在上周,所谓的“美股七巨头”(即Magnificent Seven)的整体企业估值——衡量标准为“预期市盈率”,大幅降至去年9月以来的最低水平,这一剧烈的变化同时也发生在标普500指数较近期最高点下跌10%跌入所谓的“回调区域”之际。

在上周,所谓的“美股七巨头”(即Magnificent Seven)的整体企业估值——衡量标准为“预期市盈率”,大幅降至去年9月以来的最低水平,这一剧烈的变化同时也发生在标普500指数较近期最高点下跌10%跌入所谓的“回调区域”之际。

The valuations of the major technology giants in the USA have reached a several-month low; however, caution among traders has led them to hold back, and they have not collectively opted for "buying on dips." After the sharp decline, although the valuations of the "seven giants" in the USA have dropped significantly, it seems that the buyers are aligning with "the east rises while the west falls."

According to Smart Financial APP, in the recent wave of market sell-offs, the stock prices of major American technology companies have indeed plummeted, with their valuations significantly retreating from the recent historical highs. However, many Wall Street traders still believe that the overall downward trend of these tech giants' stock prices has not yet ended, and the recent historical trends and price correction trajectories provide strong support for their cautious predictions.

Additionally, it is worth noting that after the emergence of DeepSeek, Chinese tech giants have risen strongly, igniting a global influx of funds towards Chinese tech behemoths and the Chinese stock market. Wall Street traders, who maintain a cautious stance on the 'Magnificent Seven' of the U.S. stock market and the S&P 500 Index, which has a high weighting of these giants, seem reluctant to heavily 'buy on dips' in the American tech giants and have instead started embracing the 'China AI investment frenzy,' following the so-called trend of 'the East rising and the West falling.'

Last week, the overall enterprise valuation of the so-called 'Magnificent Seven' (the seven giants of the American stock market) — measured by 'expected PE ratio' — dropped significantly to the lowest level since September of last year. This dramatic change coincided with a drop of 10% from the recent peak of the S&P 500 Index into what is referred to as the 'correction zone.'

Last week, the overall enterprise valuation of the so-called 'Magnificent Seven' (the seven giants of the American stock market) — measured by 'expected PE ratio' — dropped significantly to the lowest level since September of last year. This dramatic change coincided with a drop of 10% from the recent peak of the S&P 500 Index into what is referred to as the 'correction zone.'

However, the overall valuation of the 'Magnificent Seven' is still quite distant from the low valuations during the profit pressures of 2018 and 2022, while the uncertainties faced by the American stock market are continuously increasing. Moreover, both the professional trading forces on Wall Street focusing on 'buying on dips' strategies and retail investors seem increasingly interested in the 'Chinese tech giants' (such as the top ten Chinese tech companies) whose valuations are still much lower than those of the 'Magnificent Seven' and who have seen a dramatic turnaround in profit outlook thanks to strong Chinese policy support following the emergence of DeepSeek. This is also why the Nasdaq Composite Index has fallen for four consecutive weeks — the continuous decline hints that the massive buying force that has long engaged in the 'buying on dips' strategy has not materialized as expected.

Is the once-reliable 'buying on dips' strategy in the U.S. stock market failing this time? The cheapest 'seven giants' in months have failed to attract dip buyers.

Violeta Todorova, a senior research analyst at Leverage Shares, stated: 'While I acknowledge that valuations are much better than in December of last year, I do not believe this is the bottom. I considered the 'buying on dips' strategy, but there are still too many uncertainties in the U.S. stock market, and I believe the actual situation of the Magnificent Seven will deteriorate further before it improves.'

According to the latest data tracking by Institutions, the so-called "seven giants of the US stock market"—namely Apple, Microsoft, NVIDIA, Google's parent company Alphabet, Amazon, Facebook's parent company Meta Platforms, and Tesla—currently have an overall valuation of 26 times the expected profits for the next 12 months (which means a PE of up to 26x). This indicates that the valuations of these stocks have considerable room for decline compared to the low valuation periods of 2018 and 2022 (approximately 19x expected PE).

