上周美联储的鹰派降息导致美债利率与美元指数快速攀升,而国内货币宽松预期却推动国内利率的大幅走低。我们认为,

上周美联储的鹰派降息导致美债利率与美元指数快速攀升,而国内货币宽松预期却推动国内利率的大幅走低。我们认为,Source: China International Capital Corporation Strategy. Author: Wang Hanfeng, Liu Gang et al. After a significant sell-off in the early part of last week, overseas Chinese capital stocks rebounded strongly in the middle of the week. At the beginning of the week, investors' sentiment deteriorated further due to multiple domestic and international factors. Under the pressure of external fund outflows, there was an impact on liquidity in the market and the market performance plummeted. Fortunately, this liquidity shock eased somewhat after policy stabilization signals on Wednesday, and the market subsequently showed an almost linear upward trend. After the roller coaster market last week, we tend to believe that the panic-style rapid sale in the early stage may be temporarily over, and the market may gradually enter a consolidation and bottoming period. However, the recovery of emotions still needs some time, mainly due to: 1) The outflow of overseas funds, especially the reduction of large-scale sovereign funds, is difficult to see a significant reversal in the short term; 2) The short selling ratio in the market is still high; 3) The geopolitical tensions, Sino-US relations, epidemic, domestic policies, and uncertainties in regulation have not yet completely weakened. Therefore, looking ahead, whether the market rebound can continue depends on: 1) Whether positive policy signals can be specifically implemented; 2) Whether external uncertainties will be alleviated.

Authors: Liu Gang, Zhang Weihuan, and others.

Summary

Looking back over the past month, the market once again exhibited the familiar 'high and low' trend seen in recent years, going in circles and returning to the same starting point as a month ago. We had indicated in late November that expectations of overly strong policies might still be unrealistic, and the market has not completely escaped the turbulence pattern, maintaining a strategy of entering at a low bottom and taking profits on the exuberant right side. The performance over the past period has also confirmed this view.

Last week, the Federal Reserve's hawkish rate cuts led to a rapid rise in U.S. Treasury rates and the USD, while expectations of domestic monetary easing drove domestic rates significantly lower. We believe that new highs in U.S. Treasuries often correspond to tightening U.S. dollar liquidity, creating pressure on the valuation of Hong Kong stocks from the denominator side. Although new lows in Chinese bonds may hedge against rising U.S. Treasuries from the denominator side, the numerator will reflect the pressure of growth expectations. Therefore, overall, the combination of 'new highs in U.S. Treasuries + new lows in Chinese bonds' has a neutral to slightly negative impact on Hong Kong stocks, as historical experiences often suggest.

Last week, the Federal Reserve's hawkish rate cuts led to a rapid rise in U.S. Treasury rates and the USD, while expectations of domestic monetary easing drove domestic rates significantly lower. We believe that new highs in U.S. Treasuries often correspond to tightening U.S. dollar liquidity, creating pressure on the valuation of Hong Kong stocks from the denominator side. Although new lows in Chinese bonds may hedge against rising U.S. Treasuries from the denominator side, the numerator will reflect the pressure of growth expectations. Therefore, overall, the combination of 'new highs in U.S. Treasuries + new lows in Chinese bonds' has a neutral to slightly negative impact on Hong Kong stocks, as historical experiences often suggest.

