事实上,如果人们从事后回顾昨日的这个美联储议息日,不难发现,有着“新美联储通讯社”之称的著名记者Nick Timiraos在此次会议前对鲍威尔已沦为“不鸽不鹰的鸭子”的比喻,可谓是非常正确的——正如同知名财经博客网站Zerohedge所总结的,

事实上,如果人们从事后回顾昨日的这个美联储议息日,不难发现,有着“新美联储通讯社”之称的著名记者Nick Timiraos在此次会议前对鲍威尔已沦为“不鸽不鹰的鸭子”的比喻,可谓是非常正确的——正如同知名财经博客网站Zerohedge所总结的,

① Three years later, the term "transitory" was again used by Powell on the Federal Reserve's interest rate day to describe inflation, a moment that perhaps made many on Wall Street feel rather nostalgic; ② It seems that inspired by the "Powell Put Options," the three major US stock indices also saw significant gains on Wednesday, marking the strongest interest rate day performance in eight months.

According to Caixin, on March 20, editor Xiaoxiang reported that three years later, the term "transitory" was again used by Powell on the Federal Reserve's interest rate day to describe inflation, a moment that perhaps made many on Wall Street feel rather nostalgic.

And it seems that inspired by the "Powell Put Options" (the Federal Reserve supporting the stock market), the three major US stock indices also saw significant gains on Wednesday, marking the strongest interest rate day performance in eight months.

In fact, if people review yesterday's Federal Reserve interest rate day retrospectively, it is not difficult to find that the well-known journalist Nick Timiraos, known as the "new Federal Reserve correspondent," accurately described Powell as having become a "duck that is neither dovish nor hawkish" before this meeting—just as the well-known financial blog Zerohedge summarized, the hawkish-dovish signals from last night’s Federal Reserve interest rate night were actually intertwined, especially during the formal decision announcement at 2 a.m.:

In fact, if people review yesterday's Federal Reserve interest rate day retrospectively, it is not difficult to find that the well-known journalist Nick Timiraos, known as the "new Federal Reserve correspondent," accurately described Powell as having become a "duck that is neither dovish nor hawkish" before this meeting—just as the well-known financial blog Zerohedge summarized, the hawkish-dovish signals from last night’s Federal Reserve interest rate night were actually intertwined, especially during the formal decision announcement at 2 a.m.:

Monetary policy statement: Hawkish

The Federal Reserve removed the statement that "the risks to achieving employment and inflation targets are broadly balanced," instead stating that the uncertainty related to the economic outlook has increased.

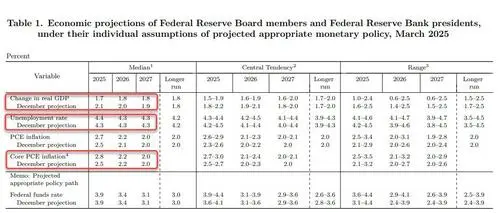

SEP economic forecast: Mixed (Stagflation)

The Federal Reserve significantly lowered its GDP growth forecast for the USA this year, while raising its forecasts for inflation and unemployment. Goldman Sachs pointed out that a notable conclusion is the "stagflation factors" in the SEP.

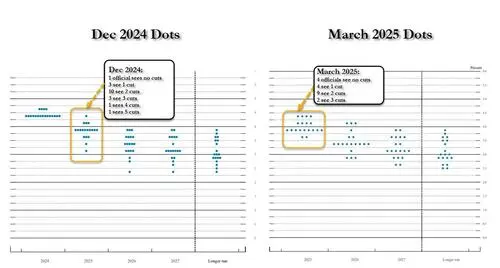

Dot plot: Hawkish

The Federal Reserve's dot plot in March continues to predict two rate cuts in 2025. However, as mentioned in the Goldman Sachs report referenced in our outlook, the specific dot distribution for interest rates this year has shifted upward. Of the 19 officials, as many as 4 now believe there will be no rate cuts in 2025, 4 expect one rate cut, 9 expect two rate cuts, and 2 expect three rate cuts.

QT reduction: Dovish

The Federal Reserve announced it will begin to further slow the pace of balance sheet reduction starting April 1. The reduction cap for U.S. Treasuries will slow from $25 billion/month to $5 billion/month, while the cap for mortgage-backed securities (MBS) will remain at $35 billion/month.

All the potential changes and information points mentioned above were almost all referenced in our outlook yesterday.

However, what might really have the biggest impact on the market last night was perhaps not all of the aforementioned details that drew attention beforehand. Instead, it was Powell's description of the impact of tariffs at the post-meeting press conference.

