13% Earnings Growth Over 3 Years Has Not Materialized Into Gains for Accel Entertainment (NYSE:ACEL) Shareholders Over That Period

13% Earnings Growth Over 3 Years Has Not Materialized Into Gains for Accel Entertainment (NYSE:ACEL) Shareholders Over That Period

During the unfortunate three years of share price decline, Accel Entertainment actually saw its earnings per share (EPS) improve by 44% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

During the unfortunate three years of share price decline, Accel Entertainment actually saw its earnings per share (EPS) improve by 44% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past. Many investors define successful investing as beating the market average over the long term. But its virtually certain that sometimes you will buy stocks that fall short of the market average returns. We regret to report that long term Accel Entertainment, Inc. (NYSE:ACEL) shareholders have had that experience, with the share price dropping 20% in three years, versus a market return of about 23%. Shareholders have had an even rougher run lately, with the share price down 11% in the last 90 days.

許多投資者將成功投資定義爲在長期內超越市場平均水平。但幾乎可以肯定,有時你會買入那些回報低於市場平均的股票。我們遺憾地報告,長期以來,Accel Entertainment, Inc. (紐交所:ACEL)的股東經歷了這一情況,股價在三年內下跌了20%,而市場的回報約爲23%。最近,股東的情況更爲嚴峻,股價在過去90天內下跌了11%。

Given the past week has been tough on shareholders, let's investigate the fundamentals and see what we can learn.

鑑於過去一週對股東來說很艱難,讓我們調查一下基本面,看看我們能學到什麼。

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

用本傑明·格雷厄姆的話說:在短期內,市場像個投票機,但在長期內,它就是個稱重機。檢視市場情緒如何隨時間變化的一種方法是觀察一家公司的股價與每股收益(EPS)之間的互動。

During the unfortunate three years of share price decline, Accel Entertainment actually saw its earnings per share (EPS) improve by 44% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

在這三年的股價下跌期間,Accel Entertainment的每股收益(EPS)實際上提高了每年44%。考慮到股價的反應,人們可能會懷疑EPS是否在此期間是一個良好的業務表現指標(可能是由於一次性損失或收益)。或者,過去的增長預期可能是不合理的。

It's worth taking a look at other metrics, because the EPS growth doesn't seem to match with the falling share price.

值得看看其他指標,因爲每股收益的增長似乎與股價下跌不匹配。

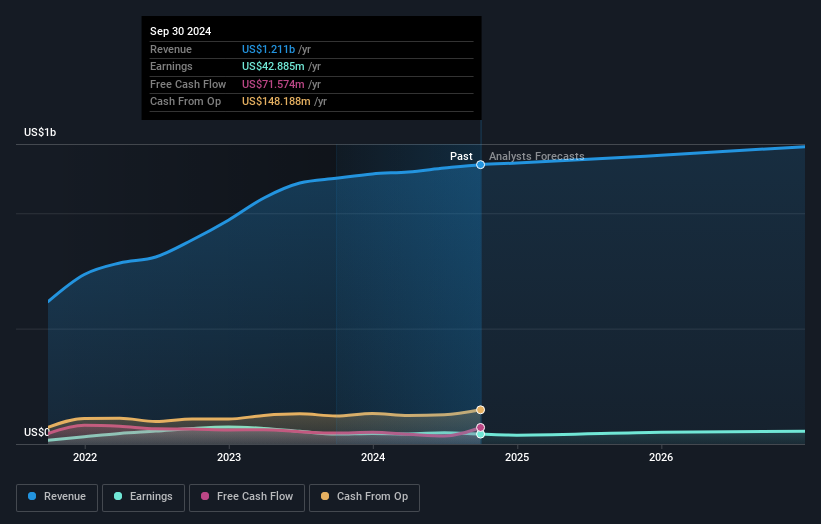

Revenue is actually up 20% over the three years, so the share price drop doesn't seem to hinge on revenue, either. It's probably worth investigating Accel Entertainment further; while we may be missing something on this analysis, there might also be an opportunity.

營業收入在三年內實際上增長了20%,因此股價下跌似乎也與營業收入無關。進一步調查Accel Entertainment可能是值得的;雖然我們在這個分析中可能遺漏了一些東西,但也可能存在機會。

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

下面的圖表顯示了收益和營收隨時間的變化情況(通過單擊圖像揭示確切的值)。

We know that Accel Entertainment has improved its bottom line over the last three years, but what does the future have in store? This free interactive report on Accel Entertainment's balance sheet strength is a great place to start, if you want to investigate the stock further.

我們知道Accel Entertainment在過去三年中改善了其底線,但未來又會怎麼樣呢?如果你想進一步調查這隻股票,這份關於Accel Entertainment資產負債表強度的免費互動報告是一個很好的開始。

A Different Perspective

不同的視角

Accel Entertainment shareholders gained a total return of 2.8% during the year. But that return falls short of the market. On the bright side, that's still a gain, and it is certainly better than the yearly loss of about 3% endured over half a decade. So this might be a sign the business has turned its fortunes around. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we've identified 2 warning signs for Accel Entertainment (1 is significant) that you should be aware of.

Accel Entertainment的股東在這一年中獲得了總回報2.8%。但是,這一回報低於市場。值得慶幸的是,這仍然是一個增長,肯定比過去五年中每年約3%的損失要好。因此,這可能是業務扭轉命運的跡象。我發現長期看股價作爲業務表現的代理指標非常有趣。但是爲了真正獲得洞察,我們還需要考慮其他信息。例如,我們已識別出2個Accel Entertainment的警告信號(其中1個是顯著的),你應該注意。

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

如果你像我一樣,那麼你一定不想錯過這份內部人士正在購買的被低估的小型股免費名單。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文中引用的市場回報反映了當前在美國交易所上市股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?對內容有疑慮?請直接與我們聯繫。或者,發送電子郵件至 editorial-team (at) simplywallst.com。

這篇來自Simply Wall ST的文章是一般性的。我們根據歷史數據和分析師預測提供評論,採用無偏見的方法,我們的文章並不旨在提供財務建議。它不構成對任何股票的買入或賣出建議,也未考慮到您的目標或財務狀況。我們旨在爲您提供以基本數據驅動的長期分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall ST在提到的任何股票中均沒有持倉。

譯文內容由第三人軟體翻譯。