我们设计、制造、推广和销售多个品牌的奢侈品,包括ZEGNA和Thom Browne。根据与雅诗兰黛公司签订的长期许可协议,我们还经营TOM FORD FASHION(“TFF”)业务。我们的销售额和实现优质定价的能力取决于我们品牌的认知、认可度和声誉,而这反过来又取决于产品设计、产品和客户服务的独特性和质量、我们商店的形象以及我们的特许经营商和其他批发客户的形象、我们广告和传播活动的成功以及我们的总体企业形象等因素。

收购新业务还可能使我们面临与所收购业务具体相关的其他风险。例如,根据TFI收购的安排(并以收购完成为准),Tom Ford International创始人兼首席执行官Tom Ford先生一直担任该品牌的创意远见者,直至2023年底。他在执掌TOM FORD品牌多年后离职最终可能会对TOM FORD FASHION业务产生重大不利影响,从而对我们的运营业绩和财务状况产生重大不利影响。

在批发渠道中,我们将产品销售给加盟商、专卖店、百货商店和在线零售商。在截至2023年12月31日的一年中,杰尼亚品牌产品批发渠道、Thom Browne和Tom Ford Fashion(在完成对TFI的收购后)的收入达到458.4欧元(占同期我们综合收入的24%)。终止或失去与我们的主要批发客户的现有商业关系,未能以经济上有利的条款(或根本没有)发展新的商业关系,或批发渠道收入大幅下降,可能会对我们的业务、经营业绩和财务状况产生重大不利影响。此外,任何非我们直接经营的零售商或我们的本地合作伙伴未能以与我们品牌的形象和声望一致的方式或按照任何商定的合同承诺(包括销售价格)来管理其门店,或在线零售商未能遵守消费者保护法或提供准确的产品描述,都可能损害我们品牌的竞争地位和形象,对我们的业务、运营结果和财务状况产生潜在的重大不利影响。请参阅“-我们的业务取决于我们品牌的认知度、诚信和声誉.”

该集团是一家全球奢侈品公司,是高端男装业务的领导者,并因其独特的纺织和制造平台而获得国际认可。传统、意大利工艺、质量和创新是其三个互补品牌的关键要素:ZEGNA、Thom Browne和TOM FORD FASHION。通过他们,我们的影响力扩大到不同的社区,从同名品牌ZEGNA的绝对标志性奢侈品,到Thom Browne的现代剪裁,再到TOM FORD FASHION的奢华魅力。得益于Thom Browne和TOM FORD FASHION,该集团还在奢侈女装和皮革制品领域发挥着重要且不断增长的作用。

自LanFisicio Ermenegildo Zegna e Figli S.p.A.成立以来(“Laniciio”或“Laniciio Ermenegildo Zegna”)在上个世纪初,Zegna一直是男装品质、风格和创新的代名词。ZEGNA品牌和Ermenegildo Zegna集团一直如此,并且将继续如此。

奢侈男装领导力

Ermenegildo Zegna集团植根于其100多年的历史,在奢侈男装领域拥有稳固的领导地位。这一无可争议的传统,加上独特且互补的品牌组合,构成了集团的主要竞争优势。ZEGNA已从最知名的男装品牌之一发展成为男装绝对奢华休闲服领域的标志品牌,在最重要的奢华街道和购物中心拥有顶级零售网络。2018年加入Thom Browne,2023年加入TOM FORD FASHION,通过抓住独特且互补的客户群体,同时利用集团的纺织和制造专业知识,进一步加强了集团的领导地位。

虽然我们的品牌保持着自己的身份和独特的设计天赋,但集团拥有作为长期工业合作伙伴和领先奢侈品牌聚合者的技能和经验。集团的内部实验室平台和制造专业知识、由杰尼亚家族领导的精干管理团队、对全球奢侈品市场(房地产开发和零售专业知识等)的广泛了解,使集团能够为其合作伙伴的业务增加价值。这方面的一个突出例子是Thom Browne在2018年收购后的表现,收入从2018年的11700万欧元增长到2023年冲销之前的38000万欧元。同样,TOM FORD FASHION业务的加入代表着利用集团平台的进一步机会。

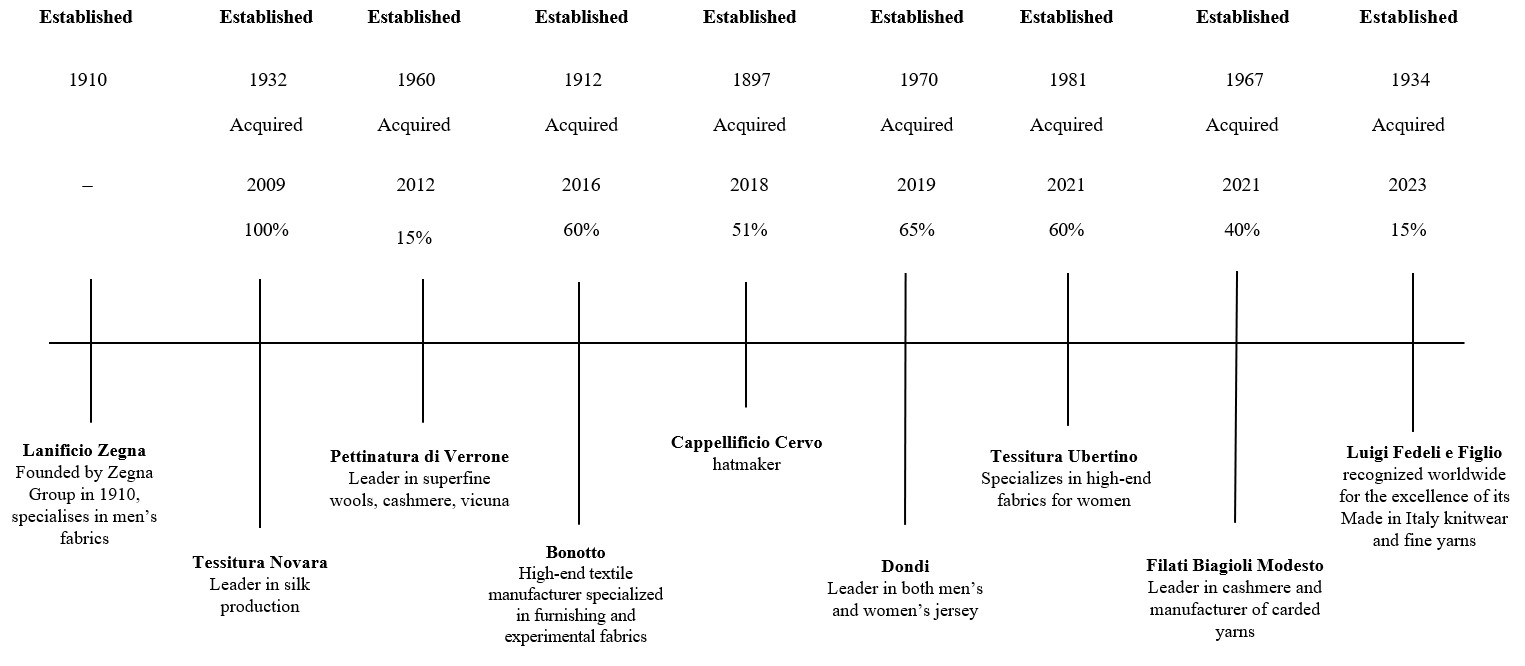

Ermenegildo Zegna Group设计、生产、销售和分销ZEGNA、Thom Browne和TOM FORD FASHION品牌的豪华男装、鞋类、皮革制品和其他配饰,Thom Browne和TOM FORD FASHION品牌的豪华女装以及Thom Browne品牌的童装。这三个品牌还为特定产品类别选择了第三方许可协议。该集团凭借其纺织品和针织品设计、制造和分销业务覆盖整个价值链(品牌包括LanFisicio Ermenegildo Zegna、Dondi、Bonotto、Tessitura di Novara、Tessitura Ubertino以及少数族裔Filati Biagioli Modesto和Luigi Fedeli e Figlio)。收购了历史悠久的意大利公司,每家公司都专门从事自己的产品领域,使集团多年来建立了一个真正的豪华纺织实验室,生产最高质量的面料并保障其意大利供应链的独特性。

Tom Ford Fashion分部对应于TOM FORD FASHION品牌的时尚业务,该品牌在TFI收购后成为本集团的一部分,代表本集团的一个新的运营和报告分部。Tom Ford Fashion部门包括与TOM Ford Fashion相关的所有活动,从系列创作和开发到营销,再到生产,以及零售和批发分销。

为测量而制作。 我们的豪华休闲服和正装产品还包括Made to Scale(Su Misura)服务,顾客可以在与风格顾问会面后,根据自己选择的面料、风格和饰面订购定制服装。这项服务不仅适用于西装,还适用于外衣、衬衫、裤子、针织衫、牛仔布和针织衫。我们的定制服务将定制提升到更高的水平,包括将独特作品组合在一起的完整体验,从草图和设计到面料的选择。每件单品都是由米兰和巴黎工作室的裁缝师使用历史悠久的剪裁技术专门为客户制作的。

截至2023年、2022年和2021年12月31日止年度,纺织产品线在冲销后产生的收入分别为150,986千欧元、136,769千欧元和102,244千欧元,占冲销后收入的7.9%、9.2%和7.9%。该纺织品产品线从事Laniciio Ermenegildo Zegna、Dondi、Bonotto、Tessitura di Novara、Tessitura Ubertino品牌的豪华面料的设计、制造和销售。我们相信,服装中使用的纺织品的卓越质量是集团多年来取得成功的主要原因之一。该集团还持有Filati Biagioli Modesto的少数股权(40%),并于最近收购了Luigi Fedeli e Figlio S.r.l.的15%股权,世界著名的意大利优质针织衫和纱线制造商。

