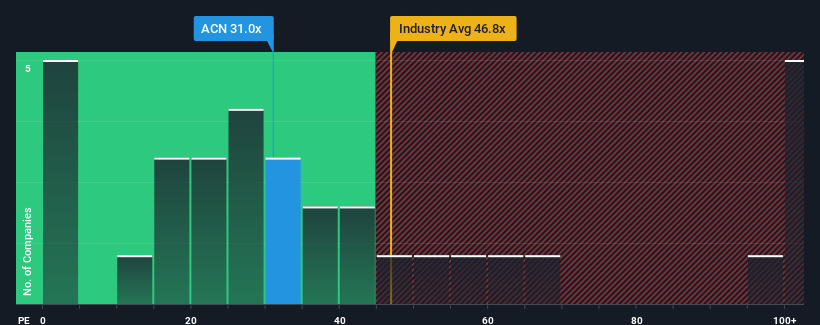

Accenture plc's (NYSE:ACN) price-to-earnings (or "P/E") ratio of 31x might make it look like a strong sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 19x and even P/E's below 11x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Accenture certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:ACN Price to Earnings Ratio vs Industry December 5th 2024 Want the full picture on analyst estimates for the company? Then our free report on Accenture will help you uncover what's on the horizon.

Is There Enough Growth For Accenture?

The only time you'd be truly comfortable seeing a P/E as steep as Accenture's is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 6.2% last year. The solid recent performance means it was also able to grow EPS by 25% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 11% per year during the coming three years according to the analysts following the company. With the market predicted to deliver 11% growth per year, the company is positioned for a comparable earnings result.

With this information, we find it interesting that Accenture is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Accenture currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. Right now we are uncomfortable with the relatively high share price as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Accenture with six simple checks.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 6.2% last year. The solid recent performance means it was also able to grow EPS by 25% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 6.2% last year. The solid recent performance means it was also able to grow EPS by 25% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

首先回顧一下,我們發現該公司去年成功將每股收益增長了6.2%。穩固的近期表現意味着過去三年內它也成功將EPS總體增長了25%。因此,我們可以開始確認該公司在此期間內實際上已經做了很好的增長收益工作。

首先回顧一下,我們發現該公司去年成功將每股收益增長了6.2%。穩固的近期表現意味着過去三年內它也成功將EPS總體增長了25%。因此,我們可以開始確認該公司在此期間內實際上已經做了很好的增長收益工作。