The Boxlight Corporation (NASDAQ:BOXL) share price has done very well over the last month, posting an excellent gain of 319%. The last 30 days bring the annual gain to a very sharp 58%.

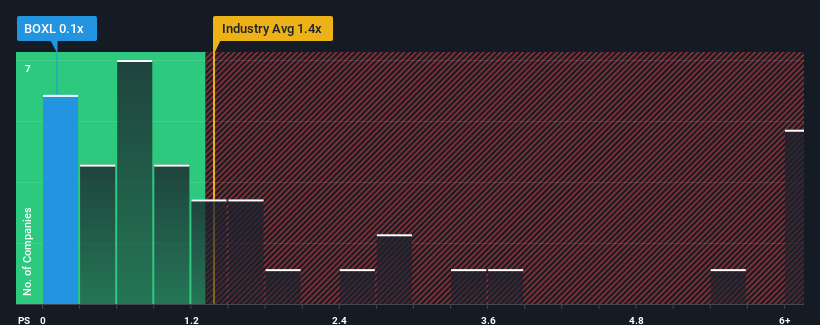

Even after such a large jump in price, Boxlight's price-to-sales (or "P/S") ratio of 0.1x might still make it look like a buy right now compared to the Tech industry in the United States, where around half of the companies have P/S ratios above 1.4x and even P/S above 4x are quite common. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

NasdaqCM:BOXL Price to Sales Ratio vs Industry January 7th 2025

How Boxlight Has Been Performing

Boxlight hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Boxlight.

Do Revenue Forecasts Match The Low P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as low as Boxlight's is when the company's growth is on track to lag the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 17%. As a result, revenue from three years ago have also fallen 13% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to slump, contracting by 3.1% during the coming year according to the three analysts following the company. With the industry predicted to deliver 6.6% growth, that's a disappointing outcome.

With this in consideration, we find it intriguing that Boxlight's P/S is closely matching its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Key Takeaway

The latest share price surge wasn't enough to lift Boxlight's P/S close to the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Boxlight's analyst forecasts revealed that its outlook for shrinking revenue is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 5 warning signs for Boxlight (3 shouldn't be ignored!) that we have uncovered.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The only time you'd be truly comfortable seeing a P/S as low as Boxlight's is when the company's growth is on track to lag the industry.

The only time you'd be truly comfortable seeing a P/S as low as Boxlight's is when the company's growth is on track to lag the industry.

你唯一能真正接受Boxlight的市銷率如此之低的情況,就是公司增長有可能落後於行業。

你唯一能真正接受Boxlight的市銷率如此之低的情況,就是公司增長有可能落後於行業。