季节性系列将在米兰时装周期间通过精致、优雅和现代的时装秀亮相,使品牌能够将自己定位为真正奢侈品的巅峰,创造引人入胜的内容,尽情享受和娱乐顶级客户和合作伙伴,并制定精心策划的VIP与会者名单,其中涵盖了TOM FORD FASHION的男性和女性。营销的策略重点是内容创作和增加对媒体的高度战略投资,以建立品牌的新准则--魅力、神秘的诱惑、精致的优雅--以建立知名度、客户忠诚度和品牌资产。

我们从ZZ Real Estate S.r.l.租赁集团业务运营中使用的部分房地产资产(“ZZ Real Estate”),该公司的前子公司,作为处置的一部分,于2021年11月1日分拆。此类房地产资产包括拥有制造设施的建筑物、公司办公室、展厅、仓库、土地和其他建筑物,包括我们在意大利的主要制造工厂和办事处(例如集团位于米兰的总部办事处,位于帕尔马、圣彼得罗·莫塞佐、维罗纳和奥莱焦的制造工厂,以及位于瓦尔迪拉纳的建筑的一部分,主要由我们占用)和瑞士(包括位于Stabio的办事处和位于Mendrisio的制造工厂)以及某些ZEGNA商店,即位于Sandigliano和Oleggio(意大利)以及伦敦(英国)。

我们还拥有Sagliano Micca(意大利)的Cappellificio Cervo以及Fossoli di Carpi(意大利)和Novi di Modena(意大利)的Dondi使用的某些房地产资产(制造设施、仓库和办公室)。

48

我们的制造设施目前有能力在必要时增加产量以满足更高的需求。

下表列出了与截至本报告日期我们开展业务时使用的自有房地产资产相关的信息。

位置

使用

近似平方米

意大利,Sagliano Micca,Via della Libertà 16

工厂、仓库和办公室

5,500

意大利,Fossoli di Carpi,意大利,via Budrione Migliarina 2/A

2023年9月5日,Ermenegildo Zegna集团和Prada集团完成了之前宣布的对Luigi Fedeli e Figlio S.r.l. 30%权益的收购,世界知名的意大利优质针织衫和纱线制造商,每个集团收购了该公司15%的股份。本集团支付了470万欧元的对价,收购了公司15%的股份。

2023年7月1日,集团收购了韩国Thom Browne业务,并开始在韩国直接运营Thom Browne业务,其网络由17家门店组成。该业务目前由Thom Browne Korea Ltd.全资拥有,一家新成立的全资子公司,将在前特许经营合作伙伴的外部支持下运营。本集团支付现金对价7,991千欧元,并确认递延对价18,583千欧元,于2023年12月31日为18,991千欧元,其中9,302千欧元预计将于2024年支付,分类为流动负债和9,预计将于2025年支付689千美元,并被归类为非流动负债。

2023年3月31日,本集团完成收购加拿大技术型越野鞋公司Norda Run Inc. 25%的权益。对价为710万美元,可选择在接下来的九年内逐步增持股份。豪华户外空间仍然是集团的重点领域,Norda Run使用地球上最好的材料生产世界上性能最好的全天候鞋类,完全符合集团用最好的材料创造最好的产品的价值观。该协议确保了通过强大的工商合作伙伴关系加速品牌增长的可能性。

2021年11月1日,本集团通过意大利法律下的法定分拆,将其若干业务出售给一家由其现有股东拥有的新公司,该新公司由(I)其房地产业务的现有股东拥有,该新公司包括本集团的前子公司EZ Real Estate,该子公司直接和间接持有本集团以前拥有的几乎所有房地产资产,以及Lanificio以前拥有的若干财产,包括Lanificio位于Valdiana的部分工业建筑和Lanificio的水电站,及(Ii)其于Elah Dufour S.p.A.的10%股权((I)及(Ii)统称为“分拆”)。2021年1月14日,集团出售了其在Agnona S.r.l的70%股权。(“阿格诺纳”)给了一个相关方,以供审议1欧,因此,阿格诺纳从2021年初开始解除合并。本集团其后于2021年9月及10月分两批出售Agnona剩余30%股权,总代价为50欧元万(出售Agnona股权连同分拆称为“性情,上述剥离的业务统称为已处置的业务”).

EZ Real Estate直接或间接拥有的大部分房地产已租赁给本集团,并将继续出租给本集团,包括存放本集团在意大利的制造设施、公司办公室、展厅、仓库、土地和其他建筑物的建筑物(包括位于米兰的总部、位于Parma、San Pietro Mosezzo、Verrone和Oleggio的制造设施,以及位于Valdiana的部分建筑物)和位于瑞士的部分建筑物(包括位于Stabio的办公室和位于Mendrisio的制造工厂),以及主要位于Sandigliano和Oleggio(意大利)和伦敦(英国)的若干Zegna门店。出售后,本集团继续根据相关租赁协议向EZ Real Estate或其附属公司支付租金,2023年和2022年的租金总额分别为12,268,000欧元和622.7欧元万。此外,已按市场条件作出适当安排,以确保构成处置一部分的Lanificio集团的房地产资产继续使用。

本集团寻求透过订立衍生合约(一般为远期出售外币合约)以预先厘定汇率或于未来日期厘定预定的汇率范围,以减轻其货币风险的影响。就杰尼亚及Tom Ford Fashion分部而言,本集团最初以欧元厘定销售价格,然后根据管理层根据合理预期及假设选定的汇率,厘定以其他货币计算的相应价格。远期销售合约乃根据估计收入及根据客户计划付款日期设定对冲合约到期日,而订立以特定货币计算的季节性价目表,以减轻实际汇率与管理层使用的预期汇率之间的差异所造成的影响。根据汇率的实际发展,可能会在相关季节进行额外的对冲交易。本集团继续在Thom Browne部门实施类似的政策,该部门在向国际市场扩张时更容易受到汇率影响。有关本集团所面对的市场风险的资料,见附注35--关于金融风险的定性和定量信息在本报告所列合并财务报表中列报。

截至2023年12月31日止年度收入为190454.9万欧元,增加41170.9万欧元,增幅+27.6%(按固定汇率计算+29.7%;有机增长+19.3%),而截至2022年12月31日止年度为149284万欧元,受Zegna和Thom Browne部门两位数增长的推动(包括以固定货币和有机增长为基础),以及Tom Ford Fashion部门在4月28日完成TFI收购后贡献的收入,2023.

(i)增加7663.1万欧元或+9.0% ZEGNA品牌产品(+4.1%固定汇率和有机增长),主要受以下推动:(a)鞋类持续积极表现和豪华休闲服的稳定增长,以及我们的裁缝和量身定制业务的反弹,特别是在美国和欧洲、中东和非洲,由于2021年受到COVID-19相关限制的影响,以及(b)作为ZEGNA One Brand新战略的一部分,从推出2022年秋冬系列开始,价格重新定位和价格上涨的影响;

(iii)增加122,666万欧元或+41.6%(按固定汇率计算+40.4%;受美国推动,北美地区有机增长+11.4%,包括2023年4月28日TFI收购完成后Tom Ford Fashion部门12家直营店的贡献,以及ZEGNA DT渠道两位数的收入增长,部分被上述批发交付转变以及纽约萨克斯第五大道商店从批发转变为DT的影响所抵消;以及

销售成本的增加主要归因于(i)TOM FORD FASHION的影响,该公司于2023年4月28日通过TFI收购,包括收购会计法对业务收购的影响,包括14欧元,368 000美元与收购后出售的所收购TFI库存公允价值的收购价格上涨以及1欧元,18.3万与订单积压有关,以及(ii)ZEGNA品牌产品、Thom Browne和Textile的销量增加。

毛利润占收入的百分比从截至2022年12月31日止年度的62.2%增加至截至2023年12月31日止年度的64.3%,主要原因是(i)与批发销售相比,DTC销售的比例更高(与批发销售相比,DTC销售的利润率更高,占截至12月31日的年度总销售额的66.4%,2023年,而截至2022年12月31日的一年为61.5%),(ii)作为ZEGNA One Brand战略的一部分,价格上涨、价格重新定位和季末销售减少的影响,该战略始于2022年秋冬系列的推出,去年(iii)供应链中固定成本的吸收率更高,以及(iv)根据ZEGNA One Brand战略,与季节性系列相比,Essentials系列的销售比例更高,这导致对缓慢流动和过时库存的拨备按比例减少。

毛利润占收入的百分比从截至2021年12月31日的年度的61.6%增加到截至2022年12月31日的年度的62.2%,主要原因是:(I)供应链中固定成本的吸收增加,原因是销售量更高,(Ii)作为新的杰尼亚One Brand战略的一部分,价格上涨、价格调整和季末销售减少的影响,从而增加了收入;(Iii)根据Jegna One Brand战略,Essentials系列的销售比例高于季节性系列,这导致缓慢流动和陈旧库存的拨备比例较低,但被(Iv)DTC销售与批发销售相比比例降低所部分抵消(DTC销售的利润率高于批发销售,占截至2022年12月31日的年度总销售额的61.5%,而截至12月31日的年度为65.9%,2021年)由于新冠肺炎相关限制的影响,导致大中国地区的某些DOS关闭。

截至2023年12月31日的年度的财务支出为6812.1欧元万,与截至2022年12月31日的年度的5434.6欧元万相比,增加了1377.5欧元万或+25.3%。财务支出增加的主要原因是:(1)由于2023年第一季行使和赎回权证,权证负债亏损2173.8欧元万(2023年亏损2290.9欧元万,2022年亏损117.1欧元万)(见附注28--其他流动和非流动金融负债(Ii)银行贷款利息和透支利息增加857.6万,以及(Iii)租赁负债利息和财务费用增加714.8万(包括与Tom Ford Fashion有关的5,632,000欧元),但因(Iv)重新计量Thom Browne非控制权益认沽期权负债的公允价值亏损1142.6欧元(2023年收益,而2022年亏损1142.6欧元万)而部分抵销,(V)本集团持有的证券亏损901.4欧元万,受金融市场表现的推动(2023年亏损441.2欧元万,而2022年亏损1342.6欧元万),以及(Vi)与对冲成本相关的496.5欧元万减少。

