Gulfport Energy (NYSE:GPOR) Might Have The Makings Of A Multi-Bagger

Gulfport Energy (NYSE:GPOR) Might Have The Makings Of A Multi-Bagger

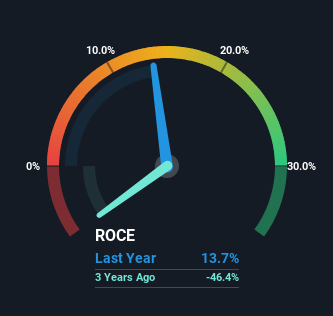

0.14 = US$391m ÷ (US$3.2b - US$327m)

0.14 = US$391m ÷ (US$3.2b - US$327m) If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Speaking of which, we noticed some great changes in Gulfport Energy's (NYSE:GPOR) returns on capital, so let's have a look.

如果我们想找到一个潜在的多倍收益股,通常会有一些潜在趋势可以提供线索。首先,我们想要确定一个逐渐增长的资本回报率(ROCE),然后与此相辅相成的是不断增加的资本基础。基本上,这意味着公司有盈利的项目可以继续再投资,这是典型的复合增长机器的特征。说到这一点,我们注意到Gulfport Energy(纽交所:GPOR)的资本回报率发生了一些重大变化,我们来看看。

What Is Return On Capital Employed (ROCE)?

什么是资本回报率(ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Gulfport Energy, this is the formula:

为了澄清,如果你不确定,ROCE是用来评估公司在其业务中投资的资本所赚取的税前收入(以百分比表示)的指标。要计算Gulfport Energy的这个指标,公式如下:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

资本利用率 = 利息和税前利润(EBIT) ÷ (总资产 - 流动负债)

0.14 = US$391m ÷ (US$3.2b - US$327m) (Based on the trailing twelve months to September 2024).

0.14 = US$39100万 ÷ (US$32亿 - US$327m)(基于2024年9月的过去十二个月)。

Thus, Gulfport Energy has an ROCE of 14%. That's a relatively normal return on capital, and it's around the 12% generated by the Oil and Gas industry.

因此,Gulfport Energy的资本回报率为14%。这算是一个相对正常的资本回报,接近于油气行业产生的12%。

Above you can see how the current ROCE for Gulfport Energy compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Gulfport Energy .

上面你可以看到Gulfport Energy当前的资本回报率与其之前的资本回报率的比较,但从过去你能了解到的有限。如果你感兴趣,可以查看我们对Gulfport Energy的免费分析师报告中的分析师预测。

How Are Returns Trending?

回报率的趋势如何?

We're pretty happy with how the ROCE has been trending at Gulfport Energy. The data shows that returns on capital have increased by 55% over the trailing five years. That's not bad because this tells for every dollar invested (capital employed), the company is increasing the amount earned from that dollar. In regards to capital employed, Gulfport Energy appears to been achieving more with less, since the business is using 47% less capital to run its operation. Gulfport Energy may be selling some assets so it's worth investigating if the business has plans for future investments to increase returns further still.

我们对Gulfport Energy的资本回报率的趋势感到非常满意。数据显示,在过去五年中,资本回报率提高了55%。这并不少,因为这表明每投资一美元(使用的资本),公司从这笔美元中获取的收入在增加。关于使用的资本,Gulfport Energy似乎以更少的资本取得了更多的成就,因为该业务使用的资本减少了47%来运行其事件;事件控件。Gulfport Energy可能在出售一些资产,所以值得调查该企业是否有计划进行未来的投资,以进一步提高回报。

In Conclusion...

结论...

In summary, it's great to see that Gulfport Energy has been able to turn things around and earn higher returns on lower amounts of capital. And with the stock having performed exceptionally well over the last three years, these patterns are being accounted for by investors. In light of that, we think it's worth looking further into this stock because if Gulfport Energy can keep these trends up, it could have a bright future ahead.

总之,看到Gulfport Energy能够扭转局面并在较低资本金额上获得更高的收益是很好的。而且,随着股票在过去三年表现得非常出色,投资者也在考虑这些模式。基于此,我们认为值得进一步关注这只股票,因为如果Gulfport Energy能够保持这些趋势,可能会有辉煌明天。

If you want to continue researching Gulfport Energy, you might be interested to know about the 2 warning signs that our analysis has discovered.

如果你想继续研究Gulfport Energy,你可能会对我们的分析发现的2个预警信号感兴趣。

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

对于喜欢投资于稳健公司的投资者,可以查看这个免费的稳健资产负债表和高股本回报率公司的列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有反馈?对内容有疑虑?请直接与我们联系。或者,发送电子邮件至 editorial-team (at) simplywallst.com。

这篇来自Simply Wall St的文章是一般性的。我们根据历史数据和分析师预测提供评论,采用无偏见的方法,我们的文章并不旨在提供财务建议。它不构成对任何股票的买入或卖出建议,也未考虑到您的目标或财务状况。我们旨在为您提供以基本数据驱动的长期分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St在提到的任何股票中均没有持仓。

译文内容由第三方软件翻译。