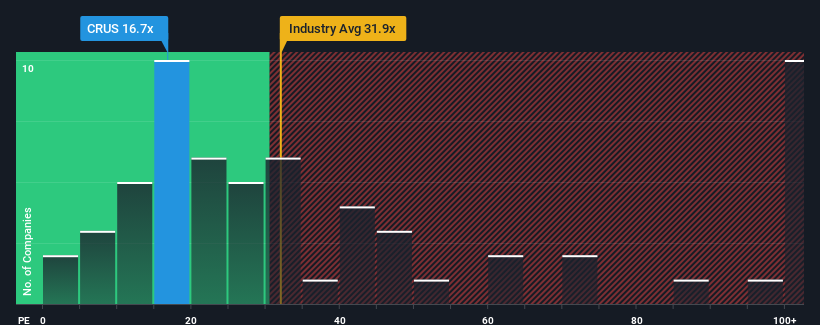

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 19x, you may consider Cirrus Logic, Inc. (NASDAQ:CRUS) as an attractive investment with its 16.7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Recent times have been advantageous for Cirrus Logic as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

NasdaqGS:CRUS Price to Earnings Ratio vs Industry December 18th 2024 Keen to find out how analysts think Cirrus Logic's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Any Growth For Cirrus Logic?

Cirrus Logic's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Retrospectively, the last year delivered an exceptional 135% gain to the company's bottom line. Pleasingly, EPS has also lifted 47% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 2.0% per annum over the next three years. With the market predicted to deliver 11% growth per year, the company is positioned for a weaker earnings result.

With this information, we can see why Cirrus Logic is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Cirrus Logic's P/E

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Cirrus Logic maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Cirrus Logic with six simple checks on some of these key factors.

If you're unsure about the strength of Cirrus Logic's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered an exceptional 135% gain to the company's bottom line. Pleasingly, EPS has also lifted 47% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Retrospectively, the last year delivered an exceptional 135% gain to the company's bottom line. Pleasingly, EPS has also lifted 47% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

回顧過去一年,該公司實現了135%的顯著收益。令人高興的是,每股收益在三年前基礎上也累計提高了47%,得益於過去12個月的增長。因此,可以公平地說,公司最近的盈利增長非常出色。

回顧過去一年,該公司實現了135%的顯著收益。令人高興的是,每股收益在三年前基礎上也累計提高了47%,得益於過去12個月的增長。因此,可以公平地說,公司最近的盈利增長非常出色。