(ii)盈利能力的提高由以下因素推动:(a)与批发销售相比,DT销售的比例更高,(b)零售店生产力提高,包括商店合理规模的影响,(c)供应链中固定成本的吸收率更高,(d)价格上涨和季末销售减少,作为ZEGNA One Brand战略的一部分,和(e)与季节性系列相比,Essentials系列的销售比例更高,并且对缓慢流动和过时库存的拨备相应减少;

(ii)支付658万欧元收购Norda Run Inc. 25%权益(“Norda”),465.6万欧元,收购Luigi Fedeli e Figlio S.r.l. 15%的权益并向Filati Biagioli Modesto S.p.A.注资450万欧元。有关这些事务的更多信息,请参阅 注17 -使用权益法核算的投资 包含在本年度报告其他地方的合并财务报表中,表格20-F;

自2013年以来,他一直是意大利时装全国商会(Camera Nazionale della Moda Italiana)战略委员会成员和顾问,并一直是美国和意大利委员会的活跃成员。2011年,杰尼亚先生被意大利共和国总统提名为Cavaliere del Lavoro,并于2016年获得莱昂纳多奖,这是一个著名奖项,颁发给一位在全球范围内有意义地提升意大利形象的意大利领导人。

Ermenegildo Zegna di Monte Rubello先生和Anna Zegna di Monte Rubello女士是兄弟姐妹。

Paolo Zegna di Monte Rubello(非执行董事)

Paolo Zegna先生目前是董事会成员,并于2006年至2021年12月担任董事长。此前,他于1989年至1998年担任董事会成员,并于1998年至2006年担任联席首席执行官。

Paolo Zegna先生也是Ottubello董事会副主席和LanFisicio Ermenegildo Zegna e Figli S.p.A.董事会主席,Achill Station Pty Ltd.和Achill Land Pty Ltd.,也是Bonotto S.p.A.董事会成员,Gruppo Dondi S.p.A.和Elah Dufour S.p. A

2023年12月18日,根据忠诚度投票计划的条款,149,734,550股和5,246,800股特别投票股A分别转让给Ottubello和Ermenegildo(Gildo)Zegna di Monte Rubello。Thomubello通过持有公司已发行和发行普通股59.8%的股权(截至2024年3月23日),成为公司的控股股东。由于参与忠诚投票计划,Ottubello的投票权约为73.9%(截至2024年3月23日)。

(1)ubello是一家意大利semplice协会,其配额目前由杰尼亚家族成员持有。截至2023年12月31日,Ottubello的董事包括Ermenegildo Zegna di Monte Rubello(董事会主席)、Paolo Zegna di Monte Rubello(董事会副主席)、Anna Zegna di Monte Rubello、Angelo Zegna di Monte Rubello、Giovanni Schneider、Alessandro Andrea Trabaldo Togna、Franca Calcia和Riccardo Mulone。苏贝洛参与我们的忠诚度投票计划。

(5)Zegna先生参与我们的忠诚度投票计划。截至2024年3月23日,杰尼亚先生在杰尼亚的投票权约为3.1%。该百分比计算为(i)Ermenegildo Zegna di Monte Rubello实际拥有的普通股和Zegna特别投票权股份A的总数与(ii)截至2024年3月23日已发行和发行的250,310,263股普通股和154,981,350股Zegna特别投票权股份A的比率。

•作为本集团对Thom Browne Group和LanFisio投资的一部分而签订的看跌合同,本集团已被要求并且未来可能被要求购买Thom Browne Group和LanFisio剩余的全部或部分非控股权益。2021年7月,本集团以总代价960万欧元额外收购了Lanificio 10%的股份,随后本集团拥有Lanificio 100%的股份。2021年6月,集团以总代价3065.3万欧元额外收购了Thom Browne Group 5%的股份,随后集团拥有Thom Browne Group 90%的股份。有关Thom Browne看跌合约的更多信息,请参阅 附注28--其他流动和非流动金融负债合并财务报表。

Transactions with other related parties connected to directors and shareholders, including in connection with the Business Combination in 2021

127

•在集团风险管理活动过程中,与瑞银集团股份公司及其子公司(统称“瑞银集团股份公司”)就借款、循环信贷额度和集团持有的金融资产(主要是现金和现金等值项目以及其他证券)以及衍生品合同进行交易。UBS Group AG还代表集团向第三方提供某些财务担保。Sergio Ermotti先生于2023年4月5日被任命为瑞银集团首席执行官后,瑞银集团股份公司及其子公司有资格成为集团的关联方。

Pursuant to Dutch law and the Articles of Association, the Board or the General Meeting at the proposal of the Board will be allowed to resolve upon interim distributions on Ordinary Shares. For this purpose, the Board must prepare an interim statement of assets and liabilities. Such interim statement shall show our financial position not earlier than on the first day of the third month before the month in which the resolution to make the interim distribution is announced. An interim dividend can only be paid if (i) an interim statement of assets and liabilities is drawn up showing that the funds available for distribution are sufficient, and (ii) our shareholders’ equity exceeds the sum of the paid-up and called-up share capital and any reserves to be maintained by Dutch law or the Articles of Association. Interim distributions will be made in cash, in kind or in the form of Ordinary Shares.

Since Ermenegildo Zegna N.V. is a holding company and its operations are carried out through its subsidiaries, the Company’s ability to pay dividends will primarily depend on the ability of its subsidiaries to generate earnings and to provide it with the necessary financial resources.

The Special Voting Shares are not listed and are transferable only in very limited circumstances (including, among other things, transfers to certain affiliates or to relatives through succession, donation or other transfers, provided that the corresponding Ordinary Shares registered in the Loyalty Register are also transferred to such party, or transfers with the approval of the Board). In particular, no shareholder will be allowed to, directly or indirectly: (a) sell, dispose of, trade or transfer any Special Voting Shares or otherwise grant any right or interest in any Special Voting Share, other than as permitted pursuant to the Articles of Association or the Terms and Conditions of the Special Voting Shares; or (b) establish or permit to establish any pledge, lien, fixed or floating charge or other encumbrance over any Special Voting Share or any interest in any Special Voting Share.

The purpose of the loyalty voting structure is to grant long-term shareholders extra voting rights by means of granting Special Voting Shares, without entitling such shareholders to any economic rights, other than those pertaining to the Ordinary Shares. However, under Dutch law, the Special Voting Shares cannot be totally excluded from economic entitlements. As a result, pursuant to the Articles of Association, holders of Special Voting Shares will be entitled to a minimum dividend, which is allocated to separate special voting shares dividend reserves. Any distribution out of a special voting shares dividend reserve or the partial or full release of any such reserve will require a prior proposal from the Board and a resolution of the meeting of holders of the relevant class of Special Voting Shares, and will be made exclusively to the holders of the relevant class of Special Voting Shares in proportion to the aggregate nominal value of the relevant class of their Special Voting Shares. The powers to vote upon the distribution from the special voting shares dividend reserve and the cancellation of all issued Special Voting Shares of a specific class are the only powers that are granted to the meeting of holders of Special Voting Shares of the relevant class pursuant to Articles of Association.

The Board is allowed to amend the Terms and Conditions of the Special Voting Shares, provided, however, that any material, not merely technical amendment will be subject to approval of the General Meeting, unless such amendment is required to ensure compliance with applicable laws and or stock exchange rules.

根据《荷兰民法典》第2:92A条,股东如自行持有本公司至少95%的已发行及已发行股本,可向其他股东提起诉讼,要求将其股份转让予申索人。诉讼程序在荷兰企业商会(Ondernemingskamer),并可按照《荷兰民事诉讼法典》的规定,以传票方式向每名小股东提起诉讼(Wetboek van Burgerlijke Rechtsvording)。荷兰企业商会可批准对所有少数股东的排挤请求,并将在必要时在任命一至三名专家(S)后确定为股份支付的价格,专家将就少数股东的股份支付价值向荷兰企业商会提出意见。一旦转让令在荷兰企业商会获得最终通过,收购股份的人必须将付款日期、地点和价格以书面形式通知被收购股份的持有人,而这些持有人的地址是他或她知道的。除非收购人知道所有收购人的地址,否则收购人必须在荷兰国家日报上公布。

对荷兰缔结的避免双重征税条约的任何提及均包括荷兰王国税收法规(Belastingregeling voor het Koninkrijk)、荷兰州税收法规(Belastingregeling voor het land荷兰)、荷兰和Curacao税收法规(贝拉廷雷林荷兰Curaçao)、荷兰和圣马丁税收法规(贝拉廷雷格林荷兰圣马丁岛)以及台北驻荷兰代表处与荷兰驻台北贸易投资办事处之间关于避免双重征税的协议。

根据荷兰国内法,根据荷兰法律成立的公司实体的股份和/或认购证持有人通常需要缴纳荷兰股息预扣税,税率为15%,根据1965年《荷兰股息预扣税法》(Wet op de dividendbelasting 1965)(“DWTA”)分配的股息。在特定条件下,根据荷兰法律注册成立的公司实体的股份和/或期权持有人还可能因荷兰预扣税而预扣税或扣除,税率为25.8%(Wet bronbelasting 2021;“WTA 2021”)。

合作伙伴关系(意大利语“società in nome collettivo”、“società in accomandita semplice”、“società semplici”以及CITA第5条中提到的类似意大利合作伙伴关系)

意大利不会对向意大利商业合作伙伴(例如意大利)支付的股息在源头上预扣任何意大利税 società in nome collettivo,società in accomandita semplice 以及CITA第5条中提到的类似合作伙伴关系)。只有58.14%的股息包含在业务合作伙伴报告的总体业务收入中。

正如《管理层关于财务报告内部控制的年度报告》所述,管理层将Tom Ford International LLC及其子公司(于2023年4月28日收购)的财务报告内部控制排除在其评估之外,其财务报表占本集团截至2023年12月31日及截至2023年12月31日止年度合并总资产和收入的15.7%和12.4%。因此,我们的审计不包括Tom Ford International LLC及其子公司对财务报告的内部控制。

•Audit fees are the aggregate fees charged by the Deloitte Entities for the audit of our annual consolidated financial statements, the review of our interim consolidated financial statements and attestation services that are provided in connection with statutory and regulatory filings or engagements.