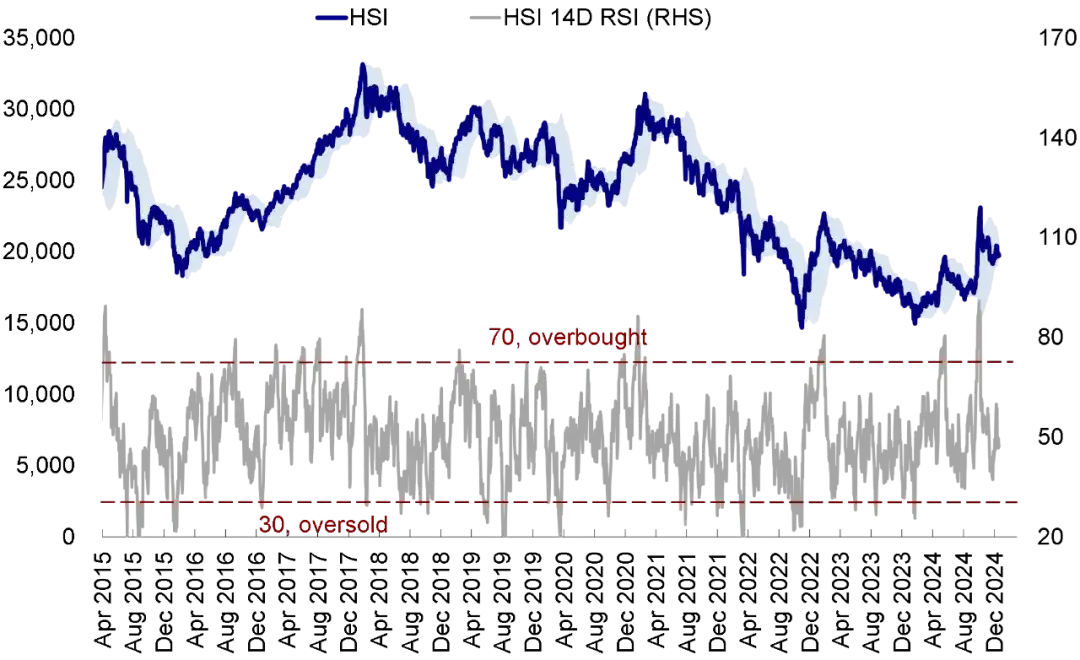

In summary, we still maintain the judgment of an overall turbulent pattern in the Hong Kong stock market, with three main reasons: first, with the important domestic window period coming to an end, the market enters a policy vacuum period before the Two Sessions; secondly, external disturbances, especially the uncertainties regarding the Federal Reserve's future path, still exist. However.technical indicatorsIt shows that the Hong Kong stock market is currently in a relatively neutral state, with the Hang Seng Index ERP, short sell proportions, and.RSIAll are at the level of the early rebound at the end of September. Against this backdrop, it is recommended to focus on three directions in terms of allocation: 1) Supply clearing, 2) Policy support, and 3) Stable returns.

Looking ahead, external shocks, especially the tariff scenarios after Trump assumed office, may determine market trajectories and domestic policy responses. 1) If tariffs are gradually imposed (initial tariffs of 30-40%), the market impact is expected to be limited, and investors are advised to maintain current oscillation structure operations; 2) If tariffs are raised to the maximum of 60%, the market may face significant disturbances. However, we believe this could provide a better buying opportunity.

Main text

New highs in US bonds and new lows in Chinese bonds.

Market trend review.

