Chewy Set For Over 50% Upside In Bull Case: 'Entering Beast Mode For 2025,' Says Analyst

Chewy Set For Over 50% Upside In Bull Case: 'Entering Beast Mode For 2025,' Says Analyst

Key growth drivers include Chewy's underpenetrated mobile app, which currently accounts for about 20% of revenues but could exceed 40-50% penetration over the next 12-24 months. The company's automation initiatives have already reduced order-to-delivery times by 10% while cutting fulfillment costs by 30% across 40% of volumes.

Key growth drivers include Chewy's underpenetrated mobile app, which currently accounts for about 20% of revenues but could exceed 40-50% penetration over the next 12-24 months. The company's automation initiatives have already reduced order-to-delivery times by 10% while cutting fulfillment costs by 30% across 40% of volumes.Mizuho Securities upgraded Chewy Inc. (NYSE:CHWY) to Outperform from Neutral and raised its price target to $42, representing a 13.29% increase from current price levels, citing improving pet category fundamentals and multiple growth catalysts for 2025.

瑞穗证券将Chewy Inc.(纽交所:CHWY)的评级从中立上调至跑赢大盘,并将其目标价提高至42美元,较当前价格水平上涨13.29%,理由是宠物品类基本面改善及2025年的多重增长催化剂。

What Happened: The e-commerce pet supplies retailer is poised to benefit from recovering industry trends and internal initiatives that could drive EBITDA margin expansion toward high single to double digits, according to Mizuho analyst David Bellinger.

发生了什么:这家电子商务宠物用品零售商有望受益于行业趋势的复苏和内部举措,这些措施可能会推动EBITDA利润率向高个位数到双位数扩张,瑞穗分析师大卫·贝林杰表示。

"The pet category is beginning to recover into 2025, yielding a return to net active customer growth for Chewy and a subsequent top-line re-acceleration," Bellinger wrote in a Jan. 6 research note, adding, "Chewy notches to our top pick overall and within our consumer internet vertical. Bull case suggests +50% upside."

贝林杰在1月6日的研究报告中写道:"宠物品类将开始在2025年恢复,Chewy的净活跃客户将恢复增长,后续的收入将加速,"并补充道,"Chewy是我们所有推荐中的首选,并在我们的消费互联网垂直领域中表现突出。乐观情况下暗示上涨50%。"

Key growth drivers include Chewy's underpenetrated mobile app, which currently accounts for about 20% of revenues but could exceed 40-50% penetration over the next 12-24 months. The company's automation initiatives have already reduced order-to-delivery times by 10% while cutting fulfillment costs by 30% across 40% of volumes.

主要的增长驱动因素包括Chewy尚未渗透的移动应用程序,目前占营业收入的约20%,但在未来12-24个月内有可能超过40-50%的渗透率。该公司的自动化措施已将订单到交付时间缩短了10%,同时在40%的业务量中降低了30%的履行成本。

Mizuho projects Chewy's revenue growth of 4.5% in fiscal 2025, accelerating to 7.9% in the financial year 2026 and 8.1% in the financial year 2027. The firm forecasts adjusted EBITDA margins reaching 5.5% in the financial year 2025, expanding to 6.5% in the financial year 2026 and 7.2% in the financial year 2027 – slightly ahead of consensus estimates.

瑞穗预计Chewy在2025财年的营业收入增长为4.5%,在2026财年加速至7.9%,在2027财年为8.1%。该公司预测调整后的EBITDA利润率在2025财年达到5.5%,在2026财年扩展到6.5%, 在2027财年达到7.2%——略高于市场共识预期。

Chewy gained significant attention last year when influential trader Keith Gill, known as Roaring Kitty, accumulated and later sold a stake in the company.

去年,具有影响力的交易员基思·吉尔(Keith Gill),以"咆哮的小猫"(Roaring Kitty)而闻名,积累并随后出售了对该公司的股份,从而引起了广泛关注。

Why It Matters: The upgrade follows Chewy's strong third-quarter performance, where it added approximately 160,000 net active customers. JPMorgan projects this growth could accelerate to 650,000 new customers in 2025.

