Unfortunately for some shareholders, the Lotus Technology Inc. (NASDAQ:LOT) share price has dived 26% in the last thirty days, prolonging recent pain. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

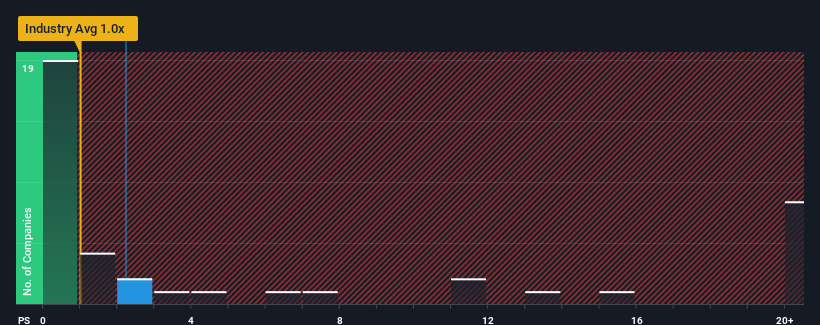

Although its price has dipped substantially, when almost half of the companies in the United States' Auto industry have price-to-sales ratios (or "P/S") below 1x, you may still consider Lotus Technology as a stock probably not worth researching with its 2.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

NasdaqGS:LOT Price to Sales Ratio vs Industry December 17th 2024

How Has Lotus Technology Performed Recently?

Recent times have been advantageous for Lotus Technology as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Lotus Technology.

How Is Lotus Technology's Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Lotus Technology's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 213% gain to the company's top line. This great performance means it was also able to deliver immense revenue growth over the last three years. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 48% per annum over the next three years. With the industry only predicted to deliver 16% per annum, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Lotus Technology's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Lotus Technology's P/S remain high even after its stock plunged. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Lotus Technology's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Plus, you should also learn about these 3 warning signs we've spotted with Lotus Technology (including 2 which shouldn't be ignored).

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should outperform the industry for P/S ratios like Lotus Technology's to be considered reasonable.

There's an inherent assumption that a company should outperform the industry for P/S ratios like Lotus Technology's to be considered reasonable.

有一個內在假設,即公司應該超越行業,才能使像路特斯這樣的市銷率被視爲合理。

有一個內在假設,即公司應該超越行業,才能使像路特斯這樣的市銷率被視爲合理。