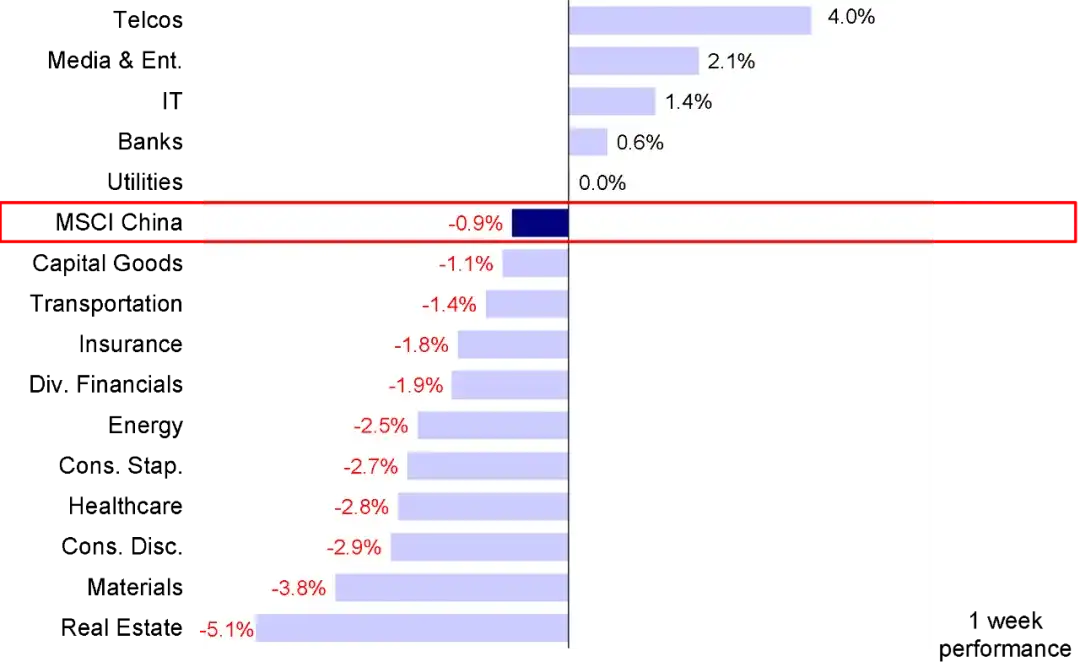

Due to the Fed's hawkish stance leading to a significant rise in US bond rates and the USD, coupled with domestic economic data falling short of expectations, the Hong Kong stock market weakened again last week. In terms of indices, the Hang Seng Index and MSCI Chinese Index fell by 1.3% and 0.9% respectively, while the Hang Seng Tech and Hang Seng National Enterprises dropped by 0.8% and 0.6% respectively. In terms of sectors, Telecommunication Services (+4.0%) and Media Entertainment (+2.1%) showed resilience, while old economy sectors such as Real Estate (-5.1%) and Materials (-3.8%) underperformed.

Chart: Last week, the MSCI Chinese Index fell by 0.9%, with Real Estate and Materials sectors being the most pressured.

Market outlook

Looking back over the past month, the market once again exhibited the familiar "high surge followed by a drop" trend, ultimately returning to its starting point from a month ago. As late November approached, with important meetings such as the Political Bureau meeting and the Economic Work Conference, the market's positive expectations regarding policies surged, temporarily pushing the market upward. However, it was pointed out at the time that overly strong expectations might still be unrealistic. The market has not completely escaped its fluctuating pattern, maintaining a strategy of intervention at a low depressed level and profiting on the excited right side ("What kind of policies does the market expect?").

This judgment is made because the market has already factored in considerable expectations at its current position; further upward movement requires more policy support, particularly fiscal policies. Nevertheless, under the "realistic constraints" of leverage levels, financing costs, and exchange rates, overly high expectations in the short term are regarded as unrealistic. The actual situation confirms this, as the performance of the market over the past period essentially validates our view. The positive signals conveyed by the Political Bureau meeting, such as "extraordinary counter-cyclical adjustments" and "moderately loose" monetary policies, prompted a rapid rise in the market. However, after fully digesting expectations, the lack of incremental information on some market concerns (such as the intensity of fiscal stimulus and consumption subsidies) during the Economic Work Conference, as well as the exceeding expectations regarding the "strengthened regulation" of the platform economy led to a market pullback, with the Hang Seng Index essentially returning to the levels seen at the end of November.