Statistics show that the Nasdaq 100 Index, which includes the strongest fundamentals of component stocks and covers the top technology companies in the USA, has rebounded for 6 trading days since reaching a historical high 17 trading days ago, but so far, these increases have not been sustained, confirming that the large buy orders have not arrived as expected, and part of the buying force has chosen to exit quickly after taking profits, rather than choosing to hold firmly for the long term like the buy-low camp in the US stock market in the past.

Despite a significant rebound in stock prices last Friday, the Nasdaq Composite Index, dominated by Technology stocks, still accumulated a decline of 2.5% last week and has fallen 11% from the historical high in February. Even from a weekly decline perspective, the Nasdaq has fallen for four consecutive weeks, with the largest-weighted company, Apple, recording its largest weekly drop in two years.

This decline starkly contrasts with the extremely optimistic scenario of the US stock market a month ago. At that time, investors were optimistic about the policies introduced by the Trump administration to promote economic growth and deregulation, continuously pushing the stock prices of Alphabet, Amazon, and Tesla to new historical highs. However, as Trump and other cabinet officials clearly stated their willingness to accept short-term economic difficulties and stock market losses to achieve long-term goals of reshaping the US economy, these expectations have completely collapsed. Trump even emphasized that "one cannot only focus on the stock market"—which is entirely contrary to his long-standing support for US stocks reaching new highs.

The series of new foreign tariff policies recently announced by Trump, who is returning to the presidency for his second term, has severely hit the confidence index of US enterprises and consumers, significantly raising consumer inflation expectations and recession expectations. This has led global Institutions and individual investors to become increasingly cautious about investing in the US market. Since February, when the new US government led by Trump has fully focused on foreign tariff policies, an increasing amount of global funds have fled the US stock market.

The market had eagerly anticipated that the so-called "Trump Put Options" would significantly boost the underperforming US stock market this year, but neither Trump nor US Treasury Secretary Mnuchin has revealed any supportive or reassuring stance toward the US stock market. Instead, they emphasized that as the US economy will free itself from dependence on government spending, it may inevitably experience a "detox" period.

Trump himself stated that the US economy will undergo a "transition period," with tariffs inevitably causing "disturbances," emphasizing that tariffs are meant to make America strong again and to "Make America Great Again." Last week, Trump once again downplayed market concerns about a recession in the USA, predicting that the country will not fall into a recession. He said at the White House: "I don't see any signs of a recession. I believe this country will prosper." Trump also added: "You can't just focus on the stock market; it will go up and down. But you know what? We have to rebuild our country."

In response, investors began to withdraw from US risk assets, aggressively selling off the best-performing tech giants in the long bull market in US stocks that began in October 2022 to realize profits. At the same time, the immense uncertainty brought by the Trump administration, particularly the significant pressure on the macroeconomic level, caused investors to remain cautious instead of choosing to "buy on dips" as usual.

Over the past decade, investors have repeatedly learned from investment experience that choosing to 'Buy on Dips' when large-cap technology stocks experience a pullback usually yields substantial returns.ROIEven during the long-term downturn in 2022 when the Nasdaq Composite Index plummeted more than 33%, it ultimately proved to present multiple excellent buying opportunities, with severely undervalued stocks like Meta Platforms reaching new historical highs in the following two years.

"The AI investment frenzy in China" is sweeping the globe! Moreover, the tech giants from the East are valued much lower.

However, as the widespread global trade war initiated by President Trump raises concerns about "stagflation" or even a deep recession in the USA, these buying opportunities, along with broader global investors' hesitation to "buy on dips" for US stocks, have found a new investment direction: the Chinese stock market, which boasts favorable valuations, strong fundamentals, and AI capabilities comparable to those of the USA.

