximately $35.9 million and retained cash of $4.6 million, which was used for operational purposes.

We derecognized the mortgage loans sold in AOMT 2024-3 and recorded an investment in majority-owned affiliates located within “other assets” on our consolidated balance sheet as of September 30, 2024.

In December 2023, we and other affiliated entities participated in asecuritization transaction of a pool of residential mortgage loans, secured primarily by first liens on one‑to‑four family residential properties. In the transaction, AOMT 2023-7 issued approximately $397.2 million in face value of bonds. Our proportionate share of 10.36% of the retained bonds and investments in MOAs was approximately $3.5 million, including a retained discount on issuance of approximately $1.4 million. We used the proceeds of the securitization transaction to repay outstanding debt of approximately $30.9 million and retained cash of $3.6 million, which was used for operational purposes.

We derecognized the mortgage loans sold in AOMT 2023-7 and recorded an investment in majority-owned affiliates located within “other assets” on our consolidated balance sheet as of September 30, 2024.

In August 2023, we and other affiliated entities participated in asecuritization transaction of a pool of residential mortgage loans, secured primarily by first liens on one‑to‑four family residential properties. In the transaction, AOMT 2023-5 issued approximately $260.6 million in face value of bonds. Our proportionate share of 34.42% of the retained bonds and investments in MOAs was approximately $7.7 million, including a retained discount on issuance of approximately $2.7 million. We used the proceeds of the securitization transaction to repay outstanding debt of approximately $63.4 million and retained cash of $10.7 million, which was used for operational purposes.

We derecognized the mortgage loans sold in AOMT 2023-5 and recorded an investment in majority-owned affiliates located within “other assets” on our consolidated balance sheet as of September 30, 2024.