Should You Be Excited About PepsiCo, Inc.'s (NASDAQ:PEP) 48% Return On Equity?

Should You Be Excited About PepsiCo, Inc.'s (NASDAQ:PEP) 48% Return On Equity?

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity While some investors are already well versed in financial metrics (hat tip), this article is for those who would like to learn about Return On Equity (ROE) and why it is important. To keep the lesson grounded in practicality, we'll use ROE to better understand PepsiCo, Inc. (NASDAQ:PEP).

虽然一些投资者已经对财务指标相当熟悉(感谢引用),但这篇文章是专为那些想要了解净资产收益率(ROE)及其重要性的人准备的。为使课程更具实用性,我们将使用ROE来更好地理解百事可乐公司(纳斯达克:PEP)。

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

ROE或股本回报率是一个有用的工具,用于评估公司如何有效地利用其股东投入的资金来产生回报。换句话说,它是一个衡量公司股东所提供资本的回报率的盈利能力比率。

How To Calculate Return On Equity?

如何计算股东权益回报率?

Return on equity can be calculated by using the formula:

净资产收益率可以通过以下公式计算:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

股东权益回报率 = 净利润(来自持续运营)÷ 股东权益

So, based on the above formula, the ROE for PepsiCo is:

因此,根据上述公式,百事可乐的roe为:

48% = US$9.4b ÷ US$20b (Based on the trailing twelve months to September 2024).

48% = 94亿美元 ÷ 200亿美元(基于截至2024年9月的过去十二个月)。

The 'return' is the income the business earned over the last year. That means that for every $1 worth of shareholders' equity, the company generated $0.48 in profit.

'回报'是企业在过去一年里赚取的收入。这意味着,对于每值1美元的股东权益,公司产生了0.48美元的利润。

Does PepsiCo Have A Good ROE?

百事可乐的ROE好吗?

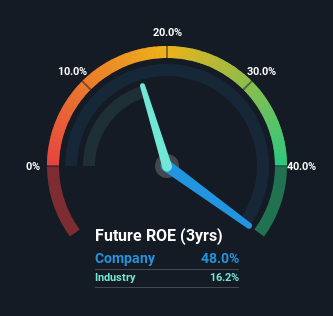

One simple way to determine if a company has a good return on equity is to compare it to the average for its industry. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. As you can see in the graphic below, PepsiCo has a higher ROE than the average (16%) in the Beverage industry.

判断一家公司的股本回报率是否良好的一个简单方法是将其与行业的平均水平进行比较。然而,这种方法仅仅作为粗略检查是有用的,因为同一行业分类内的公司可能有很大差异。正如您在下面的图形中所看到的,百事可乐的ROE高于饮料行业的平均水平(16%)。

That's clearly a positive. With that said, a high ROE doesn't always indicate high profitability. A higher proportion of debt in a company's capital structure may also result in a high ROE, where the high debt levels could be a huge risk . Our risks dashboardshould have the 2 risks we have identified for PepsiCo.

这显然是一个积极的因素。不过,高ROE并不总是意味着高盈利能力。公司资本结构中较高的债务比例也可能导致高ROE,而高债务水平可能是巨大的风险。我们的风险仪表盘应该包含我们为百事可乐识别的两个风险。

How Does Debt Impact ROE?

债务对ROE的影响是怎样的?

Most companies need money -- from somewhere -- to grow their profits. That cash can come from retained earnings, issuing new shares (equity), or debt. In the case of the first and second options, the ROE will reflect this use of cash, for growth. In the latter case, the debt required for growth will boost returns, but will not impact the shareholders' equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

大多数公司需要资金——来自某个地方——来增加他们的利润。这笔资金可以来自保留盈余、发行新股(股本)或债务。在前两种情况下,ROE将反映这种资金的使用,以支持增长。在后者的情况下,为增长所需的债务将提高回报,但不会影响股东的权益。因此,债务的使用可以改善ROE,尽管在恶劣天气的情况下伴随着额外风险,比喻来说。

Combining PepsiCo's Debt And Its 48% Return On Equity

结合百事可乐的负债和其48%的净资产收益率

PepsiCo clearly uses a high amount of debt to boost returns, as it has a debt to equity ratio of 2.30. While no doubt that its ROE is impressive, we would have been even more impressed had the company achieved this with lower debt. Debt increases risk and reduces options for the company in the future, so you generally want to see some good returns from using it.

百事可乐显然利用高负债来提升回报,因为它的负债与股本比率为2.30。虽然它的ROE无疑令人印象深刻,但如果公司能在更低负债的情况下实现这一点,我们会更为印象深刻。负债增加了风险,减少了公司未来的选择,因此一般希望看到使用负债所带来的良好回报。

Conclusion

结论

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. Companies that can achieve high returns on equity without too much debt are generally of good quality. If two companies have the same ROE, then I would generally prefer the one with less debt.

净资产收益率是评估企业盈利能力以及将利润回馈给股东的一个有用指标。能够在没有过多负债的情况下实现高净资产收益率的公司通常质量较高。如果两家公司具有相同的ROE,我通常会更偏好负债较少的那家。

But when a business is high quality, the market often bids it up to a price that reflects this. It is important to consider other factors, such as future profit growth -- and how much investment is required going forward. So you might want to check this FREE visualization of analyst forecasts for the company.

但是,当一项业务质量高时,市场通常将其价格炒得很高,这反映了这一点。考虑其他因素也很重要,例如未来利润增长——以及未来需要多少投资。因此,您可能想查看这个免费的分析师预测可视化。

But note: PepsiCo may not be the best stock to buy. So take a peek at this free list of interesting companies with high ROE and low debt.

但请注意:百事可乐可能不是最值得买入的股票。因此,来看看这个关于高ROE和低负债的有趣公司免费列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有反馈?对内容有疑虑?请直接与我们联系。或者,发送电子邮件至 editorial-team (at) simplywallst.com。

这篇来自Simply Wall St的文章是一般性的。我们根据历史数据和分析师预测提供评论,采用无偏见的方法,我们的文章并不旨在提供财务建议。它不构成对任何股票的买入或卖出建议,也未考虑到您的目标或财务状况。我们旨在为您提供以基本数据驱动的长期分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St在提到的任何股票中均没有持仓。

译文内容由第三方软件翻译。