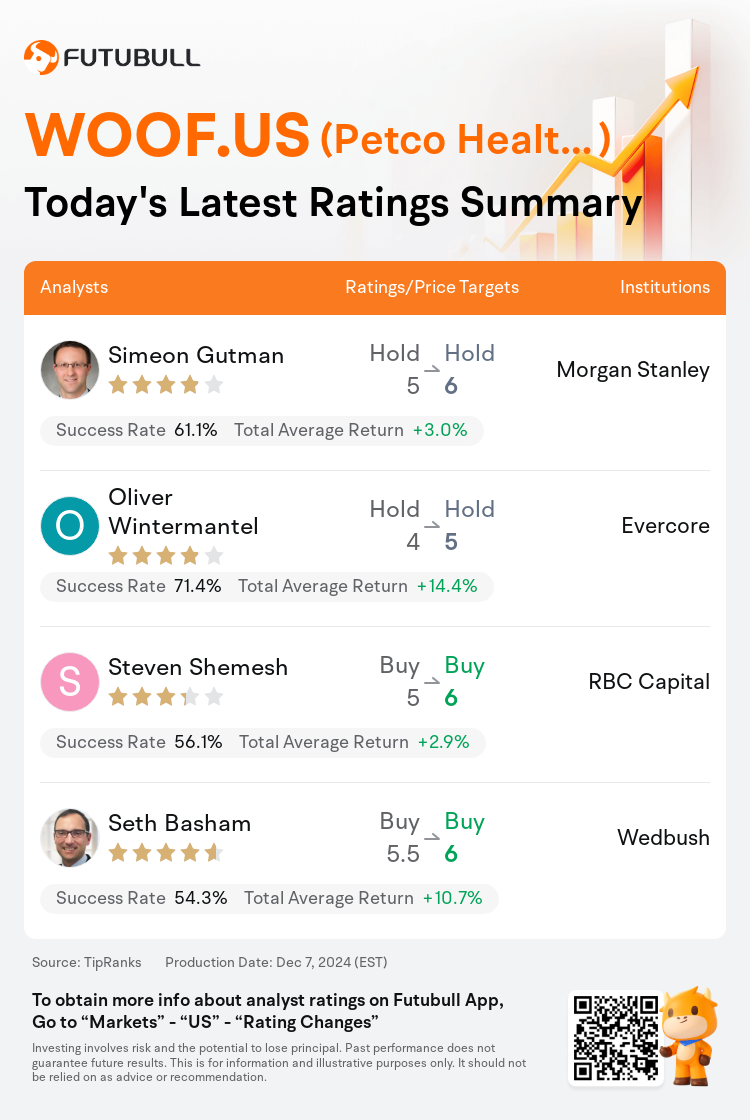

On Dec 07, major Wall Street analysts update their ratings for $Petco Health and Wellness (WOOF.US)$, with price targets ranging from $5 to $6.

Morgan Stanley analyst Simeon Gutman maintains with a hold rating, and adjusts the target price from $5 to $6.

Evercore analyst Oliver Wintermantel maintains with a hold rating, and adjusts the target price from $4 to $5.

RBC Capital analyst Steven Shemesh maintains with a buy rating, and adjusts the target price from $5 to $6.

RBC Capital analyst Steven Shemesh maintains with a buy rating, and adjusts the target price from $5 to $6.

Wedbush analyst Seth Basham maintains with a buy rating, and adjusts the target price from $5.5 to $6.

Furthermore, according to the comprehensive report, the opinions of $Petco Health and Wellness (WOOF.US)$'s main analysts recently are as follows:

Petco's adoption of strategic initiatives aimed at business enhancement appears promising, showing signs of stabilization. However, the perceived risk/reward balance is considered broad, with significant potential variations in outcomes.

Petco's Q3 results were modestly beyond expectations, and the enhancement of EBIT margins indicates the company's successful strategies, according to an analyst. Despite a sharp retracement from its 2022 peak, there is a belief that in the near term, mix, market share pressures, and company-specific aspects will influence earnings and stock performance through 2025. Over a longer horizon, the company is viewed positively due to its strong position within the appealing pet industry.

The company delivered another consistent quarter marked by sequential top-line improvement and margin efforts, which led to a 13% year-over-year EBITDA growth. Petco's consistent performance and margin progress are expected to help the stock close the multiple gap relative to its peers.

Petco's third quarter results surpassed comparable and EBITDA expectations, however, its fourth quarter guidance slightly fell short of expectations. The outlook for the fourth quarter is considered appropriately conservative given the dynamic environment, but there is potential for improvement as Petco's profit-first strategy appears to be fostering margin enhancement through supply chain savings and operational efficiencies.

Petco's Q3 update appears favorable, yet there remains hesitancy to pursue aggressively due to below-expectations Q4 guidance, persisting limited visibility, and significant ongoing tasks.

Here are the latest investment ratings and price targets for $Petco Health and Wellness (WOOF.US)$ from 4 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間12月7日,多家華爾街大行更新了$Petco Health and Wellness (WOOF.US)$的評級,目標價介於5美元至6美元。

摩根士丹利分析師Simeon Gutman維持持有評級,並將目標價從5美元上調至6美元。

Evercore分析師Oliver Wintermantel維持持有評級,並將目標價從4美元上調至5美元。

加皇資本市場分析師Steven Shemesh維持買入評級,並將目標價從5美元上調至6美元。

加皇資本市場分析師Steven Shemesh維持買入評級,並將目標價從5美元上調至6美元。

韋德布什分析師Seth Basham維持買入評級,並將目標價從5.5美元上調至6美元。

此外,綜合報道,$Petco Health and Wellness (WOOF.US)$近期主要分析師觀點如下:

寵物樂園採取的旨在增強業務的戰略舉措看起來很有前景,顯示出穩定的跡象。然而,被認爲風險/回報平衡較大,結果可能存在顯著的潛在變化。

寵物樂園的第三季度業績略高於預期,並且EBIT利潤率的提高表明公司成功的戰略,據一位分析師表示。儘管從2022年高峰時期急劇回落,但人們認爲在短期內,混合、市場份額壓力和公司特定因素將在2025年影響收益和股票表現。從更長遠的角度看,由於在吸引人的寵物行業中的優勢地位,公司被認爲是積極的。

該公司實現了又一個一貫的季度,以順序提高營收和努力提高利潤率爲標誌,導致EBITDA增長了13%。預計寵物樂園的穩健表現和利潤率進展將幫助股價縮小與同行的多重差距。

寵物樂園的第三季度業績超出了可比和EBITDA的預期,然而,其第四季度的指引略遜於預期。考慮到動態環境,第四季度的展望被認爲適當保守,但由於寵物樂園的以利潤爲先的策略似乎正在通過供應鏈節省和運營效率促進利潤率的提升,存在改善的潛力。

寵物樂園的第三季度更新看起來是有利的,但由於低於預期的第四季度指引、持續的有限可見性以及重大的持續任務,仍存在追求積極進取的猶豫。

以下爲今日4位分析師對$Petco Health and Wellness (WOOF.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。