Workday (NASDAQ:WDAY) Shareholders Have Earned a 9.5% CAGR Over the Last Five Years

Workday (NASDAQ:WDAY) Shareholders Have Earned a 9.5% CAGR Over the Last Five Years

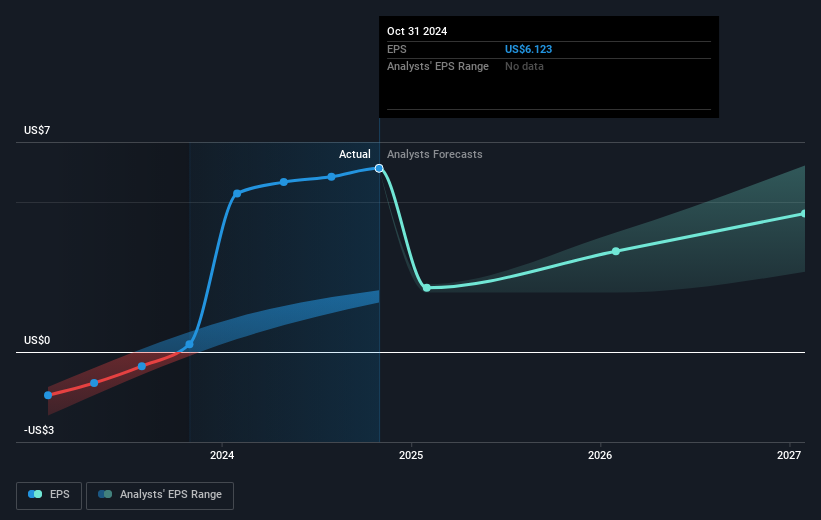

During the last half decade, Workday became profitable. That's generally thought to be a genuine positive, so investors may expect to see an increasing share price. Since the company was unprofitable five years ago, but not three years ago, it's worth taking a look at the returns in the last three years, too. Indeed, the Workday share price has gained 1.0% in three years. Meanwhile, EPS is up 264% per year. This EPS growth is higher than the 0.3% average annual increase in the share price over the same three years. So you might conclude the market is a little more cautious about the stock, these days.

During the last half decade, Workday became profitable. That's generally thought to be a genuine positive, so investors may expect to see an increasing share price. Since the company was unprofitable five years ago, but not three years ago, it's worth taking a look at the returns in the last three years, too. Indeed, the Workday share price has gained 1.0% in three years. Meanwhile, EPS is up 264% per year. This EPS growth is higher than the 0.3% average annual increase in the share price over the same three years. So you might conclude the market is a little more cautious about the stock, these days. If you buy and hold a stock for many years, you'd hope to be making a profit. Better yet, you'd like to see the share price move up more than the market average. Unfortunately for shareholders, while the Workday, Inc. (NASDAQ:WDAY) share price is up 57% in the last five years, that's less than the market return. Zooming in, the stock is actually down 3.6% in the last year.

如果你長時間買入並持有一隻股票,你希望能獲得盈利。更理想的是,你希望看到股票價格的上漲幅度超過市場平均水平。不幸的是,對於股東來說,雖然Workday, Inc.(納斯達克:WDAY)的股價在過去五年上漲了57%,但這仍低於市場回報。深入來看,該股票在過去一年實際上下跌了3.6%。

So let's investigate and see if the longer term performance of the company has been in line with the underlying business' progress.

因此讓我們調查一下,看看該公司的長期表現是否與其基礎業務的進展相符。

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

雖然一些人仍然教授有效市場假說,但已經證明市場是過於反應的動態系統,投資者並不總是理性。一個不完美但簡單的考慮市場對公司認知變化的方法是,將每股收益(EPS)的變化與股價波動進行比較。

During the last half decade, Workday became profitable. That's generally thought to be a genuine positive, so investors may expect to see an increasing share price. Since the company was unprofitable five years ago, but not three years ago, it's worth taking a look at the returns in the last three years, too. Indeed, the Workday share price has gained 1.0% in three years. Meanwhile, EPS is up 264% per year. This EPS growth is higher than the 0.3% average annual increase in the share price over the same three years. So you might conclude the market is a little more cautious about the stock, these days.

在過去的五年裏,Workday變得盈利。一般認爲這是一個真正的積極信號,因此投資者可能會期待看到股價上漲。由於公司在五年前虧損,但三年前已開始盈利,因此值得關注過去三年的回報。確實,Workday的股價在三年內上漲了1.0%。與此同時,每股收益每年增長264%。這一每股收益的增長高於同期股價平均年增幅的0.3%。所以你可能會得出市場對這隻股票目前有些謹慎的結論。

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

下面的圖像顯示了EPS隨時間的變化(如果你點擊圖像,可以看到更詳細的信息)。

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. Dive deeper into the earnings by checking this interactive graph of Workday's earnings, revenue and cash flow.

我們很高興地報告,首席執行官的薪酬比同類公司中的大多數首席執行官更爲適中。但雖然首席執行官的薪酬總是值得關注,真正重要的問題是公司是否能夠在未來實現盈利增長。通過查看Workday的盈利、營業收入和現金流的互動圖表來深入了解收益。

A Different Perspective

不同的視角

Investors in Workday had a tough year, with a total loss of 3.6%, against a market gain of about 26%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. On the bright side, long term shareholders have made money, with a gain of 9% per year over half a decade. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. Most investors take the time to check the data on insider transactions. You can click here to see if insiders have been buying or selling.

Workday的投資者經歷了艱難的一年,總虧損爲3.6%,而市場收益約爲26%。即便是好股票的股價有時也會下跌,但在過於感興趣之前,我們希望看到業務的基本指標有改善。 值得慶幸的是,長期股東在過去五年中每年獲得9%的收益,獲得了盈利。最近的拋售可能是一個機會,因此值得檢查基本數據以尋找長期增長趨勢的跡象。 大多數投資者會花時間檢查內部交易的數據。您可以點擊這裏查看內部人員是否正在買入或賣出。

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

如果你像我一樣,那麼你一定不想錯過這份內部人士正在購買的被低估的小型股免費名單。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文中引用的市場回報反映了當前在美國交易所上市股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?對內容有疑慮?請直接與我們聯繫。或者,發送電子郵件至 editorial-team (at) simplywallst.com。

這篇來自Simply Wall ST的文章是一般性的。我們根據歷史數據和分析師預測提供評論,採用無偏見的方法,我們的文章並不旨在提供財務建議。它不構成對任何股票的買入或賣出建議,也未考慮到您的目標或財務狀況。我們旨在爲您提供以基本數據驅動的長期分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall ST在提到的任何股票中均沒有持倉。

譯文內容由第三人軟體翻譯。