Neuronetics, Inc. (NASDAQ:STIM) shares have continued their recent momentum with a 30% gain in the last month alone. But the last month did very little to improve the 56% share price decline over the last year.

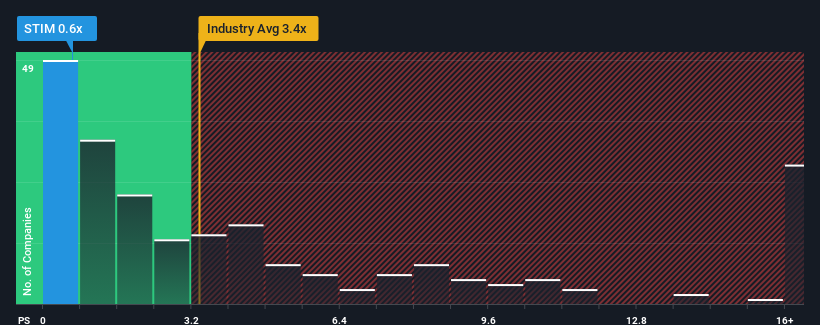

Even after such a large jump in price, Neuronetics may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.6x, since almost half of all companies in the Medical Equipment industry in the United States have P/S ratios greater than 3.4x and even P/S higher than 9x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

NasdaqGM:STIM Price to Sales Ratio vs Industry January 9th 2025

How Has Neuronetics Performed Recently?

Recent times haven't been great for Neuronetics as its revenue has been rising slower than most other companies. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Neuronetics' future stacks up against the industry? In that case, our free report is a great place to start.

Is There Any Revenue Growth Forecasted For Neuronetics?

Neuronetics' P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Retrospectively, the last year delivered a decent 5.0% gain to the company's revenues. Pleasingly, revenue has also lifted 30% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 11% per annum as estimated by the four analysts watching the company. That's shaping up to be similar to the 9.6% per annum growth forecast for the broader industry.

In light of this, it's peculiar that Neuronetics' P/S sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

What We Can Learn From Neuronetics' P/S?

Neuronetics' recent share price jump still sees fails to bring its P/S alongside the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

It looks to us like the P/S figures for Neuronetics remain low despite growth that is expected to be in line with other companies in the industry. The low P/S could be an indication that the revenue growth estimates are being questioned by the market. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Plus, you should also learn about these 5 warning signs we've spotted with Neuronetics (including 2 which don't sit too well with us).

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Neuronetics' P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Neuronetics' P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Neuronetics的市銷率對於一個預計增長非常乏力甚至營業收入下降的公司而言是典型的,並且,重要的是,其表現遠遠低於行業板塊。

Neuronetics的市銷率對於一個預計增長非常乏力甚至營業收入下降的公司而言是典型的,並且,重要的是,其表現遠遠低於行業板塊。