Freightos Limited (NASDAQ:CRGO) shares have had a really impressive month, gaining 58% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 32% over that time.

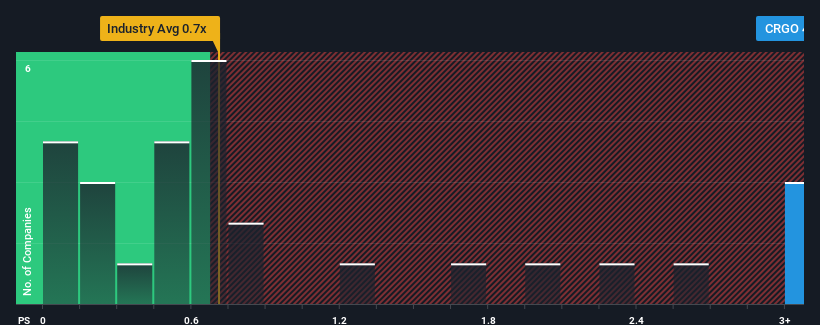

Following the firm bounce in price, when almost half of the companies in the United States' Logistics industry have price-to-sales ratios (or "P/S") below 0.7x, you may consider Freightos as a stock not worth researching with its 4.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

NasdaqCM:CRGO Price to Sales Ratio vs Industry November 28th 2024

What Does Freightos' Recent Performance Look Like?

Recent times have been pleasing for Freightos as its revenue has risen in spite of the industry's average revenue going into reverse. Perhaps the market is expecting the company's future revenue growth to buck the trend of the industry, contributing to a higher P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Freightos will help you uncover what's on the horizon.

Is There Enough Revenue Growth Forecasted For Freightos?

Freightos' P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 13%. This was backed up an excellent period prior to see revenue up by 102% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next three years should generate growth of 26% each year as estimated by the two analysts watching the company. That's shaping up to be materially higher than the 4.7% per annum growth forecast for the broader industry.

With this in mind, it's not hard to understand why Freightos' P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

Shares in Freightos have seen a strong upwards swing lately, which has really helped boost its P/S figure. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Freightos maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Logistics industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Freightos (2 can't be ignored!) that you should be aware of before investing here.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Freightos' P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Freightos' P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Freightos的市銷率將是一家預計將實現非常強勁增長,並且更重要的是,表現比行業要好得多的公司的典型水平。

Freightos的市銷率將是一家預計將實現非常強勁增長,並且更重要的是,表現比行業要好得多的公司的典型水平。