然而,随着线上零售的场景快速变化,消费者的购买行为逐渐从微信转移到短视频、直播、社区团购等领域,加上平台和连锁企业纷纷开发自身的电商工具如微信小店等,有赞的股价和业绩便一同“失宠”。

然而,随着线上零售的场景快速变化,消费者的购买行为逐渐从微信转移到短视频、直播、社区团购等领域,加上平台和连锁企业纷纷开发自身的电商工具如微信小店等,有赞的股价和业绩便一同“失宠”。Has the fluctuation in stock price indicated that the company has encountered growth opportunities due to a change in valuation logic?

Multiple bullish news from the WeChat ecosystem has been released in succession, driving the stock price of Youzan (08083) to show a significant increase. On December 19, the company's stock price closed up over 18%, but still remains below the 1 Hong Kong Dollar range, with the latest stock price at 0.138 Hong Kong Dollars as of the 24th.

Six years ago, when Youzan successfully went public through a backdoor listing, it was known as the "first stock of the WeChat ecosystem." During the flourishing era of micro-businesses, Youzan launched the WeChat-based e-commerce platform "Youzan Weichat Store" as a retail Saas service provider, becoming one of the first companies to benefit from the Internet Plus-Related dividends.

However, with the rapid changes in online retail scenarios, consumer purchasing behavior has gradually shifted from WeChat to Short Video, live streaming, Community Group Buying, and other fields. In addition, platforms and chain enterprises have developed their own e-commerce tools such as WeChat mini-stores, leading to a decline in both the stock price and performance of Youzan.

However, with the rapid changes in online retail scenarios, consumer purchasing behavior has gradually shifted from WeChat to Short Video, live streaming, Community Group Buying, and other fields. In addition, platforms and chain enterprises have developed their own e-commerce tools such as WeChat mini-stores, leading to a decline in both the stock price and performance of Youzan.

At its peak, Youzan's market cap reached over 70 billion, but it now stands at only over 4 billion, with the stock price long remaining under 1 Hong Kong Dollar, having been categorized as a "zombie stock."

Recently, the WeChat team announced that the WeChat mini-store has officially begun gray testing of the "gift-giving" feature, and several informed sources revealed that Apple is negotiating with Tencent and ByteDance to integrate their AI models into iPhones sold in China.

Now that Youzan's stock price has shown unusual movement, does this indicate that the company has welcomed a growth opportunity with a valuation logic shift?

Profit improved after adjustments, just because of "tightening one's belt"?

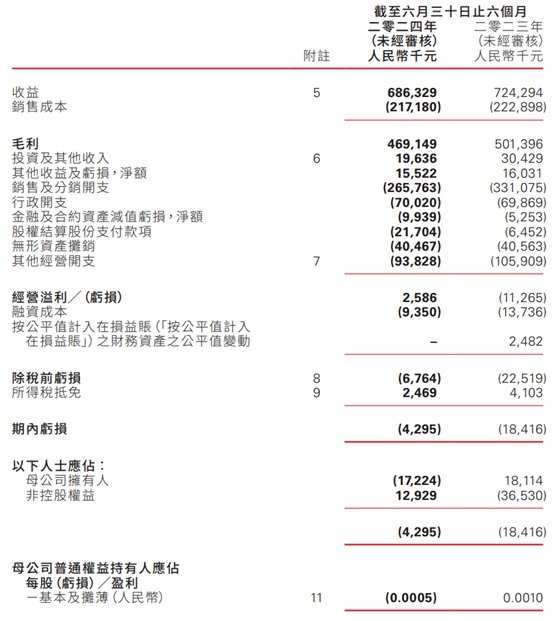

From the recent Earnings Reports, in the first half of this year, Youzan experienced a significant decline in revenue, and profit shifted from profit to loss.

Specifically, for the six months ending on June 30, 2024, the company generated approximately 0.686 billion yuan (RMB, the same below) in revenue, a year-on-year decrease of 5.2%; the loss attributable to the owners of the parent company was 17.224 million yuan, a significant decline compared to a profit of 18.114 million yuan in the same period last year. The company stated that the decrease in revenue was mainly due to a reduction in subscription solution revenue, which was partially offset by an increase in merchant solution revenue.

However, it's optimistic that the adjusted EBITDA for the first half of the year was approximately 51.22 million yuan, exceeding the total for the year 2023, with the profit margin rising to 7.5%. So far, Youzan has achieved operating profit for seven consecutive quarters.

During the reporting period, Youzan's core operating data showed robust growth. According to the Earnings Reports, in the first half of the year, the GMV generated by merchants through Youzan's solutions was approximately 49.9 billion yuan, a year-on-year increase of about 2%; the average sales revenue per merchant in the first half of 2024 was approximately 0.84 million yuan, a year-on-year increase of about 25%.

