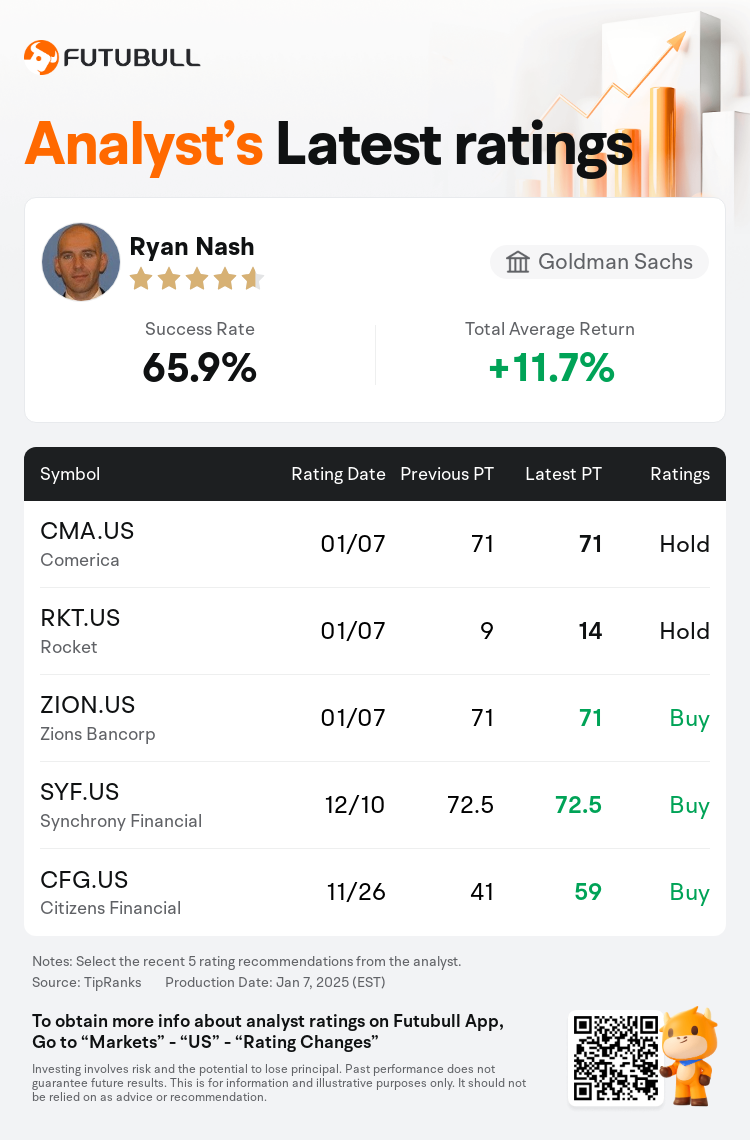

Goldman Sachs analyst Ryan Nash maintains $Comerica (CMA.US)$ with a hold rating, and maintains the target price at $71.

According to TipRanks data, the analyst has a success rate of 65.9% and a total average return of 11.7% over the past year.

Furthermore, according to the comprehensive report, the opinions of $Comerica (CMA.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $Comerica (CMA.US)$'s main analysts recently are as follows:

As the Q4 earnings season approaches for regional banks, expected trends encompass minimal growth in loans and deposits, a slight decline in net intercessor margins, and stable credit trends overall. Going forward, a key focus beyond the reported earnings will be the banks' outlooks for 2025, which are anticipated to reflect a 'higher for a bit longer' interest rate environment. The overall stance towards regional bank stocks in 2025 is optimistic, albeit moderated by the Federal Reserve's outlook on rate reductions.

Looking ahead to a more normalized environment, it is anticipated that Comerica's relative improvement in operating metrics may be slower compared to its peers. Despite the potential for tailwinds in net interest income by 2025, stemming from securities repricing and a resurgence in loan growth, challenges may persist. Particularly, the demand deposit account could continue to be a drawback in a slower rate cutting cycle, potentially impacting net interest income.