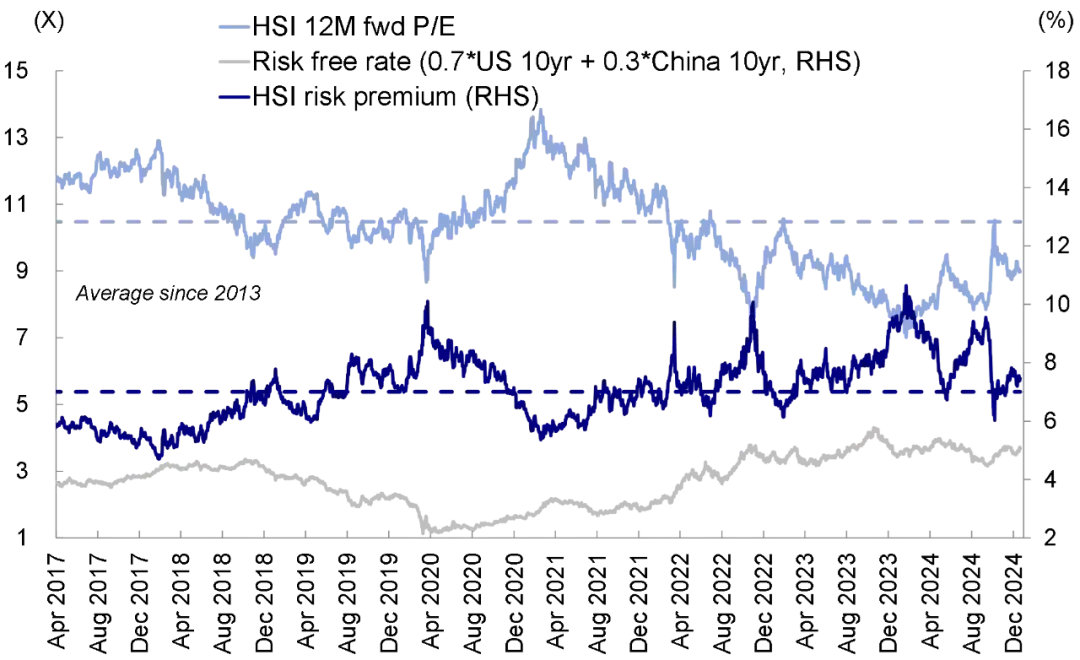

Chart: The Hang Seng Index risk premium has returned to the early levels of the market rebound at the end of September.

