Here's Why We Think Griffon (NYSE:GFF) Might Deserve Your Attention Today

Here's Why We Think Griffon (NYSE:GFF) Might Deserve Your Attention Today

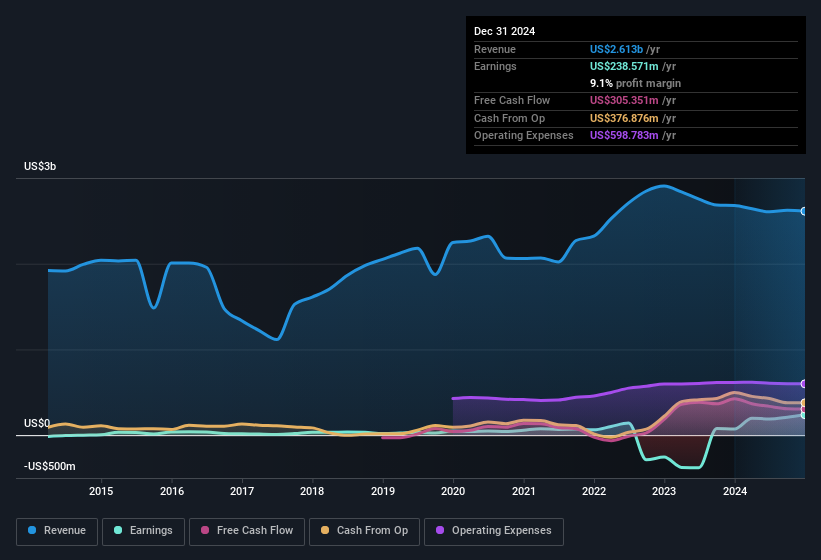

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. We note that while EBIT margins have improved from 15% to 17%, the company has actually reported a fall in revenue by 2.5%. That's not a good look.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. We note that while EBIT margins have improved from 15% to 17%, the company has actually reported a fall in revenue by 2.5%. That's not a good look.

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

許多投資者,尤其是那些缺乏經驗的投資者,通常會購買故事好的公司的股票,即使這些公司處於虧損狀態。但正如彼得·林奇在《超越華爾街》中所說,'長線投資幾乎從未獲得回報。' 虧損的公司總是在與時間賽跑,以達到財務可持續性,因此在這些公司投資的投資者可能承擔的風險超出了他們應該承擔的範圍。

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Griffon (NYSE:GFF). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Griffon with the means to add long-term value to shareholders.

如果這種公司不是你的風格,你喜歡能生成營業收入甚至獲利的公司,那麼你可能會對格里豐(紐交所:GFF)感興趣。即使這家公司在市場上被合理評估,投資者也會同意,持續產生穩定利潤將繼續爲格里豐提供增加長期股東價值的手段。

Griffon's Improving Profits

格里豐在利潤上的改善

In business, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS) performance. So a growing EPS generally brings attention to a company in the eyes of prospective investors. Commendations have to be given in seeing that Griffon grew its EPS from US$1.39 to US$5.02, in one short year. While it's difficult to sustain growth at that level, it bodes well for the company's outlook for the future.

在業務中,利潤是成功的重要指標;而股票價格往往反映每股收益(EPS)的表現。因此,增長的EPS通常會引起潛在投資者對公司的關注。值得讚揚的是,格里豐在短短一年內將其EPS從1.39美元增長到5.02美元。雖然在這樣的水平上保持增長是困難的,但這對公司的未來前景是個好兆頭。

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. We note that while EBIT margins have improved from 15% to 17%, the company has actually reported a fall in revenue by 2.5%. That's not a good look.

查看息稅前利潤(EBIT)Margin和營業收入增長通常是有幫助的,這樣可以更全面地評估公司的增長質量。我們注意到,雖然EBIT Margin已經提高從15%到17%,但公司實際報告營業收入下降了2.5%。這看起來不是很好。

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

下面的圖表展示了公司的營業收入和凈利潤隨時間的變化情況。 點擊圖表查看具體數字。

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Griffon's future profits.

你開車時並不看後視鏡,所以你可能更有興趣查看這份免費報告,其中顯示了分析師對格里豐未來利潤的預測。

Are Griffon Insiders Aligned With All Shareholders?

格里豐的內部人士與所有板塊股東一致嗎?

