Despite an already strong run, Tuya Inc. (NYSE:TUYA) shares have been powering on, with a gain of 26% in the last thirty days. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 14% over that time.

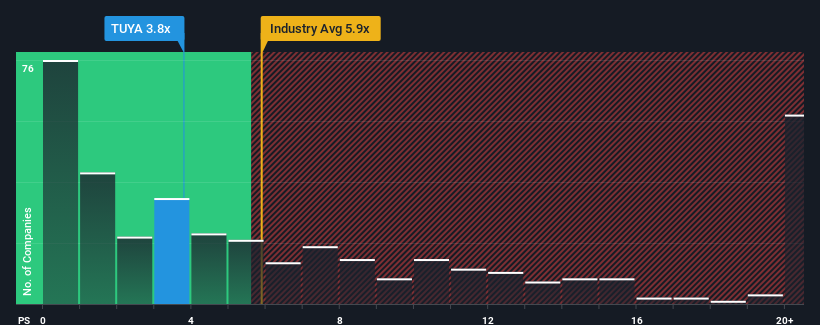

Although its price has surged higher, Tuya's price-to-sales (or "P/S") ratio of 3.8x might still make it look like a buy right now compared to the Software industry in the United States, where around half of the companies have P/S ratios above 5.8x and even P/S above 13x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

NYSE:TUYA Price to Sales Ratio vs Industry December 10th 2024

What Does Tuya's P/S Mean For Shareholders?

Tuya certainly has been doing a good job lately as it's been growing revenue more than most other companies. It might be that many expect the strong revenue performance to degrade substantially, which has repressed the share price, and thus the P/S ratio. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on Tuya will help you uncover what's on the horizon.

How Is Tuya's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as Tuya's is when the company's growth is on track to lag the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 33%. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 3.2% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

Shifting to the future, estimates from the seven analysts covering the company suggest revenue should grow by 19% over the next year. With the industry predicted to deliver 27% growth, the company is positioned for a weaker revenue result.

With this information, we can see why Tuya is trading at a P/S lower than the industry. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Tuya's P/S?

Tuya's stock price has surged recently, but its but its P/S still remains modest. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Tuya's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Tuya with six simple checks.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The only time you'd be truly comfortable seeing a P/S as low as Tuya's is when the company's growth is on track to lag the industry.

The only time you'd be truly comfortable seeing a P/S as low as Tuya's is when the company's growth is on track to lag the industry.

你唯一會真正感到舒適的看到如此低的市銷率時,是當公司的增長跟不上行業時。

你唯一會真正感到舒適的看到如此低的市銷率時,是當公司的增長跟不上行業時。