3月25日,摩根士丹利Laura Wang等分析师发布报告,上调中国主要股指目标点位,上调2025年底恒生指数、国企指数、MSCI中国和沪深300指数目标价至25800、9500、83和4220点,分别代表9%、9%、9%和8%的上行空间。

3月25日,摩根士丹利Laura Wang等分析师发布报告,上调中国主要股指目标点位,上调2025年底恒生指数、国企指数、MSCI中国和沪深300指数目标价至25800、9500、83和4220点,分别代表9%、9%、9%和8%的上行空间。

Source: Wall Street Journal.

Morgan Stanley has once again raised the Target Price for the China market, expecting an upside potential of 8%-9% for the Hang Seng Index, Hang Seng China Enterprises Index, MSCI China, and CSI 300 Index by the end of the year. The upgrade is based on three main reasons: the first earnings surprise in three and a half years, revisions to profit forecasts, and the potential for valuations to eliminate long-term discounts, moving closer to Emerging Markets levels.

Morgan Stanley has once again raised the target for the Chinese market based on three solid reasons: Q4 2024 earnings reports exceeded expectations, profit forecasts have been revised upwards, and valuations may further approach levels seen in Emerging Markets.

On March 25, Morgan Stanley analysts Laura Wang and others released a report raising the target points for major Chinese stock indices. The target prices for the Hang Seng Index, Hang Seng China Enterprises Index, MSCI Chinese Index, and CSI 300 Index have been raised to 25,800, 9,500, 83, and 4,220 points, representing upside potential of 9%, 9%, 9%, and 8% respectively.

On March 25, Morgan Stanley analysts Laura Wang and others released a report raising the target points for major Chinese stock indices. The target prices for the Hang Seng Index, Hang Seng China Enterprises Index, MSCI Chinese Index, and CSI 300 Index have been raised to 25,800, 9,500, 83, and 4,220 points, representing upside potential of 9%, 9%, 9%, and 8% respectively.

Despite ongoing uncertainties, Morgan Stanley holds a cautiously optimistic view on the prospects for the Chinese market, believing that with improving profit expectations and valuation recovery, the market is likely to see further gains:

Earnings performance exceeded expectations: MSCI Chinese companies reported their first net performance exceeding expectations in three and a half years, with Q4 2024 earnings reports indicating an 8% net surprise (calculated by company count and weighted earnings), ending a streak of disappointing results over 13 consecutive quarters.

Profit forecasts have been raised: Due to earnings reports exceeding expectations and macro improvements, Morgan Stanley has revised upwards the profit growth forecasts for MSCI China for 2025 and 2026 to 7% and 9%.

Valuation gaps are narrowing: Morgan Stanley expects the MSCI Chinese valuation to align with that of MSCI Emerging Markets, eliminating long-term discounts, with a 12-month forward P/E projection of 12.5 times.

Profit turning point: First earnings exceeding expectations in three and a half years.

After 13 consecutive quarters of disappointment, the Chinese stock market has finally迎来了 its profit turning point.

According to Morgan Stanley, the MSCI Chinese Index constituents are experiencing their first quarterly earnings exceeding expectations in three and a half years. So far, the 4Q24 Earnings Reports show an 8% net positive surprise both by number of companies and by market cap weighted—this is the first time since the third quarter of 2021, ending a consecutive 13 quarters of disappointing earnings.

In the Global major markets, China's performance is also quite impressive, ranking second globally with an 8% net surprise rate, only behind Japan's 13.7%, significantly surpassing Europe, the USA, the overall Emerging Markets, and the Asia-Pacific region (excluding Japan). This performance improvement is not concentrated in a few large market cap companies but is distributed more evenly, indicating a healthier recovery trend.

Morgan Stanley pointed out that this groundbreaking change is attributed to three main factors:

The low base effect after analysts significantly lowered earnings expectations in recent years.