•Audit-related fees are the aggregate fees charged by the Deloitte Entities for assurance and related services that are reasonably related to the performance of the audit or review of our financial statements and are not reported under “Audit Fees.” This category comprises fees for agreed upon procedures engagements and other attestation services subject to regulatory requirements.

•Tax fees are the aggregate fees charged by the Deloitte Entities for services related to tax compliance, tax advice and tax planning.

•All other fees are the aggregate fees charged by the Deloitte Entities for non-audit services rendered which are not listed above.

Audit Committee’s pre-approval policies and procedures

Our Audit Committee makes recommendations for the appointment, compensation and retention of our independent registered public accounting firm entrusted with the audit of our consolidated financial statements. Our Audit Committee has adopted a policy requiring management to obtain the Audit Committee’s approval before engaging our independent registered public accounting firm to provide any other audit or permitted non-audit services to us or our subsidiaries. Pursuant to this policy, which is designed to ensure that such engagements do not impair the independence of our independent registered public accounting firm, the Audit Committee reviews and pre-approves(if appropriate) specific audit and non-audit services in the categories Audit Services, Audit-Related Services, Tax Services, and any other services that may be performed by our independent registered public accounting firm.

ITEM 16D EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES

None.

ITEM 16E PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS

176

During the year ended December 31, 2023, no purchases of our equity securities registered pursuant to Section 12 of the Exchange Act were made by or on behalf of us or any affiliated purchaser.

ITEM 16F CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANT

Not Applicable.

ITEM 16G CORPORATE GOVERNANCE

The discussion below summarizes the significant differences between our corporate governance practices and the NYSE listing standards applicable to U.S. companies. The DCGC is based on a “comply or explain” principle, then for a discussion regarding certain ways in which our governance practices deviate from those suggested in the DCGC, please see “Item 10.B—Memorandum and Articles of Association—Certain Disclosure and Reporting Obligations of the Company.”

•NYSE listing standards generally require a majority of board members to be “independent” as determined under the NYSE listing standards. While the DCGC, in principle, requires that a majority of non-executive directors be “independent,” the definition of “independent” under the DCGC differs in its details from the corresponding definition of “independent” under the NYSE listing standards. In some cases, DCGC requirements are stricter; in other cases, the NYSE listing standards are stricter. Currently, a majority of the members of the Board are independent under the NYSE listing standards (7 out of 11 members); 5 out of the 10 non-executive directors of the Board are independent under the DCGC.

•NYSE listing standards require that when an audit committee member of a U.S. domestic listed company serves on four or more audit committees of public companies, the listed company should disclose (either on its website or in its annual proxy statement or annual report filed with the SEC) that the board of directors has determined that this simultaneous service would not impair the director’s service to the listed company. Dutch law does not require the Company to make such a determination.

•NYSE listing standards applicable to U.S. companies require that external auditors be appointed by the audit committee. The general rule under Dutch law is that external auditors are appointed by the General Meeting. In accordance with the requirements of Dutch law, the appointment and removal of our independent registered public accounting firm must be resolved upon at a General Meeting. Our Audit Committee is responsible for determining the process for selecting and determining the remuneration of the independent registered public accounting firm and oversees and evaluates the work of our independent registered public accounting firm.

•NYSE listing standards require a U.S. listed company to have a compensation committee and a nominating/corporate governance committee composed entirely of independent directors. As a foreign private issuer, we do not have to comply with this requirement, although we do have a Compensation Committee and a Governance and Sustainability Committee. The charter of our Compensation Committee states that more than half of the members of the Compensation Committee (including the chairperson) are independent under the DCGC. Currently, two out of three members of our Compensation Committee are independent both under the DCGC and under the NYSE listing standards. The charter of our Governance and Sustainability Committee states that more than half of the members of the Governance and Sustainability Committee are independent under the DCGC. Currently all three members of our Governance and Sustainability Committee are independent both under the DCGC and under the NYSE listing standards.

•Under NYSE listing standards, shareholders of U.S. companies must be given the opportunity to vote on all equity compensation plans and material revisions to those plans, with limited exceptions set forth in the NYSE listing standards. As a foreign private issuer, we are permitted to follow our home country laws regarding shareholder approval of compensation plans. Under Dutch law such approval is only required in relation to members of the board of directors if the articles of association of a company (i.e., public limited liability company (naamloze vennootschap)) stipulate that a corporate body other than the general meeting is authorized to determine the remuneration of members of the board of directors. The adoption of sub-plans under an equity incentive plan that has been approved by the general meeting does not require separate approval of the company’s general meeting, provided, however, that such sub-plans are adopted within the framework and limits of the equity incentive plan as approved by the general meeting. Approval by the general meeting is also not required in respect of equity compensation plans for employees, provided, however, that (i) such employees are no members of the board of

During the year, management performed triggering event analyses for all CGUs for DOS and performed an impairment analysis for those CGUs for DOS where a trigger has been identified. Impairment is recognized when the carrying value of a CGU for DOS assets exceeds the recoverable amount.

For those CGUs for DOS where an impairment analysis is performed, in order to determine the recoverable amount, the Company estimated the DOS assets’ value in use by making significant estimates and assumptions related to, among others, future forecasted revenues and profits for each individual store and the determination of appropriate discount rates. Estimates and assumptions related to future cash flows are determined based on the approved management’s budget and forecast for a period of three years and an estimate of the long-term growth rate.

We identified impairment of DOS assets identified with triggering events as a critical audit matter because the estimate of future store cash flows to assess the recoverability of DOS assets required significant management judgment, primarily in relation to forecasting future revenues and profitability, as well as in relation to the determination of discount rates. Changes in these estimates could have a significant impact on the measurement of the recoverable amount, resulting in a possible adjustment to the impairment charge to be recorded. This area of management estimate required a high degree of auditor judgment and an increased extent of effort, including the need to involve our fair value specialists when performing audit procedures to evaluate the reasonableness of management’s judgments used in preparing these estimates.

How the Critical Audit Matter Was Addressed in the Audit

Our audit procedures related to management’s judgments regarding forecasting future revenues and profitability as well as in relation to the determination of the discount rates included the following:

•We evaluated management’s ability to accurately perform forecasts, including management’s basis and approach for considering the impacts of changes in market conditions and economic events, by:

–inquiring of the Company's executives to understand the business initiatives supporting the assumptions in the future revenues and profits;

–performing a retrospective analysis to assess management’s ability to accurately forecast by comparing actual results to management’s historical forecast; and

–comparing the forecasts to (1) historical revenue and operating results; (2) internal communications regarding the Company’s business plan and strategy; and (3) industry and market conditions.

•With the assistance of our fair value specialists, we evaluated the reasonableness of the discount rates by testing the source information underlying management’s determination of the discount rates and the mathematical accuracy of the calculations.

Other current and non-current financial liabilities – Thom Browne Group - Valuation of put option - Refer to Notes 3, 4, 10 and 28 to the financial statements

Critical Audit Matter Description

As at December 31, 2023, the Company has a put option to buy the remaining 10% of non-controlling interests in Thom Browne Inc. (“Thom Browne”), which is recognized as a financial liability of Euro 139 million, of which Euro 22 million recognized as current.

The valuation of current and non-current financial liabilities was based on management’s forecasts of Thom Browne’s future profitability and their selection of an appropriate discount rate.

Management accounts for the put option agreement recognizing a current and non-current financial liabilities for the Company’s estimated obligation under the option. The exercise price of the put option is dependent on a measure of the brand’s profitability at the exercise date.

F-3

Therefore, the Company’s fair value determination of the current and non-current financial liabilities required management to make significant estimates and assumptions related to forecasts of future revenues and profitability and to select an appropriate discount rate. Changes in above described assumptions could have a significant impact on the measurement of the current and non-current financial liabilities.

We identified the valuation of the put option as a critical audit matter, because of the significant judgments made by management to estimate discount rate, future revenues and profitability of the Thom Browne Group. This required a high degree of auditor judgment and an increased extent of effort, including the involvement of our fair value specialists, when performing audit procedures to evaluate the reasonableness of management’s estimates and assumptions related to discount rate, future revenue and profitability.

How the Critical Audit Matter Was Addressed in the Audit

Our procedures related to the valuation of the put option included the following, among others:

•We evaluated management’s ability to accurately forecast revenues and profit of the Thom Browne Group by comparing actual revenue and profitability to management’s historical forecasts.

•We evaluated management’s assumptions related to future revenues and profitability by:

–Inquiring of the Company's executives to understand the business initiatives supporting the assumptions in the future revenues and profitability, and

–Comparing the forecasts to the current and past performance of the Thom Browne Group and to external market and industry data.

•With the assistance of our fair value specialists, we evaluated the reasonableness of the discount rate by testing the source information underlying management’s determination of the discount rate and the mathematical accuracy of the calculations.

