Nature's Sunshine Products, Inc. (NASDAQ:NATR) shareholders would be excited to see that the share price has had a great month, posting a 25% gain and recovering from prior weakness. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 6.8% over the last year.

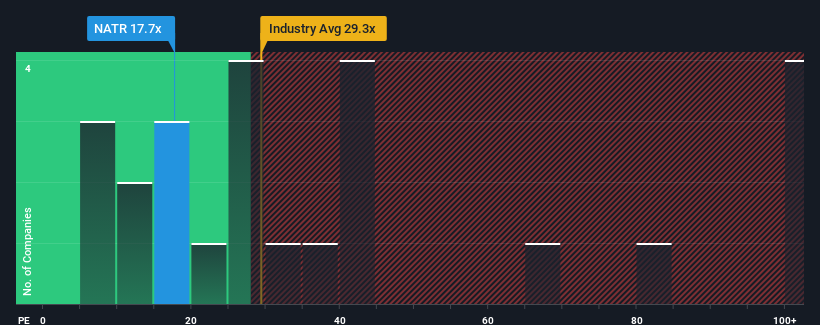

In spite of the firm bounce in price, there still wouldn't be many who think Nature's Sunshine Products' price-to-earnings (or "P/E") ratio of 17.7x is worth a mention when the median P/E in the United States is similar at about 20x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Nature's Sunshine Products certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

NasdaqCM:NATR Price to Earnings Ratio vs Industry November 30th 2024 Keen to find out how analysts think Nature's Sunshine Products' future stacks up against the industry? In that case, our free report is a great place to start.

How Is Nature's Sunshine Products' Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like Nature's Sunshine Products' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 115% gain to the company's bottom line. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 14% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to slump, contracting by 15% during the coming year according to the two analysts following the company. That's not great when the rest of the market is expected to grow by 15%.

With this information, we find it concerning that Nature's Sunshine Products is trading at a fairly similar P/E to the market. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the negative growth outlook.

What We Can Learn From Nature's Sunshine Products' P/E?

Nature's Sunshine Products' stock has a lot of momentum behind it lately, which has brought its P/E level with the market. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Nature's Sunshine Products' analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings are unlikely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Nature's Sunshine Products with six simple checks on some of these key factors.

If you're unsure about the strength of Nature's Sunshine Products' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should be matching the market for P/E ratios like Nature's Sunshine Products' to be considered reasonable.

There's an inherent assumption that a company should be matching the market for P/E ratios like Nature's Sunshine Products' to be considered reasonable.

有一個固有的假設,即公司應該像世紀陽光產品一樣匹配市場的市盈率,才能被認爲是合理的。

有一個固有的假設,即公司應該像世紀陽光產品一樣匹配市場的市盈率,才能被認爲是合理的。