Sociedad Química Y Minera De Chile (NYSE:SQM) Shareholder Returns Have Been Notable, Earning 70% in 5 Years

Sociedad Química Y Minera De Chile (NYSE:SQM) Shareholder Returns Have Been Notable, Earning 70% in 5 Years

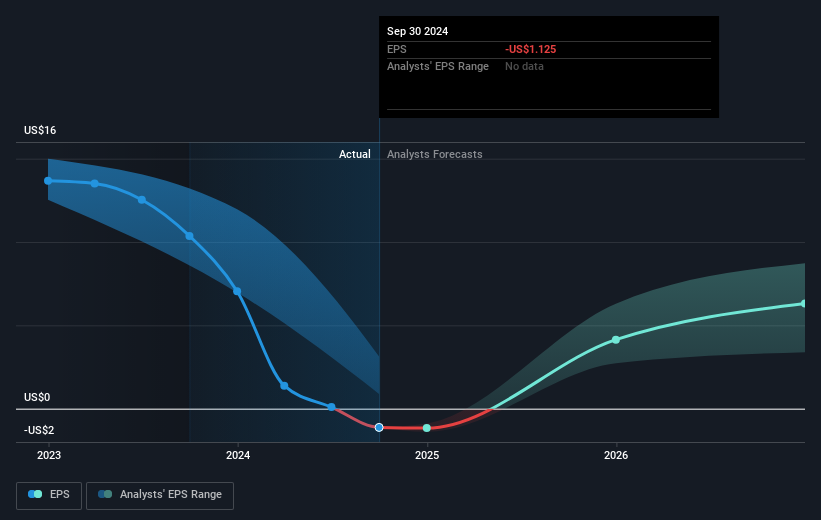

Over half a decade, Sociedad Química y Minera de Chile managed to grow its earnings per share at 29% a year. We do note that extraordinary items have impacted its earnings history. The EPS growth is more impressive than the yearly share price gain of 8% over the same period. So it seems the market isn't so enthusiastic about the stock these days.

Over half a decade, Sociedad Química y Minera de Chile managed to grow its earnings per share at 29% a year. We do note that extraordinary items have impacted its earnings history. The EPS growth is more impressive than the yearly share price gain of 8% over the same period. So it seems the market isn't so enthusiastic about the stock these days. When you buy and hold a stock for the long term, you definitely want it to provide a positive return. Better yet, you'd like to see the share price move up more than the market average. Unfortunately for shareholders, while the Sociedad Química y Minera de Chile S.A. (NYSE:SQM) share price is up 46% in the last five years, that's less than the market return. Unfortunately the share price is down 26% in the last year.

当你买入并持有一只股票较长时间时,你肯定希望它能提供正收益。更好的是,你希望股价的上涨幅度超过市场平均水平。不幸的是,对于股东而言,虽然智利化学与矿业公司(NYSE:SQM)的股价在过去五年上涨了46%,但这仍低于市场回报。不幸的是,过去一年股价下跌了26%。

After a strong gain in the past week, it's worth seeing if longer term returns have been driven by improving fundamentals.

在过去一周强劲上涨后,值得看看长期回报是否是由基本面改善驱动的。

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

用本杰明·格雷厄姆的话说:在短期内,市场像个投票机,但在长期内,它就是个称重机。检视市场情绪如何随时间变化的一种方法是观察一家公司的股价与每股收益(EPS)之间的互动。

Over half a decade, Sociedad Química y Minera de Chile managed to grow its earnings per share at 29% a year. We do note that extraordinary items have impacted its earnings history. The EPS growth is more impressive than the yearly share price gain of 8% over the same period. So it seems the market isn't so enthusiastic about the stock these days.

在五年多的时间里,智利化学与矿业公司的每股收益年均增长29%。我们确实注意到,特殊项目影响了它的收益历史。在同一时期,每股收益的增长比每年股价增长8%更令人印象深刻。因此,看来市场对这只股票最近并不那么热衷。

You can see how EPS has changed over time in the image below (click on the chart to see the exact values).

您可以在下面的图像中查看每股收益随时间的变化(单击图表查看确切值)。

It might be well worthwhile taking a look at our free report on Sociedad Química y Minera de Chile's earnings, revenue and cash flow.

查看我们关于智利化学矿业公司的盈利、营业收入和现金流的免费报告可能会非常值得。

What About Dividends?

关于分红派息的问题

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. We note that for Sociedad Química y Minera de Chile the TSR over the last 5 years was 70%, which is better than the share price return mentioned above. This is largely a result of its dividend payments!

考虑总股东回报以及任何给定股票的股价回报是非常重要的。 TSR 是一种回报计算,它考虑了现金分红的价值(假设收到的任何分红都被再投资)以及任何折扣融资和分拆计算的价值。因此,对于支付慷慨分红的公司来说,TSR 往往比股价回报高得多。我们注意到智利化学矿业公司过去五年的 TSR 为 70%,这比上述股价回报要好得多。这主要是由于其分红支付的结果!

A Different Perspective

不同的视角

Sociedad Química y Minera de Chile shareholders are down 26% for the year (even including dividends), but the market itself is up 31%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Longer term investors wouldn't be so upset, since they would have made 11%, each year, over five years. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Take risks, for example - Sociedad Química y Minera de Chile has 2 warning signs we think you should be aware of.

智利化学矿业公司的股东今年亏损了26%(即使包括分红),但市场本身上涨了31%。即使是优质股票的股价有时也会下跌,但我们希望在对业务产生过多关注之前,看到基本指标的改善。长期投资者不会太失望,因为他们在五年里每年获得了11%的收益。如果基本数据继续表明长期可持续增长,目前的卖出可能是一个值得考虑的机会。虽然考虑市场状况对股价的不同影响非常重要,但还有其他因素更为重要。以风险为例 — 智利化学矿业公司有2个警告信号,我们认为您应该关注。

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

如果你更倾向于查看其他公司——一个财务状况可能更优的公司——那么不要错过这个免费的公司列表,它们已经证明能够实现盈利增长。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

请注意,本文中引用的市场回报反映了当前在美国交易所上市股票的市场加权平均回报。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有反馈?对内容有疑虑?请直接与我们联系。或者,发送电子邮件至 editorial-team (at) simplywallst.com。

这篇来自Simply Wall St的文章是一般性的。我们根据历史数据和分析师预测提供评论,采用无偏见的方法,我们的文章并不旨在提供财务建议。它不构成对任何股票的买入或卖出建议,也未考虑到您的目标或财务状况。我们旨在为您提供以基本数据驱动的长期分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St在提到的任何股票中均没有持仓。

译文内容由第三方软件翻译。