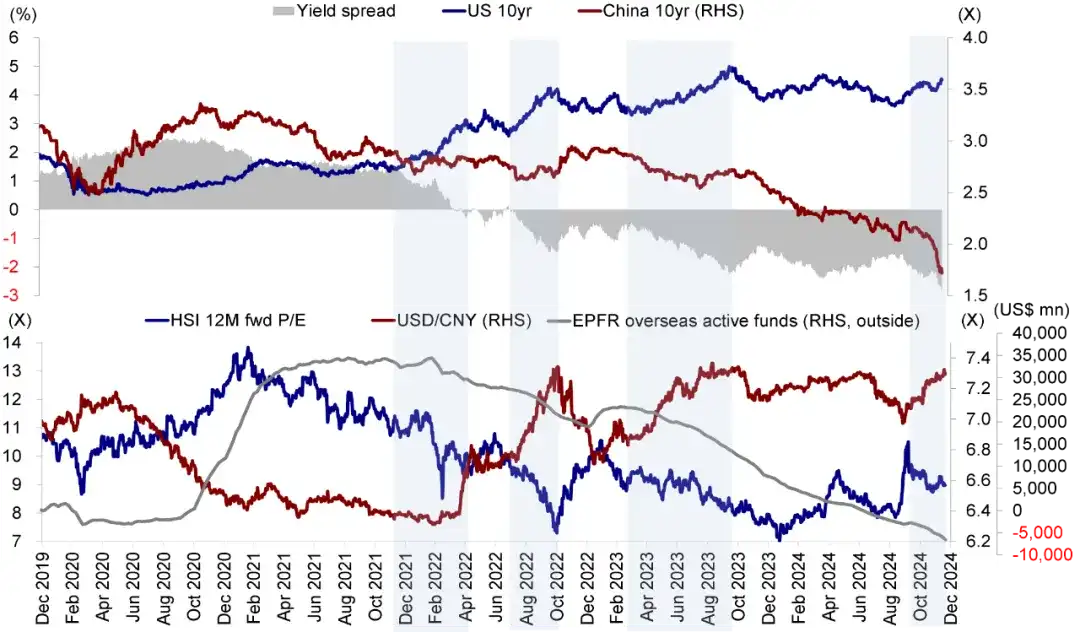

As the important domestic window periods gradually pass, external shocks—especially the hawkish interest rate cuts from the Federal Reserve—have become a source of volatility for global markets, including Hong Kong stocks, last week. At the December FOMC meeting, compared to the anticipated interest rate cuts, the updated "dot plot" signaling only two rate cuts in 2025, combined with Powell's continued emphasis on a more cautious pace of future rate cuts, triggered market fluctuations. The 10-Year T-Note yield quickly rose to nearly 4.6%, reaching a new high since late May of this year. The USD has surged to its highest level since the end of 2022. In stark contrast, domestic expectations for monetary easing have increased while expectations for fiscal strength have cooled, leading to a sharp decline in domestic interest rates. The 10-Year China bond yield briefly broke through the 1.7% mark, and the 1-Year bond yield even fell below 1%, causing the China-USA interest spread to widen to historically extreme levels. So, what impact does the combination of "new highs for U.S. bonds + new lows for Chinese bonds" have on Hong Kong stocks?

New highs for U.S. bonds: Tightened dollar liquidity applies pressure on the valuation of Hong Kong stocks from the denominator side. The most direct impact of the rise in U.S. Treasury yields alongside a stronger dollar is the tightening of overseas liquidity. Historically, in this context, overseas funds tend to weaken, and as an offshore market, Hong Kong stocks are naturally more affected. Meanwhile, the rise in U.S. bond yields will also influence the valuation pricing of Hong Kong stocks from the denominator side. Even considering that the proportion of mainland funds in Hong Kong's trading can reach around 25-30%, we still use a 7:3 weight of U.S. bonds to Chinese bonds when calculating the risk-free rate for Hong Kong stocks. Thus, changes in U.S. bond yields remain dominant, so their rapid increase in the short term will also apply pressure on the valuation of Hong Kong stocks from the denominator side.

New lows for Chinese bonds: from the denominator side, the rise in U.S. bonds is hedged, but the numerator reflects pressure on growth expectations. Conversely, the rapid decline in Chinese bond yields driven by expectations of monetary easing seems to offset to some extent the adverse effects of rising U.S. bond yields from the denominator side. However, the rapid decline in rates also implies the market's expectations of weak domestic growth in the future; therefore, although there is some support from the denominator side (but not as significant as its impact on A-shares), it instead brings greater pressure from the numerator side's growth expectations.

Therefore, overall, the combination of 'new highs in U.S. bonds + new lows in Chinese bonds' has a neutral to somewhat negative impact on Hong Kong stocks, as historical experience often suggests. Reviewing the impact of the changes in the Sino-U.S. yield spread on the Hong Kong stock market over the past five years, it has been found that during periods when 'U.S. bond yields rise + Chinese bond yields fall' leading to a widening Sino-U.S. yield spread, the valuation of the Hong Kong stock market has been significantly pressured for most of the time, periods which also often accompany an overall outflow of foreign capital from the Chinese stock market.

Chart: 'New highs in U.S. bonds + new lows in Chinese bonds' often presents a neutral to somewhat negative impact on Hong Kong stocks.