For a long time, the investment community has almost unanimously believed that the tech giants in the USA remain the highest quality companies globally, possessing market dominance, incredible profitability, and ample cash reserves. But the current question is whether these advantages have already been reflected in current stock prices. With current valuations being much higher compared to the historical crash period in 2022, particularly as the US economy slows, corporate investments in AI may not meet expectations, and given the strong rise of Chinese tech giants with more favorable valuations and strong profit potential this year, this advantage may be under threat.

For the Chinese stock market—which includes the Hong Kong and A-share markets—DeepSeek's groundbreaking launch of a "super low-cost AI big model" is driving deep penetration of big models across various industries in China. Additionally, Alibaba's strong performance and its ambitious "AI super blueprint" have become unprecedented "bull market catalysts" for global investors to reassess Chinese assets, who had already expressed concerns about the increasingly high valuations of US tech stocks.

With the comprehensive rise of China's AI startup DeepSeek, leading a new "AI large model computing paradigm" centered on "ultra-low cost" and high efficiency comparable to OpenAI, DeepSeek has begun deep integration with various industries such as healthcare, finance, and education, as well as innovations in AI products/services brought about by applications in Consumer Electronics. This is expected to drive the sales and operating profits of China's Semiconductors, Saas, Cloud Computing, and all industries into a new growth paradigm, ultimately boosting global investors' bullish sentiment towards the Chinese stock market, especially tech stocks. Looking at the investment returns of global hedge funds so far this year, the secret or key to outperforming peers since 2025 seems to be solely one guideline: allocate towards Chinese tech stocks.

The "Ten Giants of Technology" in China (Ternific 10), which include Alibaba, Tencent, Meituan, Xiaomi, BYD, JD.com, NetEase, Baidu, Geely, and Semiconductor Manufacturing International Corporation, since February have been propelled by the domestic AI large model deployment frenzy brought on by DeepSeek. The market generally believes these ten Chinese giants will be the core beneficiaries of the global AI craze, pushing their stock prices to significantly exceed the long-term bull market of the "Seven Giants" in the USA since 2023. Jeff Wenig, head of stock strategies at WisdomTree Asset Management, bluntly stated in a February tweet that the "Seven Giants" of the US are making way for the "Ten Giants of Chinese Technology."

Wall Street giant Bank of America stated that USA tech stocks are overvalued and overly held compared to Chinese tech stocks. The bank expects a large rotation from the 16 trillion dollar market cap "Seven Giants" of the USA to the 1 trillion dollar market cap "BATX" in China (Baidu, Alibaba, Tencent, Xiaomi).

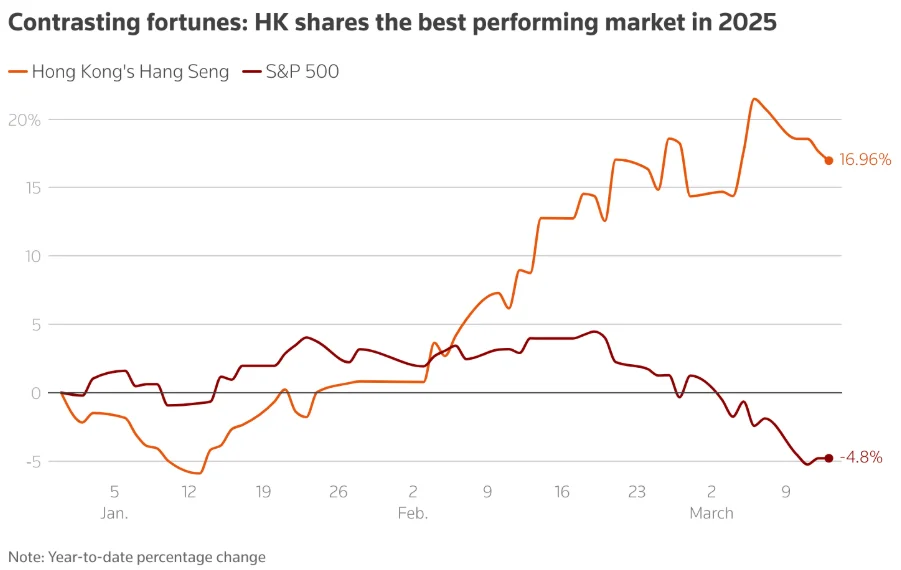

Since the beginning of this year, the Hang Seng TECH Index, which includes Chinese tech giants like Alibaba, Tencent, and Xiaomi, has skyrocketed over 30%, while the S&P 500 Index, which has dropped nearly 5% and fallen into a correction area this year, appears extremely weak.

