Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Micron Technology, Inc. (NASDAQ:MU) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Micron Technology's Net Debt?

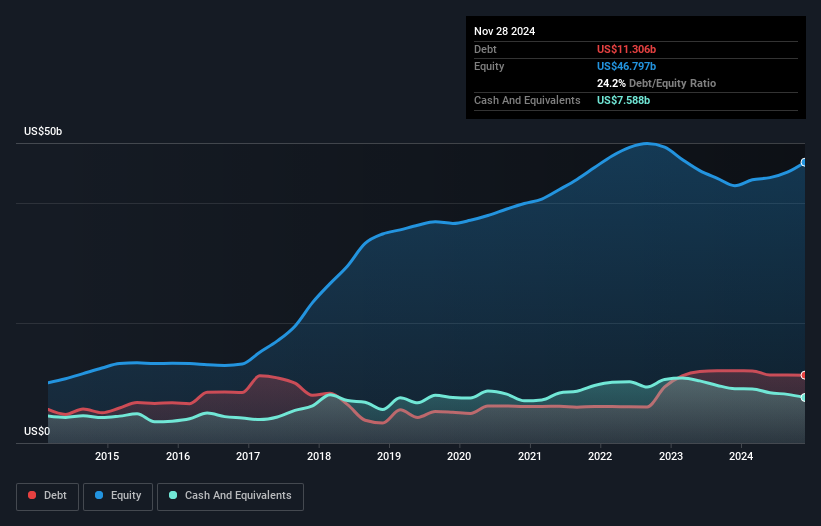

The image below, which you can click on for greater detail, shows that Micron Technology had debt of US$11.3b at the end of November 2024, a reduction from US$12.0b over a year. However, it does have US$7.59b in cash offsetting this, leading to net debt of about US$3.72b.

NasdaqGS:MU Debt to Equity History January 3rd 2025

How Strong Is Micron Technology's Balance Sheet?

According to the last reported balance sheet, Micron Technology had liabilities of US$9.02b due within 12 months, and liabilities of US$15.6b due beyond 12 months. On the other hand, it had cash of US$7.59b and US$7.42b worth of receivables due within a year. So its liabilities total US$9.65b more than the combination of its cash and short-term receivables.

Given Micron Technology has a humongous market capitalization of US$93.8b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Micron Technology's net debt is only 0.30 times its EBITDA. And its EBIT covers its interest expense a whopping 103 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. It was also good to see that despite losing money on the EBIT line last year, Micron Technology turned things around in the last 12 months, delivering and EBIT of US$4.5b. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Micron Technology's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. In the last year, Micron Technology created free cash flow amounting to 12% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Micron Technology's interest cover was a real positive on this analysis, as was its net debt to EBITDA. Having said that, its conversion of EBIT to free cash flow somewhat sensitizes us to potential future risks to the balance sheet. When we consider all the elements mentioned above, it seems to us that Micron Technology is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Micron Technology you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Howard Marks說得好,他說的不是擔心股價的波動,而是 「永久損失的可能性是我擔心的風險... 也是我認識的每位實際投資者所擔心的風險。」當你檢查公司的資產負債表的風險時,考慮它的資產負債表是很自然的,因爲企業倒閉時通常會涉及債務。重要的是,美光科技公司(納斯達克股票代碼:MU)確實有債務。但是這筆債務是股東關心的問題嗎?

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。 Simply Wall ST 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

According to the last reported balance sheet, Micron Technology had liabilities of US$9.02b due within 12 months, and liabilities of US$15.6b due beyond 12 months. On the other hand, it had cash of US$7.59b and US$7.42b worth of receivables due within a year. So its liabilities total US$9.65b more than the combination of its cash and short-term receivables.

According to the last reported balance sheet, Micron Technology had liabilities of US$9.02b due within 12 months, and liabilities of US$15.6b due beyond 12 months. On the other hand, it had cash of US$7.59b and US$7.42b worth of receivables due within a year. So its liabilities total US$9.65b more than the combination of its cash and short-term receivables.

NASDAQGS: MU 2025 年 1 月 3 日債務與股本比率的歷史記錄

NASDAQGS: MU 2025 年 1 月 3 日債務與股本比率的歷史記錄