Intangible assets – Fair value determination of intangible asset for Tom Ford license agreement – Refer to Notes 14 and 39 to the financial statements

Critical Audit Matter Description

On April 28, 2023, the Company completed the acquisition of Tom Ford International (“TFI”), the Company that owns and operates the Tom Ford Fashion business. As part of a transaction, sole ownership of the Tom Ford brand, its trademarks, and other intellectual property rights were acquired by The Estee Lauder Companies Inc. (“ELC”), and the Company has become a long-term licensee of ELC for some Tom Ford products. The Company accounted for the acquisition under the acquisition method of accounting for business combinations. Accordingly, the purchase price was allocated to the assets acquired and liabilities assumed based on their respective fair values, including an intangible asset for the license agreement for Euro 99 million. Management estimated the fair value of the license using the multi-period excess earnings method. The fair value determination of the license required management to make significant estimates and assumptions related to future revenues and profitability and the discount rate used.

We identified the valuation of the intangible asset for the Tom Ford license agreement as a critical audit matter because of the significant estimates and assumptions management makes to fair value the license agreement. This required a high degree of auditor judgment and an increased extent of effort, including the need to involve our fair value specialists, when performing audit procedures to evaluate the reasonableness of management’s forecasts revenues, profitability and the discount rate.

How the Critical Audit Matter Was Addressed in the Audit

Our audit procedures related to the forecasts of future revenues, future profitability and the discount rate used for the determination of the fair value of the Tom Ford license agreement included the following, among others:

•We evaluated the terms of the relevant contractual documents, including purchase and sale agreements and license agreement, as well as other documents including board of directors’ minutes, to understand and evaluate the business purpose and the critical terms, rights and obligations associated with the transactions.

•With the assistance of our technical accounting specialist we evaluated the Company's technical accounting analysis regarding the accounting treatment for minimum annual guaranteed royalties that the Company will pay to ELC based on the applicable accounting guidance.

•We assessed the reasonableness of management’s forecasts of future revenues and future profitability by comparing the forecasts to industry comparatives and own accumulated industry knowledge.

F-4

•With the assistance of our fair value specialists, we evaluated the reasonableness of the discount rate applied including:

◦the comparison between the discount rate used and the implied risk in the cash flow used for the license valuation, and

◦the mathematical accuracy of the calculation.

/s/ Deloitte & Touche S.p.A.

Turin, Italy

April 5, 2024

We have served as the Company's auditor since 1995.

F-5

Ermenegildo Zegna N.V.

CONSOLIDATED STATEMENT OF PROFIT AND LOSS

for the years ended December 31, 2023, 2022 and 2021

For the years ended December 31,

(€ thousands, except per share data)

Notes

2023

2022(*)

2021(*)

Revenues

6

1,904,549

1,492,840

1,292,402

Cost of sales

7

(680,235)

(564,832)

(495,702)

Gross profit

1,224,314

928,008

796,700

Selling, general and administrative expenses

8

(901,364)

(695,084)

(822,897)

Marketing expenses

9

(114,802)

(85,147)

(67,831)

Operating profit/(loss)

208,148

147,777

(94,028)

Financial income

10

37,282

13,320

45,889

Financial expenses

10

(68,121)

(54,346)

(43,823)

Foreign exchange losses

10

(5,262)

(7,869)

(7,791)

Result from investments accounted for using the equity method

17

(2,953)

2,199

2,794

Profit/(Loss) before taxes

169,094

101,081

(96,959)

Income taxes

11

(33,433)

(35,802)

(30,702)

Profit/(Loss)

135,661

65,279

(127,661)

Attributable to:

Shareholders of the Parent Company

121,529

51,482

(136,001)

Non-controlling interests

14,132

13,797

8,340

Basic earnings per share in €

12

0.49

0.22

(0.67)

Diluted earnings per share in €

12

0.48

0.21

(0.67)

_________________

(*) Starting with the year ended December 31, 2023, the Group presents the consolidated statement of profit and loss by function, which is most representative of the way the Chief Operating Decision Maker and management view the business, and therefore it provides reliable and more relevant information and is consistent with international practice. In order to conform to this new presentation, the information for the year ended December 31, 2022 and 2021 have been reclassified compared to what was previously presented by the Group.

The accompanying notes are an integral part of these Consolidated Financial Statements

F-6

Ermenegildo Zegna N.V.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME AND LOSS

for the years ended December 31, 2023, 2022 and 2021

For the years ended December 31,

(€ thousands)

Notes

2023

2022

2021

Profit/(Loss)

135,661

65,279

(127,661)

Other comprehensive (loss)/income, net of tax:

Items that will be subsequently reclassified to the statement of profit and loss:

Foreign currency exchange differences arising from the translation of foreign operations(*)

(15,887)

10,098

40,324

Net (loss)/gain from cash flow hedges

(7,553)

21,744

(6,344)

Net gain/(loss) from financial instruments measured at fair value

635

(1,482)

444

Items that will not be subsequently reclassified to the statement of profit and loss:

Net actuarial gain/(loss) from defined benefit plans

1,025

1,092

(397)

Total other comprehensive (loss)/income, net of tax

25

(21,780)

31,452

34,027

Total comprehensive income/(loss)

113,881

96,731

(93,634)

Attributable to:

Shareholders of the Parent Company

100,583

82,908

(102,106)

Non-controlling interests

13,298

13,823

8,472

_________________

(*) As a result of the acquisition of Tom Ford International in April 2023, cumulative translation losses amounting to €4,705 thousand related to the original investment held in Tom Ford International were reclassified from other comprehensive income and loss to foreign exchange losses within the consolidated statement of profit and loss for the year ended December 31, 2023. For additional information relating to the acquisition of Tom Ford International see Note 1 — General information, Note 17 — Investments accounted for using the equity method and Note 39 — Business combinations.

The accompanying notes are an integral part of these Consolidated Financial Statements.

F-7

Ermenegildo Zegna N.V.

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

at December 31, 2023 and 2022

At December 31,

(€ thousands)

Notes

2023

2022

Assets

Non-current assets

Intangible assets

14

572,274

455,908

Property, plant and equipment

15

159,608

126,139

Right-of-use assets

16

533,952

375,508

Investments accounted for using the equity method

17

18,765

22,648

Deferred tax assets

11

160,878

124,627

Other non-current financial assets

18

33,898

36,240

Total non-current assets

1,479,375

1,141,070

Current assets

Inventories

19

522,589

410,851

Trade receivables

20

240,457

177,213

Derivative financial instruments

21

11,110

22,454

Tax receivables

31,024

15,350

Other current financial assets

22

90,917

320,894

Other current assets

23

95,260

84,574

Cash and cash equivalents

24

296,279

254,321

Total current assets

1,287,636

1,285,657

Total assets

2,767,011

2,426,727

Liabilities and Equity

Equity attributable to shareholders of the Parent Company

840,294

678,949

Equity attributable to non-controlling interests

26

60,602

53,372

Total equity

900,896

732,321

Non-current liabilities

Non-current borrowings

27

113,285

184,880

Other non-current financial liabilities

28

136,556

178,793

Non-current lease liabilities

29

471,083

332,050

Non-current provisions for risks and charges

30

19,849

19,581

Employee benefits

31

29,645

51,584

Deferred tax liabilities

11

73,885

60,534

Other non-current liabilities

33

9,689

—

Total non-current liabilities

853,992

827,422

Current liabilities

Current borrowings

27

289,337

286,175

Other current financial liabilities

28

22,102

37,258

Current lease liabilities

29

122,642

111,457

Derivative financial instruments

21

897

2,362

Current provisions for risks and charges

30

16,019

13,969

Trade payables and customer advances

32

314,137

270,936

Tax liabilities

41,976

25,999

Other current liabilities

33

205,013

118,828

Total current liabilities

1,012,123

866,984

Total equity and liabilities

2,767,011

2,426,727

The accompanying notes are an integral part of these Consolidated Financial Statements.

F-8

Ermenegildo Zegna N.V.

CONSOLIDATED CASH FLOW STATEMENT

for the years ended December 31, 2023, 2022 and 2021

For the years ended December 31,

(€ thousands)

Notes

2023

2022

2021

Operating activities

Profit/(Loss)

135,661

65,279

(127,661)

Income taxes

11

33,433

35,802

30,702

Depreciation, amortization and impairment of assets

13

194,952

173,521

163,367

Financial income

10

(37,282)

(13,320)

(45,889)

Financial expenses

10

68,121

54,346

43,823

Foreign exchange losses

10

5,262

7,869

7,791

Write downs and other provisions

(1,168)

14

19,487

Write downs of the provision for obsolete inventory

19

31,850

28,561

29,600

Result from investments accounted for using the equity method

17

2,953

(2,199)

(2,794)

(Gains)/Losses arising from the disposal of fixed assets

—

(1,124)

1,153

Other non-cash expenses, net

38

66,641

23,063

230,812

Change in inventories

(72,770)

(103,112)

(27,554)

Change in trade receivables

(51,022)

(15,623)

(12,294)

Change in trade payables including customer advances

11,670

43,511

31,426

Change in current and non-current provisions for risks and charges

(6,720)

(29,102)

(5,498)

Change in employee benefits

(2,566)

(8,676)

(13,456)

Change in other operating assets and liabilities

(20,479)

(38,216)

38,927

Interest paid

(29,166)

(24,938)

(17,487)

Income taxes paid

(53,988)

(49,258)

(63,300)

Net cash flows from operating activities

275,382

146,398

281,155

Investing activities

Payments for property, plant and equipment

(57,034)

(49,114)

(79,699)

Proceeds from disposals of property, plant and equipment

—

—

3,791

Payments for intangible assets

(20,843)

(24,185)

(14,627)

Proceeds from disposals of non-current financial assets

2,345

2,585

1,536

Payments for purchases of non-current financial assets

(2,623)

(111)

