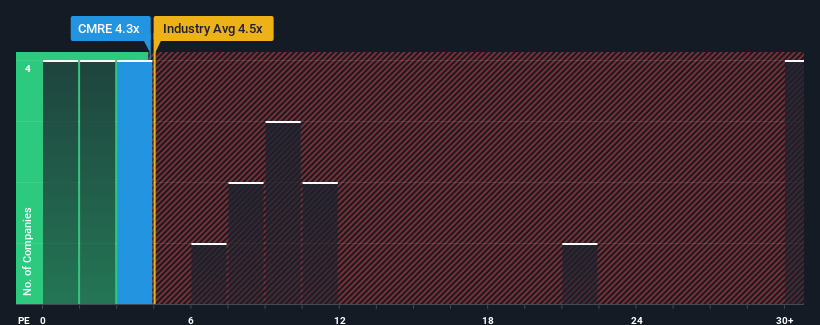

With a price-to-earnings (or "P/E") ratio of 4.3x Costamare Inc. (NYSE:CMRE) may be sending very bullish signals at the moment, given that almost half of all companies in the United States have P/E ratios greater than 20x and even P/E's higher than 35x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Costamare could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

NYSE:CMRE Price to Earnings Ratio vs Industry December 13th 2024 Want the full picture on analyst estimates for the company? Then our free report on Costamare will help you uncover what's on the horizon.

Is There Any Growth For Costamare?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Costamare's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 18% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 36% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Turning to the outlook, the next year should generate growth of 3.6% as estimated by the dual analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 15%, which is noticeably more attractive.

With this information, we can see why Costamare is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Costamare maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Having said that, be aware Costamare is showing 4 warning signs in our investment analysis, and 1 of those doesn't sit too well with us.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 18% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 36% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Retrospectively, the last year delivered a frustrating 18% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 36% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

回顧過去一年,公司淨利潤出現了令人沮喪的18%的下降。然而,在此之前的幾個強勁年份使得它在過去三年中的每股收益總體上仍增長了令人印象深刻的36%。所以我們可以首先確認,公司在此期間總體上做得很好,儘管經歷了一些波折。

回顧過去一年,公司淨利潤出現了令人沮喪的18%的下降。然而,在此之前的幾個強勁年份使得它在過去三年中的每股收益總體上仍增長了令人印象深刻的36%。所以我們可以首先確認,公司在此期間總體上做得很好,儘管經歷了一些波折。