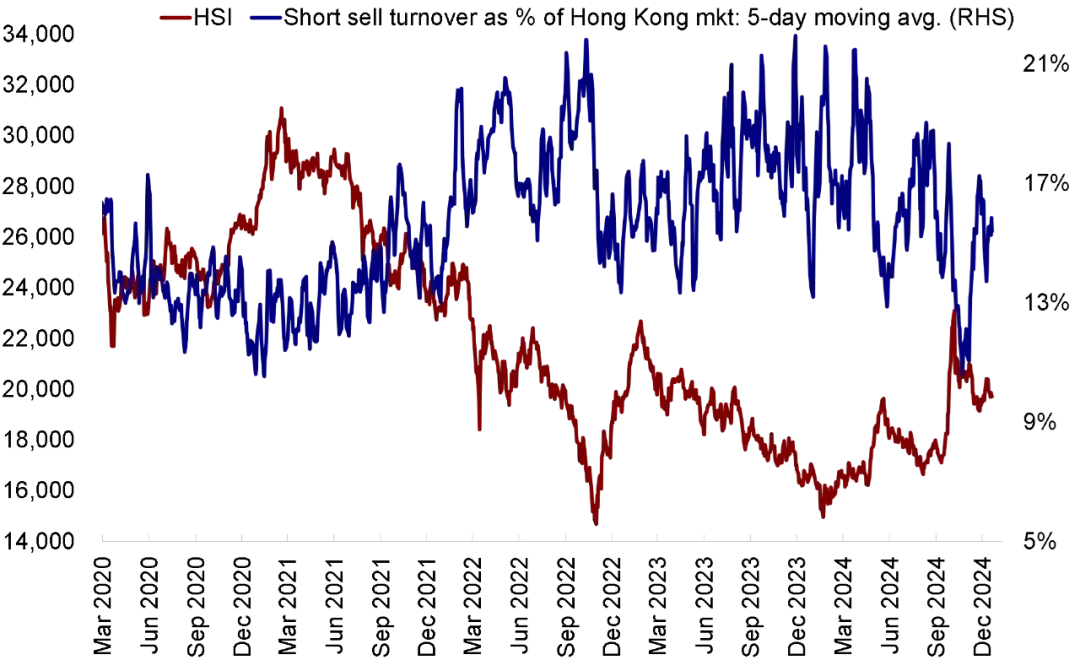

That said, we believe that investors do not need to be overly pessimistic; we still maintain the judgment of an overall oscillating pattern in the Hong Kong stock market. First, regarding the judgment on the future path of the Federal Reserve, although it requires more time to observe, we still judge that subsequent rate cuts remain possible. Short-term market expectations of excessive leverage often lead to overcorrection, and the reflexivity of interest rates and financial conditions to fundamentals allows current 'hawkish' stances to provide space for future 'cuts' ('Can the Federal Reserve cut rates again?'). Second, technical indicators also show that the Hong Kong stock market is currently in a relatively neutral state, for example: 1) the Hang Seng Index risk premium (ERP) is currently around 7.4, roughly equivalent to the levels at the beginning of the rebound at the end of September; 2) the short selling turnover ratio has declined from 17.3% at the end of November and maintained around 15.5%, close to the levels before the market rebound in late September this year; 3) the 14-day Relative Strength Index (RSI) has also dropped from a previous week's peak of 59.9 to this median level of 47.1. Meanwhile, the Hang Seng Index near 19,500 is also essentially at significant daily and monthly levels.ResistanceTherefore, under the assumption of moderate and limited domestic policy efforts, the current oscillation structure remains our baseline scenario, and the market may stay roughly flat around this position in the short term but has potential for both upward and downward movements.

Chart: The short selling turnover ratio has recently been around 15.5%.

Chart: In terms of overbought and oversold levels, the current Hong Kong stock market is also at a neutral level.

Looking ahead, as the market enters a policy vacuum period before the Two Sessions, external shocks, especially the various scenarios of tariffs following Trump's inauguration, will determine market paths and domestic policy responses. 1) If the tariffs are imposed gradually, for example, with the initial tariff set at 30-40%, adding an extra 10-20% on top of the current 19%, we expect limited market impact. This level essentially aligns with current market consensus expectations, and its actual economic impact is relatively manageable. The market's reaction may resemble that of April 2019 after the third round of tariffs, where disturbances occurred but maintained a range-bound fluctuation. Currently, the risk premium in A-shares is roughly equivalent to that of April-May 2019. In this scenario, it is recommended that investors maintain operations within the current fluctuation structure; 2) Conversely, if a maximum 60% tariff is imposed, given the insufficient market pricing and the nonlinear increase in actual impact, the market could face significant disturbances. However, should substantial volatility indeed occur, it may provide better buying opportunities, not only due to the cheap valuations but also because of a higher probability of policy hedging ("The Possible Paths in the Short Term").