(4,431)

Proceeds from disposals of current financial assets and derivative instruments

22

270,317

46,487

92,021

Payments for acquisitions of current financial assets and derivative instruments

(36,956)

(32,412)

(76,058)

Business combinations, net of cash acquired

39

(117,686)

(585)

(4,224)

Acquisition of investments accounted for using the equity method

17

(15,734)

—

(313)

Net cash flows from/(used in) investing activities

21,786

(57,335)

(82,004)

Financing activities

Proceeds from borrowings

27

204,424

—

123,570

Repayments of borrowings

27

(306,150)

(159,719)

(160,210)

Repayments of other non-current financial liabilities

28

—

(3,919)

(4,287)

Payments of lease liabilities

29

(125,732)

(121,633)

(100,611)

Proceeds from the exercise of warrants

28

4,409

—

—

Proceeds from capital contribution from Monterubello

25

—

10,923

—

Sales of shares held in treasury

25

3,654

3,390

6,343

Purchase of own shares

—

—

(384)

Dividends to owners of the parent

(25,031)

(21,852)

(102)

Dividends paid to non-controlling interests

(6,068)

(4,187)

(548)

Purchase of own shares from Monterubello

1

—

—

(455,000)

Proceeds from issuance of ordinary shares upon Business Combination

1

—

—

310,739

Proceeds from issuance of ordinary shares to PIPE Investors

1

—

—

331,385

Payments of transaction costs related to the Business Combination

1

—

—

(48,475)

Cash distributed as part of the Disposition

—

—

(26,272)

Payments for acquisition of non-controlling interests

—

—

(40,253)

Net cash flows used in financing activities

(250,494)

(296,997)

(64,105)

Effects of exchange rate changes on cash and cash equivalents

(4,716)

2,464

7,454

Net increase/(decrease) in cash and cash equivalents

41,958

(205,470)

142,500

Cash and cash equivalents at the beginning of the year

24

254,321

459,791

317,291

Cash and cash equivalents at the end of the year

24

296,279

254,321

459,791

The accompanying notes are an integral part of these Consolidated Financial Statements.

F-9

Ermenegildo Zegna N.V.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

for the years ended December 31, 2023, 2022 and 2021

Legal reserves

(€ thousands)

Share capital

Share premium

Currency translation difference

Cash flow hedge reserve

Reserve for remeasurement of defined benefit plans

Financial assets at FVOCI reserve

Other legal reserves

Reserve for treasury shares

Other reserves

Retained earnings

Total equity attributable to shareholders of the Parent Company

Total equity attributable to non-controlling interests

Total equity

At January 1, 2021(*)

4,300

—

(24,660)

(2,225)

741

243

—

(76,624)

(193,247)

893,236

601,764

43,270

645,034

(Loss)/Profit

—

—

—

—

—

—

—

—

—

(136,001)

(136,001)

8,340

(127,661)

Other comprehensive income/(loss)

—

—

40,197

(6,316)

(430)

444

—

—

—

—

33,895

132

34,027

Total comprehensive income

—

—

40,197

(6,316)

(430)

444

—

—

—

(136,001)

(102,106)

8,472

(93,634)

Legal reserves

—

—

—

—

—

—

20,351

—

(21,211)

860

—

—

—

Dividends

—

—

—

—

—

—

—

—

(102)

—

(102)

(548)

(650)

Capital increase related to the Business Combination

1,639

710,264

—

—

—

—

—

—

—

—

711,903

—

711,903

Purchase of own shares from Monterubello

—

—

—

—

—

—

—

(455,000)

—

—

(455,000)

—

(455,000)

Capital contribution from Monterubello

—

10,923

—

—

—

—

—

—

—

—

10,923

—

10,923

Issuance of shares held in treasury

—

—

—

—

—

—

—

76,624

(70,665)

—

5,959

—

5,959

Assignment of treasury shares

—

—

—

—

—

—

—

—

31,823

(31,823)

—

—

—

Acquisition of non-controlling interests

—

—

—

—

—

—

—

—

—

8,365

8,365

(8,365)

—

Acquisition of Ubertino

—

—

—

—

—

—

—

—

—

—

—

2,854

2,854

Share-based payments

—

—

—

—

—

—

—

—

74,978

—

74,978

—

74,978

Disposition

—

—

(20,465)

176

—

—

—

—

—

(235,185)

(255,474)

(2,589)

(258,063)

At December 31, 2021(*)

5,939

721,187

(4,928)

(8,365)

311

687

20,351

(455,000)

(178,424)

499,452

601,210

43,094

644,304

Profit

—

—

—

—

—

—

—

—

—

51,482

51,482

13,797

65,279

Other comprehensive income/(loss)

—

—

10,223

21,744

941

(1,482)

—

—

—

—

31,426

26

31,452

Total comprehensive income

—

—

10,223

21,744

941

(1,482)

—

—

—

51,482

82,908

13,823

96,731

Legal reserves

—

—

—

—

—

—

4,927

—

(4,927)

—

—

—

—

Dividends

—

—

—

—

—

—

—

—

—

(21,852)

(21,852)

(4,187)

(26,039)

Sale of treasury shares, net

—

—

—

—

—

—

—

3,826

—

—

3,826

—

3,826

Share-based payments

—

—

—

—

—

—

—

—

13,579

—

13,579

—

13,579

Other changes

—

—

—

—

—

—

—

—

40

(762)

(722)

642

(80)

At December 31, 2022(*)

5,939

721,187

5,295

13,379

1,252

(795)

25,278

(451,174)

(169,732)

528,320

678,949

53,372

732,321

Profit

—

—

—

—

—

—

—

—

—

121,529

121,529

14,132

135,661

Other comprehensive income/(loss)

—

—

(15,151)

(7,553)

1,123

635

—

—

—

—

(20,946)

(834)

(21,780)

Total comprehensive income

—

—

(15,151)

(7,553)

1,123

635

—

—

—

121,529

100,583

13,298

113,881

Legal reserves

—

—

—

—

—

—

(3,145)

—

3,145

—

—

—

—

Dividends

—

—

—

—

—

—

—

—

—

(25,031)

(25,031)

(6,068)

(31,099)

Sale of treasury shares, net

—

—

—

—

—

—

—

3,902

(248)

—

3,654

—

3,654

Exercise of warrants

115

64,500

—

—

—

—

—

—

(1,236)

—

63,379

—

63,379

Issuance of Special Voting Shares A

3,100

(3,100)

—

—

—

—

—

—

—

—

—

—

—

Share-based payments

—

—

—

—

—

—

—

—

19,780

—

19,780

—

19,780

Settlement of share-based payments

—

—

—

—

—

—

—

10,650

(11,093)

443

—

—

—

Other changes

—

—

—

—

—

—

—

—

5,388

(6,408)

(1,020)

—

(1,020)

At December 31, 2023

9,154

782,587

(9,856)

5,826

2,375

(160)

22,133

(436,622)

(153,996)

618,853

840,294

60,602

900,896

(*) Starting with the Semi-Annual Condensed Consolidated Financial Statements at June 30, 2023 and for the six months ended June 30, 2023 and 2022, in the consolidated statement of changes in equity the Group separately presents certain components of equity, including share premium, the reserve for treasury shares and other legal reserves, which were previously presented within other reserves. Management believes this presentation, together with the accompanying notes, facilitate a better understanding of the underlying components of the Group’s equity. As a result of this new presentation, certain comparative period amounts above have been reclassified compared to the amounts presented in the Group’s 2022 consolidated financial statements.

The accompanying notes are an integral part of these Consolidated Financial Statements.

F-10

Ermenegildo Zegna N.V.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

At December 31, 2023 and 2022 and for the years ended December 31, 2023, 2022 and 2021

1. General information

Ermenegildo Zegna N.V. (formerly known as Ermenegildo Zegna Holditalia S.p.A., and hereinafter referred to as the “Company” or the “Parent Company” and together with its consolidated subsidiaries, or any one or more of them, as the context may require, the “Ermenegildo Zegna Group” or the “Group”) is the holding company of the Group and is incorporated as a public company (naamloze vennootschap) under the laws of the Netherlands and its ordinary shares are listed on the New York Stock Exchange under the “ZGN” ticker. The Company is domiciled in Amsterdam, the Netherlands, and the Company’s registered office is Viale Roma 99/100, Valdilana (Biella), Italy.

Ermenegildo Zegna Group is a leading global luxury group, internationally recognized for the distinctive heritage of craftsmanship and design associated with the ZEGNA and Thom Browne brands and the noble fabrics and fibers of its in-house luxury textile and knitwear business. Since its foundation in 1910 through Lanificio Ermenegildo Zegna e Figli S.p.A. (“Lanificio”) in Valdilana (BI), Italy, the Group has expanded beyond luxury textile production to ready-to-wear products and accessories to become a highly recognized luxury lifestyle group. The Group designs, manufactures, markets and distributes luxury menswear, footwear, leather goods and other accessories under the ZEGNA and the Thom Browne brands, and luxury womenswear and childrenswear under the Thom Browne brand. The Group’s product range is complemented by eyewear, cufflinks and jewelry, watches, underwear and beachwear manufactured by third parties under licenses. In addition, following the completion of the acquisition of Tom Ford International (“TFI”) on April 28, 2023 (the “TFI Acquisition”), the Group has become a long-term licensee of the Estée Lauder Companies Inc. (“ELC”) for all TOM FORD men’s and women’s fashion as well as accessories and underwear, fine jewelry, childrenswear, textile, and home design products. For further information on the TFI Acquisition, see Note 39 — Business combinations. The Group’s business covers the entire value chain as a result of its design, manufacturing and distribution business and the Group has a significant international presence through the retail channel, consisting of directly operated single-brand stores (“Directly Operated Stores” or “DOS”) and online stores, as well as through the wholesale channel, represented by multi-brand stores, luxury department stores and major international airports.