It's a necessity that company leaders act in the best interest of shareholders and so insider investment always comes as a reassurance to the market. So it is good to see that Griffon insiders have a significant amount of capital invested in the stock. We note that their impressive stake in the company is worth US$247m. Holders should find this level of insider commitment quite encouraging, since it would ensure that the leaders of the company would also experience their success, or failure, with the stock.

公司領導者以股東的最大利益行事是必要的,因此內部投資總是能給市場帶來安心。因此,看到格里豐的內部人士在股票上投入了大量資金是好事。我們注意到,他們在公司的可觀持股價值爲24700萬美元。持有者應該會對這種內部承諾感到相當鼓舞,因爲這將確保公司的領導者與股票的成功或失敗一起經歷。

Is Griffon Worth Keeping An Eye On?

格里豐值得關注嗎?

Griffon's earnings have taken off in quite an impressive fashion. That sort of growth is nothing short of eye-catching, and the large investment held by insiders should certainly brighten the view of the company. The hope is, of course, that the strong growth marks a fundamental improvement in the business economics. Based on the sum of its parts, we definitely think its worth watching Griffon very closely. However, before you get too excited we've discovered 2 warning signs for Griffon that you should be aware of.

格里豐的盈利增長非常顯著。這種增長無疑引人注目,內部人士的大量投資也應該使人們對公司有更好的看法。當然,希望這種強勁增長標誌着業務經濟的根本改善。根據各部分的總和,我們絕對認爲值得密切關注格里豐。然而,在你過度興奮之前,我們發現了2個你應該注意的關於格里豐的警告信號。

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in the US with promising growth potential and insider confidence.

雖然選擇沒有增長收益和缺乏內部人買入的股票可能會產生結果,但對於重視這些關鍵指標的投資者,這裏有一份經過精心挑選的美國公司名單,這些公司具有良好的增長潛力和內部人信心。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

請注意,本文討論的內部交易是指在相關管轄區內可報告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋嗎?對內容有疑慮嗎?請直接與我們聯繫。或者,發送電子郵件至 editorial-team (at) simplywallst.com。

本文由Simply Wall ST撰寫,屬於一般性質。我們提供基於歷史數據和分析師預測的評論,僅使用無偏見的方法,我們的文章並不意圖提供財務建議。它不構成對買入或賣出任何股票的推薦,也未考慮您的目標或財務狀況。我們旨在提供基於基本數據的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall ST在提到的任何股票中沒有持倉。

譯文內容由第三人軟體翻譯。

,而今天在早盤衝高至24000附近入了熊仔后,指數大幅下跌最多接近6百多點,即時把昨日虧損賺回有突多

,而今天在早盤衝高至24000附近入了熊仔后,指數大幅下跌最多接近6百多點,即時把昨日虧損賺回有突多

,而今天再破新高, 最高 24076 , 其後收市時轉跌約70點, 出了陰燭, 暫時走勢仍未有破壞, 不過由前底至今已經上漲接近至6千點, 本人覺得有貨者可以繼續持貨直到 明顯有走勢轉壞才止賺離場, 沒貨者可以等待回調后再上車, 其實本人也希望能夠快點有回調, 一來可以上車, 二來回一回氣也健康

,而今天再破新高, 最高 24076 , 其後收市時轉跌約70點, 出了陰燭, 暫時走勢仍未有破壞, 不過由前底至今已經上漲接近至6千點, 本人覺得有貨者可以繼續持貨直到 明顯有走勢轉壞才止賺離場, 沒貨者可以等待回調后再上車, 其實本人也希望能夠快點有回調, 一來可以上車, 二來回一回氣也健康 ,暫時看法都是跟之前一樣, 覺得即使有所回調應該都不會跌得太深,但假若期貨失守22350企不穩收,便可能還有下跌空間, 期貨短期要跌破21400的機會應該也不大, 所以本人覺得如果有大幅的回調也是一個機會分注做多。近日都堅持不過夜持倉,暫只做即市, 因為不高追,也不隨便做空。

,暫時看法都是跟之前一樣, 覺得即使有所回調應該都不會跌得太深,但假若期貨失守22350企不穩收,便可能還有下跌空間, 期貨短期要跌破21400的機會應該也不大, 所以本人覺得如果有大幅的回調也是一個機會分注做多。近日都堅持不過夜持倉,暫只做即市, 因為不高追,也不隨便做空。支持阻力以現貨作參考

支持位 23150,23250,2...

評論(0)

請選擇舉報原因