Wolfe Research analyst Steven Chubak maintains $Citigroup (C.US)$ with a buy rating, and adjusts the target price from $71 to $83.

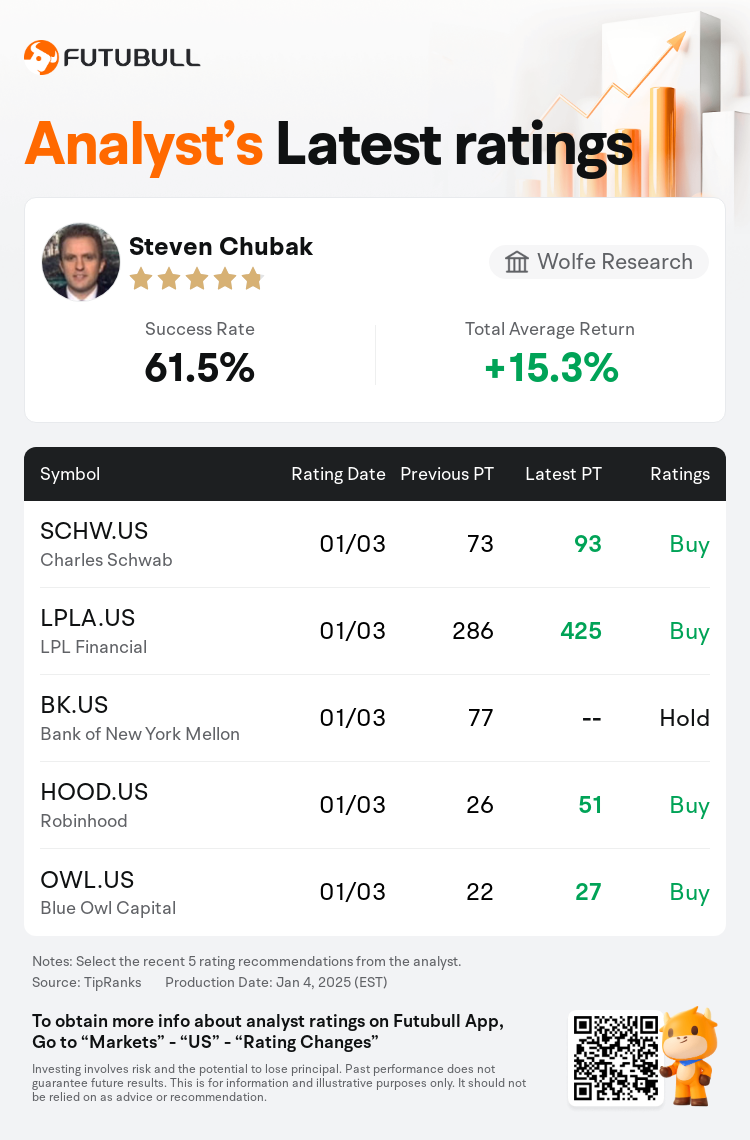

According to TipRanks data, the analyst has a success rate of 61.5% and a total average return of 15.3% over the past year.

Furthermore, according to the comprehensive report, the opinions of $Citigroup (C.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $Citigroup (C.US)$'s main analysts recently are as follows:

For the banking sector, long-term trends up to 2025 appear to be firmly in place, with only modest adjustments made to earnings projections. Looking ahead to 2028, banks are anticipated to strive for maximal growth within the boundaries of achieving a low-to-mid-teens return on tangible common equity. There remains a prevalent skepticism regarding a potential easing of regulatory and capital burdens. The sector is considered reasonably priced, presenting several investment opportunities.

Citi is considered a top choice under various scenarios excluding a recession, with expectations that expenses will surpass predictions. Pivotally, returns are anticipated to inflect significantly for the stock, with potential growth in book value even during a recession. Additionally, recent management shifts are regarded as the most substantial in decades. Over a span of three years, significant improvements are expected in earnings per share, efficiency, and returns, projecting a robust enhancement relative to peers.

Equity markets experienced a roughly 2% decline in December during a period described as a post-post-election cooldown, largely due to new expectations about the delayed likelihood of rate cuts. Additionally, a continuation of subdued activity levels was observed in investment banking from November into December, following relatively strong performance in September and October. Despite the dip in December, a rebound is anticipated at the beginning of 2025, reflecting a general sentiment that improvement in investment banking is expected eventually.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

沃爾夫研究分析師Steven Chubak維持$花旗集團 (C.US)$買入評級,並將目標價從71美元上調至83美元。

根據TipRanks數據顯示,該分析師近一年總勝率為61.5%,總平均回報率為15.3%。

此外,綜合報道,$花旗集團 (C.US)$近期主要分析師觀點如下:

此外,綜合報道,$花旗集團 (C.US)$近期主要分析師觀點如下:

對於銀行板塊,到2025年的長期趨勢似乎已經牢牢確立,只對收益預測進行了適度調整。展望2028年,預計銀行將努力在實現中低十幾的有形普通股權益回報的邊界內追求最大化增長。對於潛在的監管和資本負擔放鬆仍然存在普遍的懷疑。該板塊被認爲價格合理,提供了多種投資機會。

在不考慮經濟衰退的各種情況下,花旗被認爲是首選,預計支出將超過預測。關鍵是,股票的回報預計會顯著反彈,即使在經濟衰退期間,賬面價值也有潛在增長。此外,最近的管理層變動被視爲幾十年來最重要的。預計在三年內,每股收益、效率和回報將顯著改善,相比同行 projections出強勁提升。

在被描述爲後選舉後的降溫期,股市在12月經歷了大約2%的下跌,這主要是由於對利率下降可能延遲的新預期。此外,從11月到12月,投資銀行的活動水平繼續保持低迷,儘管9月和10月的表現相對強勁。儘管12月有所下跌,但預計將在2025年初出現反彈,反映出普遍的情緒,即最終期待到投資銀行的改善。

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。