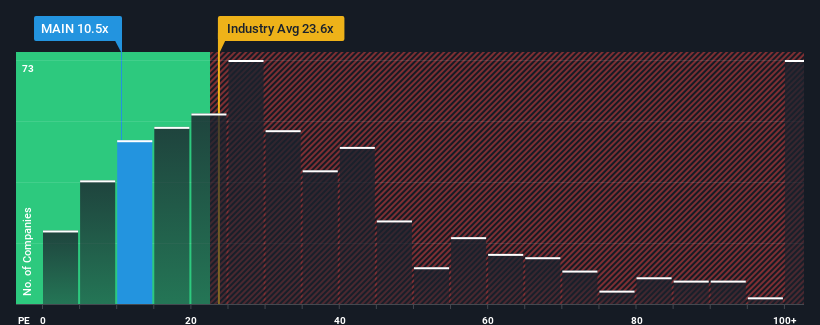

Main Street Capital Corporation's (NYSE:MAIN) price-to-earnings (or "P/E") ratio of 10.5x might make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 19x and even P/E's above 34x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for Main Street Capital as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NYSE:MAIN Price to Earnings Ratio vs Industry December 21st 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Main Street Capital.

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Main Street Capital would need to produce sluggish growth that's trailing the market.

If we review the last year of earnings growth, the company posted a worthy increase of 12%. The solid recent performance means it was also able to grow EPS by 16% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 26% during the coming year according to the six analysts following the company. With the market predicted to deliver 15% growth , that's a disappointing outcome.

In light of this, it's understandable that Main Street Capital's P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Key Takeaway

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Main Street Capital's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You should always think about risks. Case in point, we've spotted 6 warning signs for Main Street Capital you should be aware of, and 2 of them shouldn't be ignored.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Main Street Capital Corporation(紐交所:MAIN)的市盈率爲10.5倍,相較於美國市場看起來似乎是個買入機會,因爲大約一半的公司的市盈率在19倍以上,甚至市盈率超過34倍的情況也相當常見。然而,市盈率低可能是有原因的,需要進一步調查以判斷其合理性。

最近一段時間對Main Street Capital來說是有利的,因爲其盈利增長速度超過大多數其他公司。一種可能性是市盈率低是因爲投資者認爲這種強勁的盈利表現未來可能不再那麼顯著。如果不是這樣,那麼現有股東對股價的未來走勢有理由保持相當樂觀。

紐交所:MAIN市盈率與行業對比 2024年12月21日 如果您想了解分析師對未來的預測,您應該查看我們關於Main Street Capital的免費報告。

If we review the last year of earnings growth, the company posted a worthy increase of 12%. The solid recent performance means it was also able to grow EPS by 16% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

If we review the last year of earnings growth, the company posted a worthy increase of 12%. The solid recent performance means it was also able to grow EPS by 16% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

如果我們回顧過去一年的每股收益增長,公司實現了12%的可觀增長。這一良好的近期表現意味着它在過去三年中總共能夠實現16%的每股收益增長。因此,股東們可能會對中期的收益增長率感到滿意。

如果我們回顧過去一年的每股收益增長,公司實現了12%的可觀增長。這一良好的近期表現意味着它在過去三年中總共能夠實現16%的每股收益增長。因此,股東們可能會對中期的收益增長率感到滿意。