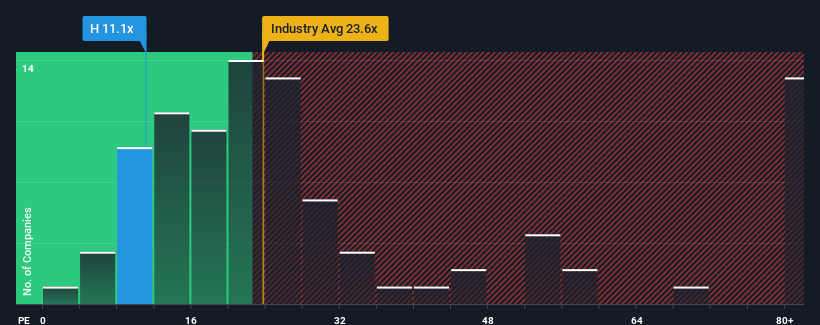

Hyatt Hotels Corporation's (NYSE:H) price-to-earnings (or "P/E") ratio of 11.1x might make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 19x and even P/E's above 34x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings growth that's superior to most other companies of late, Hyatt Hotels has been doing relatively well. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NYSE:H Price to Earnings Ratio vs Industry December 25th 2024 Want the full picture on analyst estimates for the company? Then our free report on Hyatt Hotels will help you uncover what's on the horizon.

Is There Any Growth For Hyatt Hotels?

The only time you'd be truly comfortable seeing a P/E as low as Hyatt Hotels' is when the company's growth is on track to lag the market.

If we review the last year of earnings growth, the company posted a terrific increase of 194%. Still, EPS has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings growth is heading into negative territory, declining 25% each year over the next three years. Meanwhile, the broader market is forecast to expand by 11% each year, which paints a poor picture.

In light of this, it's understandable that Hyatt Hotels' P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Hyatt Hotels' analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Hyatt Hotels (at least 1 which is a bit concerning), and understanding them should be part of your investment process.

If these risks are making you reconsider your opinion on Hyatt Hotels, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings growth, the company posted a terrific increase of 194%. Still, EPS has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

If we review the last year of earnings growth, the company posted a terrific increase of 194%. Still, EPS has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

如果我們回顧去年的盈利增長,這家公司實現了194%的驚人增長。儘管如此,EPS與三年前相比幾乎沒有上升,總體來看這並不理想。因此,對我們來說,這家公司在過去一段時間內的盈利增長結果是複雜的。

如果我們回顧去年的盈利增長,這家公司實現了194%的驚人增長。儘管如此,EPS與三年前相比幾乎沒有上升,總體來看這並不理想。因此,對我們來說,這家公司在過去一段時間內的盈利增長結果是複雜的。