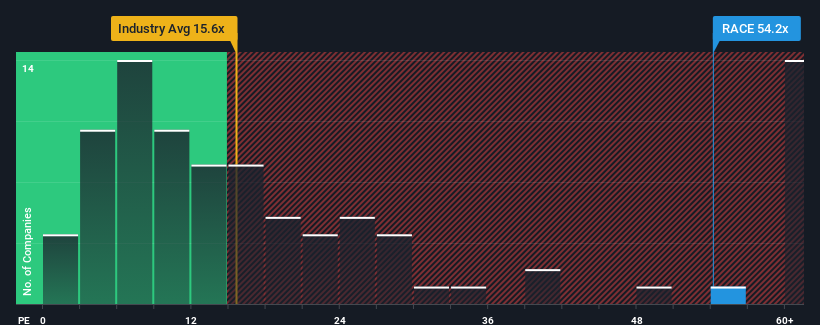

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 19x, you may consider Ferrari N.V. (NYSE:RACE) as a stock to avoid entirely with its 54.2x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Ferrari certainly has been doing a good job lately as it's been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:RACE Price to Earnings Ratio vs Industry December 15th 2024 Keen to find out how analysts think Ferrari's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Enough Growth For Ferrari?

Ferrari's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 22% last year. The latest three year period has also seen an excellent 68% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 13% per year during the coming three years according to the analysts following the company. That's shaping up to be materially higher than the 11% per annum growth forecast for the broader market.

With this information, we can see why Ferrari is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Ferrari's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Plus, you should also learn about this 1 warning sign we've spotted with Ferrari.

You might be able to find a better investment than Ferrari. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company grew earnings per share by an impressive 22% last year. The latest three year period has also seen an excellent 68% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Taking a look back first, we see that the company grew earnings per share by an impressive 22% last year. The latest three year period has also seen an excellent 68% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

首先回顧一下,我們看到該公司的每股收益在去年增長了令人印象深刻的22%。最近三年期間,每股收益整體增長了68%,得益於其短期表現。因此,可以公平地說,最近的盈利增長對公司來說非常優秀。

首先回顧一下,我們看到該公司的每股收益在去年增長了令人印象深刻的22%。最近三年期間,每股收益整體增長了68%,得益於其短期表現。因此,可以公平地說,最近的盈利增長對公司來說非常優秀。