Despite an already strong run, HubSpot, Inc. (NYSE:HUBS) shares have been powering on, with a gain of 28% in the last thirty days. The last 30 days bring the annual gain to a very sharp 42%.

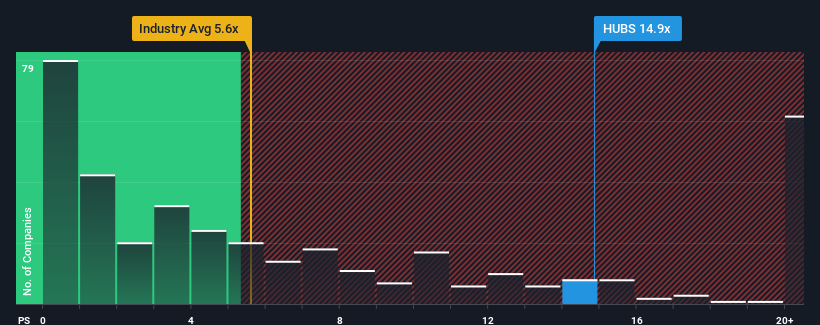

After such a large jump in price, HubSpot's price-to-sales (or "P/S") ratio of 14.9x might make it look like a strong sell right now compared to other companies in the Software industry in the United States, where around half of the companies have P/S ratios below 5.6x and even P/S below 2x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

NYSE:HUBS Price to Sales Ratio vs Industry December 2nd 2024

How HubSpot Has Been Performing

Recent times have been advantageous for HubSpot as its revenues have been rising faster than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think HubSpot's future stacks up against the industry? In that case, our free report is a great place to start.

How Is HubSpot's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like HubSpot's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 22% gain to the company's top line. The latest three year period has also seen an excellent 112% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 17% each year over the next three years. That's shaping up to be materially lower than the 21% per year growth forecast for the broader industry.

With this information, we find it concerning that HubSpot is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

The strong share price surge has lead to HubSpot's P/S soaring as well. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Despite analysts forecasting some poorer-than-industry revenue growth figures for HubSpot, this doesn't appear to be impacting the P/S in the slightest. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. At these price levels, investors should remain cautious, particularly if things don't improve.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for HubSpot that you should be aware of.

If these risks are making you reconsider your opinion on HubSpot, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should far outperform the industry for P/S ratios like HubSpot's to be considered reasonable.

There's an inherent assumption that a company should far outperform the industry for P/S ratios like HubSpot's to be considered reasonable.

人們普遍認爲,像HubSpot這樣的市銷率應遠遠超出行業才能被視爲合理。

人們普遍認爲,像HubSpot這樣的市銷率應遠遠超出行業才能被視爲合理。