We Ran A Stock Scan For Earnings Growth And Dover (NYSE:DOV) Passed With Ease

We Ran A Stock Scan For Earnings Growth And Dover (NYSE:DOV) Passed With Ease

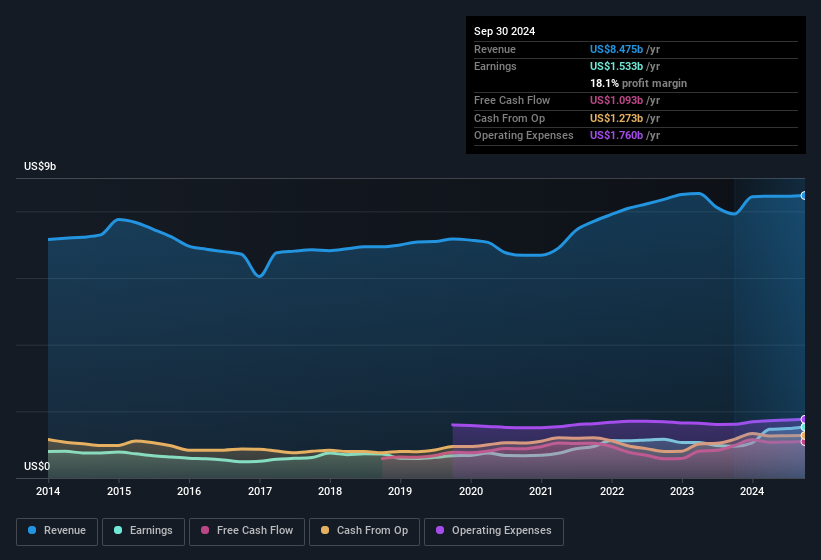

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Dover maintained stable EBIT margins over the last year, all while growing revenue 7.0% to US$8.5b. That's progress.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Dover maintained stable EBIT margins over the last year, all while growing revenue 7.0% to US$8.5b. That's progress. Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

投资者常常被发现'下一个大事'的想法所引导,即使这意味着购买没有收入,更别说利润的 '故事股票'。有时这些故事会蒙蔽投资者的头脑,让他们情感化地投资,而不是按公司基本面的优点投资。亏损型公司可以像资本的海绵一样,所以投资者应该小心,不要在错误的公司投入更多资金。

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Dover (NYSE:DOV). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

尽管处于科技股蓝天投资的时代,许多投资者仍然采取更传统的策略;在像都福集团(纽交所:DOV)这样的盈利公司中买入股票。尽管利润并不是投资时应考虑的唯一指标,但值得认可能够持续产生利润的企业。

How Fast Is Dover Growing?

都福集团的增长速度有多快?

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. That means EPS growth is considered a real positive by most successful long-term investors. Shareholders will be happy to know that Dover's EPS has grown 19% each year, compound, over three years. If growth like this continues on into the future, then shareholders will have plenty to smile about.

如果一家公司可以持续增长每股收益(EPS)足够长的时间,其股价最终应该会随之上涨。这意味着EPS增长被大多数成功的长期投资者视为真正的积极信号。股东们会高兴地知道,都福集团的EPS在过去三年里每年复合增长了19%。如果这样的增长在未来继续下去,股东们将会有很多值得高兴的事。

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Dover maintained stable EBIT margins over the last year, all while growing revenue 7.0% to US$8.5b. That's progress.

检查一家公司的增长的一个方法是查看其营业收入和息税前利润(EBIT)边际的变化。都福集团在过去一年中保持了稳定的EBIT边际,同时营业收入增长了7.0%,达到85亿美元。这是进步。

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

下面的表格显示了公司的营收和净利润如何随着时间的推移的变化。点击图表可以查看准确的数字。

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Dover's future profits.

你开车时不会盯着后视镜,所以你可能会更感兴趣这个免费的报告,展示了分析师对都福未来利润的预测。

Are Dover Insiders Aligned With All Shareholders?

都福内部人是否与所有股东保持一致?

Since Dover has a market capitalisation of US$28b, we wouldn't expect insiders to hold a large percentage of shares. But we are reassured by the fact they have invested in the company. Indeed, they have a considerable amount of wealth invested in it, currently valued at US$116m. While that is a lot of skin in the game, we note this holding only totals to 0.4% of the business, which is a result of the company being so large. So despite their percentage holding being low, company management still have plenty of reasons to deliver the best outcomes for investors.

由于都福的市场资本化为280亿美元,我们不会期望内部人士持有大量股票。但是我们放心的是,他们已经在公司投资。实际上,他们在公司的投资额相当可观,目前估值为11600万美元。尽管这在游戏中投入了不少,但我们注意到这仅占到业务的0.4%,这是由于公司规模过大。因此,尽管他们的百分比持有很低,公司管理层仍有许多理由为投资者提供最佳结果。

Does Dover Deserve A Spot On Your Watchlist?

都福值得在你的自选中占有一席之地吗?

If you believe that share price follows earnings per share you should definitely be delving further into Dover's strong EPS growth. Further, the high level of insider ownership is impressive and suggests that the management appreciates the EPS growth and has faith in Dover's continuing strength. The growth and insider confidence is looked upon well and so it's worthwhile to investigate further with a view to discern the stock's true value. You should always think about risks though. Case in point, we've spotted 4 warning signs for Dover you should be aware of, and 1 of them is significant.

如果你认为股价跟随每股收益,那么你绝对应该进一步深入了解都福强劲的每股收益增长。此外,高水平的内部人持股令人印象深刻,表明管理层重视每股收益的增长,并对都福未来的持续实力充满信心。增长和内部信心受到好评,因此进一步调查以辨别股票的真实价值是值得的。不过,你总是要考虑风险。举例来说,我们发现了4个你应该注意的都福的警告信号,其中一个是显著的。

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a tailored list of companies which have demonstrated growth backed by significant insider holdings.

总是有可能买入未增长收益并且内部人员不买入股票的股票表现良好。但是对于那些认为这些重要指数的人,我们鼓励您查看具有这些功能的公司。您可以访问定制列表,其中列出了已经展示出增长并得到内幕人员认可的公司。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

请注意,本文讨论的内部交易是指在相关司法管辖区中报告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。