这次升级是在Chewy强劲的第三季度表现之后做出的,当时该公司增加了约160,000个净活跃客户。摩根大通预计这一增长在2025年将加速到65万新客户。

Bellinger noted that concerns about higher advertising spend are "short-sighted," as the company maintains a strong return on investment metrics while investing in customer acquisition. The analyst highlighted Chewy's high revenue visibility through its Autoship subscription program, which accounts for over 80% of sales.

贝林杰指出,关于广告支出增加的担忧是"短视的",因为公司在客户获取上维持着强大的投资回报率指标。分析师强调Chewy通过其自动配送订阅计划实现了高营业收入可见度,该计划占总销售额的80%以上。

The new price target represents a multiple of 20x the financial year 2026 estimated EBITDA of $868 million, reflecting a premium to e-commerce peers given Chewy's exposure to the resilient pet category and a clear path to margin expansion. The company also has over $400 million remaining in its share buyback program.

新的价格目标代表着2026财年预计EBITDA为$86800万的20倍,反映出相比其他电子商务同行的溢价,考虑到Chewy在坚韧宠物行业的曝光和明确的利润扩张路径。该公司在股票回购计划中还有超过$40000万的资金。

Price Action: Chewy's stock closed at $37.07 on Monday, reflecting a 3.09% increase. In after-hours trading, the stock fell by 1.97%. Over the past year, Chewy has experienced a notable growth of 79.17%, according to data from Benzinga Pro.

价格走势:Chewy的股票周一收盘于$37.07,反映出3.09%的上涨。在盘后交易中,股票下跌1.97%。根据Benzinga Pro的数据,过去一年中,Chewy经历了79.17%的显著增长。

The stock's 52-week range is between $14.69 and $39.10. With a market capitalization of $14.80 billion, Chewy holds a price-to-earnings ratio of 40.29 and a relative strength index of 53.

该股票的52周区间在$14.69至$39.10之间。Chewy市值为$148亿,市盈率为40.29,相对强弱指数为53。

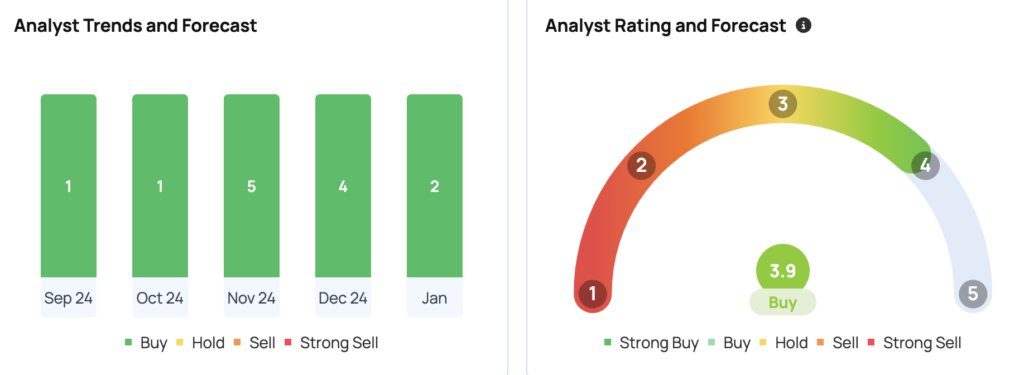

Chewy has a consensus price target of $35.19. The high target is $42, and the low is $25. Recent ratings suggest a $39 target, implying a 7.32% upside.

Chewy的共识价格目标为$35.19。最高目标为$42,最低目标为$25。近期评级建议的目标为$39,意味着7.32%的上行空间。

- Warren Buffett's Berkshire Hathaway Subsidiary Sued Over Unaffordable Loans, 2008-Style Predatory Loan Approval Tactics

- 沃伦·巴菲特的伯克希尔·哈撒韦子公司因无法负担的贷款和2008年风格的掠夺性贷款审批策略而被起诉。

Image Via Shutterstock

图片来自Shutterstock。

Disclaimer: This content was partially produced with the help of AI tools and was reviewed and published by Benzinga editors.

免责声明:本内容部分使用人工智能工具生成,并经Benzinga编辑审核发布。

译文内容由第三方软件翻译。