Cactus, Inc.'s (NYSE:WHD) Stock Is Going Strong: Is the Market Following Fundamentals?

Cactus, Inc.'s (NYSE:WHD) Stock Is Going Strong: Is the Market Following Fundamentals?

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity Cactus (NYSE:WHD) has had a great run on the share market with its stock up by a significant 12% over the last three months. Since the market usually pay for a company's long-term fundamentals, we decided to study the company's key performance indicators to see if they could be influencing the market. In this article, we decided to focus on Cactus' ROE.

Cactus (纽交所:WHD) 在股市上表现出色,过去三个月其股票上涨了显著的12%。由于市场通常会关注公司的长期基本面,我们决定研究公司的关键绩效因子,以查看它们是否会影响市场。本文中,我们决定关注Cactus的ROE。

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

ROE,即净资产收益率,是评估公司如何有效地利用来自股东投资的工具。简单来说,它用于评估公司相对于其股本的盈利能力。

How Is ROE Calculated?

净资产收益率怎么计算?

Return on equity can be calculated by using the formula:

净资产收益率可以通过以下公式计算:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

股东权益回报率 = 净利润(来自持续运营)÷ 股东权益

So, based on the above formula, the ROE for Cactus is:

因此,根据上述公式,Cactus的ROE为:

20% = US$237m ÷ US$1.2b (Based on the trailing twelve months to September 2024).

20% = US$23700万 ÷ US$12亿 (以截至2024年9月的过去十二个月为基础)。

The 'return' is the profit over the last twelve months. Another way to think of that is that for every $1 worth of equity, the company was able to earn $0.20 in profit.

'回报'是过去十二个月的利润。另一种思考方式是,对于每1美元的股本,公司能够赚取0.20美元的利润。

Why Is ROE Important For Earnings Growth?

ROE为什么对净利润增长很重要?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

到目前为止,我们已经了解到roe是公司盈利能力的一种衡量标准。根据公司选择重新投资或“留存”的利润比例,我们能够评估公司未来产生利润的能力。其他条件不变的情况下,roe和盈利留存越高,相较于不具备这些特征的公司,企业的增长率越高。

Cactus' Earnings Growth And 20% ROE

Cactus的收益增长和20%的ROE

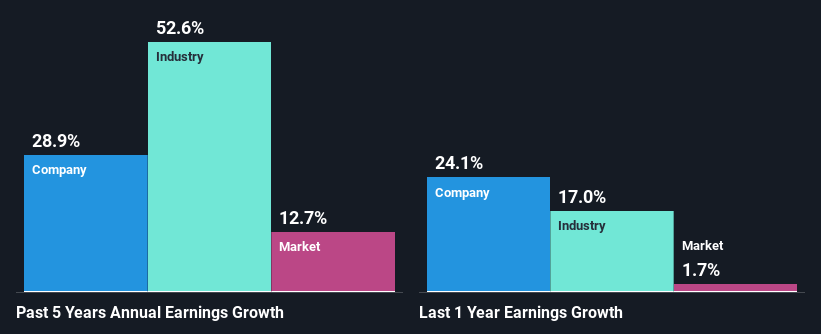

To start with, Cactus' ROE looks acceptable. Further, the company's ROE compares quite favorably to the industry average of 14%. This probably laid the ground for Cactus' significant 29% net income growth seen over the past five years. We reckon that there could also be other factors at play here. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

首先,Cactus的ROE看起来是可以接受的。此外,该公司的ROE与行业平均14%相比相当有利。这可能为Cactus在过去五年中看到的29%的净利润增长奠定了基础。我们认为这里可能还有其他因素在起作用。例如,公司的管理层可能做出了一些好的战略决策,或者公司有着较低的分红比率。

We then compared Cactus' net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 53% in the same 5-year period, which is a bit concerning.

然后我们将Cactus的净利润增长与行业进行了比较,发现该公司的增长数据低于同五年期间行业平均增长率53%,这有些令人担忧。

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Has the market priced in the future outlook for WHD? You can find out in our latest intrinsic value infographic research report.

给公司附加价值的基础在很大程度上与其盈利增长相关。 投资者接下来需要判断的是,预期的盈利增长,或者说缺乏盈利增长,是否已经体现在股价中。 通过这样做,他们可以了解到股票是走向一片清澈的沃土,还是等待着沼泽般的水域。市场是否已经考虑了WHD的未来前景?您可以在我们最新的内在价值信息图研究报告中找到答案。

Is Cactus Using Its Retained Earnings Effectively?

Cactus是否有效利用其留存收益?

Cactus' three-year median payout ratio to shareholders is 21%, which is quite low. This implies that the company is retaining 79% of its profits. So it seems like the management is reinvesting profits heavily to grow its business and this reflects in its earnings growth number.

Cactus对股东的三年中位支付比率为21%,这相当低。这意味着公司留存了79%的利润。因此,管理层似乎在重金再投资利润以发展其业务,这也反映在其盈利增长数据中。

Moreover, Cactus is determined to keep sharing its profits with shareholders which we infer from its long history of five years of paying a dividend. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 14% over the next three years. However, the company's ROE is not expected to change by much despite the lower expected payout ratio.

此外,Cactus决心继续与股东分享其利润,这可以从其持续五年的分红历史中推断出来。我们最新的分析师数据显示,预计公司未来的支付比率将在接下来的三年内降至14%。然而,尽管预期支付比率降低,公司的ROE预计不会有太大变化。

Conclusion

结论

Overall, we are quite pleased with Cactus' performance. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. As a result, the decent growth in its earnings is not surprising. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

总体来说,我们对Cactus的表现非常满意。尤其是,我们喜欢该公司在其业务上进行大量再投资,并且回报率很高。因此,其盈利增长十分可观并不令人惊讶。尽管如此,最新的行业分析师预测显示,公司的盈利增长预计将放缓。这些分析师的预期是基于行业的广泛预期,还是基于公司的基本面?点击这里查看我们分析师对于该公司的预测页面。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有反馈?对内容有疑虑?请直接与我们联系。或者,发送电子邮件至 editorial-team (at) simplywallst.com。

这篇来自Simply Wall St的文章是一般性的。我们根据历史数据和分析师预测提供评论,采用无偏见的方法,我们的文章并不旨在提供财务建议。它不构成对任何股票的买入或卖出建议,也未考虑到您的目标或财务状况。我们旨在为您提供以基本数据驱动的长期分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St在提到的任何股票中均没有持仓。

译文内容由第三方软件翻译。