Business Combination and other transactions in 2021

On December 17, 2021, the Group closed the previously announced business combination pursuant to a business combination agreement, dated as of July 18, 2021, as amended, by and among the Group, Investindustrial Acquisition Corp. (“IIAC”) and EZ Cayman, a wholly-owned subsidiary of the Group (“Zegna Merger Sub”), through a series of transactions as described below (the “Business Combination”).

Effective November 1, 2021, Ermenegildo Zegna Holditalia S.p.A. transferred its activities related to design and style, brand, marketing, planning, retail management, human resources, finance and accounting, legal, information technology and internal audit and compliance, and transferred 197 employees out of a total 212 employees to EZ Service S.r.l. (“EZ Service”), a limited liability company based in Italy that was incorporated on October 1, 2021 and is fully owned by Ermenegildo Zegna N.V. Subsequent to this transfer the Company’s activities are primarily limited to holding investments in the subsidiaries of the Group and conducting certain administrative, treasury, internal control and investor relations activities.

Also on November 1, 2021, Ermenegildo Zegna Holditalia S.p.A. completed the disposition of certain of its businesses (the “Disposition”), through the statutory demerger under Italian law to a new company owned by its existing shareholders. The Disposition included, inter alia, Ermenegildo Zegna Holditalia S.p.A.’s real estate business, consisting of its former subsidiary EZ Real Estate S.r.l. (“EZ Real Estate”), which directly and indirectly holds substantially all of the real estate assets formerly owned by the Group, as well as certain properties previously owned by Lanificio, and its 10% equity interest in Elah Dufour S.p.A. Most of the real estate properties directly or indirectly owned by EZ Real Estate were, and continue to be, leased to the Group also following the Disposition.

The following transactions related to the Business Combination were completed on December 17, 2021:

•Ermenegildo Zegna Holditalia S.p.A. implemented a cross-border conversion whereby it, by means of the execution of a Dutch notarial deed of cross-border conversion and amendment of its articles of association,

F-11

converted into a Dutch public limited liability company (naamloze vennootschap) and transferred its legal seat from Italy to the Netherlands and amended its articles of association, upon which the Company changed its name to Ermenegildo Zegna N.V. (the “Conversion”);

•In connection with the Conversion, the Company underwent a share split of 4,300,000 ordinary shares into 215,000,000 ordinary shares (the “Share Split”);

•Zegna Merger Sub merged with and into IIAC, with IIAC being the surviving entity in the merger (the “Merger”), as a result of which:

(a)each share of Zegna Merger Sub was converted into one IIAC ordinary share;

(b)a total number of 44,443,659 IIAC class A shares and class B shares were contributed to the Company in exchange for an equivalent number of the Company ordinary shares, representing a capital increase of €397.8 million measured based on the closing price of IIAC’s shares of $10.14 per share on December 17, 2021;

(c)13,416,637 outstanding IIAC public warrants were converted to an equivalent number of the Company public warrants representing a right to acquire one the Company ordinary share. The public warrants were measured at fair value by using the Euro equivalent of the closing price of IIAC warrants on December 17, 2021, amounting to a total of €20,723 thousand; and

(d)5,900,000 IIAC private placement warrants were exchanged for an equivalent number of the Company private placement warrants representing a right to acquire one the Company ordinary share, while the remaining 800,000 IIAC private placement warrants were transferred by Strategic Holding Group S.à r.l. to the Ermenegildo Zegna Group and the Company issued a corresponding number of private placement warrants to certain of its directors. The private placement warrants were measured at fair value using a Monte Carlo simulation model, amounting to a total of €10,349 thousand;

(e)The issuance of 5,031,250 the Company ordinary shares to the holders of IIAC class B shares to be held in escrow. The release of these shares from escrow is subject to achievement of certain targets within a seven-year period (“Escrow Shares”). The Escrow Shares were measured in accordance with IFRS 2 - Share-Based Payment (“IFRS 2”) using a Monte Carlo simulation model, amounting to a total of €37,906 thousand;

•Pursuant to certain agreements between the Group and IIAC, the private investment in public equity investors (“PIPE Investors”) subscribed to an aggregate of 37,500,000 the Company ordinary shares for an aggregate purchase price of €331.4 million;

•The Company repurchased 54,600,000 of its ordinary shares from the Group’s controlling shareholder, Monterubello s.s. (hereinafter “Monterubello”), in exchange for consideration of €455.0 million.

•Transaction costs incurred by the Group in relation to the Business Combination amounted to €51.4 million (€2.9 million of which were paid in 2022), of which €17.3 million were recognized directly within equity and €34.1 million were recognized in the consolidated statement of profit and loss for the year ended December 31, 2021.

The following table shows a breakdown of the net cash proceeds in 2021 from the Business Combination:

(€ thousands)

Proceeds from issuance of Ordinary Shares upon Business Combination

310,739

Proceeds from issuance of Ordinary Shares to PIPE Investors

331,385

Purchase of own shares from Monterubello

(455,000)

Payments of transaction costs related to the Business Combination

(48,475)

Net cash proceeds from the Business Combination

138,649

F-12

Following the completion of the Business Combination, on December 20, 2021, the Company’s ordinary shares and public warrants began trading on the New York Stock Exchange (“NYSE”) under the symbols “ZGN” and “ZGN WS,” respectively.

Accounting for the Business Combination

The Business Combination between the Group and IIAC was accounted for as a capital reorganization in accordance with International Financial Reporting Standards. For accounting purposes, the Business Combination was treated as the equivalent of the Company issuing shares for the net assets of IIAC, which were stated at historical cost, with no goodwill or other intangible assets recorded.

It has been determined that IIAC does not meet the definition of a “business” pursuant to IFRS 3 — Business Combinations (“IFRS 3”), hence the transaction is accounted for within the scope of IFRS 2. In accordance with IFRS 2, the difference in the fair value of the Group’s equity instruments deemed issued to IIAC shareholders (measured based on the closing price of IIAC’s shares of $10.14 per share on December 17, 2021) over the fair value of identifiable net assets of IIAC represents a service for listing amounting to €114,963 thousand and was accounted for as a share-based payment expensed as incurred.

2. Basis of preparation

Statement of compliance with IFRS

These consolidated financial statements of Ermenegildo Zegna N.V. have been prepared in compliance with the International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), as well as IFRS as adopted by the European Union. There is no effect on these consolidated financial statements resulting from differences between IFRS as issued by the IASB and IFRS as adopted by the European Union.

These consolidated financial statements were approved and authorized for issue by the Board of Directors of Ermenegildo Zegna N.V. on April 4, 2024.

Contents and structure of the Consolidated Financial Statements

The consolidated financial statements include the consolidated statement of profit and loss, the consolidated statement of comprehensive income and loss, the consolidated statement of financial position, the consolidated cash flow statement, the consolidated statement of changes in equity and the accompanying notes (collectively referred to as the “Consolidated Financial Statements”).

The financial reporting formats presented by the Group have the following characteristics:

•starting in 2023, the Group presents the consolidated statement of profit and loss by function, which is most representative of the way the Chief Operating Decision Maker and management view the business, and therefore it provides reliable and more relevant information and is consistent with international practice. In order to conform to this new presentation, the information for the year ended December 31, 2022 and 2021 has been reclassified compared to what was previously presented by the Group;

•the consolidated statement of comprehensive income and loss is presented as a separate statement and, in addition to presenting the components of profit and loss recognized directly in the consolidated statement of profit and loss during the period, presents the components of profit and loss not recognized in profit or loss as required or permitted by IFRS;

•the consolidated statement of financial position presents assets and liabilities by current and non-current items. Current items are those expected to be realized within 12 months from the reporting date or to be sold or consumed in the normal operating cycle of the Group;

•the consolidated cash flow statement has been prepared using the “indirect method,” as permitted by IAS 7 — Statement of Cash Flows (“IAS 7”), and presents cash flows by operating, investing and financing activities;

F-13

•the consolidated statement of changes in equity presents the movements in shareholder’s equity. Starting in 2023, in the consolidated statement of changes in equity the Group separately presents certain components of equity, including share premium, the reserve for treasury shares and other legal reserves, which were previously presented within other reserves. Management believes this presentation, together with the accompanying notes, facilitate a better understanding of the underlying components of the Group’s equity. As a result of this new presentation, certain amounts presented for periods prior to the year ended December 31, 2023 within these Consolidated Financial Statements have been reclassified compared to amounts previously presented by the Group;

•the notes to the consolidated financial statements comprise a summary of the material accounting policy information and other explanatory information. In order to conform the note to the consolidated financial statements with the new presentation of the consolidated statement of profit and loss by function, the explanatory information for the year ended December 31, 2022 and 2021 has been modified compared to what was previously presented by the Group.

The Consolidated Financial Statements are presented in Euro, which is the functional and presentation currency of the Company, and amounts are stated in thousands of Euros, unless otherwise indicated.

The Consolidated Financial Statements have been prepared on a going concern basis and applying the historical cost method, modified as required for certain financial assets and liabilities (including derivative instruments), which are measured at fair value, as further described in the accounting policy information below. Income and expenses are accounted for on an accrual basis.

3. Summary of material accounting policy information

New standards and amendments effective from January 1, 2023

In May 2017, the IASB issued IFRS 17 — Insurance Contracts, which establishes principles for the recognition, measurement, presentation and disclosure of insurance contracts issued as well as guidance relating to reinsurance contracts held and investment contracts with discretionary participation features issued. In June 2020 the IASB issued amendments to IFRS 17 aimed at helping companies implement IFRS 17 and make it easier for companies to explain their financial performance. The new standard and amendments are effective on or after January 1, 2023. There was no effect from the adoption of these amendments.

