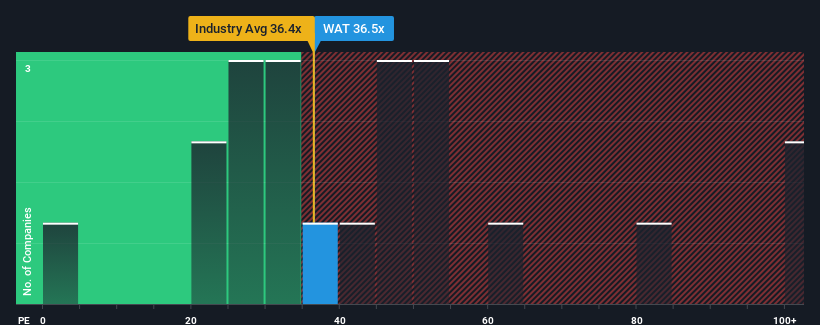

With a price-to-earnings (or "P/E") ratio of 36.5x Waters Corporation (NYSE:WAT) may be sending very bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 19x and even P/E's lower than 11x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

While the market has experienced earnings growth lately, Waters' earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:WAT Price to Earnings Ratio vs Industry December 13th 2024 Want the full picture on analyst estimates for the company? Then our free report on Waters will help you uncover what's on the horizon.

How Is Waters' Growth Trending?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Waters' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 4.9% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 6.6% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 11% per year over the next three years. With the market predicted to deliver 11% growth per annum, the company is positioned for a comparable earnings result.

With this information, we find it interesting that Waters is trading at a high P/E compared to the market. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for disappointment if the P/E falls to levels more in line with the growth outlook.

What We Can Learn From Waters' P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Waters currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Waters, and understanding should be part of your investment process.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 4.9% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 6.6% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Retrospectively, the last year delivered a frustrating 4.9% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 6.6% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

回顧過去一年,公司底線遭遇了令人失望的4.9%的下降。過去三年同樣不樂觀,公司的每股收益累計下降了6.6%。因此,不幸的是,我們必須承認公司在這段時間內的盈利增長表現不佳。

回顧過去一年,公司底線遭遇了令人失望的4.9%的下降。過去三年同樣不樂觀,公司的每股收益累計下降了6.6%。因此,不幸的是,我們必須承認公司在這段時間內的盈利增長表現不佳。