Wayfair (NYSE:W) Shareholders Are up 11% This Past Week, but Still in the Red Over the Last Three Years

Wayfair (NYSE:W) Shareholders Are up 11% This Past Week, but Still in the Red Over the Last Three Years

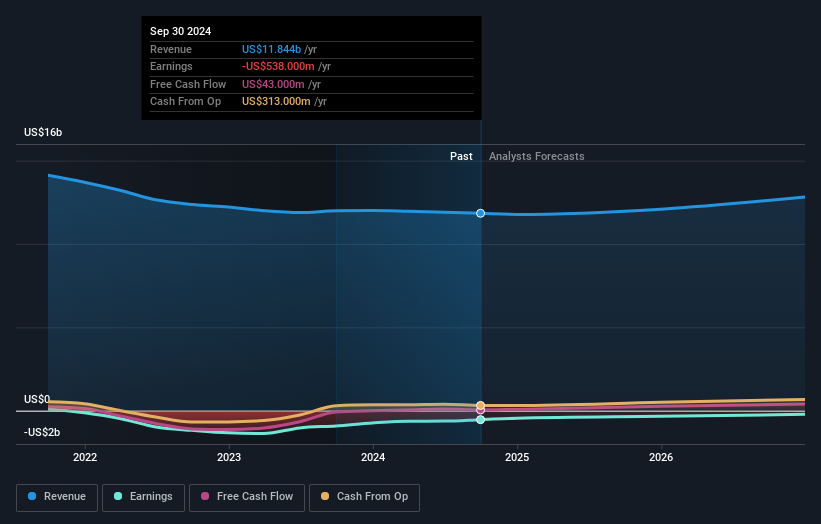

Over the last three years, Wayfair's revenue dropped 5.4% per year. That is not a good result. Having said that the 20% annualized share price decline highlights the risk of investing in unprofitable companies. We're generally averse to companies with declining revenues, but we're not alone in that. There's no more than a snowball's chance in hell that share price will head back to its old highs, in the short term.

Over the last three years, Wayfair's revenue dropped 5.4% per year. That is not a good result. Having said that the 20% annualized share price decline highlights the risk of investing in unprofitable companies. We're generally averse to companies with declining revenues, but we're not alone in that. There's no more than a snowball's chance in hell that share price will head back to its old highs, in the short term. This month, we saw the Wayfair Inc. (NYSE:W) up an impressive 38%. But that doesn't change the fact that the returns over the last three years have been stomach churning. To wit, the share price sky-dived 74% in that time. So it sure is nice to see a bit of an improvement. But the more important question is whether the underlying business can justify a higher price still.

本月,我们看到Wayfair Inc.(纽交所:W)上涨了令人印象深刻的38%。但是,这并不改变过去三年的回报令人感到不适的事实。也就是说,股价在这段时间内暴跌了74%。所以能看到一点改善真是好事。然而,更重要的问题是基础业务是否能够证明更高的价格。

While the last three years has been tough for Wayfair shareholders, this past week has shown signs of promise. So let's look at the longer term fundamentals and see if they've been the driver of the negative returns.

虽然过去三年对Wayfair的股东来说很艰难,但过去一周却显现出一些希望。那么让我们看看长期的基本面,看看它们是否导致了负回报。

Given that Wayfair didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually desire strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

考虑到Wayfair在过去 twelve 个月内没有盈利,我们将关注营业收入增长,以快速了解其业务发展。未盈利公司的股东通常期望强劲的营业收入增长。如你所想,当快速的营业收入增长得到保持时,往往会导致快速的利润增长。

Over the last three years, Wayfair's revenue dropped 5.4% per year. That is not a good result. Having said that the 20% annualized share price decline highlights the risk of investing in unprofitable companies. We're generally averse to companies with declining revenues, but we're not alone in that. There's no more than a snowball's chance in hell that share price will head back to its old highs, in the short term.

在过去三年中,Wayfair的营业收入每年下降了5.4%。这不是一个好结果。尽管如此,20%的年化股价下降突显了投资于未盈利公司的风险。我们通常不喜欢营业收入下降的公司,但我们并不孤单。在短期内,股价重返其旧高位的机会微乎其微。

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

以下图片显示了收益和营收随时间的变化(如果你点击图片,可以看到更详细的信息)。

It's probably worth noting that the CEO is paid less than the median at similar sized companies. It's always worth keeping an eye on CEO pay, but a more important question is whether the company will grow earnings throughout the years. So it makes a lot of sense to check out what analysts think Wayfair will earn in the future (free profit forecasts).

值得注意的是,CEO的薪酬低于同类公司中位数。监控CEO薪酬总是值得的,但更重要的问题是公司是否能在未来几年内增长营业收入。因此,查看分析师对wayfair未来盈利的看法(免费盈利预测)是非常有意义的。

A Different Perspective

另一种看法

While the broader market gained around 34% in the last year, Wayfair shareholders lost 2.5%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. However, the loss over the last year isn't as bad as the 7% per annum loss investors have suffered over the last half decade. We'd need to see some sustained improvements in the key metrics before we could muster much enthusiasm. It's always interesting to track share price performance over the longer term. But to understand Wayfair better, we need to consider many other factors. Case in point: We've spotted 4 warning signs for Wayfair you should be aware of, and 1 of them shouldn't be ignored.

虽然大盘在过去一年中上涨了大约34%,但wayfair的股东却损失了2.5%。然而,请记住,即使是最好的股票在十二个月的时间内有时也会表现不如大盘。然而,过去一年的损失并没有好到哪去,投资者在过去五年中每年损失7%。我们需要看到一些关键指标的持续改善,才能激发我们更多的热情。长期跟踪股价表现总是很有趣。但要更好地理解wayfair,我们需要考虑许多其他因素。举个例子:我们发现了4个wayfair的警告信号,您应该对此保持警惕,其中1个信号不容忽视。

For those who like to find winning investments this free list of undervalued companies with recent insider purchasing, could be just the ticket.

对于那些喜欢寻找获胜投资的人来说,最近有内部购买的低估公司免费列表可能是一个很好的选择。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

请注意,本文所引述的市场回报反映了目前在美国交易所上市的股票的市场加权平均回报。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。