On the first Federal Reserve meeting day after Trump kicked off Tariff War 2.0, Powell almost completely did not avoid the impact of Trump's tariffs. The Fed Chair unequivocally stated that Trump's trade agenda is likely to drive up prices, although there remains considerable uncertainty about how much they will rise and whether the price changes will be "temporary".

Powell stated that it is difficult to analyze the extent to which inflation is driven by tariffs, but the Fed will attempt to clarify this: "Clearly a part of it, a large part comes from tariffs." Powell believes it is still too early to determine whether the initial inflation impact related to tariffs can be ignored.

He pointed out that if long-term inflation expectations can be well controlled, the Federal Reserve can ignore the "one-time shock" from policies like tariffs.

Among Powell's overnight statements, the most notable was the following sentence: "If inflation would rapidly disappear without our action, if it is temporary, then it is appropriate to ignore inflation. The situation with tariff inflation might be like this. I believe it depends on whether we can quickly get through tariff inflation." Powell认为 the current base case is that any price increases due to Trump's tariff policy will be "temporary."

In fact, most Wall Street professionals may already be familiar with the Federal Reserve's description of inflation as temporary. Because during the pandemic, officials often used this term—at that time, they thought the supply constraints driving price increases would relatively quickly disappear. In April 2021, the term transitory was first included in the Federal Reserve monetary policy statement.

However, ultimately, the Federal Reserve's judgment at that time was clearly wrong. After that, inflation in the USA soared like a runaway horse, reaching a rare height of over 9% in the summer of 2022.

Now, when the term "temporary" returns to Powell's vocabulary, the only two notable differences from three years ago seem to be: this time, the subject of Powell's description has shifted from "pandemic inflation" to "tariff inflation." With the lesson learned from three years ago, Powell is not very confident that his hypothesis about inflation being "temporary" will truly hold this time. He repeatedly stated that the exact impact of tariffs on prices is uncertain.

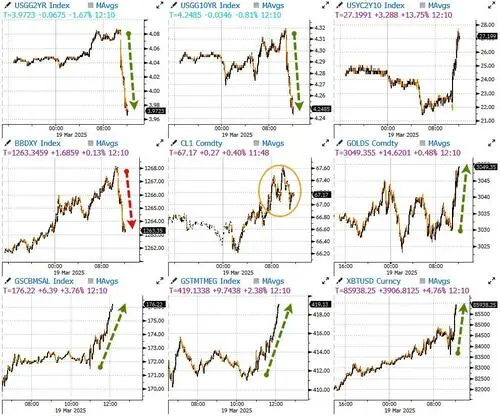

However, it is clear that the American Financial market was still very excited about Powell's statements overnight. It is not hard to see that the simultaneous rise in US stocks and bonds yesterday was concentrated mainly during Powell's news conference at 2:30 AM, especially after Powell's remarks regarding the impact of tariffs...

Adam Crisafulli, founder of Vital Knowledge, stated that regardless, given the changes in balance sheet reduction and Powell's view that tariffs would only have a "temporary" impact on inflation, Wednesday's Federal Reserve decision was undoubtedly a net positive for the market.

However, the Federal Reserve's use of the weighty term transitory again has undoubtedly immediately sparked some criticism from within the industry.

The renowned economist Mohamed A. El-Erian stated on social media on Wednesday, "I thought, especially after the significant policy missteps at the beginning of this decade, that given the current uncertainties, some Federal Reserve officials would behave more humbly."

Regarding the signals conveyed by the Federal Reserve's decision on Wednesday, Dan Siluk, the Global Short-Term and Liquidity Head and Portfolio Manager at Janus Henderson, stated in an email declaration, "The Federal Reserve's stance is 'slightly less hawkish than many on Wall Street expected.' The downward revision of growth expectations and the upward revision of the unemployment rate seem to overshadow the impact of the upward revision of inflation expectations."

Scott Colyer, the CEO of Advisors Asset Management, said on the phone, "Traders have seen through the concerns of stagflation, as officials are still easing policies. The Federal Reserve is signaling to the market that if economic growth is impacted by tariffs and rising unemployment, central bank officials are preemptively addressing any potential liquidity issues that may arise in the future."

Additionally, Charlie Ripley, a senior investment strategist at Allianz Investment Management, believes that while the results of this meeting roughly align with market participants' expectations, they clearly illustrate the dilemma the Federal Reserve faces in balancing growth and inflation expectations. On the other hand, the Federal Reserve's plan to begin slowing down the reduction of its balance sheet has somewhat reassured the market.

Editor/danial

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(1)

Reason For Report