Analysts are optimistic about bank stocks as we head towards 2025, citing potential accelerations in earnings growth driven by enhanced loan growth, increased activity in capital markets, the resumption of positive operating leverage, and ongoing share buybacks. The expectation is that price-to-earnings multiples will broaden, supported by a stable economic environment, decreased regulatory burdens, elevated returns, and ongoing mergers and acquisitions. It's argued that large-cap banks may surpass market performance into 2025 due to the anticipated quickening of earnings growth.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

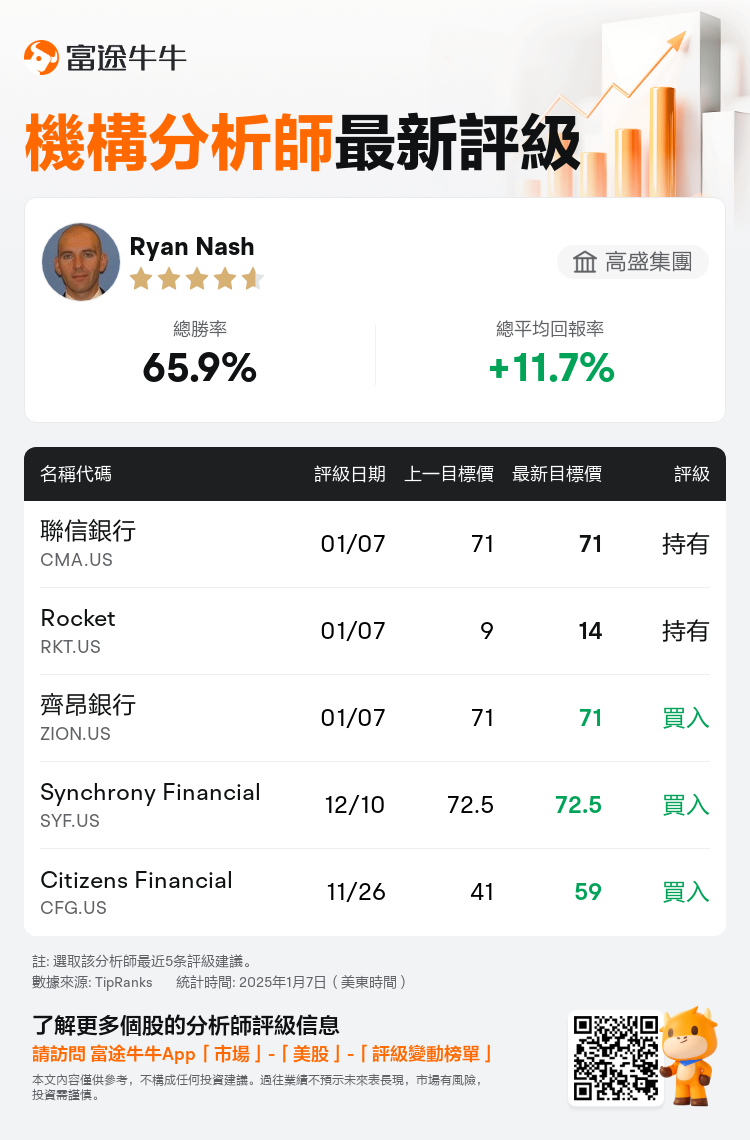

高盛集團分析師Ryan Nash維持$聯信銀行 (CMA.US)$持有評級,維持目標價71美元。

根據TipRanks數據顯示,該分析師近一年總勝率為65.9%,總平均回報率為11.7%。

此外,綜合報道,$聯信銀行 (CMA.US)$近期主要分析師觀點如下:

此外,綜合報道,$聯信銀行 (CMA.US)$近期主要分析師觀點如下:

隨着地區銀行第四季度業績季的臨近,預期的趨勢包括貸款和存款的最小增長,淨中介利潤率略有下降以及總體信貸趨勢穩定。展望未來,除了公佈的收益外,銀行對2025年的展望將是一個關鍵的焦點,預計這些展望將反映 「在更長的時間內更高」 的利率環境。儘管受到聯儲局減息前景的緩和,但2025年對區域銀行股的總體立場還是樂觀的。

展望更加正常化的環境,預計Comerica在運營指標方面的相對改善可能比同行要慢。儘管由於證券重新定價和貸款增長的復甦,到2025年淨利息收入有可能出現不利影響,但挑戰可能仍然存在。特別是,在較慢的減息週期中,活期存款賬戶可能會繼續成爲缺點,可能會影響淨利息收入。

在我們邁向2025年之際,分析師對銀行股持樂觀態度,理由是貸款增長加快、資本市場活動增加、正運營槓桿率恢復以及持續的股票回購推動盈利增長可能加速。人們預計,在穩定的經濟環境、減輕的監管負擔、更高的回報以及持續的併購的支持下,市盈倍數將擴大。有人認爲,由於預期收益增長將加快,大盤股銀行在2025年之前可能會超過市場表現。

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。