Ramaco Resources, Inc. (NASDAQ:METC) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 27% in the last twelve months.

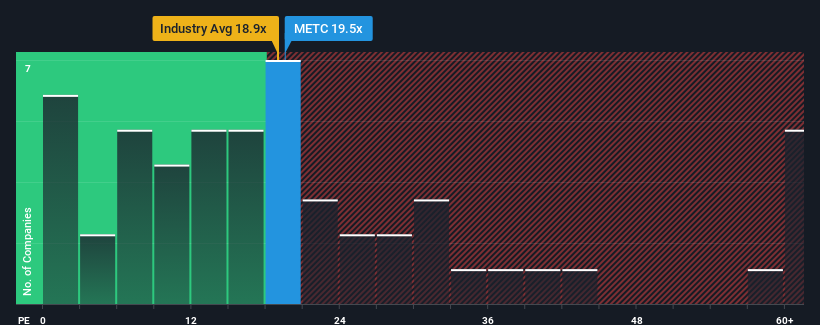

In spite of the firm bounce in price, there still wouldn't be many who think Ramaco Resources' price-to-earnings (or "P/E") ratio of 19.5x is worth a mention when the median P/E in the United States is similar at about 19x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Ramaco Resources could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

NasdaqGS:METC Price to Earnings Ratio vs Industry November 29th 2024 Want the full picture on analyst estimates for the company? Then our free report on Ramaco Resources will help you uncover what's on the horizon.

What Are Growth Metrics Telling Us About The P/E?

The only time you'd be comfortable seeing a P/E like Ramaco Resources' is when the company's growth is tracking the market closely.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 45%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 74% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 173% during the coming year according to the three analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 15%, which is noticeably less attractive.

With this information, we find it interesting that Ramaco Resources is trading at a fairly similar P/E to the market. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Key Takeaway

Ramaco Resources' stock has a lot of momentum behind it lately, which has brought its P/E level with the market. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Ramaco Resources currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

Before you settle on your opinion, we've discovered 2 warning signs for Ramaco Resources that you should be aware of.

Of course, you might also be able to find a better stock than Ramaco Resources. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The only time you'd be comfortable seeing a P/E like Ramaco Resources' is when the company's growth is tracking the market closely.

The only time you'd be comfortable seeing a P/E like Ramaco Resources' is when the company's growth is tracking the market closely.

唯一有可能接受像ramaco resources這樣的市盈率的情況是公司的增長緊密追蹤市場。

唯一有可能接受像ramaco resources這樣的市盈率的情況是公司的增長緊密追蹤市場。