Firms actively implementing self-rescue measures to enhance earnings and shareholder returns.

The acceleration of Technology/AI related investments and applications.

In addition, based on the revision of profit expectations and the improvement in macroeconomic and Forex outlook, Morgan Stanley moderately adjusted its earnings growth forecasts for MSCI Chinese Index in 2025 and 2026 to 7% and 9% respectively, up from the previous 6% and 9%.

Valuation Reassessment: From Discount to Parity.

Morgan Stanley forecasts that MSCI Chinese Index is likely to align with the valuations of MSCI Emerging Markets, eliminating the long-standing discount. Currently, the recovery of ROE for MSCI Chinese Index and the easing of geopolitical risks have driven its preliminary reassessment this year (the 12-month forward PE has risen from 10.2 times to 11.6 times), and the discount to MSCI Emerging Markets has narrowed to 6%.

Morgan Stanley believes this discount should disappear for two reasons:

The earnings results and expectation correction trajectory of MSCI Chinese Index significantly outperform the overall MSCI Emerging Markets.

In the context of potential tariff increases from the USA, MSCI Chinese Index is in a relatively favorable position—due to the reciprocal tariff scheme, the space for tariffs imposed on imports from the USA by China is limited, and only about 3% of MSCI Chinese Index's revenue is exposed to the USA market, the lowest among the top ten emerging market trading partners of the USA.

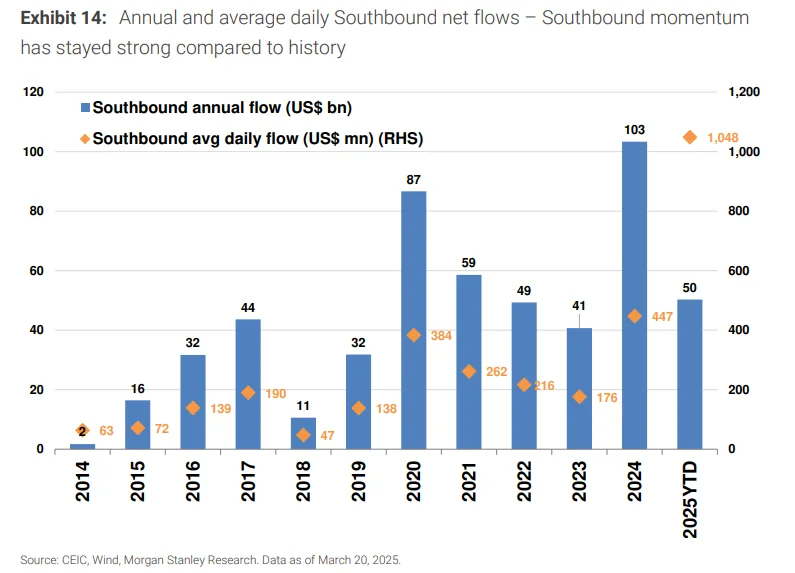

Southbound funds will continue to support Hong Kong stocks.

Southbound funds have become a stable support force for the Hong Kong stock market. In 2024, it set a record for annual net inflow of over 100 billion USD, and momentum has been stronger in 2025, achieving a net inflow of 50 billion USD in less than three months, with an average daily net inflow reaching 1 billion USD, more than double the record set in 2024.

Morgan Stanley believes that two major factors support the continued inflow of Southbound capital:

The Chinese government clearly supports the stability and prosperity of Hong Kong's capital markets, including a series of supportive measures announced by the central bank.

The Hong Kong market's greater exposure to the Internet and Technology provides a more direct option for investors seeking AI and technological innovation.

Is investing always stepping on a landmine?Futubull AI is officially launched!Providing precise answers, comprehensive insights, and grasping key opportunities!

Is investing always stepping on a landmine?Futubull AI is officially launched!Providing precise answers, comprehensive insights, and grasping key opportunities!

Editor/jayden

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(14)

Reason For Report