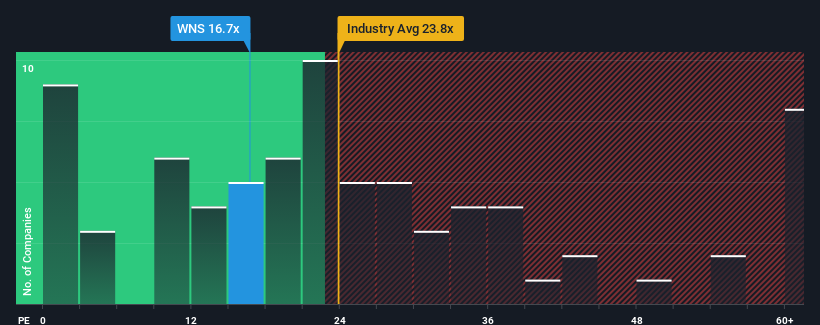

With a median price-to-earnings (or "P/E") ratio of close to 18x in the United States, you could be forgiven for feeling indifferent about WNS (Holdings) Limited's (NYSE:WNS) P/E ratio of 16.7x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

While the market has experienced earnings growth lately, WNS (Holdings)'s earnings have gone into reverse gear, which is not great. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

NYSE:WNS Price to Earnings Ratio vs Industry December 23rd 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on WNS (Holdings).

How Is WNS (Holdings)'s Growth Trending?

The only time you'd be comfortable seeing a P/E like WNS (Holdings)'s is when the company's growth is tracking the market closely.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 23%. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 16% in total. So we can start by confirming that the company has generally done a good job of growing earnings over that time, even though it had some hiccups along the way.

Turning to the outlook, the next three years should generate growth of 18% per annum as estimated by the ten analysts watching the company. With the market only predicted to deliver 11% per year, the company is positioned for a stronger earnings result.

In light of this, it's curious that WNS (Holdings)'s P/E sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Bottom Line On WNS (Holdings)'s P/E

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that WNS (Holdings) currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for WNS (Holdings) with six simple checks will allow you to discover any risks that could be an issue.

If you're unsure about the strength of WNS (Holdings)'s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 23%. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 16% in total. So we can start by confirming that the company has generally done a good job of growing earnings over that time, even though it had some hiccups along the way.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 23%. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 16% in total. So we can start by confirming that the company has generally done a good job of growing earnings over that time, even though it had some hiccups along the way.

回顧過去一年的盈利,令人沮喪的是公司的利潤下降了23%。這在一定程度上抑制了它過去的良好表現,因爲它三年的每股收益增長總計仍然是值得注意的16%。所以我們可以首先確認,公司在這段時間內總體上做得不錯,儘管過程中也有一些波折。

回顧過去一年的盈利,令人沮喪的是公司的利潤下降了23%。這在一定程度上抑制了它過去的良好表現,因爲它三年的每股收益增長總計仍然是值得注意的16%。所以我們可以首先確認,公司在這段時間內總體上做得不錯,儘管過程中也有一些波折。