From the perspective of index valuation, according to LSEG statistics, even after the surge since February, the expected PE ratio of the Hong Kong Hang Seng Index over a 12-month period is only 7x (the expected PE ratio is a commonly used indicator to measure stock valuation). In contrast, even during a technical correction, the expected PE ratio of the S&P 500 Index, which is heavily weighted towards the "Seven Giants," remains as high as 20x.

Société Générale research reports show that the valuation premium of China's "Seven Tech Giants" has dropped from 115% before 2021 to about 55% currently. This is still about 20 percentage points lower than the average premium over the past five years. Compared to the US "Seven Giants," China's "Seven Tech Giants" face a greater degree of valuation discount, currently about 45%. The "Seven Giants" referenced by Société Générale are Tencent, Alibaba, Xiaomi, BYD, Semiconductor Manufacturing International Corporation, JD.com, and NetEase.

According to Art Hogan, chief market strategist at B. Riley Wealth: "Currently, no one is willing to recklessly bottom-fish the US 'Seven Giants' to catch falling knives, as the US market is filled with too much uncertainty, which is why we have yet to see any sustained nature of a rebound."

Although the 'Seven Giants' of the USA generally exceeded expectations in their Q4 results, Wall Street analysts have recently significantly lowered these giants' earnings expectations for 2025, primarily based on the logic that the 'tariff war' initiated by Trump will drive costs significantly up, affecting global market profits. According to Bloomberg Intelligence forecasts, the profit growth expectation for the 'Seven Giants' of the US in 2025 has dropped from 24% in mid-January to around 20%, whereas the overall profit growth for the 'Seven Giants' in 2024 is as high as 34%. In contrast, the expected profit growth rate for the components of the S&P 500 Index overall this year is 12%, above last year's 10%.

From the recent developments of the 'Big Seven' of the USA stock market, each company's situation is different. For instance, Tesla has always been an exception; it has the smallest scale among the seven giants, the lowest profit margin, but the highest valuation, mainly due to the high attention from investors towards CEO Elon Musk. Despite a 48% drop in Tesla's stock price over the past three months, its valuation still stands at 82 times the expected profit.

In contrast, Apple, with the second highest valuation, appears more conservative, currently valued at 29 times expected profits, but still close to historical highs. The fundamental outlook for Apple has been significantly downgraded by Analysts due to a sharp decline in sales in the Chinese market and cost surge due to tariff factors. The lowest valuation among the 'Big Seven' is Alphabet, at about 18x. Nevertheless, even Alphabet's current valuation is still much higher than the lows during the crash in 2022.

Bullish investors have their own arguments. The 14-day relative strength index of the "Big Seven" index of US stocks (the Bloomberg Mag 7 index) RSI, a measure of momentum Technical Indicators) recently fell below 24, the lowest point since 2019, and far below the typical level indicating oversold conditions of 30 points. Although it has since rebounded to 36, it is still well below the level that represents "overbought" at 70 points.

According to Leverage Shares' Todorova, despite the selling tide, the fundamental reasons supporting large tech stocks have not significantly changed, and it may only be a matter of time before investors return to this sector. She stated: 'The current situation is more about the macro and geopolitical environment rather than a drastic deterioration in these companies' fundamentals. In the coming months, we will have more clarity on the Federal Reserve's monetary policy plans and the state of the US economic growth. If the market begins to recover at that time, I think the 'Big Seven' will once again outperform the Large Cap of the USA stock market.'

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(1)

Reason For Report