In addition to external disturbances, November's economic data also indicate that domestic fundamentals require further policy efforts to boost them. In November, the total retail sales of consumer goods grew by 3% year-on-year, a decrease of 1.8 percentage points from October, falling below market expectations. Although factors like e-commerce platforms bringing forward the "Singles' Day Sales" promotions had an impact, focusing on the year-on-year growth of non-trade-in goods from October to November reveals a mere 3.2% growth, which is at a year-low and highlights that internal consumer demand remains weak. Meanwhile, Real Estate Development investment has dragged down overall fixed asset investment, decreasing from a 3.4% year-on-year growth in January-October to 3.3% in January-November. In our report titled 'Hong Kong Stock Market Outlook 2025: Dark Clouds Without Rain', we pointed out that to address the current contraction in domestic credit and the private sector's ongoing "deleveraging", it is necessary to lower actual financing costs. Our estimates show that a further reduction of 40-60 basis points in the 5-Year LPR could help align financing costs with investment return objectives, but the Fed's slower interest rate cuts and exchange rate pressures may constrain short-term easing space. On the other hand, from the perspective of more effectively revitalizing investment return expectations, we estimate a need for a "one-time" and "new" 7-8 trillion yuan of broad expenditure to bridge the output gap accumulated over the past three years (implying a growth rate of about 9%), which still falls short of currently known scales (the adjustment of the general public budget deficit rate to about 4% corresponds to 1 trillion yuan, plus 2 trillion yuan for debt relief). This suggests that while incremental stimulus will exist, overly high expectations may not be realistic.

Therefore, in this context, we maintain the judgment of the market's overall structural fluctuation. In terms of allocation, under the assumption of an overall fluctuating pattern, we recommend focusing on three categories of industries: First, sectors where supply and policy environments are sufficiently cleared, which would perform better with any marginal recovery in demand, including parts of Consumer Services such as Internet, home appliances, textile and apparel, and electronics. Second, sectors supported by policies, such as home appliances and Autos under trade-in schemes, as well as trends in the self-reliant technology field such as computers and semiconductors; Third, sectors offering stable returns, such as state-owned enterprises with high dividends.

Specifically, the main logic supporting our above viewpoint, as well as the changes to pay attention to this week, mainly include:

1) November's retail sales in China fell short of expectations, while Real Estate Development investment dragged down fixed asset investment. Overall, the November economic data is relatively weak, despite the continuing effects of the trade-in policy; internal demand remains muted. The total retail sales of consumer goods grew by 3% year-on-year in November, a decline of 1.8 percentage points from October. This year's e-commerce platforms further advanced the "Singles' Day Sales" promotion, which accelerated the growth of retail sales in October but correspondingly overdrew November's demand. The growth in retail sales was mainly driven by the trade-in policy for consumer goods, and according to China International Capital Corporation's macro research team, the year-on-year growth of retail sales for trade-in goods in November was 8.2% (down from 8.9% in October), maintaining a high growth rate. However, the year-on-year growth for non-trade-in retail sales from October to November was only 3.2%, which is at a year-low, indicating that internal consumer demand has not improved. At the same time, fixed asset investment from January to November grew by 3.3% year-on-year (3.4% in January-October), with Real Estate Investment still being a major drag, while broad Infrastructure and manufacturing investment remained relatively stable.

Chart: Domestic data for November shows a general weakening, with retail sales falling short of expectations, and Real Estate Development investment dragging down fixed asset investment.

2) In December, the Federal Reserve's FOMC cut interest rates by 25 basis points, but the forecast for rate cuts in 2025 has been reduced to two times. At the December FOMC meeting, the Federal Reserve announced a 25 basis point rate cut, lowering the benchmark rate to 4.25-4.5%, in line with market expectations. However, compared to the fully in-line rate cut, the Federal Reserve conveyed a more hawkish signal regarding the pace of future cuts, indicating that the pace of future rate cuts may slow. 1) The "dot plot" anticipates only two rate cuts in 2025 (3.75-4%), which is fewer than the market's expectation of three times; 2) In the meeting statement, the Federal Reserve slightly added language considering the "magnitude and timing," suggesting that future rate cuts may slow down; 3) Powell has continuously hinted in the press conference that the pace of future rate cuts may slow, indicating that after the 100 basis points cut since September, the current policy has become significantly less restrictive, and more "cautious" actions will be needed moving forward.

