Carvana (NYSE:CVNA) Shareholders Have Earned a 308% Return Over the Last Year

Carvana (NYSE:CVNA) Shareholders Have Earned a 308% Return Over the Last Year

Carvana grew its revenue by 12% last year. That's not great considering the company is losing money. So the 308% gain in just twelve months is completely unexpected. It's great to see that some have made big profits, but we aren't so sure that the increase is justified. It just goes to show that big money can be made if you buy the right stock early.

Carvana grew its revenue by 12% last year. That's not great considering the company is losing money. So the 308% gain in just twelve months is completely unexpected. It's great to see that some have made big profits, but we aren't so sure that the increase is justified. It just goes to show that big money can be made if you buy the right stock early. Carvana Co. (NYSE:CVNA) shareholders might be concerned after seeing the share price drop 13% in the last month. But that cannot eclipse the spectacular share price rise we've seen over the last twelve months. In that time, shareholders have had the pleasure of a 308% boost to the share price. So we wouldn't blame sellers for taking some profits. Of course, winners often do keep winning, so there may be more gains to come (if the business fundamentals stack up).

Carvana公司(纽交所:CVNA)的股东在看到股价在过去一个月下跌13%后,可能会感到担忧。但这并不能掩盖我们在过去十二个月中看到的股价惊人上涨。在这段时间里,股东享受到了308%的股价增长。因此,我们不会指责卖家获利了结。当然,赢家往往会继续获胜,因此可能会有更多的收益(如果业务基本面能够支撑的话)。

So let's assess the underlying fundamentals over the last 1 year and see if they've moved in lock-step with shareholder returns.

那么让我们来评估一下过去一年内的基本面,看看它们是否与股东回报步调一致。

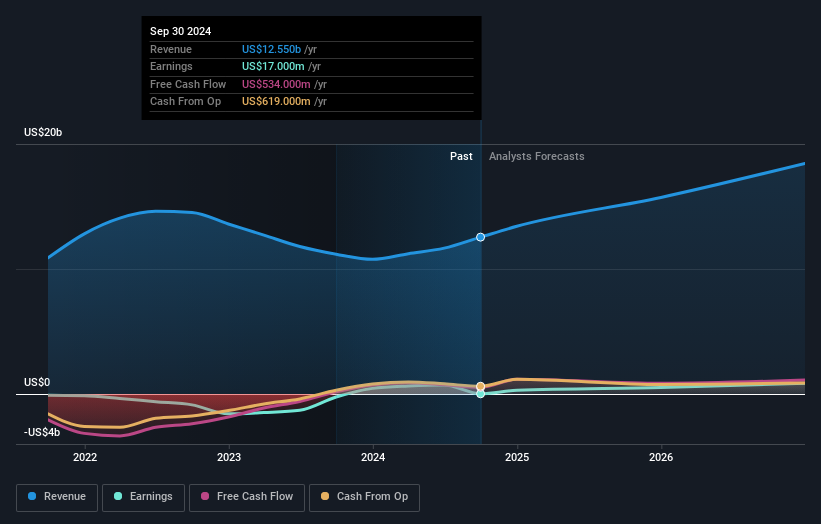

Given that Carvana only made minimal earnings in the last twelve months, we'll focus on revenue to gauge its business development. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. It would be hard to believe in a more profitable future without growing revenues.

考虑到Carvana在过去十二个月中仅实现了微薄的盈利,我们将重点关注营业收入来评估其业务发展。一般来说,我们会与亏损的公司一起考虑像这样的股票,仅仅因为利润的量是如此之低。如果没有营业收入的增长,很难相信未来会更盈利。

Carvana grew its revenue by 12% last year. That's not great considering the company is losing money. So the 308% gain in just twelve months is completely unexpected. It's great to see that some have made big profits, but we aren't so sure that the increase is justified. It just goes to show that big money can be made if you buy the right stock early.

Carvana去年的营业收入增长了12%。考虑到公司正在亏损,这并不算好。因此,短短十二个月内的308%增长是完全意想不到的。看到一些人获得了丰厚的利润真的很棒,但我们并不确定这一增长是否合理。这正说明了,如果早期买入正确的股票,可以赚取巨额财富。

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

您可以在下面的图像中查看收益和营业收入随时间的变化(点击图表查看确切值)。

We consider it positive that insiders have made significant purchases in the last year. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. This free report showing analyst forecasts should help you form a view on Carvana

我们认为,内部人士在过去一年进行了重大购入是一个积极的迹象。尽管如此,大多数人认为盈利和营业收入增长趋势是对业务更有意义的指引。这个免费的报告显示了分析师的预测,应有助于你对Carvana形成看法。

A Different Perspective

不同的视角

It's good to see that Carvana has rewarded shareholders with a total shareholder return of 308% in the last twelve months. Since the one-year TSR is better than the five-year TSR (the latter coming in at 18% per year), it would seem that the stock's performance has improved in recent times. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with Carvana (at least 1 which is a bit unpleasant) , and understanding them should be part of your investment process.

看到Carvana在过去十二个月回报股东总回报率达到308%是件好事。由于一年期的总回报率优于五年期总回报率(后者为每年18%),这似乎表明该股票的表现最近有所改善。在最好的情况下,这可能暗示着一些真正的业务动力,这意味着现在可能是深入研究的好时机。在考虑市场条件对股价的不同影响时,还有其他因素更为重要。例如,投资风险的始终存在的阴影。我们已发现Carvana的3个警示信号(至少有一个是有点令人不快的),了解这些应该成为你投资过程的一部分。

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of undervalued small cap companies that insiders are buying.

还有很多其他公司内部人士正在买入股票。你可能不想错过这份内部人士正在购买的被低估的小盘公司的免费名单。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

请注意,本文中引用的市场回报反映了当前在美国交易所上市股票的市场加权平均回报。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有反馈?对内容有疑虑?请直接与我们联系。或者,发送电子邮件至 editorial-team (at) simplywallst.com。

这篇来自Simply Wall St的文章是一般性的。我们根据历史数据和分析师预测提供评论,采用无偏见的方法,我们的文章并不旨在提供财务建议。它不构成对任何股票的买入或卖出建议,也未考虑到您的目标或财务状况。我们旨在为您提供以基本数据驱动的长期分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St在提到的任何股票中均没有持仓。

译文内容由第三方软件翻译。