Is Gogo (NASDAQ:GOGO) Using Too Much Debt?

Is Gogo (NASDAQ:GOGO) Using Too Much Debt?

Zooming in on the latest balance sheet data, we can see that Gogo had liabilities of US$97.0m due within 12 months and liabilities of US$661.0m due beyond that. Offsetting these obligations, it had cash of US$188.3m as well as receivables valued at US$64.8m due within 12 months. So it has liabilities totalling US$504.9m more than its cash and near-term receivables, combined.

Zooming in on the latest balance sheet data, we can see that Gogo had liabilities of US$97.0m due within 12 months and liabilities of US$661.0m due beyond that. Offsetting these obligations, it had cash of US$188.3m as well as receivables valued at US$64.8m due within 12 months. So it has liabilities totalling US$504.9m more than its cash and near-term receivables, combined. David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Gogo Inc. (NASDAQ:GOGO) does have debt on its balance sheet. But is this debt a concern to shareholders?

David Iben说得很好,'波动性并非我们关心的风险。我们关心的是避免资本的永久损失。' 当我们考虑一家公司有多大风险时,我们总是喜欢看看它对债务的运用,因为债务过载可能导致毁灭。 我们注意到Gogo Inc.(纳斯达克:GOGO)的资产负债表上确实有债务。 但这笔债务会让股东担心吗?

Why Does Debt Bring Risk?

为什么债务会带来风险?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

一般来说,只有在公司无法轻易偿还债务时,债务才会变成一个真正的问题,无论是通过筹集资本还是通过自身的现金流。如果情况变得非常糟糕,贷款人可以接管企业。然而,更常见(但仍然昂贵)的情况是,一家公司必须以低廉的股价稀释股东权益,以控制债务。当然,债务的好处是它通常代表廉价的资本,特别是当它取代了公司股权稀释,并具备以高回报率再投资的能力时。在我们考虑债务水平时,我们首先综合考虑现金和债务水平。

What Is Gogo's Net Debt?

什么是 Gogo 的净债务?

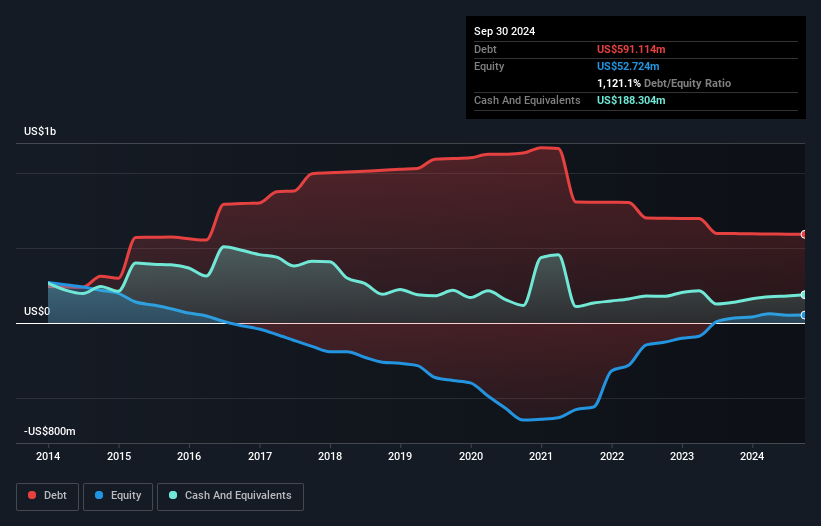

As you can see below, Gogo had US$591.1m of debt, at September 2024, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$188.3m in cash leading to net debt of about US$402.8m.

正如您下面所看到的,截至2024年9月,Gogo的债务为5,9110万美元,与前一年大致相同。 您可以单击图表以获取更详细信息。 另一方面,它有1,8830万美元的现金,从而形成了约4,0280万美元的净债务。

A Look At Gogo's Liabilities

认真审视gogo的负债情况

Zooming in on the latest balance sheet data, we can see that Gogo had liabilities of US$97.0m due within 12 months and liabilities of US$661.0m due beyond that. Offsetting these obligations, it had cash of US$188.3m as well as receivables valued at US$64.8m due within 12 months. So it has liabilities totalling US$504.9m more than its cash and near-term receivables, combined.

深入了解最新的资产负债表数据,我们可以看到Gogo在12个月内到期的负债为9700万美元,在此之后到期的负债为66100万美元。抵消这些义务的是,它有现金18830万美元,以及12个月内到期的应收账款为6480万美元。因此,它的负债总额为50490万美元,超过了其现金和短期应收账款的总和。

This deficit isn't so bad because Gogo is worth US$1.03b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

这个赤字并不算太糟,因为Gogo的价值为10.3亿美元,因此如果有需要,可能会筹集足够的资本来强化其资产负债表。但很明显,我们务必仔细检查它是否能够在不稀释股权的情况下管理债务。

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

我们通过将公司的净债务与其息税折旧摊销前利润(EBITDA)相除,并计算其息税前利润(EBIT)如何覆盖其利息费用(利息覆盖率)来衡量公司的债务负担相对于其盈利能力。因此,我们同时考虑债务的绝对数量以及所支付的利率。

Gogo has a debt to EBITDA ratio of 3.3 and its EBIT covered its interest expense 4.1 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Worse, Gogo's EBIT was down 22% over the last year. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Gogo's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Gogo的债务与EBITDA比率为3.3,其EBIT覆盖了其利息支出的4.1倍。这表明虽然债务水平相当可观,但我们不会说它们构成问题。更糟糕的是,Gogo的EBIT在过去一年下降了22%。如果收益继续按照这种轨迹发展,偿还债务将会比说服我们在雨中参加马拉松更为困难。在分析债务水平时,资产负债表是显而易见的起点。但最终能否维持健康的资产负债表前景,更多取决于未来的盈利。因此,如果您关注未来,可以查看这份展示分析师盈利预测的免费报告。

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Gogo produced sturdy free cash flow equating to 51% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

但是,我们的最终考虑也很重要,因为公司不能用纸面利润偿还债务;它需要冷硬现金。因此,我们显然需要查看EBIT是否导致相应的自由现金流。在过去三年中,Gogo产生了坚实的自由现金流,相当于其EBIT的51%,这正是我们所预期的。这笔冷硬现金意味着在需要时它可以减少债务。

Our View

我们的观点

We'd go so far as to say Gogo's EBIT growth rate was disappointing. But at least its conversion of EBIT to free cash flow is not so bad. Once we consider all the factors above, together, it seems to us that Gogo's debt is making it a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Gogo is showing 3 warning signs in our investment analysis , and 1 of those is significant...

我们认为gogo inc的EBIt增长率令人失望。但至少其将EBIt转化为自由现金流的能力并不差。综合考虑上述所有因素后,我们认为gogo inc的债务使其存在一定风险。有些人喜欢这种风险,但我们会谨慎考虑潜在的风险,因此我们可能更愿意减少其负债。当您分析债务时,资产负债表显然是需要关注的重点领域。但最终,每家公司都可能面临超出资产负债表之外的风险。请注意,在我们的投资分析中,gogo inc显示出3个警示信号,其中1个相当重要...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

如果在所有这些之后,您更感兴趣的是具有坚实资产负债表的快速增长公司,那么不要拖延,查看我们的净现金增长股票列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。