At the same time, the number of paying merchants decreased. In the first half of 2024, the number of new paying merchants was 9,116; the number of existing paying merchants was 59,541, a significant decrease compared to 72,621 in the first half of 2023.

Thanks to the continuous progress of the New Retail Business and the focus on developing large and medium-sized clients, in the first half of the year, Youzan's GMV from store Saas business was approximately 25 billion yuan, increasing its share to about 50%, a year-on-year growth of 7%.

A deeper analysis of the financial data reveals that the company’s adjusted profits are improving, not due to revenue growth, but primarily due to a decrease in expenses.

In terms of revenue structure, the subscription solutions revenue for the first half of the year was approximately 0.377 billion yuan, a year-on-year decrease of 10.6%, while the merchant solutions revenue was around 0.307 billion yuan, showing a slight increase of 2.2%. The growth of the latter could not compensate for the overall decline in revenue.

During the reporting period, Youzan's sales expenses amounted to 0.2658 billion yuan, a reduction of approximately 65.3 million yuan compared to the same period last year. Other expenses also decreased by 3.1 million yuan to 0.1155 billion yuan, showing a year-on-year decrease.

According to the Zhitong Finance APP, Youzan has actually been optimizing its organizational structure for several years and has made significant progress in cost control. Compared with 0.288 billion yuan in sales costs in the first half of 2022, the company’s sales costs have shrunk to 0.217 billion yuan this year, significantly reducing the proportion of revenue; the company has 1582 employees, which is more than half reduced from over 4000 employees in mid-2021.

Evidently, squeezing profits through layoffs and cost reductions is not sustainable in the long term. So, does Youzan have any new highlights in terms of 'revenue generation'?

Can betting on AI become a new growth point?

In recent years, due to multiple factors such as slowed growth in the macro economy and intensified industry competition, the SaaS industry has consistently struggled to escape the dilemma of 'not making money'.

According to the '2023-2024 Financial Performance Review and Future Outlook of Chinese Enterprise-level SaaS Listed Companies' released by Ernst & Young, since 2022, the gross margin levels of Chinese enterprise-level SaaS companies have generally declined. Among them, because vertical SaaS companies deeply cultivate specific industries, once their products are refined to a certain degree of maturity, they often can form strong competitive advantages and bring about higher gross margin levels. In contrast, general SaaS companies face more intense competition, resulting in relatively lower average gross margin levels.

Behind the difficulty in profitability lies the numerous challenges faced by many SaaS companies: continuous loss of users from WeChat to other e-commerce platforms, price competition due to intensified competition, lack of competitive barriers, and the "cooling off" of private traffic.

However, with AI applications beginning to be implemented across various industries, the SaaS industry has also seen new growth possibilities, such as Youzan launching the large model-driven AI application "Add Me Asia Vets." As the underlying model for the intelligent product system of Youzan, Add Me Asia Vets can support the intelligence of all product lines including Youzan's micro-mall, Youzan stores, Youzan CRM, Youzan smart shopping guide, Youzan corporate WeChat assistant, Youzan beauty industry, and Community Group Buying.

According to Zhito Finance APP, after several upgrades, "Add Me Asia Vets" has expanded its functionality to five major sectors, including marketing content creation, functional usage assistance, data query analysis, automatic task execution, and business consulting suggestions.

At the recent Youzan 12th anniversary conference, Youzan founder and CEO Bai Ya also launched a new AI product intelligent agent and full-managed service. Among them, the Youzan intelligent agent generates items including business opportunity guidance, intelligent hosting, marketing expert, business report, smart outfit, and intelligent sales; the full-managed service includes Short Video and graphic marketing for Xiaohongshu and WeChat video accounts, fan interaction, commodity inventory, order fulfillment, review management, pre-sale and after-sale, etc.

Bai Ya believes that leveraging AI capabilities through the new "AI + SaaS" can significantly lower the usage threshold of SaaS, resulting in more than tenfold efficiency improvements and more than tenfold customer success effect enhancements.

However, Youzan's path to AI may not be so easy. It is well known that large AI models require substantial investment in computing power, data, and other areas, which will bring high trial-and-error costs to enterprises. From the earnings reports, it can be seen that in the first half of recent years, Youzan's R&D expenditure was only 93.828 million yuan, a decrease of about 12% compared to the same period last year, accounting for 13.68% of revenue, which is at a relatively low level.

In addition, some viewpoints suggest that in an era of consumer downgrading, the merchants using SaaS software are competing more on cost-effectiveness, and as a type of tool, the transformation brought by SaaS may be limited.

It can be seen that despite the boost from AI, Youzan's future still faces many challenges. In the case of poor profitability and reduced R&D spending, how much of Youzan's AI "halo" can be translated into actual performance growth remains to be seen over time.