Playa Hotels & Resorts N.V. (NASDAQ:PLYA) shares have continued their recent momentum with a 29% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 47% in the last year.

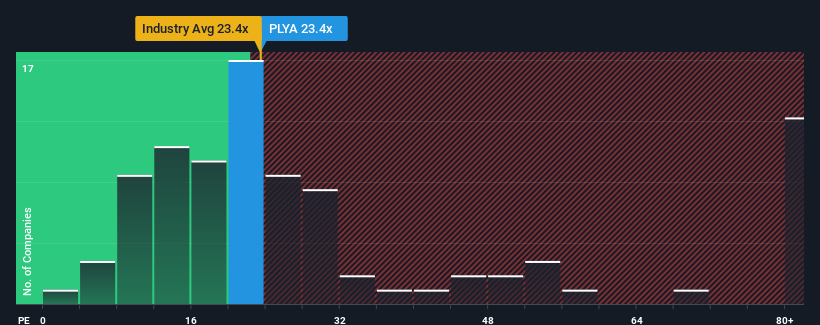

After such a large jump in price, Playa Hotels & Resorts' price-to-earnings (or "P/E") ratio of 23.4x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 18x and even P/E's below 10x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for Playa Hotels & Resorts as its earnings have been rising faster than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

NasdaqGS:PLYA Price to Earnings Ratio vs Industry January 1st 2025 Want the full picture on analyst estimates for the company? Then our free report on Playa Hotels & Resorts will help you uncover what's on the horizon.

What Are Growth Metrics Telling Us About The High P/E?

Playa Hotels & Resorts' P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 97% last year. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Looking ahead now, EPS is anticipated to slump, contracting by 2.9% during the coming year according to the five analysts following the company. Meanwhile, the broader market is forecast to expand by 15%, which paints a poor picture.

With this information, we find it concerning that Playa Hotels & Resorts is trading at a P/E higher than the market. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock at any price. There's a very good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the negative growth outlook.

The Bottom Line On Playa Hotels & Resorts' P/E

Playa Hotels & Resorts shares have received a push in the right direction, but its P/E is elevated too. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Playa Hotels & Resorts' analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings are highly unlikely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

You need to take note of risks, for example - Playa Hotels & Resorts has 2 warning signs (and 1 which is potentially serious) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Playa Hotels & Resorts' P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

Playa Hotels & Resorts' P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

Playa Hotels & Resorts的市盈率對於預計能夠實現穩健增長並且表現優於市場的公司來說是典型的。

Playa Hotels & Resorts的市盈率對於預計能夠實現穩健增長並且表現優於市場的公司來說是典型的。