Should You Be Worried About Ameresco, Inc.'s (NYSE:AMRC) 4.9% Return On Equity?

Should You Be Worried About Ameresco, Inc.'s (NYSE:AMRC) 4.9% Return On Equity?

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity One of the best investments we can make is in our own knowledge and skill set. With that in mind, this article will work through how we can use Return On Equity (ROE) to better understand a business. We'll use ROE to examine Ameresco, Inc. (NYSE:AMRC), by way of a worked example.

我们能做出的最佳投资之一就是投资于自己的知识和技能。考虑到这一点,本文将探讨如何使用股本回报率(ROE)更好地理解一项业务。我们将通过一个实例来使用ROE来审视阿梅雷斯克公司(纽交所:AMRC)。

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

股本回报率或ROE是股东需要考虑的重要因素,因为它告诉他们自己的资本是如何有效地被再投资的。简单来说,它衡量的是公司相对于股东权益的盈利能力。

How To Calculate Return On Equity?

如何计算股东权益回报率?

Return on equity can be calculated by using the formula:

净资产收益率可以通过以下公式计算:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

股东权益回报率 = 净利润(来自持续运营)÷ 股东权益

So, based on the above formula, the ROE for Ameresco is:

因此,根据上述公式,Ameresco 的 ROE 为:

4.9% = US$49m ÷ US$1.0b (Based on the trailing twelve months to September 2024).

4.9% = 4900万美元 ÷ 10亿美元(基于截至2024年9月的过去十二个月)。

The 'return' is the income the business earned over the last year. That means that for every $1 worth of shareholders' equity, the company generated $0.05 in profit.

“回报”是指企业在过去一年中获得的收入。这意味着每增加1美元的股东权益,公司就产生了0.05美元的净利润。

Does Ameresco Have A Good Return On Equity?

阿梅雷斯克的净资产收益率好吗?

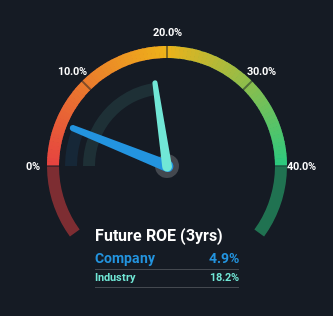

By comparing a company's ROE with its industry average, we can get a quick measure of how good it is. The limitation of this approach is that some companies are quite different from others, even within the same industry classification. If you look at the image below, you can see Ameresco has a lower ROE than the average (18%) in the Construction industry classification.

通过将公司的ROE与其行业平均水平进行比较,我们可以快速衡量其表现。这种方法的局限性在于,有些公司即使在同一行业分类中也与其他公司有很大不同。如果你查看下面的图像,可以看到阿梅雷斯克的ROE低于施工行业分类的平均水平(18%)。

That's not what we like to see. That being said, a low ROE is not always a bad thing, especially if the company has low leverage as this still leaves room for improvement if the company were to take on more debt. A high debt company having a low ROE is a different story altogether and a risky investment in our books.

这并不是我们想要看到的。然而,低ROE并不总是坏事,特别是如果公司杠杆率较低,这仍然留有提升空间,如果公司愿意承担更多的债务的话。高负债公司拥有低ROE则完全是另一回事,是我们认为的高风险投资。

How Does Debt Impact ROE?

债务对ROE的影响是怎样的?

Most companies need money -- from somewhere -- to grow their profits. That cash can come from issuing shares, retained earnings, or debt. In the first and second cases, the ROE will reflect this use of cash for investment in the business. In the latter case, the use of debt will improve the returns, but will not change the equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

大多数公司需要资金——从某个地方来——以增长他们的利润。这笔现金可以来自发行股票、保留盈余或债务。在前两种情况下,ROE将反映这笔现金用于业务投资的情况。在后者的情况下,债务的使用将提高回报,但不会改变股本。因此,债务的使用可以提高ROE,尽管在风雨交加的情况下,风险随之增加,打个比方。

Combining Ameresco's Debt And Its 4.9% Return On Equity

结合阿梅雷斯克的债务和其4.9%的ROE

Ameresco clearly uses a high amount of debt to boost returns, as it has a debt to equity ratio of 2.16. Its ROE is quite low, even with the use of significant debt; that's not a good result, in our opinion. Investors should think carefully about how a company might perform if it was unable to borrow so easily, because credit markets do change over time.

阿梅雷斯克显然利用高额债务来提升回报,其债务与股权比率为2.16。即使使用了大量债务,它的ROE仍然相当低;在我们看来,这不是一个好结果。投资者应仔细考虑如果公司无法如此轻松地借款,可能会表现如何,因为信贷市场会随着时间而改变。

Conclusion

结论

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. A company that can achieve a high return on equity without debt could be considered a high quality business. If two companies have the same ROE, then I would generally prefer the one with less debt.

净资产收益率是判断一个企业盈利能力及回报股东能力的有用指标。一家能够在没有债务的情况下实现高净资产收益率的公司可以被视为优质企业。如果两家公司的ROE相同,我通常会更偏好债务较少的那家公司。

But when a business is high quality, the market often bids it up to a price that reflects this. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So I think it may be worth checking this free report on analyst forecasts for the company.

但是,当一家企业质量高时,市场往往会将其价格推高,反映出这一点。利润增长率与股票价格中反映的预期相比,尤其重要。因此,我认为查看这份有关分析师预测的免费报告可能值得。

If you would prefer check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

如果你更愿意查看另一家公司——一家潜在的财务状况优秀的公司——那么一定不要错过这份有趣公司的免费列表,这些公司有高股本回报率和低负债。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有反馈?对内容有疑虑?请直接与我们联系。或者,发送电子邮件至 editorial-team (at) simplywallst.com。

这篇来自Simply Wall St的文章是一般性的。我们根据历史数据和分析师预测提供评论,采用无偏见的方法,我们的文章并不旨在提供财务建议。它不构成对任何股票的买入或卖出建议,也未考虑到您的目标或财务状况。我们旨在为您提供以基本数据驱动的长期分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St在提到的任何股票中均没有持仓。

译文内容由第三方软件翻译。