3) The November PCE price index in the USA was below expectations. The November PCE price index increased by 2.4% year-on-year (vs. October's growth of 2.3%), although it is the highest level since July this year, the growth rate was below the expected 2.5%. On a month-on-month basis, it grew by 0.1%, which also fell short of the expected 0.2%. Excluding food and energy prices, the core PCE in November increased by 2.8% year-on-year, which is also lower than the expected 2.9%. The overall underperformance of November data also indicates a slowdown in price pressure; following the release of the data, the USD and 10-Year T-Note significantly weakened.

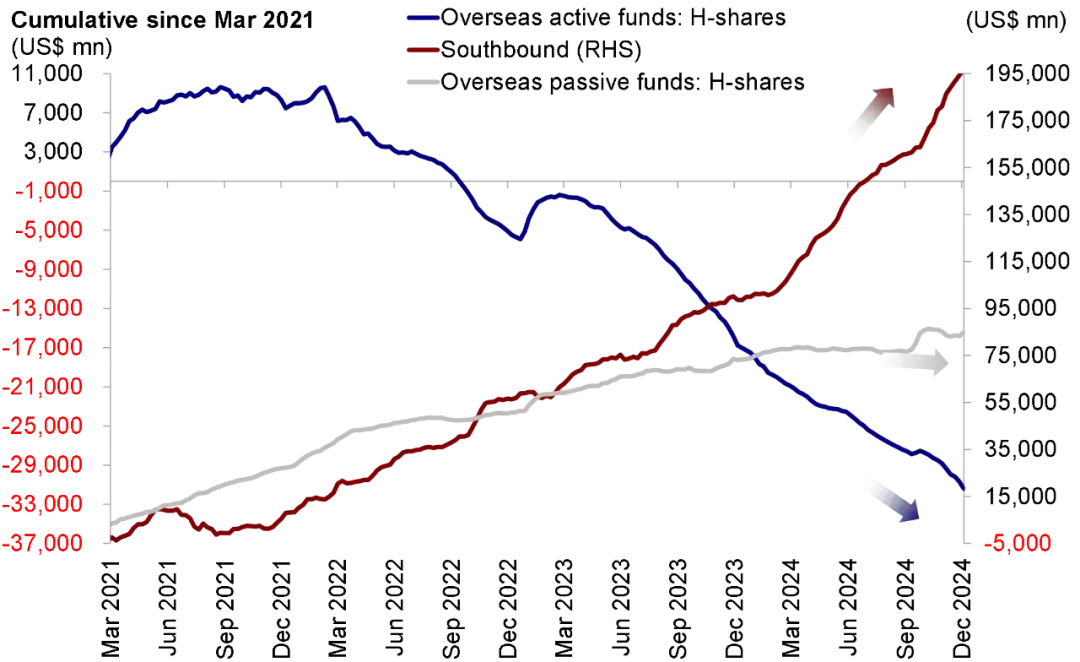

4) Outflow of overseas active funds has expanded, while passive funds have turned into inflow, with accelerated inflow from southbound capital. EPFR data shows that as of December 18, the outflow of overseas active funds from the Chinese stock market has expanded to 0.7 billion USD (vs. a previous outflow of 0.48 billion USD in the prior week), marking ten consecutive weeks of outflow. Meanwhile, overseas passive funds have switched back to inflow of 1.55 billion USD (vs. a prior outflow of 0.23 billion USD). Simultaneously, southbound capital inflow has accelerated compared to the previous week, from a previous inflow of 21.12 billion HKD to an inflow of 25.89 billion HKD.

Chart: The outflow of overseas active funds has expanded, and southbound capital inflow has accelerated.

Key Events

December 31, China's Manufacturing PMI, January 20, Trump officially takes office.

[1]https://www.gov.cn/yaowen/liebiao/202412/content_6992258.htm

[2]https://www.research.cicc.com/zh_CN/report?id=356401&entrance_source=ReportList

[3]https://www.federalreserve.gov/newsevents/pressreleases/monetary20241218a.htm

编辑/jayden