Here's Why We Think HEICO (NYSE:HEI) Might Deserve Your Attention Today

Here's Why We Think HEICO (NYSE:HEI) Might Deserve Your Attention Today

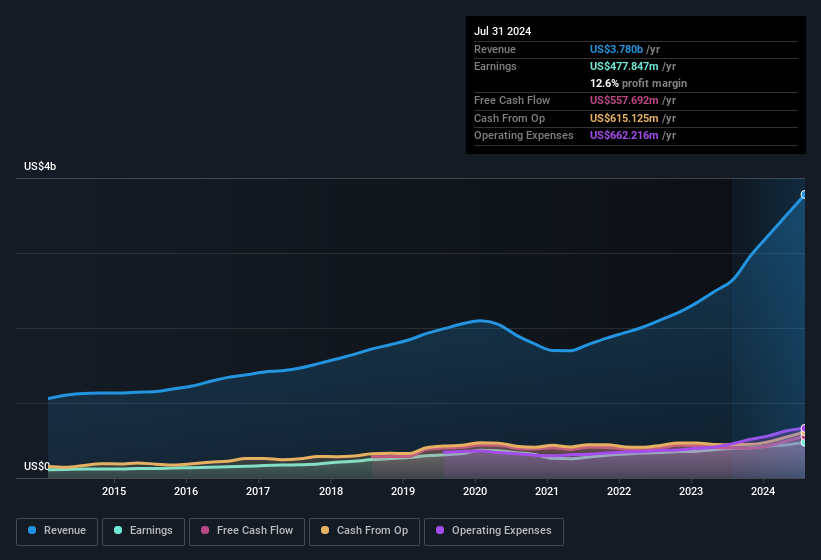

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While we note HEICO achieved similar EBIT margins to last year, revenue grew by a solid 43% to US$3.8b. That's a real positive.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While we note HEICO achieved similar EBIT margins to last year, revenue grew by a solid 43% to US$3.8b. That's a real positive. It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

对于许多投资者,特别是那些经验不足的人,即使这些公司亏损,也会购买有好故事买的股票。但正如彼得 · 林奇在《华尔街之上》中所说,“冷门股几乎从来没有回报”。亏损的公司可能会像资本的海绵一样行事,因此投资者应该小心,不要把好钱投在坏钱上。

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like HEICO (NYSE:HEI). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

如果这种高风险高回报的想法不适合您,您可能更感兴趣的是像HEICO(NYSE:HEI)这样盈利能力强、增长迅速的公司。现在这并不是说该公司提供了最佳的投资机会,但盈利能力是业务成功的关键组成部分。

How Quickly Is HEICO Increasing Earnings Per Share?

HEICO的每股收益增长速度有多快?

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. That means EPS growth is considered a real positive by most successful long-term investors. It certainly is nice to see that HEICO has managed to grow EPS by 18% per year over three years. So it's not surprising to see the company trades on a very high multiple of (past) earnings.

如果您认为市场甚至略显高效,那么从长期来看,您会期待一个公司的股价遵循其每股收益(EPS)的结果。这意味着EPS增长被大多数成功的长期投资者视为真正的利好。看到HEICO在过去三年每年成功增长18%的EPS确实很让人高兴。因此,看到公司以(过去)收益的很高倍数交易并不奇怪。

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While we note HEICO achieved similar EBIT margins to last year, revenue grew by a solid 43% to US$3.8b. That's a real positive.

核对公司增长的一种方法是观察其营业收入和利息税前利润(EBIT)毛利率的变化。尽管我们注意到HEICO的EBIT毛利率与去年相似,但营业收入实现了强劲的43%增长,达到了38亿美元。这是一个真正的利好。

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

下图显示了该公司底线和顶线随着时间的推移而发展的情况。点击图片以获取更精细的详细信息。

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of HEICO's forecast profits?

在投资中,正如在生活中一样,未来比过去更重要。为什么不查看一下HEICO预测利润的免费交互式可视化呢?

Are HEICO Insiders Aligned With All Shareholders?

海科航空内部人士是否与所有股东保持一致?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. Because often, the purchase of stock is a sign that the buyer views it as undervalued. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

一家公司内部人员对公司感兴趣总是引发一些好奇,许多投资者都在寻找内部人员将自己的钱投在对自己看好的公司。因为经常情况下,买入股票表示买方认为股票被低估了。当然,我们永远无法确定内部人员在想什么,我们只能评判他们的行动。

The US$436k worth of shares that insiders sold during the last 12 months pales in comparison to the US$2.0m they spent on acquiring shares in the company. This bodes well for HEICO as it highlights the fact that those who are important to the company having a lot of faith in its future. We also note that it was the Independent Director, Julie Neitzel, who made the biggest single acquisition, paying US$191k for shares at about US$263 each.

过去12个月内内部人士卖出的43.6万美元股票价值相形见绌,与他们以200万美元购买公司股票的金额相比显得微不足道。这对海科航空来说是个好兆头,因为它凸显了那些对公司重要的人对其未来充满信心。我们还注意到,独立董事朱莉·奈策尔进行了最大宗的单笔交易,以每股263美元的价格支付了19.1万美元购买股票。

The good news, alongside the insider buying, for HEICO bulls is that insiders (collectively) have a meaningful investment in the stock. Notably, they have an enviable stake in the company, worth US$4.6b. Coming in at 14% of the business, that holding gives insiders a lot of influence, and plenty of reason to generate value for shareholders. So there is opportunity here to invest in a company whose management have tangible incentives to deliver.

对于HEICO的看涨者来说,好消息是除了内部人士的买入,他们(集体)在这家股票中有着丰厚的投资。值得注意的是,他们在公司中拥有值得羡慕的46亿美元股权。占据公司14%的股份,这一持股让内部人士拥有很大的影响力,也有充分的理由为股东创造价值。因此,在这里有机会投资一家管理层具有明显激励的公司。

Should You Add HEICO To Your Watchlist?

您是否应将海科航空添加到您的自选名单?

You can't deny that HEICO has grown its earnings per share at a very impressive rate. That's attractive. Furthermore, company insiders have been adding to their significant stake in the company. Astute investors will want to keep this stock on watch. You should always think about risks though. Case in point, we've spotted 1 warning sign for HEICO you should be aware of.

您无法否认海科航空的每股收益增长速度非常令人印象深刻。这是很有吸引力的。此外,公司内部人士一直在增加他们在公司的重要股份。审慎的投资者将希望密切关注这支股票。然而,您应始终考虑风险。例如,我们已经发现了海科航空的一个警示信号,您应该注意。

Keen growth investors love to see insider activity. Thankfully, HEICO isn't the only one. You can see a a curated list of companies which have exhibited consistent growth accompanied by high insider ownership.

热衷于成长的投资者喜欢看到内部人员的活动。幸运的是,海科航空不是唯一一个。您可以看到一个经过筛选的公司名单,这些公司表现出稳定的增长并伴随着高内部持股。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

请注意,本文讨论的内部交易是指在相关司法管辖区中报告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。