In February 2021, the IASB issued amendments to IAS 1 — Presentation of Financial Statementsand IFRS Practice Statement 2: Disclosure of Accounting Policies which require companies to disclose their material accounting policy information rather than their significant accounting policies and provide guidance on how to apply the concept of materiality to accounting policy disclosures. These amendments are effective on or after January 1, 2023. Certain accounting policy disclosures were updated a result of the adoption of these amendments.

In February 2021, the IASB issued amendments to IAS 8 — Accounting Policies, Changes in Accounting Estimates and Errors: Definition of Accounting Estimates which clarify how companies should distinguish changes in accounting policies from changes in accounting estimates. These amendments are effective on or after January 1, 2023. There was no effect from the adoption of these amendments.

In May 2021, the IASB issued amendments to IAS 12 — Income Taxes: Deferred Tax related to Assets and Liabilities Arising From a Single Transaction that clarify how companies account for deferred tax on transactions such as leases and decommissioning obligations. These amendments are effective on or after January 1, 2023. There was no effect from the adoption of these amendments. As a result of adopting the amendments the Group recognizes deferred taxes arising from lease accounting on a gross basis.

In December 2021, the IASB issued an amendments to IFRS 17 — Insurance Contracts: Initial Application of IFRS 17 and IFRS 9 - Comparative Information, which provides a transition option relating to comparative information about financial assets presented on initial application of IFRS 17. The amendment is aimed at helping entities to avoid temporary accounting mismatches between financial assets and insurance contract liabilities, and therefore improve the usefulness of

F-14

comparative information for users of financial statements. The amendment is effective on or after January 1, 2023. There was no effect from the adoption of these amendments.

In May 2023, the IASB issued amendments to IAS 12 — Income taxes: International Tax Reform – Pillar Two Model Rules, to clarify the application of IAS 12 — Income taxes to income taxes arising from tax law enacted or substantively enacted to implement the Organisation for Economic Co-operation and Development (OECD)/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) Pillar Two model rules (Pillar Two income taxes). The amendments introduce: (i) a mandatory temporary exception for the recognition of and disclosure relating to deferred tax assets and liabilities arising from the jurisdictional implementation of the Pillar Two model rules, which was effective immediately upon issuance of the amendment and which the Group applied from that date, and (ii) disclosure requirements for affected entities to help users of the financial statements better understand an entity’s exposure to Pillar Two income taxes arising from that legislation, particularly before the effective date of the Pillar Two model rules, which apply for annual reporting periods beginning on or after January 1, 2023, but not for any interim periods ending on or before December 31, 2023. Please refer to Note 11 — Income taxes for additional information relating to Pillar Two model rules.

New standards, amendments and interpretations not yet effective

The standards, amendments and interpretations issued by the IASB that will have mandatory application in 2024 or subsequent years are listed below:

In January 2020, the IASB issued amendments to IAS 1 — Presentation of Financial Statements: Classification of Liabilities as Current or Non-Current to clarify how to classify debt and other liabilities as current or non-current, and in particular how to classify liabilities with an uncertain settlement date and liabilities that may be settled by converting to equity. These amendments are effective on or after January 1, 2024. The Group does not expect any material impact from the adoption of these amendments.

In September 2022, the IASB issued amendments to IFRS 16 — Leases: Liability in a Sale and Leaseback to improve the requirements for sale and leaseback transactions, which specify the measurement of the liability arising in a sale and leaseback transaction, to ensure the seller-lessee does not recognize any amount of the gain or loss that relates to the right of use it retains. These amendments are effective on or after January 1, 2024. The Group does not expect any material impact from the adoption of these amendments.

In October 2022, the IASB issued amendments to IAS 1 — Presentation of Financial Statements: Non-current Liabilities with Covenants, that clarify how conditions with which an entity must comply within twelve months after the reporting period affect the classification of a liability. These amendments are effective on or after January 1, 2024. The Group does not expect any material impact from the adoption of these amendments.

In May 2023, the IASB issued amendments to IAS 7 — Statement of Cash Flows and IFRS 7 — Financial Instruments: Disclosures: Supplier Finance Arrangements, that introduce new disclosure requirements to enhance the transparency and usefulness of the information provided by entities about supplier finance arrangements and are intended to assist users of financial statements in understanding the effects of supplier finance arrangements on an entity’s liabilities, cash flows and exposure to liquidity risk. The amendments are effective on or after January 1, 2024. The Group is evaluating the potential impact from the adoption of these amendments.

In August 2023, the IASB issued amendments to IAS 21 — The Effects of Changes in Foreign Exchange Rates: Lack of Exchangeability, to clarify how an entity has to apply a consistent approach to assessing whether a currency is exchangeable into another currency and, when it is not, to determine the exchange rate to use and the disclosures to provide. These amendments are effective on or after January 1, 2025. The Group is evaluating the potential impact from the adoption of these amendments.

F-15

Material accounting policy information

Basis of consolidation

Subsidiaries

Subsidiaries are entities over which the Group has control. Control is achieved when the Group has the power over the investee, it is exposed, or has rights to, variable returns from its involvement with the investee, and has the ability to use its power to affect its returns. Subsidiaries are consolidated on a line by line basis from the date on which the Group obtains control. The Group reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control listed above.

Subsidiaries are deconsolidated from the date when control ceases. When the Group ceases to have control over a subsidiary, it derecognizes the assets (including any goodwill) and liabilities of the subsidiaries at their carrying amounts, derecognizes the carrying amount of non-controlling interests in the former subsidiary and recognizes the fair value of any consideration received from the transaction. Any retained interest in the former subsidiary is then remeasured to its fair value.

The Group recognizes any non-controlling interests (“NCI”) in the acquiree on an acquisition-by-acquisition basis, either at fair value or at the non-controlling interests’ share of the acquiree’s identifiable net assets. Net profit or loss and each component of other comprehensive income/(loss) are attributed to the owners of the parent and to the non-controlling interests.

All intra-group balances and transactions and any unrealized gains and losses arising from intra-group transactions are eliminated in preparing the Consolidated Financial Statements.

Foreign currency transactions

The functional currency of the Group’s entities is the currency of their primary economic environment. Transactions in foreign currencies are recorded at the exchange rate prevailing at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies at the balance sheet date are translated at the foreign currency exchange rate prevailing at that date. Exchange differences arising on the settlement of monetary items or on reporting monetary items at rates different from those at which they were initially recorded during the period or in previous financial statements are recognized in the consolidated statement of profit and loss.

Consolidation of foreign entities

Upon consolidation, all assets and liabilities of Group entities with a functional currency other than the Euro are translated using the closing rates at the date of the consolidated statement of financial position. Income and expenses are translated into Euro at the average foreign currency exchange rate for the period. Translation differences resulting from the application of this method are recognized within other comprehensive income/(loss) and accumulated in the currency translation reserve until the disposal of the investment, at which date the accumulated amount is reclassified to profit/(loss). Average foreign currency exchange rates for the period are used to translate the cash flows of foreign subsidiaries in preparing the consolidated statement of cash flows. Goodwill, assets acquired and liabilities assumed arising from the acquisition of entities with a functional currency other than the Euro are recognized in the Consolidated Financial Statements in the functional currency and translated at the foreign currency exchange rate at the acquisition date. These balances are translated at subsequent balance sheet dates at the relevant foreign currency exchange rate.

F-16

The following table presents the principal foreign currency exchange rates used by the Group to translate other currencies into Euro:

2023

2022

2021

At December 31,

Average

At December 31,

Average

At December 31,

Average

U.S. Dollar

1.105

1.081

1.067

1.053

1.133

1.183

Swiss Franc

0.926

0.972

0.985

1.005

1.033

1.081

Chinese Renminbi

7.851

7.660

7.358

7.079

7.195

7.629

Pound Sterling

0.869

0.870

0.887

0.853

0.840

0.860

Hong Kong Dollar

8.631

8.465

8.316

8.245

8.833

9.193

Singapore Dollar

1.459

1.452

1.430

1.451

1.528

1.589

United Arab Emirates Dirham

4.058

3.971

3.917

3.867

4.160

4.344

Japanese Yen

156.330

151.990

140.660

138.027

130.380

129.877

South Korean Won

1,433.660

1,412.880

1,344.090

1,358.073

1,346.380

1,353.958

Interests in associates and in joint arrangements

An associate is an entity over which the Group has significant influence. Significant influence is the power to participate in the financial and operating policy decisions of the investee without having control or joint control over those policies.

A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the arrangement.

Associates and joint ventures are accounted for using the equity method of accounting, from the date significant influence or joint control is obtained, respectively.

Under the equity method, the investments are initially recognized at cost and adjusted thereafter to recognize the Group’s share of the profit/(loss) and other comprehensive income/(loss) of the investee. The Group’s share of the investee’s profit/(loss) is recognized in the consolidated statement of profit and loss. Distributions received from an investee reduce the carrying amount of the investment. Post-acquisition movements in other comprehensive income/(loss) are recognized in other comprehensive income/(loss) with a corresponding adjustment to the carrying amount of the investment. Unrealized gains on transactions between the Group and its associates and joint ventures are eliminated to the extent of the Group’s interest. Unrealized losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. When the Group’s share of the losses of an associate or joint venture exceeds the carrying amount of the Group’s investment, the Group discontinues recognizing its share of further losses. Additional losses are provided for, and a liability is recognized, only to the extent that the Group has incurred legal or constructive obligations or made payments on behalf of the related investee. The Group discontinues the use of the equity method from the date the investment ceases to be an associate or joint venture, or when it is classified as available-for-sale.

Scope of consolidation

Ermenegildo Zegna N.V. is the parent company of the Group and it holds, directly or indirectly, interests in the Group’s subsidiaries. The following table presents the Group’s scope of consolidation at December 31, 2023 and 2022:

Company