We Think That There Are Issues Underlying Workday's (NASDAQ:WDAY) Earnings

We Think That There Are Issues Underlying Workday's (NASDAQ:WDAY) Earnings

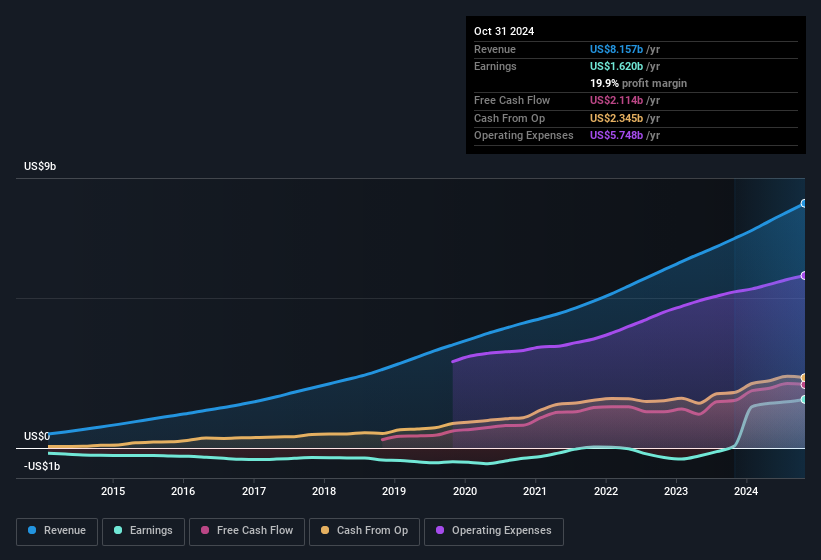

For the year to October 2024, Workday had an accrual ratio of -0.14. That implies it has good cash conversion, and implies that its free cash flow solidly exceeded its profit last year. To wit, it produced free cash flow of US$2.1b during the period, dwarfing its reported profit of US$1.62b. Workday's free cash flow improved over the last year, which is generally good to see. Importantly, we note an unusual tax situation, which we discuss below, has impacted the accruals ratio.

For the year to October 2024, Workday had an accrual ratio of -0.14. That implies it has good cash conversion, and implies that its free cash flow solidly exceeded its profit last year. To wit, it produced free cash flow of US$2.1b during the period, dwarfing its reported profit of US$1.62b. Workday's free cash flow improved over the last year, which is generally good to see. Importantly, we note an unusual tax situation, which we discuss below, has impacted the accruals ratio. Last week's profit announcement from Workday, Inc. (NASDAQ:WDAY) was underwhelming for investors, despite headline numbers being robust. We did some digging and found some worrying underlying problems.

上周Workday, Inc.(纳斯达克:WDAY)的利润公告让投资者感到失望,尽管表面数字相当强劲。我们做了一些挖掘,发现了一些令人担忧的潜在问题。

Examining Cashflow Against Workday's Earnings

审查Workday的现金流与盈利情况

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

许多投资者没有听说过现金流量的计提比率,但它实际上是衡量一个公司在给定期间的自由现金流(FCF)支持其利润能力的有用指标。计提比率从该期间的利润中减去FCF,并将结果除以公司在该时间内的平均营运资产。该比率告诉我们一个公司的利润超过了其自由现金流的多少。

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

因此,当公司的应计负债比率为负时,实际上是一件好事,但如果其应计负债比率为正,那就是一件坏事。虽然应计负债比率为正不是问题,表明某种程度的非现金利润,但高应计负债比率可以说是一件坏事,因为这表明纸面利润与现金流不匹配。因为一些学术研究表明,高应计负债比率往往导致利润较低或利润增长较少。

For the year to October 2024, Workday had an accrual ratio of -0.14. That implies it has good cash conversion, and implies that its free cash flow solidly exceeded its profit last year. To wit, it produced free cash flow of US$2.1b during the period, dwarfing its reported profit of US$1.62b. Workday's free cash flow improved over the last year, which is generally good to see. Importantly, we note an unusual tax situation, which we discuss below, has impacted the accruals ratio.

截至2024年10月的一年中,Workday的应计比率为-0.14。这表明其现金转换良好,并且自由现金流相较于去年的利润有了显著的超越。具体而言,其在此期间产生的自由现金流为21亿美元,远超其报告的16.2亿美元的利润。Workday的自由现金流在过去一年中有所改善,这通常是好的。重要的是,我们注意到一个飞凡的税务情况,下面将对此进行讨论,影响了应计比率。

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

这可能会让您想知道分析师对未来盈利能力的预测。幸运的是,您可以单击此处查看基于其估计的未来盈利能力的互动图表。

An Unusual Tax Situation

一种不寻常的税务情况

Moving on from the accrual ratio, we note that Workday profited from a tax benefit which contributed US$964m to profit. This is meaningful because companies usually pay tax rather than receive tax benefits. Of course, prima facie it's great to receive a tax benefit. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. While we think it's good that the company has booked a tax benefit, it does mean that there's every chance the statutory profit will come in a lot higher than it would be if the income was adjusted for one-off factors.

在关注应计比率的同时,我们注意到Workday受益于一项税收优惠,带来了96400万美元的利润。这是非常重要的,因为企业通常是支付税款而不是获得税收优惠。当然,从表面上看,获得税收优惠是件好事。然而,细节之处在于,这类优惠只会影响到记录的年份,通常是一次性的。如果税收优惠没有被重复,我们预计其法定利润水平会下降,至少在没有强劲增长的情况下。虽然我们认为公司获得了税收优惠是好事,但这确实意味着法定利润很可能会远高于如果收入调整了一次性因素后的水平。

Our Take On Workday's Profit Performance

我们对Workday利润表现的看法

In conclusion, Workday has strong cashflow relative to earnings, which indicates good quality earnings, but the tax benefit means its profit wasn't as sustainable as we'd like to see. Based on these factors, we think it's very unlikely that Workday's statutory profits make it seem much weaker than it is. Ultimately, this article has formed an opinion based on historical data. However, it can also be great to think about what analysts are forecasting for the future. At Simply Wall St, we have analyst estimates which you can view by clicking here.

总之,Workday的现金流相对于营业收入表现强劲,表明其盈利质量良好,但税收优惠意味着其利润并不像我们希望的那样可持续。基于这些因素,我们认为Workday的法定利润显得比实际情况要弱得多的可能性非常小。最终,本文基于历史数据形成了一个观点。然而,考虑分析师对未来的预测也是很棒的。在Simply Wall St,我们有分析师的预测估计,您可以通过点击这里查看。

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

在本文中,我们已经看到了一些可能损害利润数字作为业务指南的因素。 但是,如果您能够集中精力于细节,就会有更多的发现。 一些人认为高回报股本是优质业务的好迹象。 虽然这可能需要您进行一些研究,但您可能会发现此自由集合的公司拥有高回报股本,或此持股股票的股票列表 这个列表很有用。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。