Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Coherent Corp. (NYSE:COHR) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

What Is Coherent's Net Debt?

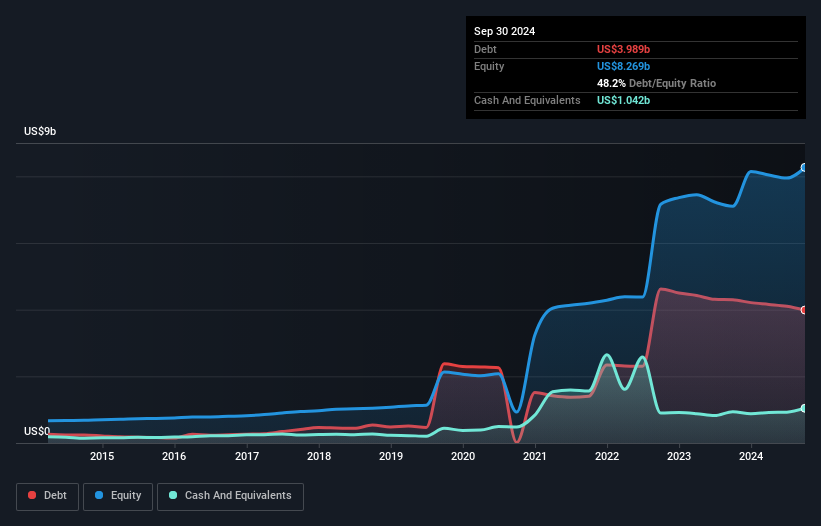

The image below, which you can click on for greater detail, shows that Coherent had debt of US$3.99b at the end of September 2024, a reduction from US$4.29b over a year. However, it does have US$1.04b in cash offsetting this, leading to net debt of about US$2.95b.

NYSE:COHR Debt to Equity History January 5th 2025

How Strong Is Coherent's Balance Sheet?

According to the last reported balance sheet, Coherent had liabilities of US$1.36b due within 12 months, and liabilities of US$5.07b due beyond 12 months. On the other hand, it had cash of US$1.04b and US$819.7m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.57b.

This deficit isn't so bad because Coherent is worth a massive US$16.4b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn't worry about Coherent's net debt to EBITDA ratio of 3.7, we think its super-low interest cover of 0.86 times is a sign of high leverage. In large part that's due to the company's significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Even worse, Coherent saw its EBIT tank 23% over the last 12 months. If earnings keep going like that over the long term, it has a snowball's chance in hell of paying off that debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Coherent's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Coherent produced sturdy free cash flow equating to 60% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

To be frank both Coherent's interest cover and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Coherent stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Coherent you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。 Simply Wall ST 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

According to the last reported balance sheet, Coherent had liabilities of US$1.36b due within 12 months, and liabilities of US$5.07b due beyond 12 months. On the other hand, it had cash of US$1.04b and US$819.7m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.57b.

According to the last reported balance sheet, Coherent had liabilities of US$1.36b due within 12 months, and liabilities of US$5.07b due beyond 12 months. On the other hand, it had cash of US$1.04b and US$819.7m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.57b.

根據上次報告的資產負債表,Coherent的負債爲13.6億美元,12個月後到期的負債爲50.7億美元。另一方面,它有10.4億美元的現金和價值8.197億美元的應收賬款將在一年內到期。因此,其負債超過其現金和(短期)應收賬款總額45.7億美元。

根據上次報告的資產負債表,Coherent的負債爲13.6億美元,12個月後到期的負債爲50.7億美元。另一方面,它有10.4億美元的現金和價值8.197億美元的應收賬款將在一年內到期。因此,其負債超過其現金和(短期)應收賬款總額45.7億美元。