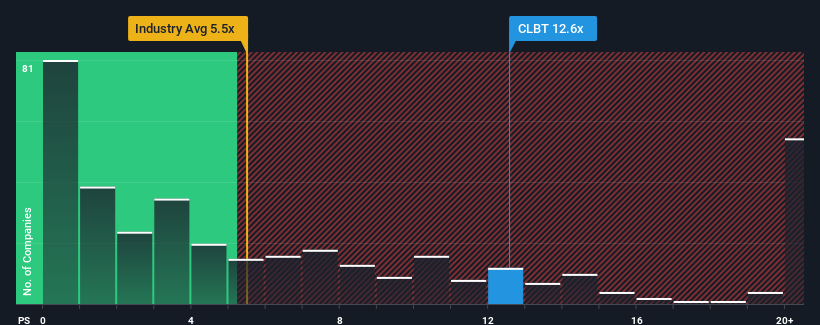

You may think that with a price-to-sales (or "P/S") ratio of 12.6x Cellebrite DI Ltd. (NASDAQ:CLBT) is a stock to avoid completely, seeing as almost half of all the Software companies in the United States have P/S ratios under 5.4x and even P/S lower than 2x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

NasdaqGS:CLBT Price to Sales Ratio vs Industry December 24th 2024

What Does Cellebrite DI's Recent Performance Look Like?

With revenue growth that's superior to most other companies of late, Cellebrite DI has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. If not, then existing shareholders might be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Cellebrite DI will help you uncover what's on the horizon.

What Are Revenue Growth Metrics Telling Us About The High P/S?

The only time you'd be truly comfortable seeing a P/S as steep as Cellebrite DI's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 26% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 64% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the eight analysts covering the company suggest revenue should grow by 15% per annum over the next three years. That's shaping up to be materially lower than the 20% per year growth forecast for the broader industry.

With this in consideration, we believe it doesn't make sense that Cellebrite DI's P/S is outpacing its industry peers. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

It comes as a surprise to see Cellebrite DI trade at such a high P/S given the revenue forecasts look less than stellar. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. At these price levels, investors should remain cautious, particularly if things don't improve.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Cellebrite DI that you should be aware of.

If these risks are making you reconsider your opinion on Cellebrite DI, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

您可能會認爲,Cellebrite DI Ltd.(納斯達克:CLBT)以12.6倍的市銷率是一個完全不值得投資的股票,因爲幾乎一半的美國軟件公司市銷率低於5.4倍,甚至低於2倍的市銷率也並非罕見。儘管如此,我們需要更深入地分析,以判斷是否有合理的依據來解釋這一高企的市銷率。

Retrospectively, the last year delivered an exceptional 26% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 64% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Retrospectively, the last year delivered an exceptional 26% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 64% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

回顧過去一年,該公司的營業收入實現了26%的顯著增長。最近的強勁表現意味着它在過去三年中,營業收入總共增長了64%。因此,可以公平地說,最近的營業收入增長對公司來說非常出色。

回顧過去一年,該公司的營業收入實現了26%的顯著增長。最近的強勁表現意味着它在過去三年中,營業收入總共增長了64%。因此,可以公平地說,最近的營業收入增長對公司來說非常出色。