The Personalis, Inc. (NASDAQ:PSNL) share price has fared very poorly over the last month, falling by a substantial 33%. The good news is that in the last year, the stock has shone bright like a diamond, gaining 155%.

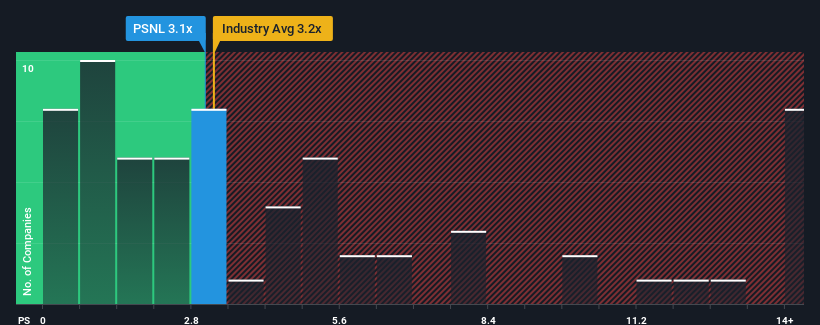

Even after such a large drop in price, it's still not a stretch to say that Personalis' price-to-sales (or "P/S") ratio of 3.1x right now seems quite "middle-of-the-road" compared to the Life Sciences industry in the United States, where the median P/S ratio is around 3.2x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

NasdaqGM:PSNL Price to Sales Ratio vs Industry December 6th 2024

What Does Personalis' Recent Performance Look Like?

Personalis certainly has been doing a good job lately as it's been growing revenue more than most other companies. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Keen to find out how analysts think Personalis' future stacks up against the industry? In that case, our free report is a great place to start.

How Is Personalis' Revenue Growth Trending?

Personalis' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 24%. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Turning to the outlook, the next three years should generate growth of 35% each year as estimated by the six analysts watching the company. With the industry only predicted to deliver 7.1% per annum, the company is positioned for a stronger revenue result.

With this in consideration, we find it intriguing that Personalis' P/S is closely matching its industry peers. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Key Takeaway

With its share price dropping off a cliff, the P/S for Personalis looks to be in line with the rest of the Life Sciences industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Looking at Personalis' analyst forecasts revealed that its superior revenue outlook isn't giving the boost to its P/S that we would've expected. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Before you take the next step, you should know about the 4 warning signs for Personalis that we have uncovered.

If these risks are making you reconsider your opinion on Personalis, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Personalis' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Personalis' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Personalis的市銷率對於一個預計只會實現適度增長的公司而言是非常典型的,重要的是,它的表現與行業板塊持平。

Personalis的市銷率對於一個預計只會實現適度增長的公司而言是非常典型的,重要的是,它的表現與行業板塊持平。